Stocks & Equities

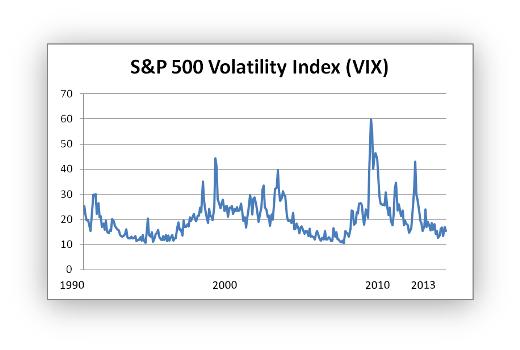

The following chart tells two stories. The first is that the deficit spending and debt monetization of the past few years has calmed the markets. Volatility (more accurately fear), as measured by the VIX index of S&P 500 options, has meandered back below 20, implying that most financial market players are pretty relaxed about the world’s near-term prospects.

….read more HERE

One final comment on TAPER-gate.

A number of strategists and analysts were surprised by Ben Bernanke and the Fed’s decision not to “Taper” the rate of QE money-printing at their September meeting.

However, this behavior from the Fed is not without precedent.

Back in the autumn of 2008 when the Fed first implemented the policy of Quantitative Easing, Ben Bernanke was very quick to assure markets that the Fed would begin to “Exit” from this policy in April of 2009. That helped to make this very experimental policy more palatable.

To “Taper” merely means to slow the rate. But “Exit” refers to a complete reversal of the policy; actually removing the printed money.

Well, April 2009 came and went despite Bernanke’s promise of an “Exit.” Now, here were are five years later, and we have yet to see a single dollar from QE1, QE2, or QE3 removed from the money supply.

This might provide some insight into the Fed’s actual intention to “Taper.” For years they have found reason after reason not to “Exit.” Expect the same with respect to “Tapering.” Over the last three months, Bernanke has become more vocal that “Tapering” is data dependent. Somehow, I sense that the data will tend to be interpreted to support the notion of continued Quantitative Easing. It is unlikely that the policy of QE will never really end until investors say that it has to by pushing market-determined interest rates significantly higher at some point in the future.

Continued Quantitative Easing is not necessarily always the recipe for sizable stock market gains, but it will have the effect of placing a floor under the market and limiting the amount of actual and implied future volatility. This should help to provide a comfortable environment for stock market investors, at least over the near- to mid-term.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results.

Richardson GMP Limited, Member Canadian Investor Protection Fund.

Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.

On Sept 18 markets had to rapidly “re-price” their anticipation of Fed policy when the Fed decided to NOT taper…stocks, bonds and commodities all jumped higher while the US Dollar tumbled. In last week’s blog I wondered if the “re-pricing” would be sustained…or if it would create a “blow-off” top…perhaps even producing a Key Turn Date…when a number of markets reverse direction at the same time signaling an important change in Market Psychology. As we go into October its beginning to look like we had a Key Turn Date on Sept 18/19…setting the stage for big moves ahead.

On Sept 18 markets had to rapidly “re-price” their anticipation of Fed policy when the Fed decided to NOT taper…stocks, bonds and commodities all jumped higher while the US Dollar tumbled. In last week’s blog I wondered if the “re-pricing” would be sustained…or if it would create a “blow-off” top…perhaps even producing a Key Turn Date…when a number of markets reverse direction at the same time signaling an important change in Market Psychology. As we go into October its beginning to look like we had a Key Turn Date on Sept 18/19…setting the stage for big moves ahead.

Here’s what happened since the “re-pricing” of Sept 18 and 19:

Gold: dropped as much as $70 over the next 3 days…rallied back some…closed last week $40 below the “re-pricing” highs.

DJIA: dropped as much as 500 points from the All Time Highs made following the Fed surprise…closed lower in 6 of the last 7 sessions…down 2.7%.

Euro and the Yen: surged higher on the Fed surprise…and pretty much sustained those gains at last week’s close.

CAD: traded to 3 month highs (98 cents) on the Fed surprise but closed last week below 97 cents.

WTI crude: Hit $108 on the Fed surprise…but closed at $103 last week, down $5.

Bonds: The US long bond had a huge 3 point range Sept 18…closing near its highs. Bonds gained another 1½ points last week to reach 2 months highs…with support from several sources… the Fed said the economy was too weak (bond bullish) for them to cut back on their stimulation (more bond buying)…they caught a “safe haven” bid as stocks were sold…and shorts were scrambling to cover after the big sell-off since May.

Potential market turmoil ahead:

Fed: Will or won’t they taper at the Oct 29/30 meeting…a strong employment report this coming Friday (Oct 4) could renew “taper talk.”

Fed: Who will replace Bernanke?

Gov’t: Facing a shutdown on Oct 1…acrimonious political theater…debt ceiling could be reached by mid-October…more acrimonious political theater.

Europe: Now that Merkel is re-elected what changes in Europe?

My short term trading:

In last week’s blog I wrote that stocks and/or gold could be sold short following their quick “Fed surprise” rallies…and that selling pressure in both markets could intensify if they broke below their pre Fed surprise levels. I didn’t want to buy the break in the US Dollar (I’m pre-disposed to be US$ bullish, but the chart pattern looked bearish) and I was neutral on bonds (I felt that a short covering rally was over-due but I could see much higher interest rates ahead.) I chose to short gold because it was already in a downtrend (for the previous 2 weeks, for the last year, for the last 2 years) rather than short stocks which were in an uptrend (for the previous 3 weeks, for the last year, for the last 4 years.)

This past Tuesday (Sept 24) gold traded as much as $70 below its Sept 19 highs…but quickly bounced back. I was thinking that gold might keep dropping…might take out the pre Fed surprise lows at $1291…but it didn’t…so I covered my short term trade with a $38 profit and went to cash…sitting on the sidelines waiting for the market to set up another short term trading opportunity.

I didn’t short the US stock market because it was in an uptrend and picking a top to a bull market that is making All Time Highs is clearly a case of trading what I think the market should be doing rather than what it is doing. I also didn’t short the US stock market because I felt that would be “doubling up” my short on gold…that they were essentially the same trade…that they were both reversing on the same change in Market Psychology. In previous blogs I’ve written that since May I’ve only traded the US stock market from the short side…with plenty of time spent sitting on the sidelines! I’m still pre-disposed to look for an opportunity to get short stocks…but at the moment I’m sitting in cash without a position.

My trading motivation and methodology are intertwined. I don’t like losing money but I’m willing to take risks…I just want to avoid taking stupid risks. So I develop an opinion about Market Psychology to help me gauge where a market is in terms of a bullish or bearish phase…within my selected time frame…and then I wait for a low risk opportunity to establish a position. If the market goes against me I get out with a small loss…if it goes my way I try to add to the trade. If it goes somewhat in my favor, like the gold trade above, but then stops I don’t mind closing the position and going to cash.

Futures and futures options are the best way to trade currencies, metals, stock indices and many other financial and commodity markets. Call 604 664 2842 to talk with Drew Zimmerman

Michael Campbell interviews Mark Leibovit of VRTRADER.COM who has been consistently ranked in the group of top market timers by TIMER DIGEST, including #1 US Market Timer of the Year, #1 Gold Timer of the year, #1 Intermediate Market Timer for the 10 year period ending in 2007.

Michael Campbell interviews Mark Leibovit of VRTRADER.COM who has been consistently ranked in the group of top market timers by TIMER DIGEST, including #1 US Market Timer of the Year, #1 Gold Timer of the year, #1 Intermediate Market Timer for the 10 year period ending in 2007.

Michael Campbell: We had the Fed Reserve come out about 10 days ago and really throw a monkey wrench into what the markets are doing. Did it make a big difference to you on how you look at the markets?

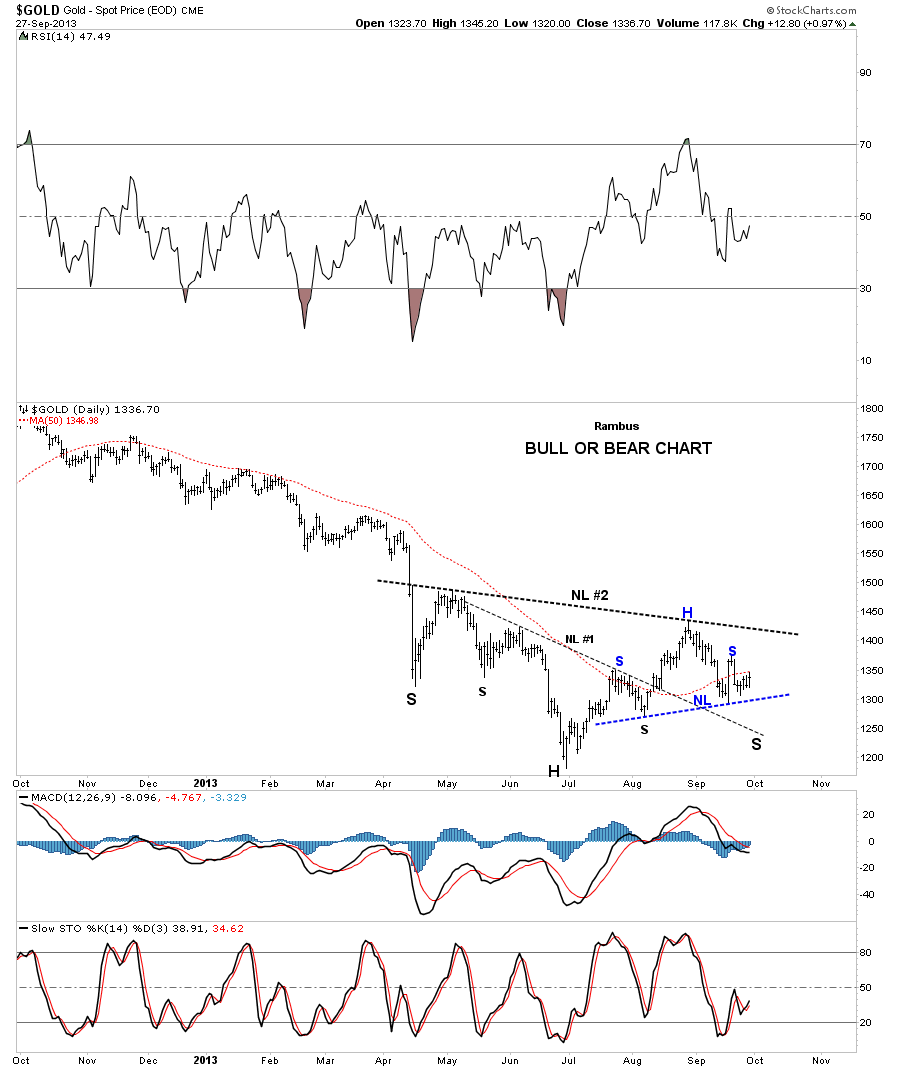

As far as the downside if we take out the $1275 -$1300. area from a practical point of view the risk is to those lows down at $1180.

In this Report I would like to look at the Chartology of the precious metals complex as this is either a consolation phase or as some think a bottoming formation is building out that will lead to the next bull market. In order to grasp what is really going on we need to look at all the possibilities and try to gain some perspective on which course of action the precious metals complex is likely to move in the short to intermediate time frame up or down.

The first chart I would like to show you is what I call my bull or bear chart. Many chartists are looking at the inverse H&S bottom that actually started to form back in April of this year, left shoulder. The head was formed during the late June low followed by the ten week rally to the September high around the 1435 area. As you can see there are two black necklines labeled #1 and #2 that shows a possible double inverse H&S bottom. In order to keep the symmetry alive gold would need to decline down toward the 1250 area where it could then form the second right shoulder. To confirm an inverse H&S bottom is in place gold would have to takeout the bigger neckline #2 around the 1400. This would be the bullish case for gold. The bearish argument for gold is that it is forming a H&S consolidation pattern as shown by the blue annotations. The flash rally that took everyone by surprise made the right shoulder high which quickly reversed direction. So at this point we have two inconclusive patterns to work with.

….17 more charts & commentary HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair