Gold & Precious Metals

Gold lovers’ hearts are beating faster this week, as the metal rose above $1,300 an ounce for the first time since November. The precious metal also climbed above its 200-day moving average, which hasn’t happened in about a year.

ISI’s John Mendelson noted earlier this week that the generic gold future “rallied off its mid-December low and has decisively broken out above its downtrend line connecting the descending tops from late August, a near-term positive.” The next price he’s targeting is $1,350, the price gold was at in late October.

So while gold may correct over the next several months as the metal enters its seasonally weak period of the year, this looks promising for gold investors.

Here are a few more gold charts that just might have your heart beating faster:

1. The Love Trade Endures in the East

In January, 246 tons of gold were withdrawn from the Shanghai Gold Exchange, as China continues expressing its love for the precious metal. This marks a record level of gold deliveries on the exchange as well as a significant increase over the same time last year.

In addition, you can see on the chart below that January’s total also exceeds world mining production for the month.

As Ralph Aldis, portfolio manager of the Gold and Precious Metals Fund and the World Precious Minerals Fund, says, “Once the metal moves from the West and goes into China, we won’t get that gold back very easily.”

2. Money Supply Grew Faster in January

In the first month of 2014, the M2 money supply, which is a measure of money supply that includes cash, savings and checking deposits, grew faster than the previous two years. In 2012, M2 grew 7.6 percent and in 2013, money supply rose 4.7 percent; at an annualized rate, January’s money supply growth “reached an annualized rate of increase of 8.75 percent,” according to Bloomberg’s Precious Metal Mining team.

This may mean “the U.S. Federal Reserve is trying to resurrect inflation, thus increasing the appeal of gold, the supply of which can only increase about 1.5 percent to 2.5 percent annually,” says Bloomberg.

Last year, gold started to take it on the chin when the real rate of return went from a negative 0.62 percent in March to a positive 0.54 percent by December. Like I told Jim Goddard from HoweStreet, a positive real rate of return is typically a major headwind for gold.

Listen to the podcast of the radio show now.

Between March and December of 2013, two things happened: 1) Yields rose in anticipation that the Federal Reserve would begin tapering its bond purchases, and 2) the consumer price index declined. However, going forward, I anticipate that CPI will increase, and, given the modest economic growth we’ve been seeing in the U.S. economy, interest rates won’t be able to rise too quickly.

3. Gold Stocks Poised to Rebound After Rare 3-Year Loss

What I think is tremendously powerful for gold stock investors is this chart. At the beginning of January, we took a look back at the annual returns for the Philadelphia Gold & Silver Index. In three decades, there were only three times that gold stocks only saw a consecutive 3-year loss.

These aren’t the only gold charts to love. See more in my latest presentation from the World Money Show.

Lessons on Value Investing from the World’s Greatest Success Story

Lessons on Value Investing from the World’s Greatest Success Story

If you have been in the investing world for any period of time you are undoubtedly familiar with the man who many label as the greatest investor of all time – Warren Buffet. For those who require a little background, Warren Buffet is the self-made billionaire who built an empire through an unwavering focus on the simplest tenets of value investing. For nearly 50 years, Warren Buffet has earned prominence as the genius behind Berkshire Hathaway and has generated its investors a staggering average compound rate of return of 19.8% per year (1965 – 2011). This has resulted in an overall gain of 513,055%, compared to the S&P500 which returned 6,397% including dividends. An investment of $1,000 would have grown to over $5.1 million with the power of compounding returns.

Many detractors to Buffet’s value-investment style claim that his success cannot be replicated by individual investors. Often cited is Buffet’s solid reputation as a capital allocator and the deep investigative resources of his investment company Berkshire Hathaway. Undoubtedly Warren Buffet is a genius and we would not expect that any but the most gifted individuals would ever be able to replicate his success in its entirety. Nevertheless we can easily dispel the myth that reputation and resources were the ingredients to his success. Going back to 1956, before Buffet was a world famous billionaire (or millionaire for that matter), he was a relatively unknown man who operating his first investment partnerships out of an office in his bedroom. The limited partnerships were started with his own capital and a few some contributions from family and friends. He had no world renowned reputation, no staff of highly-skilled MBAs, and no special resources outside of himself. Buffet recognized the most basic and useful facets of valuing investing and applied the concepts to generate great success. Throughout the years he has participated in numerous interviews and writes a letter to his shareholders on an annual basis. Through these small snippets of information the general public has been able to gain some insight into how Buffet views the investing world. The following are a couple of his most well read quotes with a little insight into how anyone can use them to better far more intelligent investors.

“Price is what you pay. Value is what you get.”

Separating value from price is the most fundamental tenet of Buffet’s investment strategy. Pretty much everybody has a basic understanding of what the word “value” means but unfortunately this is rarely applied to investment decisions. There is a saying that most investors spend more time researching the purchase of their television set than they do their investments. This is largely due to a lack of knowledge and valuation skills which is why many investors rely on stock price movements as a signal of investment quality. When Buffet starts researching a stock he says he intentionally will not look at the market price. Instead he starts with valuing the underlying business as if it were a private company. He looks at the cash flow…he determines whether or not the business model is sustainable and if the earnings are being inflated by too much leverage (debt). Buffet then determines what we would pay for the actual company without any consideration for the fact that it is publicly-listed. If after making this determination the current stock price is significantly below his measurement of intrinsic value then he may move forward and make his purchase.

“I never attempt to make money on the stock market. I buy on the assumption that they could close the market the next day and not reopen it for five years.”

Don’t worry…nobody is planning on closing the market for the next five years. What Buffet is saying is that he doesn’t buy a stock with the intention of following the short-term market fluctuations and selling in and out on whims. When Buffet buys a stock, he is buying an ownership interest in an underlying company. This is largely the reason that Buffet is so successful. Rather than wasting his energy following day-to-day market oscillations (as many investors do), he focuses on the business that he has acquired and gauges success based on sustainable generation and growth of the underlying cash flow. Many businesses generate returns for their shareholders through the distribution of cash flow in the form of dividends. A successful company will also be able to grow their dividends over time. Eventually success is recognized in the markets. Although it can take time for value to be realized, there are very few examples of companies that produce strong and growing cash flow over time without either this eventually being recognized in the share price or by an independent buyer looking to acquire the company.

“We simply attempt to be fearful when others are greedy and to be greedy only when others are fearful.”

We are often asked by clients whether or not we utilize a timing strategy to move in and out of the markets with changes in the business cycle. Although market timing may appear to be a sound investment strategy, in practice, the results investors generate are far from astonishing. “Hindsight is 20-20, while foresight is legally blind”. The truth is that there are no magical indicators that will tell you (with consistent success) when to buy and sell stocks. If there were then we would expect to see at least one of these magical market timers (or technical analysts) on Forbes list of the world’s richest people (but we have not). Buffet as well does not subscribe to the traditional idea of market timing. He has however been able to apply his value investment methodology to creating a somewhat modified version of the strategy. If we take a step back to 2008 at the time of the stock market crash we will remember the fear that plagued the markets. Stock market prices dropped to levels not seen in over a decade causing private and professional investors to rush to the exits. Although fear was abundant and the outlook was grim, this was exactly the best time to be greedy with many very high-quality companies available for purchase at a fraction of their real value. If we go back to the summer of 2000, when the NASDAQ’s chart (along with the charts of many other exchanges) was nearly parabolic, investor optimism was high and greed pushed market valuations of internet stocks well beyond reasonable levels. This was undoubtedly a good time to be fearful. We would never suggest that you try and time the markets based on anyone’s assessment of market sentiment. This won’t produce any better results than any other market timing strategy. However, the next time market valuations have undergone expansion far beyond historical ranges, and experts are justifying the sentiment with the mantra “everything is different now”, you might want to consider separating yourself from the crowd and become a little more fearful.

“Success in investing doesn’t correlate with I.Q….. Once you have ordinary intelligence, what you need is the temperament to control the urges that get other people into trouble in investing.”

This has got to be my favorite quote from Warren Buffet. It gives hope to every ordinary investor who believes that they cannot compete with the pros. While Buffet is commonly referred to as the “smartest man in the room”, he himself openly confesses that his skills outside of capital allocation are fairly limited. And within this skillet Buffet utilizes only the simplest and most basic techniques in investment analysis. There are no super computers systems, no Nobel prize winning mathematicians, and certainly no new age strategies in the Berkshire Hathaway investment management office. The biggest asset (aside from their near $400 billion in capital) is their underlying philosophy that investment success is derived from purchasing high-quality, cash flow positive businesses at undervalued prices and holding those businesses over a long-term horizon. By controlling the emotions of fear and greed, individual investors can set themselves apart from the investment heard and create for themselves a very practical competitive advantage that the vast majority of people (including professionals) do not have.

Say you were in the market to purchase a private business. After months of searching you finally find an attractive opportunity. You are able to purchase a growing business, generating positive cash flow, with a solid and secure financial position, an effective and ethical management team, and a price that is significantly less than your assessment of the real intrinsic value. Assuming you are very positive on the long-term prospects of this new company and plan to own it long into the future, would you really care if the market of potential “private-business” acquirers dries up for a couple of years? You are not planning on selling the business and you are potentially benefiting from every dollar of cash flow that is generates (whether from dividends or ownership of a larger company in the event the cash flow is reinvested). In this situation, the astute business person would not spend their time following the day-to-day or minute-to-minute changes in the availability of potential acquirers.

|

KeyStone’s Latest Reports Section |

Disclaimer | ©2014 KeyStone Financial Publishing Corp.

As I expected, the US Fed pulled the trigger and announced an initial “taper” of the Quantitative Easing (QE) program. Starting this monthly purchases of T Bills and Mortgage Backed Securities will be reduced by $10 billion.

Equity markets rallied strongly then flattened as traders locked in profits and awaited earnings and fresh economic readings. Mom and Pop were piling into Wall St but no one who actually works there thought things look very cheap.

The gold market took a quick dive on the taper announcement and then regained its feet. It’s now trading above where it was then the taper was announced. After all the hand wringing why hasn’t the reaction been larger?

Traders with strong convictions about gold see it heading lower so they are out of the market, if not short. I don’t think there are a lot of new players in the market on the sell side.

It’s possible new sellers will appear each time QE is reduced but reactions should get smaller as traders accept QE is ending and price it in. On top of that you have a huge short position in gold that has to unwind sometime.

Every major brokerage house in North America is calling for lower gold prices. Even traditional gold bulls are hedging their bets and saying gold should have a final down leg to $1100. That level of unanimity is exactly what a contrarian wants to see. It’s very reminiscent of 2009 when HRA called a bottom on the big board in part because everyone though the market had to go lower.

Most brokers were wrong about gold prices year after year through most of this bull market. I don’t see a reason to believe they are suddenly more prescient.

Even gold bug commentary I’ve seen either warns about the end of QE or comes up with reasons why QE won’t be ended. Suddenly QE is the only reason the gold price moves.

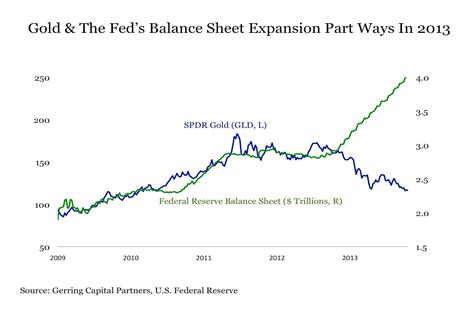

Few seem to have noticed that QE3 did nothing for the gold price. Take a look at the chart below comparing the gold price with the size of the US Fed’s balance sheet—a proxy for the cumulative amount of QE—since late 2009. There was some positive correlation during QE1 and QE2 but it’s been strongly NEGATIVE since the start of QE3.

QE isn’t “money printing” and does not affect the money supply in the manner most people expect. The confusion isn’t surprising. Even the Fed is unsure about the impact of its program. There have been recent studies by Fed economists that question the transmission mechanism and basic effectiveness of QE.

(From the January 29, 2014 HRA Journal: Issue 208-209 (Part I)

The Fed studies concluded that QE’s most important aspect is as a signaling tool. In other words, QE may be “working” because the Fed’s actions convince market participants that the Fed really, really means it when they promise to keep interest rates low.

The Fed creates money to complete QE transactions but it’s really an asset swap. In a QE transaction the Fed will purchase financial assets from a bank and pay for them with money (that is where the printing comes in). It doesn’t change the overall total of financial assets in the system but does change their composition. Banks have a higher cash total in their reserves and a smaller amount of Treasuries or approved mortgage debt.

So why isn’t there more money, and inflation, being created? Everyone who took Economics 101 remembers the “money multiplier”. Banks in a fractional reserve system would lend money to the extent allowed by their primary reserve requirements.

If a bank was required to hold 10% of its capital as reserves in cash or deposits with the Fed (as it is in the US) the bank could create ten times as many loans (which are assets to a bank) as its reserves on deposit. Creating those loans would generate new money on deposit in the banking system. It’s the private banking system that really grows the money supply.

In the simple macroeconomic models we all learned, bank lending and hence the money supply would increase in lockstep at ten times the rate of primary reserve increases. If bank reserves were increased by a trillion dollars the money supply would increase by ten trillion. That calculation underlies warnings about hyperinflation you hear from hard money advocates.

Pretty much EVERYONE uses the money multiplier argument to either rail against or praise QE. That includes Wall St, which is decidedly not full of hard money advocates. The problem is that this time honored measure doesn’t work.

If you look at the long term chart of US M2 money supply (currency in circulation, chequing/savings accounts and money market funds—basically) above you can see that its risen by about $3.4 trillion since the financial crisis. Not chump change.

The change in the Fed’s balance sheet since the start of the financial crisis (before the start of that chart on the previous page) is about $3 trillion. Using this very simplified but generally accurate comparison we get a “money multiplier” of about 1.1!

Even that lower multiplier assumes the Fed is the only actor in the economy. Some of the money supply growth is organic based on a slowly recovering economy. More importantly, it means there is no reason to expect a big inflation push because of QE alone or a big price collapse when the Fed backs out of it.

The potential money supply growth that worries traders really comes from bank lending. Banks do not have reserve constraints right now. In theory US banks could lend out trillions without having to even give a thought to their reserve ratio. Of course, they do have liquidity and solvency constraints, as many found out the hard way in 2008-2009. Bank are being very cautious and only starting to relax lending standards.

It’s not just about banks either. Even if banks were willing to lend to anyone they still need to find customers to borrow. Without credit demand there won’t be loan growth even if bankers are feeling reckless.

The lower chart on the next page shows year over year changes in US household credit demand, going back to 1970. Credit growth was never below 4% and averaged about 8% until 2007, and then it fell off a cliff.

Credit contracted from 2007 until H2 2013 as consumers retrenched. There was no net demand for new credit until a few months ago.

Credit demand is now positive again. This is borne out by consumer spending numbers. Spending has exceeded wage gains during several recent months and the savings rate is declining again.

Whether this is a “good” thing or not isn’t the point. If credit creation is the mother of money supply growth then we may start seeing money supply expansion now, even though the Fed is starting to taper.

The chart below shows inflation rates for major economies going back to the start of 2007. Inflation went to low (or negative) values in most major economies during the financial crisis. There was a recovery to a lower high then rates fell back again starting in 2011. This includes the US where the Fed was supposedly printing money like mad. If that was intended to inject inflation into the system it’s been a complete fail.

I’m cheering for inflation. I think moderate CPI (not just S&P, wine and modern art) price growth would be a good thing. There is no reason to fear it in developed countries. Inflation driven by money supply growth and/or higher capacity utilization will be the result of a higher growth track and higher confidence levels. I think there is a shot at that this year. Not great growth rates but better ones at least.

I’m not expecting much when it comes to inflation but it could at least begin to trend up rather than down. I certainly hope it does. There isn’t much room to maneuver on the downside and other areas, particularly the EU, could still see outright deflation if we screw this up.

So what does this mean for major markets and gold? The biggest fear in both of those markets is that “tightening” by the Fed will drive up yields and compete with both gold and equities.

Yields have moved up since early last year but the Fed’s done a good job of talking down market so far. Even with the start of tapering announced 10 year yields have held below 3%. I’m sure they will go higher this year but not to real danger levels. I expect we see 10 year yields at something like 3.5-4%, enough to be a headwind for the markets but not enough to derail them. The Fed isn’t likely to be actually selling bonds until late this year at the earliest. Yes, the Fed has a lot of debt to unload but we need to keep the amount in perspective. The US debt market does about $800 billion in daily volume and bid to cover ratios for recent US debt auctions have been good. I don’t see the Fed blowing this market up.

Its orthodox belief among hard money advocates that there will be a debt collapse. Is it possible? Sure. Is it likely? No. It would be better if the US (and everyone else) got debt levels down but a country that can issue 10 year paper in its home currency that yields 3% does not have a shaky debt market.

Mortgage debt is a little trickier but only by degree. The Fed is a bigger part of this market but there is no need to just sell indiscriminately. Reversing mortgage debt purchases can be stretched out too.

Yellen will spend a lot of time convincing the market there will be no near term rate increase. As long as they don’t screw up the messaging there shouldn’t be a debacle here. So far its working though I think we can thank a skittish market for that rather than superior communication skills of Fed governors.

If the US growth accelerates a bit bond yields should naturally lift anyway. Higher yields due to higher confidence are a good thing, especially if it is accompanied by a mild upturn in inflation.

The bottom line is that I don’t expect a contraction in money supply or exploding bond yields because of QE being rolled back. Either of those would be damaging to the gold market and equities. The money supply might even expand faster this year if the mood of consumers and banks continues to improve.

Higher capacity utilization is needed to give companies the confidence to increase prices. That, and wage gains, is the most direct route to CPI numbers that are increasing rather than decreasing every month. Real interest rates are what matter. A small increase in inflation accompanying an increase in bond yields won’t generate any panic.

Inflation last year decreased in large part due to lower energy prices. That increased the real yield on Treasuries which may have helped on the demand side even as traders worried about QE. Most energy analysts believe the US can get to oil self-sufficiency if the production growth of the past few years continues. This may lead to lower prices that keep inflation subdued though it’s the core rate—which excludes energy and food prices—that I expect to see getting a bit stronger.

Even if you’re convinced unwinding QE will lead to disaster it will be some time before the Fed is selling bonds. The Fed is reinvesting interest paid on its current holdings which is adding another $25 billion a month to the purchases, more or less.

It’s unlikely the Fed will be actually selling debt before 2015 and I’m sure they will watch bond yields like a hawk. I doubt the Fed will be a seller unless yields are stable. Yellen may be more cautious than Bernanke but remember there are several new voting members on the Fed committee. Most are hawks that will resist extending QE.

Ω

….go HERE to read Part 2

The HRA–Journal and HRA-Special Delivery are independent publications produced and distributed by Stockwork Consulting Ltd, which is committed to providing timely and factual analysis of junior mining, resource, and other venture capital companies. Companies are chosen on the basis of a speculative potential for significant upside gains resulting from asset-based expansion. These are generally high-risk securities, and opinions contained herein are time and market sensitive. No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer, solicitation or recommendation to buy or sell any securities mentioned. While we believe all sources of information to be factual and reliable we in no way represent or guarantee the accuracy thereof, nor of the statements made herein. We do not receive or request compensation in any form in order to feature companies in these publications. We may, or may not, own securities and/or options to acquire securities of the companies mentioned herein. This document is protected by the copyright laws of Canada and the U.S. and may not be reproduced in any form for other than for personal use without the prior written consent of the publisher. This document may be quoted, in context, provided proper credit is given.

©2014 Stockwork Consulting Ltd. All Rights Reserved.

Published by Stockwork Consulting Ltd.

Box 85909, Phoenix AZ, 85071

Toll Free 1-877-528-3958

I have just an exclusive report on silver covering some fundamentals and technical analysis as to why silver is about to explode for Silver-Phoenix500.com which is a must read…

I have just an exclusive report on silver covering some fundamentals and technical analysis as to why silver is about to explode for Silver-Phoenix500.com which is a must read…

Now that the silver, gold and mining stock bull market has returned my focus will be more on opportunities in the precious metals sector again as it was during the last PM bull market.

Read this major report that is complete with trading ideas and opportunities.

Exclusive Silver Investing Report:

http://www.silver-phoenix500.com/article/silver-global-price-forecast-sterling-opportunity

Chris Vermeulen

Author of “Technical Trading Mastery – 7 Steps To Win With Logic“

I would also like to note that in celebration of the the new precious metals bull market and Valentines day you get get a full year of my trade alerts and trading portfolio at the price of a 6 month membership today! Subscribe Today and Start Profiting from Gold and Silver!

Subscribers of my newsletter are up over 10% on our silver position this week already…

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair