Currency

Canada added 11.9k jobs in September bringing our unemployment rate down to 6.9% The drop in the unemployment rate was not caused by a surge in jobs but instead the participation rate falling down to only 66.4%.

CAD Futures were up initially on the news however they are now trading back to unchanged on the day, showing the initial bullishness is erased by the poor secondary data and global conditions.

Drew Zimmerman

Investment & Commodities/Futures Advisor

604-664-2842 – Direct

604 664 2900 – Main

604 664 2666 – Fax

800 810 7022 – Toll Free

The commodity hedge funds are simply collapsing. This is one reason why you will also see the low in gold unfold. With all the ranting, screaming, claims of hyperinflation, threats of investigations, and prognostications that the dollar will end, not only has gold declined, but the appetite for investing in commodities in general.

The commodity hedge funds are simply collapsing. This is one reason why you will also see the low in gold unfold. With all the ranting, screaming, claims of hyperinflation, threats of investigations, and prognostications that the dollar will end, not only has gold declined, but the appetite for investing in commodities in general.

Clive Capital, who was once the largest Commodity hedge fund, announced it was winding down and returning $1 billion to investors after two years of losses. Being bullish on commodities (including gold) has not paid off in the last two years. Numerous hedge funds are closing. This has included Arbalet, Bluegold, Centaurus, and Fortress. Clive Capital wrote in their announcement to clients:

“We perceive there to be limited suitable opportunities at this point in the economic-demand and the commodity-supply cycles to enable us to utilise our directional, long volatility approach to generate the strong returns of the past.”

This is reflecting the collapse in liquidity and the general deflationary side of this implosion within the world economy. As the G20 continues to hunt money now on a global scale, they will force more and more capital into hiding and the economic contraction to become far worse the more they tax and seek to make illegal anyone with money outside their own country. They are lawyers – not economists or market traders. They only see their own side – power. They do not comprehend what they are doing to the world economy and how they are destroying the future for the next generation reflected in the more than 60% unemployment among the youth.

More From Martin:

Deflation + Inflation = Stagflation

Robot Manufacturing – Ed Note: 30 Seconds of video below to get the idea.

“Here is a fascinating look at auto manufacturing at Tesla. Reflections on “Real Problems” follow. I will tie the two seemingly unrelated ideas together.”

Please take that video into consideration when considering a rant from Paul Craig Roberts called The Real Crisis Is Not The Government Shutdown

Roberts claims the “The real crisis is that jobs offshoring by US corporations has permanently lowered US tax revenues by shifting what would have been consumer income, US GDP, and tax base to China, India, and other countries where wages and the cost of living are relatively low. On the spending side, twelve years of wars have inflated annual expenditures. The consequence is a wide deficit gap between revenues and expenditures.”

I will grant him that war-mongering is a huge problem. As for the loss of manufacturing jobs, I would point out that even China is losing them – to automation.

More importantly Roberts fails to understand the relationship between Fed policy and Nixon closing the gold window for the initial outsourcing. Roberts also fails to understand that unions wrecked GM and that GM is on the rebound because of wage reductions made in GM’s bankruptcy.

Gold and the Trade Deficit

For an explanation as to how gold is related to the trade deficit, please see Hugo Salinas Price and Michael Pettis on the Trade Imbalance Dilemma; Gold’s Honest Discipline Revisited

Roberts continues with his mostly-nonsensical rant:

The real crisis is the absence of intelligence among economists and policymakers who told us for 20 years not to worry about the offshoring of US jobs, because we were going to have a “New Economy” with better jobs.

As I report each month, not a single one of these “New Economy” jobs has appeared in the payroll jobs statistics or in the Labor Department’s projections of future jobs. Economists and policymakers simply gave away a good chunk of the US economy in order to enhance corporate profits. One result has been to create in the US the worst distribution of income of all developed countries and of many undeveloped ones.

In the scheme of things, the enhanced profits are a short-run thing, because by halting the growth in consumer income, jobs offshoring has destroyed the US consumer market.

Disability Fraud and the Demand for Goods

The demand for consumer goods is surprisingly high. And I believe that’s a bad thing. People ought to be more concerned about retirement, and less concerned about the latest toy or gadget, than they are.

Rampant fraud in collecting disability checks and welfare just may explain the lack of concern, or at least a healthy chunk of it.

I have been talking about disability fraud for five years, but mainstream media is just now investigating: Mainstream Media Finally Catches on to Disability Fraud: 60 Minutes Reports on “Disability USA”

The “real” problem is not offshoring, NAFTA, or declining real wages as Roberts suggests. Those are symptoms of problems not the “real problem”. However, I can easily name many real problems.

Ten Real Problems

- Fractional Reserve Lending

- The Fed

- Lack of a gold standard

- Deficit Spending

- Public unions

- Davis Bacon and prevailing wage laws drive up costs

- Disability fraud

- Warmongering

- Politicians get into bed with corporations, unions, and crony constituents

- Lack of incentives to hold down costs on medicare, food stamps, and entitlements

If you fix the first four or five, most of the rest of the problems will be fixed automatically.

Wage Inequality and Declining Real Wages

The primary reason for wage inequity is the Fed’s inflationary boom-bust practices. In addition, public unions and untenable pension obligations drive up costs (and taxes).

As I have stated dozens of times, inflation benefits those with first access to money (the banks and the already wealthy).

Three Key Reads On Who Benefits From Inflation

- Top 1% Received 121% of Income Gains During the Recovery, Bottom 99% Lose .4%; How, Why, Solutions

- Reader Asks Me to Prove “Inflation Benefits the Wealthy” (At the Expense of Everyone Else)

- Illusion of Prosperity: Deflating the American Dream; No Recovery in “Real” Income

Ironically, “onshoring” is now the buzzword. Thanks to robotics, some manufacturing has returned to the US (but the jobs didn’t, and won’t).

When it comes to “real” problems, Roberts really misses the boat.

By Mike “Mish” Shedlock

“The rate suppression that QE has imposed on developed countries since 2009 triggered a search for yield that flooded emerging economies with short-term ‘hot’ money.”

~ Stephen Roach, former chairman of Morgan Stanley Asia

Dear Mountaineers,

According to Moody’s, the consequences of a US “shutdown” would be negligible for growth in the U.S., and the debt ceiling “will be raised under certain conditions, but should not propel the U.S. into a bankruptcy situation”. As I write this letter, this no worries stance is shared by most analysts. And, financial markets largely reflect this view as well. So far, in financial markets, it’s been pretty much a non-event.

For instance, one might expect US interest rates to start rising in light of America slipping and sliding towards default. Reuters, on Monday, October 7th, reported that “The three main credit rating agencies have all warned, in varying degrees, the United States rating could be cut should it hit an expected October 17 deadline when Washington is set to run out of cash, endangering its ability to pay its debt.”

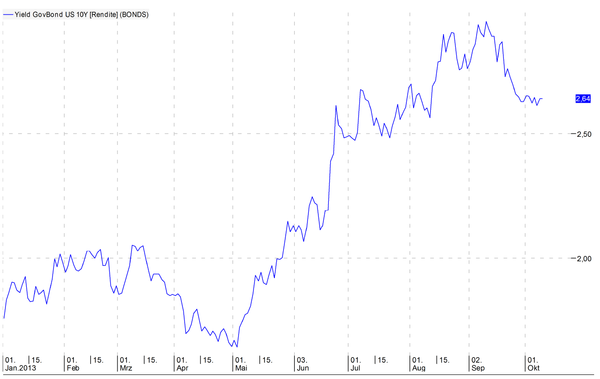

Yield on 10Y US government bond, Oct. 9th 2013

Source: BFI Wealth Management, VWD Group data source

Yet, so far, with exception of some short-term rates, yields have not budged. As depicted in the chart above, the yield on 10-year Treasury paper has even come down over the past few weeks and, at this point, is moving sideways.

What’s interesting about the chart above is the fact that the 10Y yield shot up starkly starting in May, and has been dropping since early September. As we all know, this was the market’s prompt and loud response to the tapering comments made by Ben Bernanke. When the US Fed so much as whispers the possibility of tapering off, bond and stock markets react immediately, in worry of QE being removed. Equally, when Mr. Bernanke removes his threat of rehab, i.e. taking away the “cheap money drug”, financial markets go back into party mode, and the recovery story is back on track.

What sticks out here, really, is the fact that the Fed runs the show. Being the print manager of the world’s (currently still) number one reserve currency, apparently, entails all the power. What the US Treasury and politicians do in Washington appears largely irrelevant. As long as the Fed continues printing money to the tune of some USD 85 billion a month, the party may go one, irrespective of the Obama-Boehner showdown.

When trust is lost

So, as investors, can we all sit back, relax and watch the show in amusement and indifference? I’m not so sure. The credibility of the US dollar, its Treasury papers, and the US economy overall, to this day, are still very solid.

However, trust is a fickle thing. The concerns of investors around the world are growing. They are starting to put pressure on financial markets as we move closer toward October 17th. More and more analysts are concerned that, unless the U.S. government is able to show the rest of the world a desire to move forward and resolve its issues – at least until the next budget and debt ceiling will arrive with certainty – the trust and confidence in the US leadership, the US economy and its currency could take a severe hit. The potential consequences of a loss of trust in the world’s leading economy and number one currency should not be underestimated.

While I too am of the opinion that a last-minute resolution or back-door maneuver will most probably be found –we’ve been here before, several times over – one should not count out that OTHER possibility. In fact, warnings and official alerts abound. If this gets ugly, the “how could I have known?” excuse will not easily fly.

IMF world economic outlook and warnings

In its latest World Economic Outlook, the International Monetary Fund (IMF) warns that the world will “settle into a subdued medium-term growth trajectory” unless leading economies change course to improve prospects for recovery.

Launching its twice-yearly forecasts, the IMF trimmed its predictions of global expansion for 2013 and 2014, with the downgrade as a result of weaker prospects in emerging economies. The IMF still expects a “modest acceleration of activity” next year, led by advanced economies and particularly the United States with an expected 2.6% growth next year, “so long as US politicians manage to resolve the government shutdown and extend the debt ceiling.”

“Activity will move into higher gear as fiscal consolidation eases and monetary conditions stay supportive,” the IMF said. In other words, if the US doesn’t take away the drugs, we’ll be able to enjoy an extended party. But, the IMF did also very clearly warn of dire consequences if the drugs and punchbowl were removed, i.e. if the US government shutdown morphs into a failure to raise the debt ceiling next week.

Olivier Blanchard, the fund’s chief economist, said it would lead to “an extreme fiscal consolidation and [would] almost surely derail the US recovery” with wider global disruption. “If there was a problem lifting the debt ceiling, it could well be that what is now a recovery would turn into a recession or even worse,” he added.

Of course, the global economy has been on drugs – cheap and cheaper money – for over three decades now. Money creation and quantitative easing has turned into an addiction and getting off that addiction will not happen without pain. In fact, at this point, we are sailing into uncharted territory in terms of scope and scale of the monetary and fiscal imbalances we face.

US fiscal and monetary profligacy unveiled by the Treasury

If you live under the assumption that the US government operates in a fiscally sustainable manner and that the US economy is growing strongly, you need to re-adjust your compass. If the latest shutdown spectacle hasn’t already changed your mind, possibly a recent report from the U.S. Treasury Department will help.

The report is nothing short of an official admission and confirmation of the decades’ long woeful mismanagement of U.S. economic, fiscal and monetary policy. The assumption widely held is that the political impasse will likely be resolved in the 11th hour just as it has been during prior showdowns. But, the report describes a broader background and its implications.

The U.S. Treasury Department warns that the economy could plunge into a downturn worse than the Great Recession if Congress fails to raise the federal borrowing limit and the country defaults on its debt obligations. A default could cause the nation’s credit markets to freeze, the value of the dollar to plummet and U.S. interest rates to skyrocket, according to the Treasury report released Thursday.

Keeping a cool head in this situation is probably the right decision. We’ve seen these kinds of shutdowns and showdowns before over and over again. Economically, and in financial markets, these episodes generally have had little impact. Raising the debt ceiling has become the thing to do regularly.

Yet, the intensity of quantitative easing has increased over the past few years. Keeping markets in party mode requires more and more intervention, more and more debt. There’s no turning back and no way out without a painful rehab.

What to expect? Can game theory give us some answers?

Can game theory be employed to explain, or even better “de-code”, the budget showdown in Washington? Game theory, as defined inWikipedia, is the study of strategic decision-making. More formally, it is “the study of mathematical models of conflict and cooperation between intelligent rational decision-makers”.

In an interesting interview with Professor Daniel Diermeier, a specialist in game theory in politics, whether game theory can be used is addressed. He compares the uncompromising positions in the current “budget game” with the situation found during the Cuba Crisis in 1962, when America and the Soviet Union almost unleashed a nuclear war.

The situation is also comparable to a game of chicken, where two cars are driving at each other and the first one to swerve away loses. Swerving is worse for you than not swerving, but if nobody swerves then you die. Similarly, John Boehner doesn’t want to “swerve” (pass a clean continuing resolution or debt ceiling increase) and Obama doesn’t want to “swerve” (sign a CR that defunds Obamacare, or sign a non-clean debt ceiling increase). But if neither swerves, then the shutdown continues and/or we default.

A rational strategy in any case would be to give in and make way because there is much more to lose than there is to win. But if one assumes that the other guy will do that for rational reasons, then you better keep your course. Therefore, to act or appear to act rational in this kind of showdown is a risk in itself, especially if you want to win.

All bets are off

Professor Diermeier’s interview is interesting indeed. However, unfortunately, we can’t say that game theory will give us any certainty or help recognize the “chicken” in this game, at least not in advance.

All bets are off. Beware!

Sincerely,

Frank Suess

About Frank Suess & Switzerland Based Mountain Vision

Frank R. Suess, CEO & Chairman of BFI Capital Group, is the chief editor of Mountain Vision. An advocate of free-market principles, Mr. Suess frequently speaks and writes on global economic, geo-political and financial matters, spanning from the US to China. Mr. Suess started his career in management consulting, having held senior positions with Andersen Consulting and PricewaterhouseCoopers, where he consulted a number of international corporations. He has an MBA, cum laude, from the Haas School of Business, UC Berkeley, CA, USA and a Bachelor´s degree in Finance, magna cum laude, from Saint Mary´s College, Moraga, CA, USA.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair