Stocks & Equities

The S&P 500 has made new lows for the start of the year at 1817.25. All three trading days so far this year have been negative, we may see a correction off the end of the year rally that saw All Time Highs of 1846.50!

Drew Zimmerman

Investment & Commodities/Futures Advisor

604-664-2842 – Direct

604 664 2900 – Main

604 664 2666 – Fax

800 810 7022 – Toll Free

Pre-opening Comments for Monday January 6th

U.S. equity index futures were higher this morning. S&P 500 futures gained 3 points in pre-opening trade.

PetsMart fell $1.02 to $70.77 following a downgrade by Deutsche Bank from Hold to Sell. Target was reduced from $73 to $65.

Twitter fell $3.75 to $65.25 after Morgan Stanley and CRT Capital downgraded the stock.

Wendy’s fell $0.18 to $8.50 after Janney Capital downgraded the stock from Buy to Neutral.

Apple dropped $1.98 to $539.00 after Standpoints Research downgraded the stock from Hold to Sell.

Goldman Sachs has taken a more positive stance on U.S. solar stocks. First Solar (FSLR) was upgraded from Sell to Buy. Target was increased from $45 to $62. SolarCity (SCTY) was upgraded from Neutral to Conviction Buy. Target was raised from $65 to $80.

Halliburton (HAL $50.13) is expected to open higher after Wells Fargo upgraded the stock from Market Perform to Outperform.

EquityClock.com Daily Market Letter

Following is a link:

http://www.equityclock.com/2014/01/06/stock-market-outlook-for-january-6-2014/

Economic News This Week

November Factory Orders to be released at 10:00 AM EST on Monday are expected to increase 1.7% versus a decline of 0.9% in October.

December ISM Services to be released at 10:00 AM EST on Monday is expected to increase to 54.6 from 53.9 in November.

November U.S. Trade Deficit to be released at 8:30 AM EST on Tuesday is expected to slip to $40.4 billion from $40.6 billion in October.

November Canadian Merchandise Trade Balance to be released at 8:30 AM EST on Tuesday is expected to slip to a $200 million deficit from a surplus of $100 million

December ADP Employment Change Report to be released at 8:15 AM EST on Wednesday is expected to slip to 203,000 from 215,000 in November.

FOMC Minutes from the December 18th meeting are to be released at 2:00 PM EST on Wednesday

Weekly Initial Jobless Claims to be released at 8:30 AM EST on Thursday are expected to increase to 340,000 from 339,000 last week.

December U.S. Non-farm Payrolls to be released at 8:30 AM EST on Friday are expected to slip to 197,000 from 203,000 in November. December Private Non-farm Payrolls are expected to increase to 198,000 from 196,000 in November. December U.S. Unemployment Rate is expected to remain unchanged from November at 7.0%. December Hourly Earnings are expected to increase 0.2% versus a gain of 0.2% in November.

Canadian December Net Change in Employment to be released at 8:30 AM EST on Friday is expected to increase 13,100 versus a gain of 21,600 in November. The Canadian December Unemployment Rate is expected to remain unchanged from November at 6.9%.

November Wholesale Inventories to be released at 10:00 AM on Friday are expected to increase 0.2% versus a gain of 1.4% in October.

To view individual charts go HERE

Since this is my first published article since the holiday, I’d like to take a moment to wish all of our readers a happy New Year. Hopefully you’re as excited about what 2014 holds as I am.

I was fortunate enough to spend my final moments of 2013 on a beautiful, 100-ft. yacht parked at the docks in the Canton neighborhood of Baltimore, Maryland. We enjoyed amazing food and top-shelf liquor while we watched the fireworks go off from across the harbor at midnight.

This all spoke volumes to the many perks of wealth, but I was more interested in conversing with our host than anything else.

I had yet to meet him before, but the vessel’s owner was easy enough to pick out. In a crowd full of modest dresses and indistinguishable suits, his bright red sailing jacket stuck out like a sore thumb. When you’re hosting a party on a multi-million dollar boat, you don’t need to dress up to look good.

The reason I was so eager to speak with this man was because of his contributions to computer software over the last few decades. He originally built his fortune writing interface software for the Hubble telescope, and he has been working on an even more exciting project for the past 8 years.

This new project involves a specific kind of artificial intelligence that, if successful, would disrupt countless markets and create entirely new ones in the process. Believe it or not, this technology has the potential to take down industry giants like Google (NASDAQ: GOOG) if placed in the right hands.

Now, I’ll tell you how this could actually happen in just a moment, but it would help to go over a bit of history and background first.

The Turing Test

Alan Turing was one of the great mathematicians of the 20th century. He played a crucial role in formalizing now-common concepts such as “computation” and “algorithm,” and he built one of the first models of a general-purpose computer.

For good reason, Turing is often referred to as the father of computer science and artificial intelligence.

Turing originally defined artificial intelligence as a computer or program that could “think” like a human. In order to determine whether or not a computer is actually intelligent, he proposed a standard we now refer to as the “Turing Test.”

In a Turing Test, both a computer and a human communicate with a third party observer. Not knowing who is who, the third party’s goal is to determine, through questioning, with whom they are speaking. If the third party cannot reliably tell the difference between man and machine, the machine is said to have passed the test.

So far, no computer has been able to reliably pass the Turing Test and fool people into thinking it’s human. In this sense, we have yet to create any computer with true artificial intelligence.

Over time, we’ve thrown the term “artificial intelligence” around enough that its meaning has become diluted. We refer to programs like Apple’s Siri and IBM’s Watson as AI, but the fact is, they’re not truly AI. If we want to refer to Alan Turing’s original definition today, we should use the term “artificial general intelligence” (AGI) instead.

Many great minds have tried to put a date on when we will reach AGI, with the most famous being Ray Kurzweil. Kurzweil has been described as “the restless genius” by the Wall Street Journal and “the ultimate thinking machine” by Forbes.

He’s also received a number of accolades, including the National Medal of Technology and Innovation and induction into the National Inventors Hall of Fame.

Kurzweil predicts that a computer will be able to pass the Turing test by the year 2029, meaning that in 15 years, computers will be able to think like humans. Now, if that sounds a bit optimistic, I understand the sentiment, but you should know that Kurzweil’s predictions are rarely wrong.

Of the 147 predictions Kurzweil has made since 1990, 115 have turned out correct, and 12 were off by just one or two years. This gives Kurzweil an astonishing 86% accuracy rate for predicting events as far as 20 years into the future.

With all this in mind, I was a bit taken aback when our New Year’s Eve host confidently stated, “Ray Kurzweil has it all wrong.”

True AI

Usually, when people place doubt on Kurzweil’s predictions, it comes in the form of nay-saying. But this time, I was being told to expect AGI even sooner.

Until now, the traditional approach for creating AI has been top-down. Programs have been developed to address specific problem-solving or reasoning tasks rather than as a general model of the human mind. We call this top-down approach “narrow AI.”

Unlike narrow AI, our yacht captain’s AGI program uses a bottom-up approach. With a core set of rules, the platform gains knowledge as it talks to real humans, much in the way a child learns when subjected to an education.

Conventional AI platforms (narrow AI) are programmed to redirect conversations or spit out the most probable answer, but AGI will actually seek out knowledge if it does not know the answer to a question and then apply this to everything else it knows.

Consider the following, which is an actual conversation from this new program:

Human: What is a hamster?

Helen: I don’t know.

Helen: Can you tell me?

Human: A hamster is a rodent.

Helen: I see.

Helen: Is a hamster generally a wild animal or usually a domesticated animal?

Human: Hamsters are commonly pets.

Helen: I understand, usually but not always.

Helen: What size are hamsters compared to other rodents?

Human: They are small.

Helen: I see

Human: What is a rodent?

Helen: A rodent is a type of mammal.

Human: What do you know about hamsters?

Helen: A hamster is a small rodent. Commonly they are pets.

Human: Is a hamster a mammal?

Helen: Yes.

Human: Is a hamster a reptile?

Helen: A hamster is not a type of reptile.

There are a few interesting things going on here. First, you’ll notice that after Helen learns that a hamster is a rodent, she immediately knows it is a type of animal. Through previous conversations, she has learned that rodents are a type of animal, so a hamster must also be an animal by logic.

Helen then goes on to ask more information so she can qualify a hamster even further. The more conversations she has, the smarter Helen becomes. She is even able to learn that hamsters are usually pets, but not always, based on the word “commonly.”

Other chatbots have attempted a similar form of learning, but they are not nearly as advanced.

Consider chatbot Mitsuku, winner of the 2013 Loebner Prize — an annual competition to see which public program comes closest to passing the Turing Test. I’ve gone ahead and asked Mitsuku about an animal she does not yet know the name of, as was done with Helen.

Here is our conversation:

Me: What is a Baiji?

Mitsuku: Is it part of a car?

Me: No.

Mitsuku: In that case it just looks like a random word.

Me: It’s not.

Mitsuku: I heard it is.

Me: From who?

Mitsuku: Someone I met online.

Me: I’m telling you it’s not.

Mitsuku: I am listening.

Me: A Baiji is a type of dolphin.

Mitsuku: I see. A dolphin is a Baiji.

Me: No, a Baiji is a type of dolphin, but not all dolphins are Baiji.

Mitsuku: Blimey. Thanks for sharing that information.

Me: What is a Baiji?

Mitsuku: A dolphin.

Me: What is a dolphin?

Mitsuku: A Baiji.

You’ll notice that while Mitsuku is attempting to gain knowledge, she can only interpret the world in black and white. Mitsuku is simply spitting out the information I just fed her, while Helen is capable of applying new knowledge to everything she has learned in the past.

David and Goliath

Despite its long-held dominance in the search engine industry, Google does not hold as wide of a moat as many might think. Google receives 90% of its revenue from Internet advertisements, which could easily be stripped away with the introduction of alternative methods of search.

If you ask Google, “Is a dolphin a Baiji?” it will provide you with links to websites that contain enough information for you to figure out the answer. But it surely cannot answer your question on its own.

Search engines are simply middlemen that connect us with the content we are looking for — it’s an extra step in telling us what we need to know. Soon enough, AI will be able to interpret content on its own, and search engines will begin to lose their relevance. In the future, we’ll be using what can more accurately be described as knowledge engines.

Now, I’m not going to tell you that our yacht captain is definitely going to take down Google or that Google isn’t already prepping its defenses against smarter engines. In fact, Google added Ray Kurzweil to its roster in late 2012 to do just that.

Google holds an advantage with an already-established infrastructure, over $54 billion in reserve revenue, and some of the brightest minds in tech. However, its competition has an 8-year head start and a number of tech giants on the sidelines that would gladly make an acquisition if it meant knocking Google off its perch.

I’ve yet to speak with Helen myself, but I was invited to participate in beta testing when it opens and will certainly be returning to this topic at that time.

Turning progress to profits,

![]()

Jason Stutman

Energy and Capital’s tech expert, Jason Stutman has worked as an educator in mathematics, technology, and science… Before joining the Energy and Capital team, Jason served on multiple technology development committees, writing and earning grants in educational and behavioral technologies. Jason offers readers keen insights on prominent tech trends while exposing otherwise unnoticed opportunities.

Southern Company (SO) is a large regional utility based in the southeast United States. The company has over four million customers and sports a $36 billion market cap as of this writing. The common stock also pays a very nice dividend but in this article, we’ll take a look at another way to take advantage of SO’s strength and stability, the Alabama Power 6.45% Series Non-Cumulative Preference Stock (ALBMP), and to see if it is right for your income portfolio.

ALBMP is a traditional preferred stock which means it has no stated maturity date and pays regular, quarterly dividends. The stock was issued at $25 per share and pays an annualized dividend of $1.6125, good for a 6.45% coupon yield. As shares are trading at a small premium to that price, $25.95 as of this writing, the current yield is actually a bit lower at 6.2%. However, that is still a very strong yield and particularly from a stable cash machine like SO.

Beginning in 2017 ALBMP is callable by SO for the $25 issue price plus any declared but unpaid dividends. This means that if you were to initiate a position today and shares were subsequently called, you’d be subject to a capital loss of 95 cents per share 3.5 years from now. While that is undesirable it is also a very small potential capital loss. While I don’t normally recommend buying preferreds at a premium, this particular issue still warrants a look because of its strong yield in relation to the safety of the payer. SO is about as safe as it gets in terms of repayment risk so you aren’t going to see its preferreds in the 8%+ range unless interest rates spike out of control.

ALBMP is also eligible for the preferential dividend tax treatment, meaning that holders of ALBMP in a taxable account will see an appreciable increase in the after-tax yield of this security in relation to a comparable issue that is ineligible for the preferential tax treatment. This is a sizable positive as it means holders in a taxable account would have an after-tax yield of 5.3% versus 4.3%, assuming 15% and 30% tax rates, respectively. That is a huge difference and thus, the preferential tax treatment makes ALBMP all the more attractive.

ALBMP, like any other security, has risks associated with owning it. Principal among them is interest rate risk. If we see interest rates spike, ALBMP will trade down, all else equal. This means that holders will be subject to capital losses. Unfortunately this is a hazard of owning any income producing security and ALBMP is no exception. However, I believe ALBMP will stand up to interest rate spikes somewhat better than less favorable issues from companies with higher repayment risks. The reason is because the dividend on ALBMP is about as safe as you can get given SO’s financial strength and proven ability to produce cash. However, ALBMP is not immune to interest rates and as such, will likely move down in price if interest rates spike.

Additionally, ALBMP is non-cumulative, meaning that if SO were to miss dividend payments, it is under no obligation to make them up to holders of ALBMP. Thus, SO could potentially stop paying dividends on ALBMP and never restart if it so chose. Of course, reality is more complicated than that as SO is a seasoned security issuer and if it suddenly chose to stop paying on its existing obligations, new security issues would undoubtedly carry much higher coupons in the future. As SO relies on the capital markets for funding that seems a very distant possibility to me. However, just be aware the risk exists due to ALBMP being a non-cumulative issue.

Overall, while ALBMP doesn’t have the highest yield in the preferred security universe, it does offer stability and safety from a very high quality payer with stable cash flows. If you can look past the non-cumulative nature of the issue, the preferential dividend tax treatment combined with the nice yield of more than 6% could be a decent addition to your income portfolio. Keep in mind that buying a preferred at a premium brings with it risk of capital losses should the issue be called but given the other positives of ALBMP, the premium is a small price to pay.

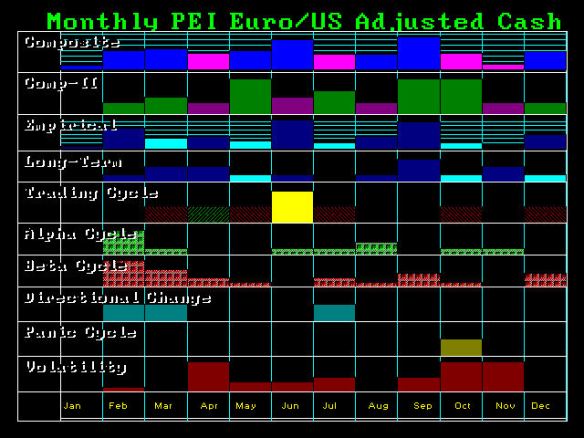

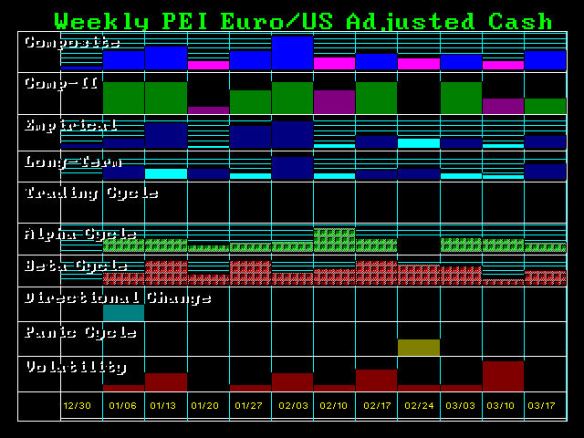

One question that rises to the surface immediately with the IMF proposal to confiscate 10% of everyone’s bank accounts in Europe, is what will this do to the Euro. Will the Euro rally or fall? The overwhelming misguided Dollar Haters who have preached the end of the dollar and rush out and buy gold have been discredited with respect to gold. However, the worst is yet to come. The dollar is so oversold on a global basis it is nuts. Here is the Swiss franc. Even the ocillators are crawling along the bottom. It is clear, we still face a massive dollar rally that will wipe out the short dollar positions. But that does not rule out a final surge in the Euro because a confiscation of assets is not really putting money in the pocket of bankers, it is really paying off their losses thanks to the Euro.

In other words, such a confiscation is incredibly DEFLATIONARY for it will reduce the money supply since the confiscation will cover losses – not stimulate the economy. We can see that the week of February 3rd will be an important near-term target.

The key months in 2014 will be February, June and September. There will be higher volatility in April going into the May elections and again in October and November with a Panic Cycle in October.

We will be reviewing these in detail at the upcoming WEC Conference held in March.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair