In our previous essay, we examined the situation in crude oil in different time horizons. Back then, we wrote that the short-term situation had improved as crude oil had broken above both short-term resistance lines on relatively high volume and had come back above the previously-broken medium-term support line and the long-term one.

In our previous essay, we examined the situation in crude oil in different time horizons. Back then, we wrote that the short-term situation had improved as crude oil had broken above both short-term resistance lines on relatively high volume and had come back above the previously-broken medium-term support line and the long-term one.

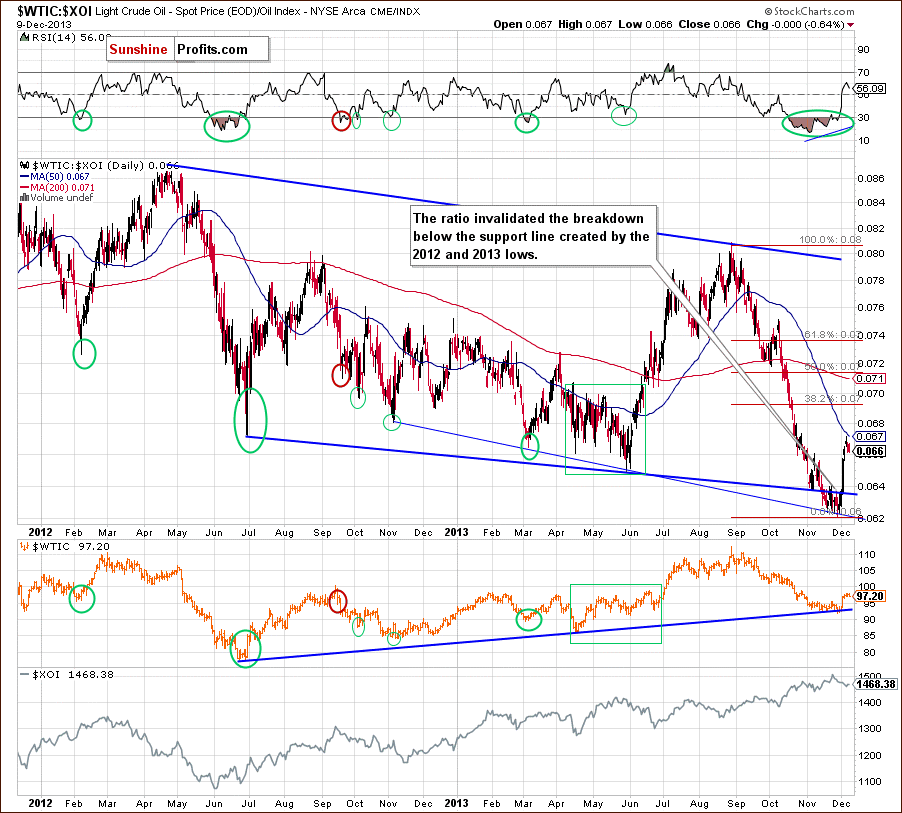

In the following days, crude oil extended gains and approached its 200-day moving average. What’s next? Is the worst already behind oil bulls and we will see further improvement? Before we try to answer these questions, we’ll examine three interesting ratios to see if there’s anything on the horizon that could drive crude oil higher or lower in the near future. Let’s start with the oil-to-oil-stocks ratio (charts courtesy by http://stockcharts.com).

At the end of October, the ratio declined and broke below the long-term declining support line created by the 2012 and 2013 lows. Additionally, the WTIC:XOI ratio verified the breakdown, which was a strong bearish signal. In our previous Oil Investment Update we wrote that as long as the breakdown below the bold blue support line was not invalidated, another downswing couldn’t be ruled out.

Looking at the above chart, we see that the ratio reached the next long-term support line (marked with the thin blue line on the previous chart) and rebounded sharply in the previous week. In this way, the ratio invalidated the breakdown below the support line based on the 2012 and 2013 lows, which is a strong bullish sign.

Last week, the ratio reached its 50-day moving average and reversed the course – similarly to what we saw in April, May and June. However, we should keep in mind that back then, new lows in ratio didn’t trigger a fresh low in crude oil. Therefore, if history repeats itself once again, we may see lower values of light crude in near future, but another big move lower doesn’t seem likely.

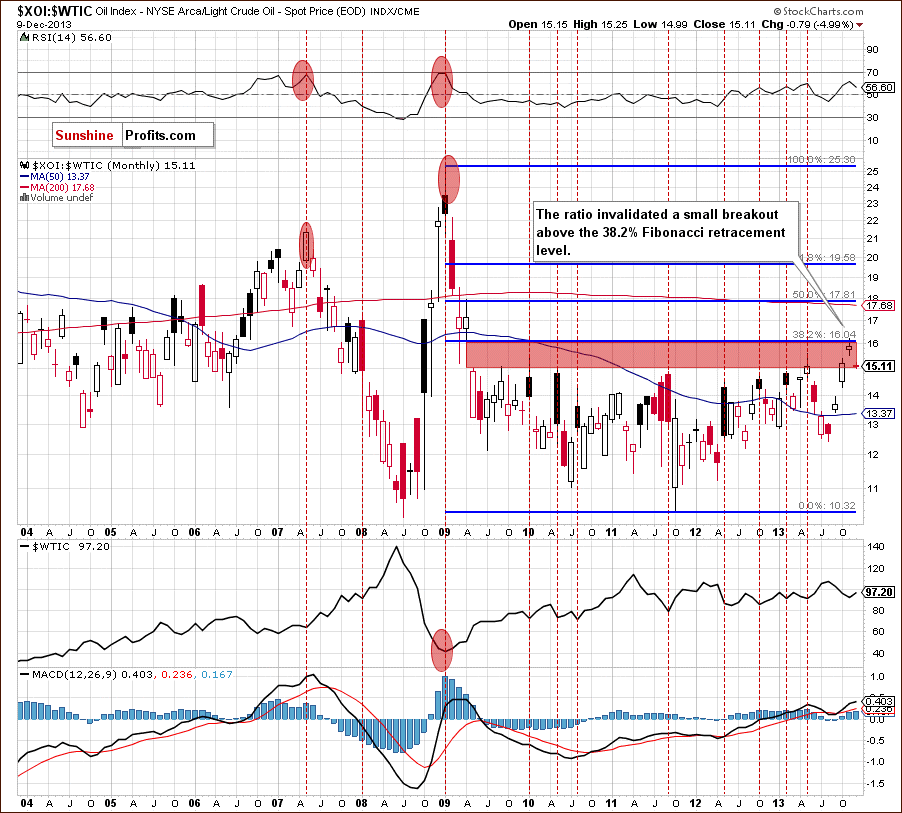

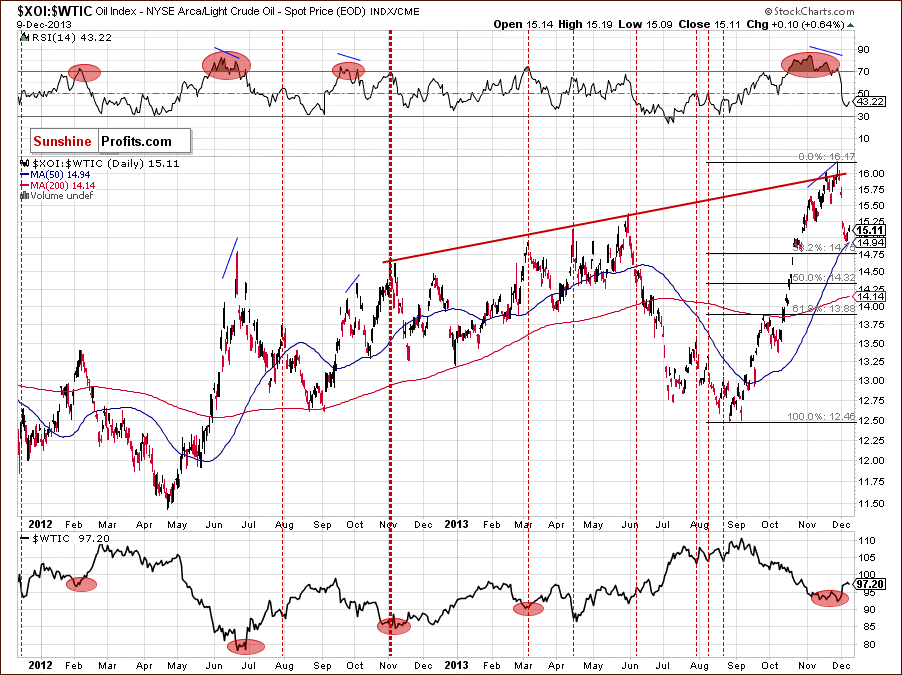

Having discussed the above, we’ll examine the oil-stocks-to-oil ratio. What impact could it have on future oil moves? Let’s start with the long-term chart.

Looking at the above chart, we see that the ratio reached the 38.2% Fibonacci retracement level (based on the entire 2009-2011 decline) and invalidated a small breakout above this strong resistance level, which was a bearish signal. This circumstance triggered a downswing, which took the ratio to the lower line of the gap between the April 2009 low and May 2009 high (marked with the red rectangle), which is not supporting further growth. From this perspective, the implications for oil are bullish.

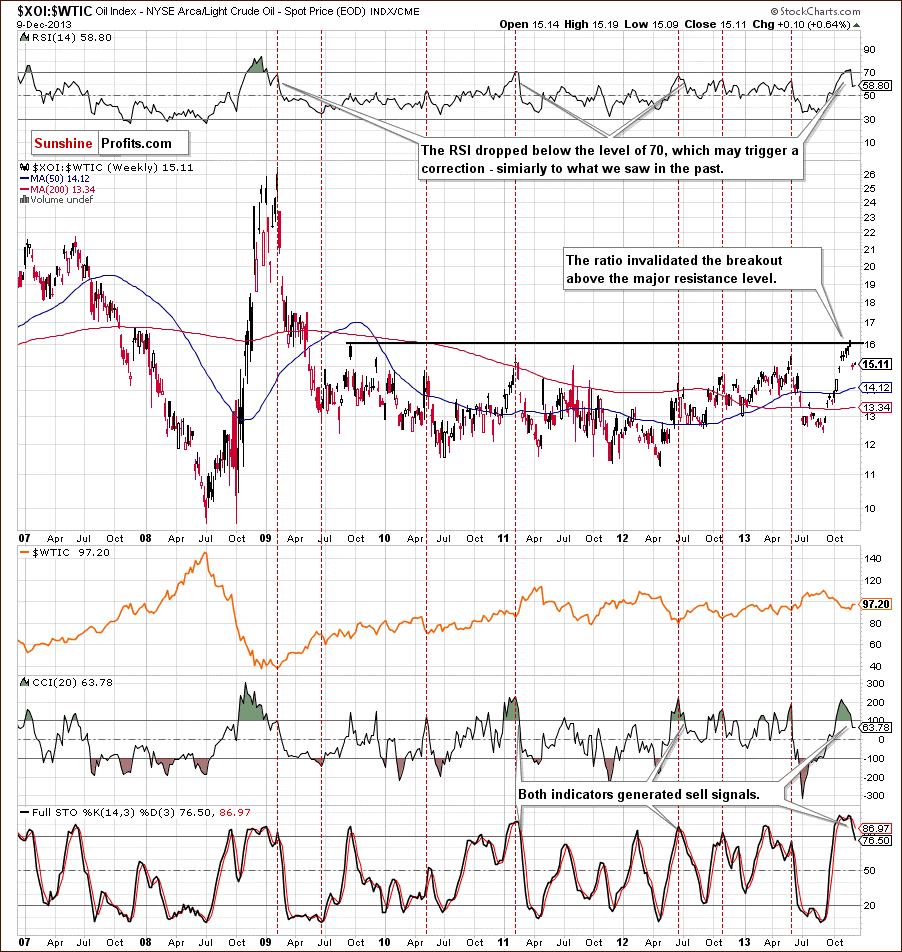

Now, let’s zoom in on our picture and examine the weekly chart.

After an invalidation of the breakout above the resistance level created by the September 2009 high, which is slightly below the 38.2% Fibonacci retracement (marked on the previous chart), the ratio declined, which triggered an upswing in crude oil. Additionally, the RSI dropped below the level of 70, which suggests further deterioration in the ratio. We saw similar situations in the past and in all previous cases such circumstances had a positive impact on the price of light crude.

When we factor in the position of the CCI and the Stochastic Oscillator, we clearly see that both indicators generated sell signals, which is another bearish signal. From this perspective, the implications for crude oil are also bullish.

Now, let’s check the short-term outlook.

After an invalidation of the breakout above the resistance level created by the September 2009 high, which is slightly below the 38.2% Fibonacci retracement (marked on the previous chart), the ratio declined, which triggered an upswing in crude oil. Additionally, the RSI dropped below the level of 70, which suggests further deterioration in the ratio. We saw similar situations in the past and in all previous cases such circumstances had a positive impact on the price of light crude.

When we factor in the position of the CCI and the Stochastic Oscillator, we clearly see that both indicators generated sell signals, which is another bearish signal. From this perspective, the implications for crude oil are also bullish.

Now, let’s check the short-term outlook.

Looking at the above chart, we see that last week the ratio bounced off the medium-term rising resistance line based on the November 2012 and May 2013 highs (marked with the red line) and declined, which was in perfect tune with an upswing in crude oil.

With this downward move, the ratio reached its 50-day moving average and approached the 38.2% Fibonacci retracement level. This strong support zone triggered a corrective upswing in the recent days, which preceded a decline in light crude. Taking into account the fact that the correction is still shallow, we may see further improvement in the ratio and deterioration in crude oil.

When we take a closer look at the chart above, we notice that earlier this year we had similar situation in April. At that time, although we saw a corrective upswing in the ratio, it didn’t pushed light crude to a new low. If history repeats itself, we may see further improvement in crude oil after a corrective downswing.

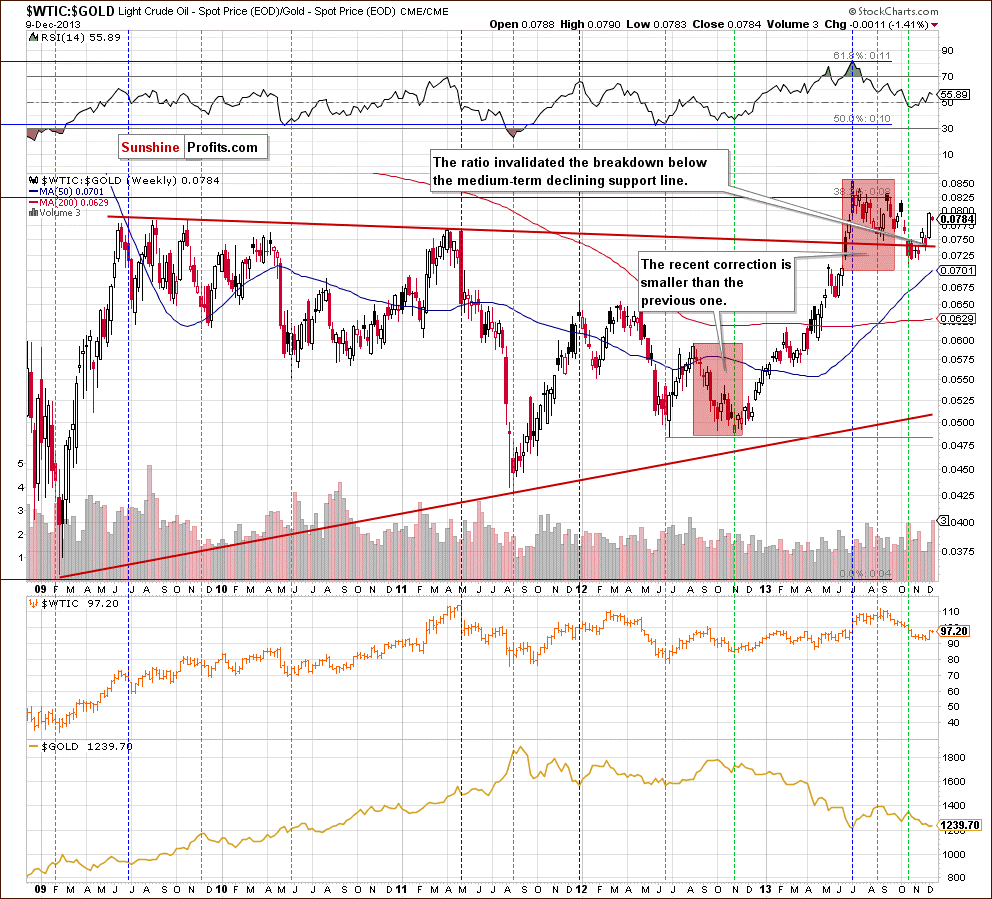

Before we finish this section, we would like to focus on the oil-to-gold ratio.

As you can see on the weekly chart, the ratio’s 2012 low was in tune with the bottom of a correction in crude oil. In November 2012, the ratio declined to its previous low, which triggered a corrective move in light crude. After that, we saw a post-double-bottom rally, which supported higher prices of crude oil.

Looking at the above chart, we see that the ratio’s 2013 top wasn’t in perfect tune with light crude’s 2013 high. However, when we take a closer look, we notice that the ratio’s September high was visibly lower than the previous one. Meanwhile, crude oil was trading near its 2013 high. This negative divergence between the ratio and the price of light crude was a negative sign and resulted in a decline in the following weeks.

With this downward move, the ratio dropped below long-term declining support line, which was a bearish sign. However, as it turned out in recent weeks, the breakdown was invalidated, which is a bullish signal for light crude.

Additionally, the recent correction is smaller than the previous one (August-November 2012), which suggests that another move to the upside is quite likely. As mentioned earlier, the rising ratio has had a positive impact on the price of crude oil since the beginning of the year. We can assume that higher values of the ratio will likely support the price of light crude.

What’ interesting, earlier this year the rising ratio had a negative impact on the price of gold. The ratio’s 2013 high was in tune with gold’s low in July. After that, this negative correlation between the ratio and gold pushed the yellow metal higher. There was a short period of time (in September), when they both dropped together, however, as it turned out, it was just a temporary phenomenon and the October decline in the ratio triggered an upward move in gold.

As you can see on the above chart, the negative correlation between the ratio and gold remains in place at the moment. Since the beginning of November the rising ratio has pushed the yellow metal lower and it seems that if this relationship remains in place in the coming days/weeks, we will likely see further deterioration in gold.

Summing up, the WTIC:XOI ratio invalidated the breakdown below the support line based on the 2012 and 2013 lows, which is a positive factor supporting the bullish case.

When we factor in the long-, medium- and the short-term XOI:WTIC charts, we clearly see that the ratio invalidated breakouts above a strong resistance zone created by the long-, medium- and short-term lines. This is another strong positive signal for oil bulls. On top of that, after discussing the situation in the oil-to-gold ratio, we can assume that the implications for crude oil are also bullish and further growth in crude oil is just around the corner.

About the Author

Nadia Simmons

Nadia is a private investor and trader, dealing in stocks, currencies, and commodities. Using her background in technical analysis, she spends countless hours identifying market trends, major support and resistance zones, breakouts and failures. In her writing, she presents complex ideas with clarity that enables you to easily understand market changes, and profit on them.

You can read Nadia’s analyses at SunshineProfits.com where she publishes her articles on gold and crude oil trading.