Timing & trends

“Connecting bright, ambitious young people with wealthy individuals who want to invest in their futures.”

“Connecting bright, ambitious young people with wealthy individuals who want to invest in their futures.”

The Dream Machine

The stated goal of Upstart is to connect bright, ambitious young people with wealthy individuals who want to invest in their futures — and, with any luck, help them achieve their dreams. “Upstart was founded to help people do what they were meant to do,” the company announced at its launch in August 2012. “Many talented college grads take jobs they’re not excited about, rather than following their true passions. Whether constrained by debt or just comforted by traditional career options, too many students take the perceived ‘safe path.’”

‘What makes human capital contracts unique is that the investment made is not in a particular company or idea, but in a person. After all, supporters argue, companies are no more than the product of the people who create them. So why not simplify the investment process? Why not treat the person as the startup — or, by Girouard’s clever inversion — the upstart?”

….continue reading A Group Of Investors Is Buying A Stake In The Next Generation Of Geniuses

As it tries to punish Russia for the latter’s dismemberment of Ukraine, the West is discovering that the balance of power isn’t what it used to be. Russia is a huge supplier of oil and gas — traded in US dollars — which gives it both leverage over near-term energy flows and, far more ominous for the US, the ability to threaten the dollar’s rein as the world’s reserve currency. And it’s taking some big, active steps towards that goal. As Zero Hedge noted on Tuesday:

Russia Prepares Mega-Deal With India After Locking Up China With “Holy Grail” Gas Deal

Last week we reported that while the West was busy alienating Russia in every diplomatic way possible, without of course exposing its crushing overreliance on Russian energy exports to keep European industries alive, Russia was just as busy cementing its ties with China, in this case courtesy of Europe’s most important company, Gazprom, which is preparing to announce the completion of a “holy grail” natural gas supply deal to Beijing. We also noted the following: “And as if pushing Russia into the warm embrace of the world’s most populous nation was not enough, there is also the second most populated country in the world, India.” Today we learn just how prescient this particular comment also was, when Reuters reported that Rosneft, the world’s top listed oil producer by output, may join forces with Indian state-run Oil and Natural Gas Corp to supply oil to India over the long term, the Russian state-controlled company said on Tuesday.

Rosneft CEO Igor Sechin, an ally of President Vladimir Putin, travelled to India on Sunday, part of a wider Asian trip to shore up ties with eastern allies at a time when Moscow is being shunned by the West over its annexation of Crimea. Rosneft said it had also agreed with ONGC they may join forces in Rosneft’s yet-to-be built liquefied natural gas plant in the far east of Russia to the benefit of Indian consumers.

We just have one question: will payment for crude and LNG be made in Rubles or Rupees? Or in gold. Because it certainly won’t be in dollars.

Rosneft, which is increasing oil flows to Asia to diversify away from Europe, did not provide any additional details but said it had discussed potential cooperation with Reliance Industries and Indian Oil.

It did not have to: it is quite clear what is going on. While the US is bumbling every possible foreign policy move in Ukraine (and how could it not with John Kerry at the helm), and certainly in the middle east, where it is alienating Israel and Saudi just to get closer to Iran, Russia is aggressively cementing the next, biggest (certainly in terms of population and natural resources), and most important New Normal geopolitical Eurasian axis: China – Russia – India.

There is only one country missing – Germany. Because while diplomatically Germany is ideologically as close to the US as can be, its economy is far more reliant on China and Russia, something the two nations realize all too well. The second the German industrialists make it clear they are shifting their allegiance to the Eurasian Axis and away from the Group of 6 (ex Germany) most insolvent countries in the world, that will be the moment the days of the current reserve petrocurrency will be numbered.

To understand why trade deals between Russia, China and India are potentially huge, a little history is useful: Back in the 1970s, the US cut a deal with Saudi Arabia — at the time the world’s biggest oil producer — calling for the US to prop up the kingdom’s corrupt monarchy in return for a Saudi pledge that it would accept only dollars in return for oil. The “petrodollar” became the currency in which oil and most other goods were traded internationally, requiring every central bank and major corporation to hold a lot of dollars and cementing the greenback’s status as the world’s reserve currency. This in turn has allowed the US to build a global military empire, a cradle-to-grave entitlement system, and a credit-based consumer culture, without having to worry about where to find the funds. We just borrow from a world voracious for dollars.

But if Russia, China and India decide to start trading oil in their own currencies — or, as Zero Hedge speculates, in gold — then the petrodollar becomes just one of several major currencies. Central banks and trading firms that now hold 60% of their reserves in dollar-denominated bonds would have to rebalance by converting dollars to those other currencies. Trillions of dollars would be dumped on the global market in a very short time, which would lower the dollar’s foreign exchange value in a disruptive rather than advantageous way, raise domestic US interest rates and make it vastly harder for us to bully the rest of the world economically or militarily.

For Russia, China and India this looks like a win/win. Their own currencies gain prestige, giving their governments more political and military muscle. The US, their nemesis in the Great Game, is diminished. And the gold and silver they’ve vacuumed up in recent years rise in value more than enough to offset their depreciating Treasury bonds.

The West seems not to have grasped just how vulnerable it was when it got involved in this latest backyard squabble. But it may be about to find out.

For Part 1-13 of The Currency War read HERE

About Dollar Collapse

About Dollar Collapse

DollarCollapse.com is managed by John Rubino, co-author, with GoldMoney’s James Turk, of The Collapse of the Dollar and How to Profit From It (Doubleday, 2007), and author of Clean Money: Picking Winners in the Green-Tech Boom (Wiley, 2008), How to Profit from the Coming Real Estate Bust (Rodale, 2003) and Main Street, Not Wall Street (Morrow, 1998). After earning a Finance MBA from New York University, he spent the 1980s on Wall Street, as a Eurodollar trader, equity analyst and junk bond analyst. During the 1990s he was a featured columnist with TheStreet.com and a frequent contributor to Individual Investor, Online Investor, and Consumers Digest, among many other publications. He currently writes for CFA Magazine.

The Dow rose 91 points yesterday. Gold was flat – after getting battered last week.

The Dow rose 91 points yesterday. Gold was flat – after getting battered last week.

Today, we go even farther into the unknown… beyond eventually and past sooner or later… to what happens next.

Specifically, we don’t think central bankers are going to take the end of the world lying down. They’ve got tricks up their sleeves. These are not new tricks. They’ve been used many times in many different forms. But they’ve never been used on the scale we now foresee.

But before we begin guessing, let us tell you a bit about what is really happening here at Finca Gualfin, our ranch here in northwestern Argentina.

Three days ago, Jorge – the farm manager – came to us with a problem:

“Señor Bonner, we found two calves dead. They looked fat and healthy. I’m afraid it is a disease called la mancha. I saw it many years ago. Healthy young cows just all of a sudden fall down and die. It almost wiped out our herd.”

We still don’t know what la mancha is. But it is evidently not something to trifle with. Word went to Salta, a city about six hours away, that we had an emergency. A veterinarian advised us to inoculate the whole herd. Within hours, the medicine was on a bus bound for the hamlet of Molinos, about an hour and a half from the ranch.

The next morning, all the hands were turned out – including your editor. We mounted up and headed out to the campo – an immense valley of some thousands of acres. Our job was to sweep the valley of all the cows…driving them to the main corral, where they would be vaccinated.

The operation took three days. Your editor was probably more of a liability than a help. Driving cattle is not as easy as the local gauchos make it look.

When the Debt Bubble Pops

Meanwhile, away from the ranch…

The end of the world comes when the debt bubble pops. But before we get there, we will see more attempts by central banks to keep the debt bubble expanding. From Richard Duncan, author of The New Depression: The Breakdown of the Paper Money System:

Given that the Fed has been driving the economic recovery by inflating the price of stocks and property, it is unlikely to allow falling asset prices to drag the economy back down any time soon. To prevent that from happening, it looks as though the Fed will have to extend QE into 2015 and perhaps significantly beyond.

So far, so predictable. But there is a “sooner or later” for QE, too. There will come a time when the world can take no more debt… and at that point, the debt bubble will finally blow up.

Then we get the equal and opposite reaction. Asset prices that have been inflated by debt will be deflated by debt de-leveraging. A depression will most likely follow.

This is not a bad thing… not at all. Contrary to popular opinion, crashes and depressions do not destroy wealth. They merely tell you that the wealth you thought you had really didn’t exist.

As long as the EZ money flows freely, mistakes remain invisible. Rotten companies are kept alive. Bad speculations seem to pay off. Debts that can never be paid are still serviced. Stocks with little or no earnings shoot up.

Then when the bubble explodes the mistakes become painfully obvious. Phony gains return from whence they came. Investors reprice assets at more realistic levels. (After first going to unrealistically low levels and presenting opportunities for patient investors with plenty of cash onboard).

Only then, when the economy has been thoroughly thrashed can it get up, dust itself off and get back to work.

But central bankers are not likely to let it happen. They’ve made their careers by pretending to improve the economy. When the bust comes they will swing into action with more quack cures.

That is when we arrive at the second stage of the coming debt deflation. It is when we will wish we had bought more gold… more real estate… more old cars and new potatoes.

Most likely (but this is not guaranteed) central banks will find new and bolder ways to get money into consumers’ hands. (Remember Ben Bernanke’s “helicopter” speech?) This will be followed by a crisis of a different sort: high levels of consumer price inflation.

Put on your seat belt. It’s gonna be one helluva ride.

Regards,

Bill

Wall Street’s Dirty Secret

From the desk of Chris Hunter, Editor-in-Chief, Bonner & Partners

Wall Street has a dirty secret…

On average, over a five-year period, about 25% of actively managed funds outperform their indexes.

That’s just one in four funds that do a better job, on average, than an index-tracking ETF or passive mutual fund.

Another roughly 25% will underperform by a small amount. Another roughly 25% will underperform by a large amount. And another roughly 25% will shut up shop before five years is over.

In other words, by investing in actively managed funds you are giving yourself 3-to-1 odds of underperforming a passive index.

Here are the results from the S&P Indices Versus Active Funds (SPIVA) US Scorecard for 2013. It shows the percentage of active funds outperformed by the index over five years ending 2013.

As you can see, for the five years ending in 2013, small-cap funds did slightly better than usual. The small-cap index outperformed just 66.8% of them for the period. Large-cap funds did a couple of percentage points better than the average. And mid-cap funds did slightly worse than average.

This is strong evidence that you’re far better off holding plenty of diversified passive index funds in your portfolio, than chasing after elusive… and expensive… actively managed funds.

Of course, you can seek out some outperformance with a small portion of your portfolio… by stock picking or getting someone else to stock pick for you.

Just be aware that the odds are heavily stacked against your beating a passive-investing strategy over the long run.

This spike in short-term yields (2-year shown) is what harpooned gold last week and finally got it under control.

More importantly, this spike in the 2-year vs. the 30-year really hurt gold.

These spikes predictably came as the FOMC successfully managed to get the market thinking about an end to the damaging Zero Interest Rate Policy, ZIRP.

Interlude

Yes, it is that time again when the letter writer veers off course into a brain dump. You, dear long time subscriber, have heard this before. But for newer subscribers I feel a point needs to be made so that your expectations of this market report are well in line with its raison d’être.

This is not a ‘go gold!’, ‘got gold?’ style pump house. Simply stated, I would rather live in a world where I do not feel gold is a necessary asset class. I would rather live in a world where bureaucrats were not in control of interest rate functions and hence, to some degree in control of financial markets.

Under this interest rate manipulation, the concept of saving has been utterly torn apart in the United States via the now 5+ year old ZIRP. If you do not speculate, you do not profit. The problem is that the risks in speculation are rising with every lurch higher in the stock market and junk bonds, to name two of the primary beneficiaries.

So it’s everybody into the (risk) pool and everyone foolish enough to depend on savings… screw you. So I [omitted, not for public consumption] because I continue to unwaveringly believe that this big macro operation, going in one form and degree of intensity or another since 2001, is little more a than racket to be unwound.

But if the moment were to come when I feel we really are on the right track – and folks, withdrawing ZIRP [could] theoretically at least be considered one component of ‘on the right track’ – this market report would simply move on from the precious metals sector because frankly, I find it a strange place inhabited by some strange people.

The problem though is partially represented by the distortion built into this chart…

Something is just not right here. Long into an economic recovery and even longer into a bull market in stocks the Fed Funds rate (FFR) is still pinning T Bill yields to the mat. Now, the Fed Chief babbles about a rate hike out in 2015, “that type of thing”. Gold then reverses its ascent (it was ripe, given the Ukraine hype coming out of the gold ‘community’) on the implications of rising short-term yields.

Using the 2003-2007 bull market as a template, the FFR should have begun to rise in 2010. Now it is 4 years later than that and the Fed is talking about a rate hike out in 2015, “that type of thing”. Please. They are playing poker against the market and for now the market is not calling any bluffs.

Back on the Funda’s

So last week we had a group of interest rate manipulators meet for 2 days and then a press conference by the group’s leader. She “you know” intimated that the ideal timing to begin phasing out ZIRP would be approximately “you know” sort of like maybe 6 months after QE3 is entirely tapered. “You know”, if the economy is still strengthening then; that sort of thing.

Okay tell me now, who knows what the economy will be doing then? As things stand now last week was a negative for gold, which was in need of a correction. But the key question going forward will be whether or not these negatives will endure or go back to business as usual as FOMC day fades to background?

So the long-term / short-term interest rate fundamental dropped to its lowest point of the gold bear market last week. What can we conclude from that?

- Gold’s fundamental underpinning took a hit.

- When measuring the length of the sideways channel on the yield spread, we note that gold may have already discounted this drop as its price is much lower than it was in summer of 2012 when the spread first declined to 80.

- The yield spread, driven down by a jawbone and a lot of market emotion and media hype last week is at a potential bounce point.

So fundamentally speaking, gold bugs want to see last week’s hysterics fade pretty quickly and by extension, the spread hold the support area (notwithstanding a day or two of down spiking for good measure).

If the market comes to believe that the Fed means business on the Funds Rate and 2, 3, 5 year yields continue to rise relative to long-term yields, it would be bearish for the price of gold. I make the distinction between “bearish for the price of gold” and ‘bearish for gold’ because price is a reflection of the value assigned to gold at any given time.

For as long as it lasts, a phase where the market perceives itself to be under the sound monetary stewardship of the Fed – regardless of sustainability – would be gold price bearish.

Of course last week may have been a flash in the pan, as the Fed got the respect it always seems to get from the market during the ongoing phase of stock mini mania and economic mini revival. There are other phases you know, when the market gives them the finger. That is out in the future.

Let’s watch the dust settle on the interest rate front and evaluate weekly.

Postscript (current, 3.25.14)

So tell me, what was China doing late last week and early this week as gold got harpooned? Did gold suddenly decline because of the much hyped ‘China demand drop’? Did supposedly massive physical demand suddenly dry up on the spur of a moment? There’s always a seller on the other end of that demand you know.

Ukraine hyperbole unwound and that was expected to take something off the top. But chasing funnymentals like China, physical demand (vs. COMEX shortages) and Ukraine around is what got the gold community in trouble in the first place.

There is no debate, real interest rates jumped last week and gold got clobbered. There are other key fundamentals as well. Unfortunately with the media just pumping out story after story it is no wonder people get so confused.

NFTRH is a serious market management service (including ‘in-week’ technical updates), and is a value at only $29 per month (or 10%+ savings on an annual subscription).

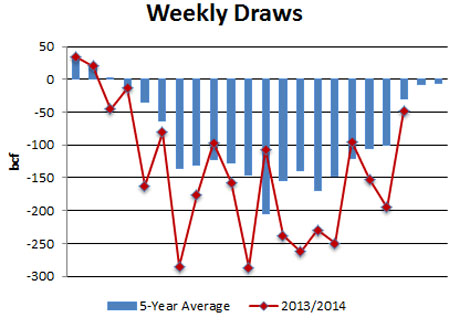

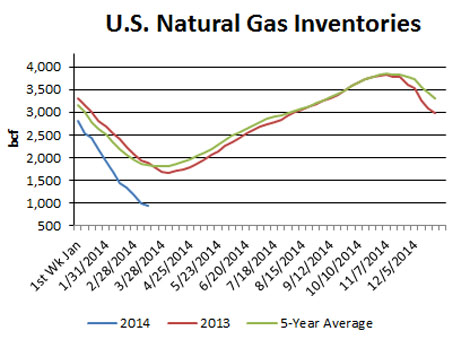

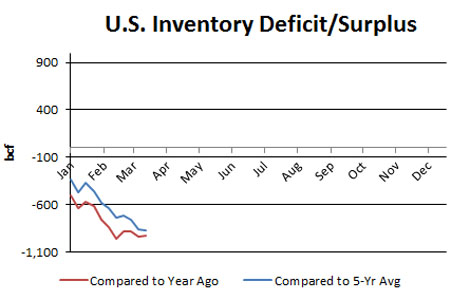

Natural gas inventories fell by 48 bcf last week, below expectations.

Natural gas inventories fell by 48 bcf last week, below expectations.

Natural gas was last trading higher by close to 3 percent to $4.35/mmbtu after the Energy Information Administration reported that operators withdrew 48 billion cubic feet from storage last week, below the 55 to 60 bcf that most analysts were expecting.

The latest withdrawal was below last year’s draw of 62 bcf, but above the five-year average draw of 30 bcf.

In turn, inventories now stand at 953 bcf, which is 923 bcf below the year-ago level and 875 bcf below the five-year average (calculated using a slightly different methodology than the EIA).

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair