Personal Finance

In this week’s issue:

- Weekly Commentary

- Strategy of the Week

- Stocks That Meet The Featured Strategy

Stockscores Market Minutes Video

Some traders only want to look at the market once a week. You can do this by seeking stocks making good chart breaks on the three year weekly chart. This week, Tyler shows how to set up the Market Scan to find these stocks plus he provides his regular market analysis for the last time in 2013. View the video by clicking here.

Things You Must Do To Be Successful in 2014

2013 was a Beta year for the market. That means that the large cap stocks all went up and you made good profits if you simply owned the index. It was one of those rare difficult years to beat the market because the overall market did so well.

I expect that 2014 will require a lot more stock picking acumen. Investors are going to have to seek out the real leading individual stocks that can beat the market.

Here are five things that all investors and traders, whether long or short term, must do to beat the indexes in 2014.

Understand Reward for Risk

Most traders focus on the stock but you will be far more successful if you focus on the reward for risk profile of the trade. Risk is the difference between your entry and stop loss price. Reward is the difference between a profitable exit and the entry price. The tighter you can make your stop with lowering your probability of success, the higher the reward for risk ratio can be. Seek out trades that have a lot more upside potential than downside risk.

Focus on Abnormal Behavior

The best way to beat the market is to trade on inside information. Most of us don’t get quality inside information but it is not that hard to follow those that do. When there is significant fundamental change underway in a company, the stock will often trade abnormally. Prove it to yourself by looking at the stocks that made big gains last year. You will see that most of these market beating trends started with abnormal price action.

Learn to Read Chart Patterns

Most market beating stocks start with abnormal activity but not all abnormal activity leads to market beating trends. The important qualifier is the chart pattern. Stocks making abnormal activity out of predictive chart patterns have a good chance of going in to market beating trends.

Limit Losses, Let Profits Run

Imagine you do 10 trades. On five of them, you lose $100. On three of them, you make $100. On the final two, you make $1000 each. After 10 trades you have made a very good profit because you limited the size of your losses and let your profits run.

Ignore Public Information

Public information is useless because it is already priced in to the stock. It may be interesting, it may make you feel good about the stock that you own but it has no value to your investment decision. In fact, it may be destructive because we often fall in love with the public story, causing us to hold on to losing stocks with the “hope” that the stock will turn around.

STOCKS THAT MEET THE FEATURED STRATEGY

1. T.HSE

Money is starting to flow back to the Energy sector, Husky’s chart is breaking out this week to four year highs after spending most of 2013 trading sideways below $32 resistance. Historical yield is 3.66%

2. T.PPL

I featured T.PPL earlier this week to readers of the Tradescores.com daily newsletter, it has continued higher since and looks likely to continue its long term upward trend after building a base for the past 7 months. Historical yield is 4.59%

References

- Get the Stockscore on any of over 20,000 North American stocks.

- Background on the theories used by Stockscores.

- Strategies that can help you find new opportunities.

- Scan the market using extensive filter criteria.

- Build a portfolio of stocks and view a slide show of their charts.

- See which sectors are leading the market, and their components.

Disclaimer

This is not an investment advisory, and should not be used to make investment decisions. Information in Stockscores Perspectives is often opinionated and should be considered for information purposes only. No stock exchange anywhere has approved or disapproved of the information contained herein. There is no express or implied solicitation to buy or sell securities. The writers and editors of Perspectives may have positions in the stocks discussed above and may trade in the stocks mentioned. Don’t consider buying or selling any stock without conducting your own due diligence.

It might have gone against the conventional wisdom to see the markets trade higher on the basis that the US Federal Reserve will begin, come January, to be less accommodative to the US economy, but it’s not exactly as if the markets have had a perfectly rational last few years. Amidst one of the shakiest recoveries from the greatest recession to plague the US economy since the Great Depression, we continue to see equity markets trader higher as all the disbelievers missed out on the seventh greatest annualized gain in the American stock markets since World War II. No question, it was the US Federal Reserve’s influence on long term borrowing rates that bestowed confidence in American consumers, and nonetheless fueled this American recovery, but as the Fed begins to adapt their stimulus measures to adequately reflect the necessities of this continued recovery, we can be certain the party’s not over yet.

Ben Bernanke, in his final press conference as the Chairman of the US Federal Reserve, assured investors of one thing, and that was that the Fed will continue to adapt to the needs of the economy. And just as easily as they could trim asset purchases by 10 billion a month equally split between Treasury bonds and mortgage back securities, they could increase by 10 billion as well. But as we at Border Gold have argued in past newsletters, the taper of the fed’s asset purchases was very much an inevitable occurrence; moreover, it is absolutely not to be confused with the end of an era of easy money policies in the months and years to come.

Ben Bernanke, in his final press conference as the Chairman of the US Federal Reserve, assured investors of one thing, and that was that the Fed will continue to adapt to the needs of the economy. And just as easily as they could trim asset purchases by 10 billion a month equally split between Treasury bonds and mortgage back securities, they could increase by 10 billion as well. But as we at Border Gold have argued in past newsletters, the taper of the fed’s asset purchases was very much an inevitable occurrence; moreover, it is absolutely not to be confused with the end of an era of easy money policies in the months and years to come.

And as the easy money policies will continue the biggest influence on the market will be near zero short term interest rates, controlled by the Federal Funds Rate. Offered in the form of forward guidance, Bernanke made clear in his policy statement that rates will remain low “well past the time that the unemployment rate declines below 6-1/2 percent.” And that low of emergency level interest rates will be the fuel to the fire for the markets. It makes sense for the stock markets to be able to trade higher, almost in relief to the fact the world’s largest economy is no longer so desperately in need of such extraordinary stimulus. But it is the caveat that the highly accommodative economic environment will remain in place.

As the Berkley Economist Barry Eichengreen phrases it, a reduction “by $10bn a month is best dismissed as a taper in a teapot… $10bn of monthly security purchases are a drop in the bucket for a central bank with a $4tn balance sheet.” And in fact, by Bernanke beginning the taper, he began the very seamless hand off to Janet Yellen to fulfill the role of an accommodative central banker. This is as the markets can now digest the milestone that a measure once dubbed “QE Infinity” has the possibility of coming to an end.

***

A Note on Gold:

Following what was a supposed short covering rally with the rest of the market given the Fed’s decision to taper, gold immediately sold off heading for that June low of 1180 US/oz. Thursdays close on the Comex, below 1200 US/oz. was the yellow metals lowest in three years’ time. From a technical stand 1180 stands out as an important number, but as this market faces tax loss selling pressure going into year end precious metal markets are giving an indication that they are in the process of forming a bottom in Q1 of 2014.

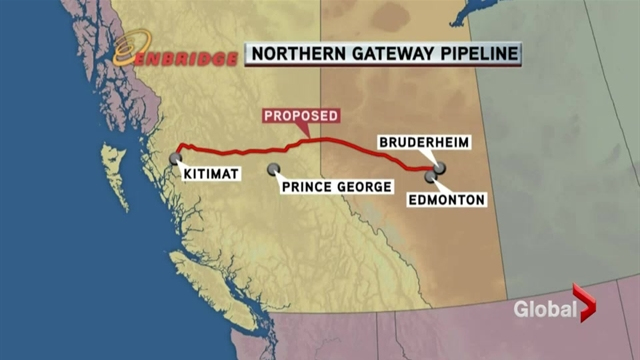

The Northern Gateway Pipeline Gets Green Light from Review Panel

The Northern Gateway Pipeline Gets Green Light from Review Panel

Without a doubt the Western Canadian energy patch has faced its challenges over the past few years. With no access to international markets and severely constrained transportation infrastructure into the United States, Canadian crude oil and natural gas trades at a substantial discount to international prices.

On Thursday, a key milestone was passed with respect to connecting Canada’s Oil Sands with buyers in Asian. The Joint Panel responsible for reviewing the Northern Gateway Project proposal issued their final report and recommended to the federal government that the pipeline be approved, subject to 209 specific conditions, which include the pipeline developer having $950 million in liability coverage and “unfettered access” to $100 million within 10 business days of a large spill. The ultimate fate of the project is now in the hands of the federal government which has 180 days to make their (yay or nay) decision.

At this point, it seems almost certain that the federal government will approve the Northern Gateway project with the allowed time frame. The economic argument is virtually undebatable. 98% of Canadian crude exports are sent to the United States who may not be a reliable customer over the next decade. Technological advancement has allowed our only energy customer to access unconventional oil and gas reserves which were previously uneconomic and the International Energy Agency expects the U.S. to be energy independent by 2020. Canadian companies have also had serious difficulties building the much needed infrastructure which is required to access U.S. markets. KeyStone XL, which would connect Canadian oil reserves to refineries in Texas, has faced unending regulatory delay and we feel little reason to be confident that a decision will be made in the near term. The federal government claims to understand the importance of diversifying Canada’s energy exports and have been supporters of Northern Gateway since the project was first proposed.

Even with final approval from the federal government almost a certainty, we don’t anticipate that the contentious battles over the project with end…rather they will likely intensify. The environmental movement will continue to fight against the Northern Gateway and any Oil Sands development at all costs. But another potential battle could be against British Columbia’s provincial government who have vowed to support the project only if five specific conditions are met. These conditions include an environmental review, world-leading response and prevention systems, appropriation liabilities and responsibilities in the event of a spill, and addressing Aboriginal and First Nations rights. However, these four conditions, at least on paper, are unlikely to be sticking points. It is the fifth condition, that British Columbia share in the economic benefits of the pipeline, which may cause a little more political entanglement. BC Premier Christy Clark has vowed to stop the pipeline if all five of these conditions are not met, but it is uncertain if she has the power as approval of the project appears, at least technically, to be a federal decision.

Regardless of the battles that ensue, it is highly likely that most of the players will eventually reach their consensus and the project will proceed largely as planned. The importance and potential benefits of the pipeline seem too important to ignore and both the federal and BC provincial governments have expressed their commitment to resource development. Accessing international markets would be a monumental step for the Canadian energy sector and would undoubtable open up a wide range of investment opportunities for Canadian investors.

|

KeyStone’s Latest Reports Section |

Disclaimer | ©2013 KeyStone Financial Publishing Corp.

Regards,

Jenny McConnell,

Administrative Assistant/Office Manager

Many times in our previous essays we have written that if you want to be an effective and profitable investor, you should look at the situation from different perspectives and make sure that the actions that you are about to take are really justified. Therefore, at the beginning of the month we examined gold and silver mining stocks to find out what kind of impact they could have on precious metals’ future moves. Back then, we concluded that the medium-term outlook for gold was bearish and mining stocks seemed to be leading gold lower. To make sure that our assumptions were correct, we decided to check the chart featuring gold’s price from the non-USD perspective and also from the European perspective. You could read the conclusions in our essay from Dec. 6, 2013.

A week ago we introduced you to 3 signs of gold’s upcoming decline. At that time we wrote in the summary:

(…) the medium-term outlook for gold remains bearish and it seems that we might see another sizable downswing shortly.

In the following days, after the essay was posted, gold, silver and mining stocks reversed and started their recent declines. Day by day, we saw lower values of gold, silver and mining stock indices. With this downward move, the yellow metal, the HUI Index and the AXU Index declined below their December’s lows (to be precise: at the same time silver dropped to slightly above its previous low).

Taking these circumstances into account, you are probably wondering whether the recent declines will continue or not. Although we saw a small rebound in the early European session, we clearly see that the precious metal sector remains weak.

As we emphasized in our previous essays, many times in the past the situation in the U.S. dollar and the euro gave us important clues about future precious metals’ moves. Therefore, today we’ll examine the US Dollar Index (from many perspectives) and the Euro Index to see if there’s anything on the horizon that could drive the precious metal market higher or lower in the near future. We’ll start with the medium-term USD Index chart (charts courtesy by http://stockcharts.com).

Looking at the above chart, we see that earlier this week we had a similar situation to the one that we saw last week. Just like a week ago, the USD Index broke below the medium-term support line based on the February 2012, September 2012 and January 2013 lows (the bold black line) and the lower medium-term line based on the September 2012 and the January 2013 lows (the thin black line). However, once again this deterioration was only temporary. The dollar quickly rebounded and invalidated the breakdown below both medium-term support/resistance lines, which is a sign of strength and a bullish factor. From this perspective, there was no true breakdown and the trend remains up.

Let’s check the short-term outlook.

On the above chart, we see that earlier this week, the USD Index tried to break above its horizontal support line based on the June low without a positive result. These circumstances triggered a sharp decline on Wednesday – just before the Fed released its statement. However, the greenback quickly reversed course when the Federal Reserve announced that it will start winding down its stimulus program (small, but still) and rallied above the 80.5 level.

With this upswing, the U.S. dollar broke above the declining short-term resistance line. Although, the USD Index declined in the following hours and came back below both resistance lines, it turned out on the following day that this small deterioration was temporary. On Tuesday, the greenback extended its rally and moved higher breaking above both resistance lines once again. Taking this fact into account, we can conclude that the outlook remains bullish and that it could be the case that the decline is already over and that another rally in the US Dollar is just starting.

Let’s now take a look at the long-term Euro Index chart. (larger view click on image or HERE)

The first thing that catches the eye on the above chart is the target area, which was reached once again.

In the previous week, the European currency almost reached the October high. Back then, it seemed that further growth was limited, not only because of this resistance level, but – even more importantly – because of the long-term declining resistance line based on the 2008 and 2011 highs (in terms of weekly closing prices). As a reminder, this strong resistance line successfully stopped growth in October and triggered a sharp decline. Additionally, at that time, a similar situation preceded a local top in precious metals. On top of that, previous tops (in 2008 and then in 2011) were followed by major declines in the precious metals sector. If history repeats itself, we may see similar price action in this situation.

Looking at the above chart, we clearly see that earlier this week the Euro Index reversed course after reaching a strong resistance zone and declined below the level of 137. What’s most interesting, precious metals followed that decline, which suggests that we’ll likely see further deterioration in the PM’s sector – similarly to the one seen in the past.

Please take a moment to compare the euro’s performance in the past few weeks with the performance of the precious metals sector (lower part of the above chart).

Let’s now take a look at the medium-term Euro Index chart.

Looking at the above chart, we see that the Euro Index climbed once again this week and reached its very strong resistance zone created by the previous 2013 high and the short-term rising support line based on the July and September lows. As you see on the weekly chart, the European currency didn’t manage to break above these levels, which triggered a sharp decline and pushed the euro slightly above the 38.2% Fibonacci retracement level based on the Nov.-Dec. rally. From this perspective, the outlook for the coming weeks is bearish.

Having discussed the above, let’s take a look at our Correlation Matrix to find out how all this can translate to precious metals and mining stock prices.

Basically, the short-term numbers don’t tell us much at this time when we look at them directly, but can tell us something if we look a bit beyond them.

The correlation between the USD Index and the precious metals sector is slightly positive in the 30-day column (and even moderately significant in the case of the mining stocks), which tells us that in the past 30 days PMs and the USD Index have moved on average in a similar direction. However, this was the case when they both declined. When the USD moved higher (this week), metals and miners declined even more. This is a very bearish combination – whatever the USD does, the precious metals sector seems to either decline modestly or strongly.

Once we know the relationship between the U.S. currency and the precious metal sector, let’s check the current situation in gold.

(Larger click image or HERE)

In our essay on gold from Dec. 6, 2013 we wrote the following:

(…) earlier this week we saw a major change on the above chart as gold broke below the rising long-term support line (…) the implications are bearish, especially that the RSI indicator is currently not oversold – it’s above 30 and well above its previous 2013 lows. Back in 2008, the RSI indicator moved close to its previous lows when the final bottom was in. In this case we would need to see much lower gold prices to have RSI close to the 20 level. The next stop for gold is at its 2013 low, slightly above $1,170. It seems to us, however, that this will not be the final bottom for this decline, we expect the final one to form close to $1,100, possibly even at $1,050.

Last week, we saw a very temporary move above the previously-broken rising long-term support line, which was followed by another decline. In our previous Premium Update, we wrote that if gold was not able to hold above this line despite a decline in the USD Index, then it was truly a weak market and quite likely to decline much more.

Looking at the above chart, we see that earlier this week we had such price action. Gold didn’t manage to successfully climb above the rising long-term support line (not to mention staying above it), which triggered a sharp decline. With this downward move, the yellow metal not only declined below last week’s low, but also slipped below the level of $1,200. These circumstances clearly show the weakness of the buyers and it seems that the previous 2013 low will be reached quite soon.

The exact target for gold is quite difficult to provide. For silver and mining stocks there are, respectively: combinations of strong support levels, and a major support in the form of the 2008 low. In the case of gold, there are 4 support levels that could stop the decline and each of them is coincidentally located $50 below the previous one starting at $1,150: $1,150, $1,100, $1,050, and $1,000.

Summing up, the current situation in both currencies suggests that we are likely to see further deterioration in the Euro Index and improvement in the USD Index in the near future. Taking these facts into account and combining them with the current relationship between the U.S. dollar and the PMs, we can conclude that the implications for the precious metal market are bearish. Please note that the exact target for gold is quite difficult to provide based on the gold chart alone. While it’s likely that the final bottom will form below $1,150 and above $1,000 (or at least not much below this level), if we want to get a more specific price projection, we should use other techniques, especially those which worked in mid-2013 when the previous gold’s low was formed.

Thank you for reading.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief

Tools for Effective Gold & Silver Investments – SunshineProfits.com

Tools für Effektives Gold- und Silber-Investment – SunshineProfits.DE

* * * * *

About Sunshine Profits

Sunshine Profits enables anyone to forecast market changes with a level of accuracy that was once only available to closed-door institutions. It provides free trial access to its best investment tools (including lists of best gold stocks and silver stocks), proprietary gold & silver indicators, buy & sell signals, weekly newsletter, and more. Seeing is believing.

Disclaimer

All essays, research and information found above represent analyses and opinions of Przemyslaw Radomski, CFA and Sunshine Profits’ associates only. As such, it may prove wrong and be a subject to change without notice. Opinions and analyses were based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are believed to be accurate, Przemyslaw Radomski, CFA and his associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Mr. Radomski is not a Registered Securities Advisor. By reading Przemyslaw Radomski’s, CFA reports you fully agree that he will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Przemyslaw Radomski, CFA, Sunshine Profits’ employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

Rosenberg thinks the U.S. economy will surprise to the upside next year.

Gluskin Sheff’s David Rosenberg, who has been turning increasingly bullish, has published his 2014 outlook.

In fact, the title of his note is “The Year of the Horse: The one that’s about to break out of the gate.”

Here’s a brief summary of his ten major calls for 2014:

- There is more upside potential in 2014 than downside risks. Rosenberg thinks in 2014, the “upside macro surprise shifts from the UK to the U.S.” 1984, 1994, and 2004 ended up being surprise years, and Rosenberg writes that investors should “beware of all years that end with a ‘4’, since they “all fit this bill of economic acceleration.”

- The stock market suggests that economic growth will improve in 2014. The market is seen as a leading indicator of growth. In the last 60 years, real GDP growth has always been positive when the S&P 500 climbed 60%. Any surprise in growth will be to the up side.

- Fiscal headwinds will subside and business spending could emerge as the key catalyst for growth next year. 2013 was rough with the “early year tax bite, the sequestering and the government shutdown.” But things are picking up. “The deceleration to 0% productivity growth, which has a direct link to profit margins, will finally incentivize the business sector to invest organically in their own operations with belated positive implication for capes growth.”

- The U.S. economy does not suffer from secular stagnation. The economy had so far been held back by household and federal government balance sheet repair. Rosenberg expects the economy to surprise “to the high side after a prolonged period of unsatisfactory post-recession growth.” But he points out that “the upside for next year from a business or economic perspective as opposed from a market standpoint is considerable.”

- The capital stock is very old and will be replaced. “The last time the corporate sector allowed its capital stock to get this old and obsolete was back in 1958 and then annual growth rate in volume capital spending rise to from -6% to 13.5%,” writes Rosenberg. “Revived capex growth is likely going to emerge as a key bullish cyclical theme for 2014.”

- With the housing recovery’s role in supporting the economy, the torch will have to be handed over to the consumer. “The flow of savings into the household sector is now running in excess of a $600 billion annual rate, up 6.4% from year-ago levels, and serving up a nice cushion for the spending outlook.”

- Job market and consumer confidence improve. Rosenberg thinks we are two or three months from see jobs outside of the financial sector hit a new all-time high.

- Future returns in the stock and bond markets will be muted. In the bond market, coupons are low and banks have been trying to fight deflation and this “limits the potential for future yield declines, that it seems hardly likely that there will be any capital gains down the road.” The stock markets in the U.S. has had 25% gains “in what has turned into a backdrop almost exclusively reliant on multiple expansion.” Instead he thinks returns will have to be found in “yield curve plays to credit strategies to sector rotation.”

- The Fed will fall behind the curve. “There was always this symbiotic relationship — the Fed would lead the bond market, and then pay heed to what the market was saying in return,” writes Rosenberg. “The problem now is that it is next to impossible for the Fed to heed a message from a market that is trying to dominate.”

- Expect volatility as Janet Yellen prepares to take over from Ben Bernanke. Volatility always becomes a “watchword” during a transition of Fed chairs. What’s more, at least six Fed governors and bank presidents are set to step down as well, which also means a new FOMC.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair