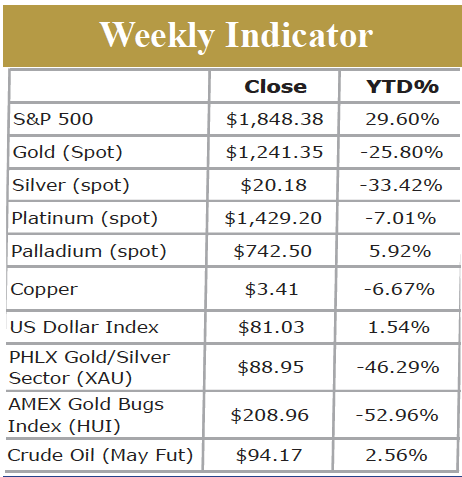

Energy & Commodities

In this week’s Bulletin, I am highlighting the recent positive action in Uranium shares, specifically URA – the GlobalX Uranium ETF, shown below in both a daily and weekly chart. The key has been recent accumulation patterns confirmed using my own Leibovit ‘VR’ Indicator (shown below with green arrows). Weekly accumulation has been underway for nearly four months as prices rise to the blue 50 weekly moving average (currently at 17). The blue daily 50 day moving average sits at 16.25. As a point of reference, the February, 2011 peak in URA stood at 67.26 and it’s lowest low occurred in October, 2013 at 13.82. My target? I would look for a minimum move to 18.75 with potential as high as 22.00-23.00. I can find no recent news regarding Uranium which I interpret as a bullish sign.

In this week’s Bulletin, I am highlighting the recent positive action in Uranium shares, specifically URA – the GlobalX Uranium ETF, shown below in both a daily and weekly chart. The key has been recent accumulation patterns confirmed using my own Leibovit ‘VR’ Indicator (shown below with green arrows). Weekly accumulation has been underway for nearly four months as prices rise to the blue 50 weekly moving average (currently at 17). The blue daily 50 day moving average sits at 16.25. As a point of reference, the February, 2011 peak in URA stood at 67.26 and it’s lowest low occurred in October, 2013 at 13.82. My target? I would look for a minimum move to 18.75 with potential as high as 22.00-23.00. I can find no recent news regarding Uranium which I interpret as a bullish sign.

Mark Leibovit is Chief Market Strategist and Publisher for the Leibovit VR Gold Letter and the author of ‘The Trader’s Book of Volume’ which was published in 2011 by McGraw-Hill. You may have recognized Mark as one of the ten “Elves” on Louis Rukeyser’s Wall Street Week television program where he served as a weekly consultant for 7 years and also as a regular Market Monitor guest for 30 years on PBS’ The Nightly Business Report. He is a popular speaker at investment conferences both in the U.S. and Canada and is often seen on PBS, BNN and FOX Business News. TIMER DIGEST Magazine has named him the #1 Gold Timer for the twelve-month period from 8/26/10 to 8/26/11 and for the 5-year period ending 2010. He was also named the #1 Intermediate Market Timer for the 10-year period ending in 2007. Mr. Leibovit was a member of the Chicago Board Options Exchange where he became a market maker in several stocks including Newmont Mining. Through the late 1980s he was Technical Research Director for Rodman & Renshaw and subsequently began publishing several financial newsletters. He holds a CIMA and AIF designation and is a member of the Market Technicians Association (MTA) and the CFA Institute.

A Guide to Our Metal Commentary

Our charts are based on data compiled at the market close prior to publication. If you have questions on our current stops or targets, please don’t hesitate to drop us an email at mark.vrtrader@gmail.com. If overall market action necessitates a bulletin, we will send it out as necessary, but I would encourage you to subscribe to the VRtrader Platinum service which often sends out multiple bulletins each day. Please go to www.vrtrader.com for more information. Charts herein incorporate the common 50 and 200 day moving averages. If you would like access the Leibovit Volume Reversal signals daily, subscribe to my ‘Add-on’ Leibovit VR Indicator from either Metastock or ESignal.

Please note that daily and weekly charts can show different technical patterns. Sometimes the formation of Positive Leibovit Volume Reversals occurs in the weekly charts and not in the daily charts. Just look for the red ‘VRs’ which represent sellers and the blue ‘VRs’ which represent buyers. The blue line in our metal charts represents the 200 day moving average and the green line represents the 50 day moving average. Keep in mind moving averages are only points of reference, but their existence becomes a self-fulfilling (almost like magnets) among traders.

© 2014. Volume Reversal Ventures LLC. All Rights Reserved.

The Leibovit VR Gold Letter is a weekly publication of Volume Reversal Ventures LLC and is offered online via email.

For rights, permissions, subscription and customer service, contact the publisher at vrcustomerservice@gmail.com,

call at 928-282-1275.

Disclaimer: All investments are subject to risk, which should be considered on an individual basis before making any investment decision. Volume Reversal Ventures LLC, the owner, publisher and editor of The Leibovit VR Gold Letter, is not responsible for errors and omissions. This publication is intended solely for information and educational purposes only and is not to be construed, under any circumstances, as an offer to buy or to sell or a solicitation to buy or sell or trade in any commodities or securities named within this newsletter. Information gathered to create this letter is from sources believed to be reliable, but is in no way guaranteed. Furthermore, you cannot be assured that your will profit or that any losses can or will be limited. It is important to know that no guarantee of any kind is implied nor possible where projections of future conditions in the markets are attempted. Hypothetical or simulated performance results have certain inherent limitations as to liquidity and execution among other variables. Some recommended trades may include securities held by Volume Reversal Ventures LLC or its officers or affiliates or family members and their personal investment decisions may be different those discussed or made in The Leibovit VR Gold Letter. Volume Reversal Ventures LLC is not compensated in any way for publishing information about companies mentioned in the financial commentary. All readers should consult their own personal investment adviser before making an investment decision. Copyright © 2013 The Leibovit Gold VR Letter and Volume Reversal Ventures LLC.

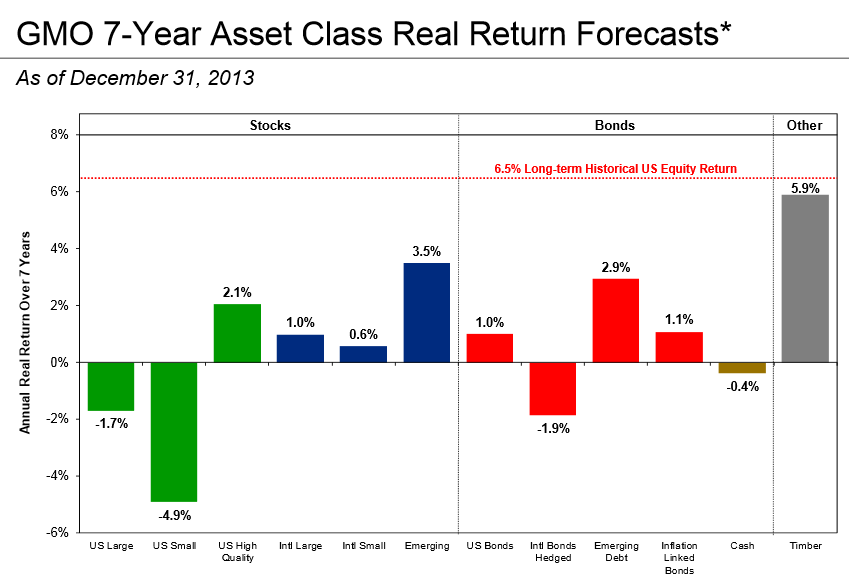

Value investor Grantham, Mayo, Van Otterloo (GMO) now estimates US stocks are poised for annualized losses for the next seven years. (click on image or HERE for larger view)

*The chart represents real return forecasts for several asset classes and not for any GMO fund or strategy. These forecasts are forward-looking statements based upon the reasonable beliefs of GMO and are not a guarantee of future performance. Forward-looking statements speak only as of the date they are made, and GMO assumes no duty to and does not undertake to update forward-looking statements. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results may differ materially from those anticipated in forward-looking statements. US inflation is assumed to mean revert to long-term inflation of 2.2% over 15 year.

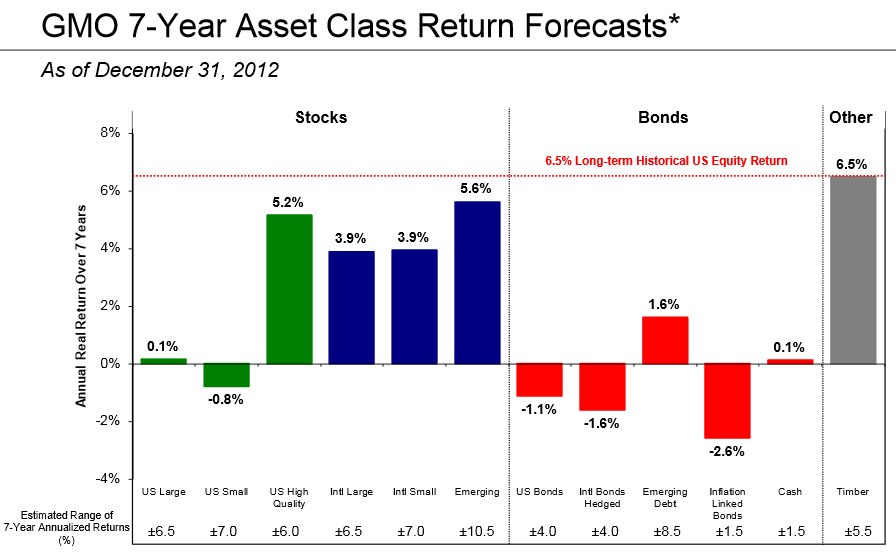

A year ago the chart looked like this. (Click HERE or on image for larger view)

Charts from GMO Asset Class Forecasts.

Reflections on Extreme Valuations

Was GMO wrong last year? Of course not. Expected returns are just that. Extreme valuations can always become even more extreme (and they did).

My Thoughts:

During periods of market excess, avoiding bubbles and instead investing in out of favor but attractive assets can be quite painful to live through in the short-term. But those who remain disciplined and on the right side of the somber judgment eventually get rewarded with significant gains amid widespread losses for those favoring that which has been working well during the period of excess.

GMO 10-Year History

Let’s step back a bit and look at GMO’s 10-Year history from 1999-2009. Please consider the chart below from What a Decade!

Highlighting in yellow is mine.

In December 1999, GMO thought the S&P 500 would deliver negative returns for a decade. In 2007 that prediction probably looked ridiculous. Yet, it happened.

When GMO predicts negative returns, it’s smart to pay attention.

Here are GMO’s “Lessons Learned in the Decade”.

Lessons Learned

- The Fed wields even more financial influence than we thought.

- Low rates have a more powerful effect on driving financial assets than on driving the economy.

- The Fed is capable of being extremely out of touch with the real world – “what housing bubble?” – plus more doctrinaire – “no, the low rates had no effect on housing” – than anyone could have imagined.

- Congress is nearly dysfunctional, primarily controlled by large corporations, and hamstrung by the supermajority now routinely required in the Senate.

- Government administrations can be incompetent for long periods.

- Poor leadership can really damage a country’s hard- won reputation in a mere 10 years.

- Obama is not a miracle worker!

- The two time-tested investment tools, value (P/E ratios and P/B ratios) and price momentum, are now much more heavily used and not so reliable as they once were, say from 1977 to 1997.

- Asset classes really are more inefficiently priced than individual stocks on average, and therefore offer greater opportunities for adding value and reducing risk.

- Developed countries, including the U.S., are past their prime compared with developing countries: it is indeed a new world order.

- Education and training are the keys to increasing wealth on a sustainable basis and the U.S. is in danger of losing its once large edge here.

- We all live on an island, which can be overexploited and turned into a barren Easter Island if we are not careful. Resources are finite and biodiversity is fragile, and both must be protected. Carbon emissions are the single greatest threat.

- Being a global policeman is expensive, and somewhere between difficult and impossible.

- The Fed learns no lessons!

Fed Uncertainty Principle Revisited

The only point I disagree with is number 12 “carbon emissions are the single greatest threat” to finite resources and biodiversity.

Arguably the most important points are 1-3 and 14 “The Fed learns no lessons“.

Readers will recognize those points as part of my Fed Uncertainty Principle, written April 3, 2008, before the big collapse.

Fed Uncertainty Principle:

The fed, by its very existence, has completely distorted the market via self reinforcing observer/participant feedback loops. Thus, it is fatally flawed logic to suggest the Fed is simply following the market, therefore the market is to blame for the Fed’s actions. There would not be a Fed in a free market, and by implication there would not be observer/participant feedback loops either.

Corollary Number One:

The Fed has no idea where interest rates should be. Only a free market does. The Fed will be disingenuous about what it knows (nothing of use) and doesn’t know (much more than it wants to admit), particularly in times of economic stress.

Corollary Number Two: The government/quasi-government body most responsible for creating this mess (the Fed), will attempt a big power grab, purportedly to fix whatever problems it creates. The bigger the mess it creates, the more power it will attempt to grab. Over time this leads to dangerously concentrated power into the hands of those who have already proven they do not know what they are doing.

Corollary Number Three:

Don’t expect the Fed to learn from past mistakes. Instead, expect the Fed to repeat them with bigger and bigger doses of exactly what created the initial problem.

Corollary Number Four:

The Fed simply does not care whether its actions are illegal or not. The Fed is operating under the principle that it’s easier to get forgiveness than permission. And forgiveness is just another means to the desired power grab it is seeking.

Bubble Valuation Blues

It’s not just GMO singing the bubble valuation blues. John Hussman has independently concluded the same thing.

On November 11, 2013 in Textbook Pre-Crash Bubble Hussman commented “The problem with bubbles is that they force one to decide whether to look like an idiot before the peak, or an idiot after the peak. There’s no calling the top, and most of the signals that have been most historically useful for that purpose have been blazing red since late-2011.“

Such is the nature of the game. Everyone thinks they can get out at the top. Few ever do.

Hovering With an Anvil

Please consider this snip from Hussman’s Hovering With an Anvil from January 13 (emphasis mine).

The ratio of nonfinancial equity market capitalization to GDP is about twice its pre-bubble norm, and is presently associated with an expectation of negative total returns for the S&P 500 over the coming decade. Measures based on properly normalized earnings are a little bit more favorable, with the overall outcome that we broadly expect nominal total returns for the S&P 500 of about 2.3% annually over the coming decade, with negative total returns on horizons of less than about 7 years.

Keep in mind that the 2000-2002 decline wiped out the entire total return of the S&P 500, in excess of Treasury bills, all the way back to May 1996. The 2007-2009 decline wiped out the entire total return of the S&P 500, in excess of Treasury bills, all the way back to June 1995. Our present expectations are rather conservative by comparison.

I side with GMO and Hussman.

Wine Country Conference II

I am pleased to again mention that John Hussman is a speaker and host of the second annual Wine Country Conference will be held May 1st & 2nd, 2014.

We have an exciting lineup of speakers for this year’s conference.

- John Hussman: Founder of Hussman Funds, Director of the John P. Hussman Foundation which is dedicated to providing life-changing assistance through medical research

- Steen Jakobsen: Chief Economist of Saxo Bank

- Stephanie Pomboy: Founder of MacroMavens macroeconomic research

- David Stockman: Ronald Reagan’s budget director, best-selling author, former Managing Director of The Blackstone Group

- Mebane Faber: Co-founder and the Chief Investment Officer of Cambria Investment Management

- Jim Bruce: Producer, Director, and Writer of Money For Nothing: Inside the Federal Reserve

- Chris Martenson: Reknown speaker and founder of Peak Prosperity

- Mike “Mish” Shedlock: Investment advisor for Sitka Pacific and Founder of Mish’s Global Economic Trend Analysis

In addition, we expect confirmation from a number of other highly respected fund managers and speakers. This year’s event is two days and will include additional “break-out” groups.

For speaker bios, please check out Wine Country Conference Speakers.

This Year’s Cause: Autism

$100,000 of the money raised last year came from a generous matching grant from the John P. Hussman Foundation.

Some of us in the industry who have done well are making an effort to give something back. John Hussman is at the very top of that list.

One of John’s kids has severe autism. This year, all net proceeds will go to support autism programs.

Conference Details

For further details about the 2014 conference, please see Wine Country Conference May 1st & 2nd, 2014

Nothing Like It!

This event is not just another “come and hear someone talk” kind of thing. Attendees and their significant others can expect an educational, fun, and relaxed time.

Last conference, we arranged wine tours. They were a big hit. We will do so again. One of the wine estates we visited had a Bocce Ball court. On a couple of miracle shots, I won both games I played.

Stay an extra day and golf or travel. I did. The conference hotel is a fun place in and of itself.

Unlike many other conferences, you will have easy access to speakers.

Want to chat with me, Steen, John, or anyone else at the conference? You will have an easy chance.

Not only do we have an excellent lineup of speakers, you will have an opportunity to meet with them, have intimate discussions on important investment topics, with a lot of fun on the side, including wine tours and great wine.

There’s nothing like it in the investment business. And your money goes to a great cause! What can be better?

For more information, please visit any of our blogs today:

- Eric Sprott Blog

- James Turk Blog

- Jim Rickards Blog

- The Silver Liberation Blog

- Peter Schiff Blog

- Marc Faber Blog

- Jim Rogers Blog

- Sprott Money Blog

- David Morgan Blog

- Gold and Silver News

- Mike Maloney Blog

Please note, all of our services are offered to you completely for free. We are able to remain this way purely from ad revenue (ads clicked) and our sponsors. Thank you for your support.

Please visit these recommended links:

“World economic freedom has reached record levels. But after seven years of straight decline,

the U.S. has dropped out of the top 10 most economically free countries.”

– Wall Street Journal, January 13, 2014

BOB HOYE

PUBLISHED BY INSTITUTIONAL ADVISORS

JANUARY 15, 2014

Key lines in the cartoon are:

“Depleting The Resources Of The Soundest Government In The World”

“Young Pinkies From Columbia And Harvard”

What appears to be Trotsky is outlining a radical agenda.

Since the early 1970s, the bitter academic Saul Alinsky has inspired legions of the politically

ambitious. Including many in today’s White House.

The opening paragraph of his Rules For Radicals says it all:

“What follows is for those who want to change the world from what it is to what they believe it should be. The Prince was written by Machiavelli for the Haves on how to hold power. Rules for Radicals is written for the Have-Nots on how to take it away.”

– Rules for Radicals: A Pragmatic Primer for Realistic Radicals

Considering that political disaster has been the inevitable consequence of every great experiment in authoritarian government, what are today’s American authoritarians really winning?

Power, but not yet unlimited.

The full article follows:

Wall Street Journal, January 13, 2014

Regulation, taxes and debt knock the U.S. out of the world’s

top 10.

By Terry Miller

World economic freedom has reached record levels, according to the 2014 Index of Economic Freedom, released Tuesday by the Heritage Foundation and The Wall Street Journal. But after seven straight years of decline, the U.S. has dropped out of the top 10 most economically free countries.

For 20 years, the index has measured a nation’s commitment to free enterprise on a scale of 0 to 100 by evaluating 10 categories, including fiscal soundness, government size and property rights. These commitments have powerful effects: Countries achieving higher levels of economic freedom consistently and measurably outperform others in economic growth, long-term prosperity and social progress. Botswana, for example, has made gains through low tax rates and political stability.

Those losing freedom, on the other hand, risk economic stagnation, high unemployment and deteriorating social conditions. For instance, heavy-handed government intervention in Brazil’s economy continues to limit mobility and fuel a sense of injustice.

It’s not hard to see why the U.S. is losing ground. Even marginal tax rates exceeding 43% cannot finance runaway government spending, which has caused the national debt to skyrocket. The Obama administration continues to shackle entire sectors of the economy with regulation, including health care, finance and energy. The intervention impedes both personal freedom and national prosperity.

But as the U.S. economy languishes, many countries are leaping ahead, thanks to policies that enhance economic freedom—the same ones that made the U.S. economy the most powerful in the world. Governments in 114 countries have taken steps in the past year to increase the economic freedom of their citizens. Forty-three countries, from every part of the world, have now reached their highest economic freedom ranking in the index’s history.

Hong Kong continues to dominate the list, followed by Singapore, Australia, Switzerland, New Zealand and Canada. These are the only countries to earn the index’s “economically free” designation. Mauritius earned top honors among African countries and Chile excelled in Latin America. Despite the turmoil in the Middle East, several Gulf states, led by Bahrain, earned designation as “mostly free.”

BOB HOYE, INSTITUTIONAL ADVISORS – WEBSITE: www.institutionaladvisors.com

We’re pleased to post the full agenda for the 25th annual World Outlook Financial Conference including an expanded offering of workshops and seminars. Come out and hear some of the world’s top market analysts and prognosticators. You can’t afford to miss the event.

We’re pleased to post the full agenda for the 25th annual World Outlook Financial Conference including an expanded offering of workshops and seminars. Come out and hear some of the world’s top market analysts and prognosticators. You can’t afford to miss the event.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair