Bonds & Interest Rates

While the Fed’s decision to taper back its monthly asset purchase program to $75 billion has received a lot of attention, many have overlooked the news out of China.

The seven-day repurchase rate was up to a six-month high of 7.6% in Shanghai on Friday. It closed at 7.06% on Thursday. The People’s Bank of China [PBoC] injected money through short-term liquidity operations on Thursday.

We already saw a severe credit crunch in China back in June, and some are worried that we’re going to see a repeat of that.

Hedge fund manager Jim Chanos described this week’s run up in money market rates as “a bit of a banking crisis,” in a CNBC interview.

Read more: http://www.businessinsider.com/chinese-interest-rates-are-spiking-again-2013-12#ixzz2o0jVR5MD

With all the excitement over the Fed’s Taper of QE3 yesterday, it is beginning to dawn on bond market investors that someone will need to come in and pick up the slack in demand caused by the Taper. In January, there will be $5 billion in Treasury bonds and $5 billion in mortgage-backed bonds that would be normally scooped up by the Fed that will need to find a buyer.

When the Fed began QE3, Treasury bonds were on the cusp of entering a secular bear market after enjoying a secular bull market for the previous three decades (see the charts above). However, because it was early (and because investors weren’t listening to our warnings!), investors were still piling into bonds and bond mutual funds. It was hard to break a habit that had been so fruitful for 30 years.

As a result, at the beginning of QE3, the Fed was essentially “crowding out” relatively enthusiastic bond buyers.

Now, 16 months after the Fed starting buying mortgage-backed bonds and 12 months after the Fed started buying longer-term Treasuries, investors are transitioning out of these areas and into equities and other higher-yielding investments. Besides being lured by better returns elsewhere, who wants to buy a 10-year Treasury and get hammered as market rates really only have one way to go?

The bond market vigilantes have already begun to make an appearance, selling longer-dated bonds this morning rather than holding on to them into January when it might require an even higher yield to entice very reluctant investors to soak up the $10 billion in excess supply.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results.

Richardson GMP Limited, Member Canadian Investor Protection Fund.

Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.

With yesterday’s news of the Fed’s decision to Taper the pace of QE3, markets and economies that have benefitted the most are jittery.

The Fed countered the Taper decision with an announcement that they are likely to ignore their previous threshold target for unemployment and keep their Zero Interest Rate Policy (ZIRP) for longer than expected. This was likely the main reason for many equities markets rising. ZIRP can be viewed as a longer-term source of liquidity and was enough to counter the reduction in shorter-term liquidity (the Tapering of QE).

The problem for emerging markets such as India and China is that the benefits from the ZIRP policy had long since faded. They had become passively reliant upon the immediate potency of Quantitative Easing. This was the high-octane fuel that instantaneously drove a number of international property bubbles and convenient current-account surpluses as capital rushed in. (The irony is that earlier this year India and Brazil were complaining about too much excess liquidity and capital rushing into their economies).

Initially, the emerging markets’ problems resulting from less QE might not seem that serious. However, these areas, and especially China, have been a critical component to the global economy. Without their economic growth, it is unlikely that the North American economy would have grown much at all recently.

The unintended consequences of a Taper might be more than what the Fed bargained for.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results.

Richardson GMP Limited, Member Canadian Investor Protection Fund.

Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.

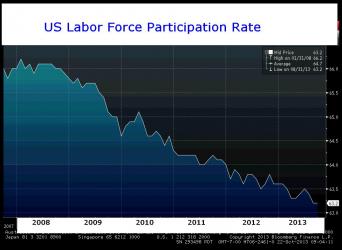

Here they are: the most important charts of the year.

Here they are: the most important charts of the year.

We asked our favorite portfolio managers, strategists, analysts, and economists across the Street for the charts that they deem the most important right now, and this is what they sent us.

Much of the focus is on the 10-year Treasury yield — where does it go, and what is the read-across for other financial markets around the globe? Many are focused on the stock market as well, the consensus being that indices will rise to new highs again in 2014.

But there are a lot of other things going on as well.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair