Gold & Precious Metals

- Most junior gold and silver stocks have taken a horrific beating over the past few years, even while gold prices have remained relatively elevated.

- Bank analysts suggest that high mine costs are largely to blame for this sell-off.

- Recently, naked shorting seems to have diminished. Gold stocks have rallied very strongly over the past month, on enormous volume.

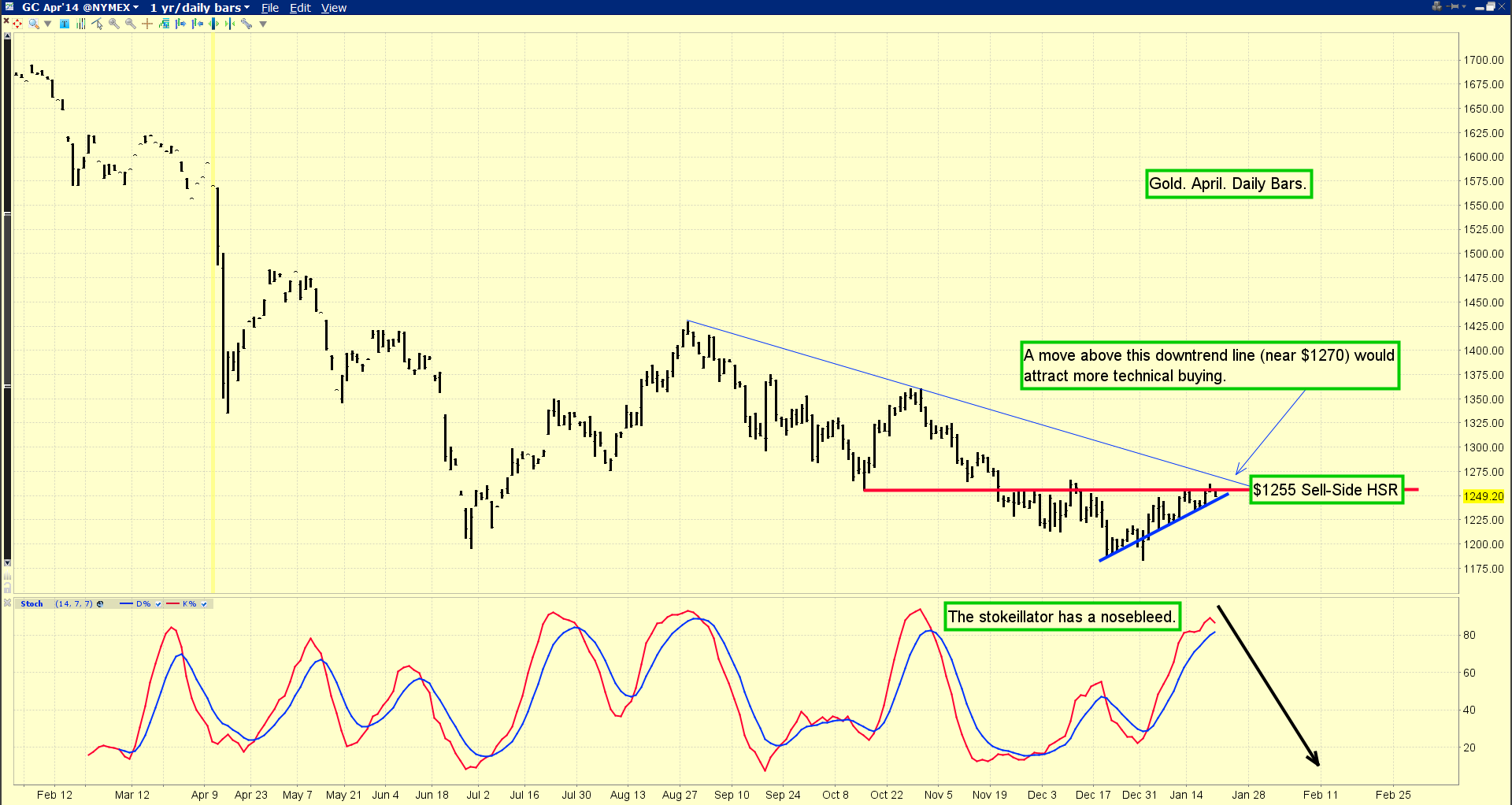

- Can the rally continue, and is it related to lower mining costs? In the short term, there’s no question that gold and gold stocks are technically overbought.

- Note the position of my stokeilllator (14,7,7 Stochastics series) on this daily gold chart. After reaching about 90, the lead line is rolling over. Click to enlarge

- It could be said that this key oscillator has a nosebleed, from altitude sickness.

- So, light trading profits in gold and related items should be booked by aggressive investors now.

- In the bigger picture, a rise above the light blue trend line in the $1270 area could attract strong technical buying, initiating a very powerful move to the upside.

- From a fundamental perspective, the cost of energy is very important to mining companies. Lower mine costs, combined with a relatively stable gold price, mean more profits for mining companies. Larger profits can attract very strong institutional buying of high quality gold shares.

- Please click here now. This interesting weekly chart compares GDXJ to oil. The 14,3,3 Stochastics and RSI oscillators are both very bullish, and volume is powerful.

- Against oil prices, junior gold stocks appear to have broken out to the upside. A short term pullback after such a strong breakout is to be expected, followed by a much bigger rally.

- I’ve compared the recent price performance of junior gold stocks to heavyweight boxer George Foreman, because they are crushing every other asset in their path.

- Please click here now. This daily chart shows that over the past month, GDXJ has gained about 25% against the Dow.

- It’s now running into some overhead HSR (horizontal support and resistance). I’ve marked that in red colour on the chart. After such a powerful move to the upside, a brief pause is perfectly normal.

- The “health” of an intermediate trend rally is maintained by the occurrence of regular minor trend sell-offs.If that doesn’t happen, a much more painful sell-off often ensues.

- Many investors sold gold stocks for a “tax write-off” in December, and some of them bought the Dow with the proceeds of that transaction. I think investors should sell gold stocks at a profit, not a loss, and I wouldn’t buy the Dow with any of those profits.

- As 2014 progresses, the Fed will probably taper more aggressively, because money supply velocity (via M1V and M2V) is likely to accelerate, catching the Fed by surprise.

- That accelerated taper is likely to cause the economy to slow a bit, weighing on energy prices.

- Institutional money managers would then be quite likely to move funds from the Dow into gold stocks.

- Yesterday was a US holiday, and stock markets were closed. The Toronto market was open, and gold stocks had a good day of trading.

- Please click here now. Double-click to enlarge. This daily ZJG.TO chart (Bank of Montreal junior gold stocks ETF) is the Canadian version of GDXJ. Investors in Canadian gold stocks should book light trading profits, but be open to the possibility that a much bigger rally will follow any pullback.

- The US markets are all open again today. Where should US junior gold stock investors look to re-enter the market, using the GDXJ chart?

- For the likely answer, please click here now. On this two hour bars chart, I’ve highlighted three key re-buy price zones. Gamblers could buy in the $34.99 area, with an optional stoploss order placed under the minor trend low at $33.20. I don’t use stoplosses, and I’m not a big gambler, but I will lightly buy that $34.99 area.

- On any potential pullback for junior gold stocks, the buy-side HSR at $33.40 is what should be the “meat and potatoes” buy zone. It’s where junior gold stock investors may want to re-buy GDXJ, and their favourite individual stocks, with a bit more size!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Special Offer For Website Readers: Please send me an Email to freereports4@gracelandupdates.com and I’ll send you my free “Cameco & Barrick Parade Leaders!” report. Both Cameco and Barrick may be key leading indicators of what is coming for junior uranium and precious metal stocks. I’ll show you why that is, and which juniors may be poised to lead phase two of the gold stocks rally!

Thanks!

Cheers

St

Stewart Thomson

Graceland Updates

Note: We are privacy oriented. We accept cheques. And credit cards thru PayPal only on our website. For your protection. We don’t see your credit card information. Only PayPal does. They pay us. Minus their fee. PayPal is a highly reputable company. Owned by Ebay. With about 160 million accounts worldwide.

Written between 4am-7am. 5-6 issues per week. Emailed at aprox 9am daily.

Email: stewart@gracelandupdates.com

Rate Sheet (us funds):

Lifetime: $799

2yr: $269 (over 500 issues)

1yr: $169 (over 250 issues)

6 mths: $99 (over 125 issues)

To pay by cheque, make cheque payable to “Stewart Thomson”

Mail to:

Stewart Thomson / 1276 Lakeview Drive / Oakville, Ontario L6H 2M8 Canada

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualifed investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

Today’s note is going to be “uncomfortable”…

But it could lead to one of your biggest trading profits this year.

Let me explain…

Last month, we showed you the big boom in biotech…

Remember, biotech is one of the greatest “boom and bust” sectors known to man.

Since 1983, the sector has seen four triple-digit runs… and one quadruple-digit run of 1,347% in the early 1990s. The busts were equally spectacular, taking the entire sector down by as much as 70%.

After the most recent bust in 2009, the Nasdaq Biotech Index started a huge rally… The index is up 250% in five years. And it was the top-performing sector in 2013.

Despite the big run higher, we argued that there would be more gains ahead…

If you gathered 1,000 average investors together, fewer than 10 could confidently say that biotech is one of the top-performing sectors of 2013. In other words, despite the enormous bull market, folks aren’t “hot” on biotech… yet.

Money is flowing into these stocks… Valuations are increasing… The story is starting to appear here and there. But it’s not on the front page of the papers. It’s not a feature story on CNBC. And you won’t hear about it at cocktail parties.

It’s what we call a “stealth” bull market. And it still has room to run higher.

Since then, the double-long biotech fund (BIB) has gained more than 19%. That’s a big move for just three weeks.

Now here’s the “uncomfortable” part…

If you have big gains in biotech, sit tight.

Many traders, when they see profits in their accounts, get “itchy trigger fingers.” They want to pocket a gain before it has the chance to vanish.

Over the long term, that’s the wrong strategy. If you collect your profits early, you may cheat yourself out of a big move higher. And with biotech, that could be a very big move higher…

Right now, the companies in Datastream’s Biotech Index are trading at over 40 times earnings. That’s up from 20 times earnings three years ago. But at the peak in 1999-2000, the index traded up to nearly 140 times earnings.

One classic piece of trading wisdom comes from legendary trader Jesse Livermore. As detailed in the book Reminiscences of a Stock Operator, Livermore said: “It never was my thinking that made big money for me. It was always my sitting. Got that? My sitting tight!”

In other words, his biggest gains came from “sitting tight” through big bull-market moves.

So that’s our recommended action to take with biotech today. If you have a large, short-term gain, you might be tempted to take it off the table. But the trend here is still moving higher. So it’s better just to let a trailing stop tell you when it’s time to get out. (We recommend a 15% trailing stop in DailyWealth Trader.) That will give your profits room to grow.

It might be uncomfortable to sit tight on this trade. But it’s the right thing to do.

Good trading,

Amber Lee Mason

P.S. This idea – that you should let your winners run – is half of the most important lesson you can learn about trading. We made a short educational video to walk you through the whole lesson… and explain why it’s so important. You can watch it right here. (It’s just three minutes long.)

Further Reading:

“We love to sell our winners too soon,” Dr. David ‘Doc’ Eifrig writes. “It’s a nearly universal impulse… but a terrible investing choice.” So how do you know when your winners have had enough time to run? Doc says the strategy for knowing when to sell is “determined by why you bought in the first place.” Get all the details on Doc’s strategy here.

On the other hand, Steve Sjuggerud says most people don’t know when to sell a falling stock. “So they’re frozen into inactivity… until you hear the all-too-familiar phrase, ‘Well, it’s too late to sell now.'” But by creating an exit strategy, Steve says “you’ll never lose another night’s sleep worrying about which way your investments will go tomorrow… Because unlike most investors, you’ll have a plan.” Learn how to create your own exit strategy here.

As the Fed runs low on ammunition to further suppress the gold price, Ian Gordon, founder and chairman of the Longwave Group, is extremely bullish on gold. In this interview with The Gold Report, he recounts his history of the manipulation of the gold price and its implications for the global economy. He also expands on research showing that juniors are more effective and cost efficient at making discoveries.

The Gold Report: Gold was among the worst performing assets in 2013. How have its trading patterns and performance over the last two years informed your predictions for 2014?

Ian Gordon: I’m extremely bullish for the gold price in 2014. Part of that bullishness is related to my work on cycles. Indeed, I am confident that 2014 will see the beginning of the 4th long-term cycle for precious metals and precious metals stocks and the bullish phase of this cycle should last about three years.

The prices of precious metals and precious metals stocks have been badly bruised following their price peaks in 2011, due in part to what I consider to be manipulation in the COMEX. There is a long history of gold price manipulation: In the 1960s, the London Gold Pool was formed to try to hold the price at $35/ounce ($35/oz)—the price the U.S. dollar was pegged to—because gold was leaving the U.S. The London Gold Pool lasted for six years, at which point it became impossible to maintain the $35/oz price and that effectively forced the U.S. off gold in 1971. In the 1970s, the gold price rose, eventually reaching $800/oz in 1980. In an attempt to contain the rising gold price, the International Monetary Fund and the U.S. sold gold during the late 1970s. In 1999, the price of gold bottomed at $250/oz, then started to bubble up.

As the price of gold started to rise, the U.S. inveigled countries like Canada, the United Kingdom and several others to sell their physical gold, in an effort to contain the price. When those overt gold sales failed to stop the price from rising, Western central banks moved to gold leasing. That was done so funds that were borrowing the gold could sell it to suppress the price. That came to an end when there was no more gold to lease, perhaps evidenced by the fact that U.S. cannot return just 300 tons of gold to Germany.

The final battlefield for the U.S. war on gold is being waged in the COMEX. Gold was down $480/oz during 2013, and on two days in April, it was down $246/oz, which is more than half the total drop in the gold price for all of 2013. The ratio on the COMEX of paper gold to physical gold is now effectively 100:1.

It seems to me the U.S. is running out of ammunition to suppress the price of gold, to convince people that the paper dollar is better than gold. All the physical gold has been moving to Asia. The war will end in 2014. The manipulation will be exposed for what it is. When that happens, the gold price will rise dramatically.

TGR: Is there any evidence that gold’s previous price performance can be used to forecast its future performance, or are we in uncharted territory?

IG: Whenever we have manipulation in markets it becomes much more difficult to make forecasts. For example, the stock market is being driven higher through massive monetary stimulus on the part of the central banks, particularly the Federal Reserve.

Our research demonstrates that cycles of secular bull and bear markets occur within what we call the longwave cycle seasons. We are now in the winter of the longwave cycle, when debt is effectively taken out of the economy. The central banks are resisting that process and have been since 2000. During the winter of the longwave season, gold is in a secular bull market and stocks should be in a secular bear market.

We’ve been in a secular bull market for gold and the gold stocks effectively since 2000. The HUI Gold BUGS Index bottomed at $35.50 in 2000; today it’s just above $200. The gold price bottomed at $251/oz and today is above $1,225/oz. Within these secular cycles there are long-term and intermediate cycles. Long-term cycles last between four and five years and there are four and a half of these long-term cycles in each secular cycle. I have written about how these cycles fit together; this can be seen on my website.

We should be in a price bottom of the 3rd long-term cycle and beginning the bullish phase of the 4th long-term cycle for precious metals and precious metals stocks. In my cycle work I have estimated that this bullish phase should take the price of gold to $3,300/oz and the HUI Index to $990 sometime early in 2017. It won’t be straight up; there will be intermediate corrections along the way.

TGR: Is 2014 the year that the financial system crumbles?

IG: I’m absolutely convinced that will happen this year. According to our cycle work, we’re in a currency crisis very much akin to the crisis of the last longwave winter during the 1931–1933 global currency crisis. I believe we will see world currencies fail this year. The euro and the dollar are going to be in jeopardy.

Out of that, a new world monetary system will evolve, much as it did at Bretton Woods in 1944. This will be a very difficult process as people lose faith in fiat paper currencies and turn to gold and silver.

TGR: Some people argue that this apocalyptic gold narrative does nothing to help gold stocks and gold investors. How do you respond to that?

IG: I think that is ridiculous. The world is facing an unprecedented fiat paper money currency crisis that can only end very badly. I know that gold goes up in the longwave winter as it did after 1929, and before that, after 1873. The price of gold rises because people no longer trust paper money.

The paper money fiasco is getting out of hand. France and Italy are teetering. When they collapse, it will be very difficult to keep the euro functioning as a currency.

I’m confident that the gold bull market is nowhere near over because in times of crisis gold becomes the money of choice. As I have already said, we are facing a mammoth crisis.

TGR: In a December 2013 issue of That Was the Week That Was, you noted some points made by Richard Schodde of MineEx Consulting when he compared the performance of juniors and seniors in mineral exploration in Canada and elsewhere since 1960. What were some of his findings?

IG: I think the most important thing we can take from his analysis is the importance of the junior companies in the exploration field. Between 1960 and 2012, 46% of the largest discoveries were made by junior companies. The juniors also were much more efficient than their senior counterparts in making those discoveries. It cost the juniors far fewer dollars to make discoveries similar to those made by the seniors.

TGR: If gold stays at around $1,200/oz, Schodde expects about $1.3 billion ($1.3B) to be spent annually on exploration in Canada. You help exploration companies arrange financing. How did 2013 compare with 2012 in that regard?

IG: Both were difficult years. Many junior mining companies are fighting just to survive. Toronto, the principle financial hub for the mining sector, was to a large extent put out of the financing game because the gold funds were experiencing significant redemptions and had to sell positions to make those payments. There was no money for financing.

I’ve noticed that Europeans and Americans along the eastern seaboard remain pretty active in financing the juniors. Europeans understand gold and they understand that paper currencies are in serious trouble.

TGR: Can you offer a couple of investable themes as 2014 begins?

IG: I’m extremely bullish on the gold price. The gold price will explode to the upside once it becomes apparent that the emperor has no clothes and no gold, and the war on the gold price ends. That means junior mining companies with good assets and good management will do likewise.

On the other hand I’m extremely bearish on the stock market simply because of my cycle work. Since 2000, we’ve been in a 2, 5, 2, 5 sequence: two years down, five years up, two years down and five years up. These are Fibonacci numbers and in cycles such numbers are very important. It suggests to me that the end is nigh for the stock market in 2014.

When that happens, the Federal Reserve will be out of ammunition to keep stock prices higher. Interest rates in the U.S. are essentially at zero and we’re pushing money at the rate of $75B a month into the major U.S. banks. When the market caves in, the Fed will be unable to bring it back because it has no room to cut interest rates. If the Fed keeps printing money at the current rate or increases it, the dollar will be under tremendous pressure. The Fed is caught between a rock and a hard place.

TGR: So, even if quantitative easing (QE) comes back, it won’t suffice.

IG: Increasing QE to induce money back into the stock market through the banks will destroy the dollar. Once that begins, interest rates have to rise and that will be the quandary facing the Fed.

TGR: Ian, thank you for your time and your insights as we head into 2014.

A globally renowned economic forecaster, author and speaker, Ian Gordonis founder and chairman of the Longwave Group, which comprises two companies—Longwave Analytics and Longwave Strategies. The former specializes in Gordon’s ongoing study and analysis of the Longwave Principle originally expounded by Nikolai Kondratiev. With Longwave Strategies, Gordon assists select precious metal companies in financings. Educated in England, Gordon graduated from the Royal Military Academy, Sandhurst. After a few years serving as a platoon commander in a Scottish regiment, he moved to Canada in 1967 and entered the University of Manitoba’s History Department. Taking that step has had a profound impact because, during this period, he began to study the historical trends that ultimately provided the foundation for his Long Wave theory. Gordon has been publishing his Long Wave Analyst website since 1998. Eric Sprott, chairman, CEO and portfolio manager at Sprott Asset Management, describes Gordon as “a rare breed in the investment-adviser arena.” He notes that Gordon’s forecasts “have taken on a life force of their own and if you care to listen, Gordon will tell you how it will all end.”

DISCLOSURE:

1) Brian Sylvester conducted this interview for The Gold Report and provides services to The Gold Report as an independent contractor.

2) Streetwise Reports does not accept stock in exchange for its services or as sponsorship payment.

3) Ian Gordon: I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

Streetwise – The Gold Report is Copyright © 2014 by Streetwise Reports LLC. All rights are reserved. Streetwise Reports LLC hereby grants an unrestricted license to use or disseminate this copyrighted material (i) only in whole (and always including this disclaimer), but (ii) never in part.

Streetwise Reports LLC does not guarantee the accuracy or thoroughness of the information reported.

Streetwise Reports LLC receives a fee from companies that are listed on the home page in the In This Issue section. Their sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

Participating companies provide the logos used in The Gold Report. These logos are trademarks and are the property of the individual companies.

Since the April 2013 gold meltdown there have been no less than half a dozen failed rallies in the gold miners – is this time different?

….read more HERE

Jim Rogers has one of the greatest track records in history…

He delivered a 4,200% return to investors of his legendary Quantum Fund in the 1970s… at a time when the U.S. stock market returned just 47%. And then he walked away from managing money.

Today, Jim and I agree on a major investment idea. We agree that the time has come to move a portion of your money OUTSIDE of the U.S. dollar… and into a place you’ve probably never considered.

I have a simple way to make the investment… and I believe it’s the safest place to park your cash over the next few years.

Jim is more ambitious. He believes it could be a triple-digit winner. Either way, it’s an idea you need to consider today.

Let me explain…

This summer, Jim predicted that China’s currency could soar by 300%, 400%, or even 500% against the U.S. dollar in the next couple decades. “If anyone wants to sell renminbi, I’d be willing to buy,” Jim said.

And just last month, Jim said he expects China’s currency to replace the U.S. dollar as the world’s most important currency in the next 20 years. (He is so optimistic about China, he moved his family from New York to Asia, and his young daughter now speaks fluent Mandarin.)

Anyone investing in China’s currency over the last few years has done well. Just this week, the dollar hit a new low versus China’s currency… the renminbi. In fact, the dollar has looked pretty bad against the renminbi over the last decade. Take a look:

Importantly, Jim and I both believe this trend will continue for one simple reason… China’s currency is deeply undervalued.

The renminbi is undervalued by 30%-50%, according to The Economist magazine.

China’s currency has appreciated 3%-4% per year in recent years. I think that’s our “base case” going forward. However, we might do much better than that in the coming years… thanks to Janet Yellen.

“There will be a prolonged period of appreciation for the renminbi,” Li Daokui, a former adviser to China’s central bank, said when he heard Yellen got the job. He knows Yellen will keep printing money and keep interest rates at zero for a “relatively longer period,” which would further weaken the dollar.

So we can expect to earn 3%-4% a year in profits simply by holding cash in China’s currency – with the potential for much bigger gains if smart people like Jim Rogers are right.

The easiest way to make the trade is through a U.S.-traded exchange-traded fund (ETF) that pays a 3.3% dividend.

I’m talking about the PowerShares Chinese Yuan Dim Sum Bond Fund (DSUM).

This fund holds a portfolio of “dim sum” bonds. A dim-sum bond is issued OUTSIDE of China, but it is IN China’s currency. This is exactly what we want.

With DSUM, you’ll earn a 3.3% dividend. PLUS, you’ll get the renminbi’s appreciation – around 3%-4% a year, maybe more. You may also see a capital gain as DSUM’s bonds increase in value. It could add up to 10% a year… in an income investment.

You MUST face the facts… You have too much of your wealth in the U.S. dollar…

Every day, our politicians are actively making the U.S. dollar more unattractive in global markets. Meanwhile, China is actively making its currency more attractive.

According to one of the best investors of all time – Jim Rogers – the renminbi could overtake the U.S. dollar within 20 years as the world’s most important currency. And he says it could go up in value by 300%, 400%, or 500% in the next couple decades.

You can choose to ignore this trend and see your wealth in U.S. dollars shrink. Or you can position a portion of your portfolio in China’s currency to take advantage of it. I recommend parking some of your cash outside the U.S. through shares of DSUM.

Good investing,

Steve Sjuggerud

Further Reading:

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair