Personal Finance

When was the last time you bought a stock that gained over 1,000%?

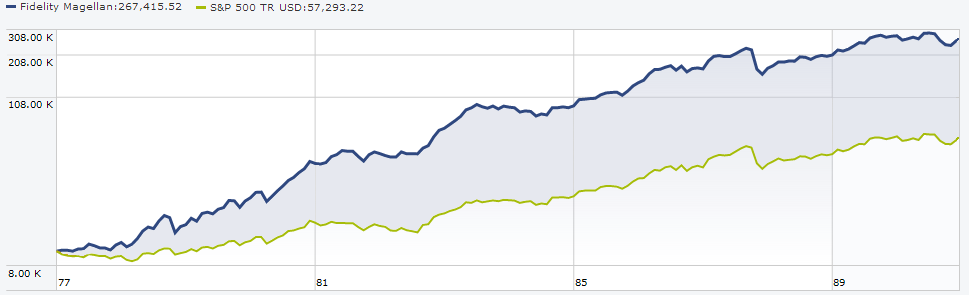

Peter Lynch bought more than a hundred of them during his 13-year stint as head of Fidelity’s Magellan fund.

He called them “ten baggers” – stocks that increased in price more than tenfold. Some of his best picks include Fannie Mae, Ford Motor, Philip Morris, Taco Bell, Dunkin’ Donuts and General Electric to name a few.

Combining Growth and Value

Peter Lynch is best described as a growth/value investor. And his 29.2% annualized return over 13 years at Fidelity makes him the greatest mutual fund manager of all time. But what made him a true legend?

After stepping down from the Magellan throne, Lynch shared his secrets with retail investors.

His best-selling books, One Up On Wall Street and Beating the Street, laid out his investment process in clear and concise detail. Through these works, he taught small investors how to achieve market-beating success by using knowledge they already possessed.

His famous investment philosophy is simply, “Invest in what you know.” Since most people tend to become experts in a particular field, Lynch believed this basic principal could help individual investors find good undervalued stocks.

What separates him from other growth stock investors is his discipline to buy only at reasonable prices. This combination of growth and value made him a legendary stock picker.

Price Follows Earnings

Peter Lynch’s primary focus was on earnings, knowing that stock prices follow earnings over a large time frame. By buying shares when the price was temporarily depressed in relation to their earnings, he was able to profit from both the correction in price and the hopeful continuation of growth.

Avoid Hot Stocks

Lynch also avoided “hot” stocks and sectors. This included an avoidance of technology producers and seldom exposure to the energy markets. Even though he missed the boat on Apple and a few other tech giants, Lynch assures us that the losses from investing in these sectors would have far outweighed any potential gains.

Peter Lynch’s Investment Formula

He instead looked for simple companies with better-than-industry numbers and demonstrating the following investment metrics:

P/E Ratio

His now-famous “Peter Lynch chart” plotted a stock’s price against its historical earnings line – a theoretical price at 15 times earnings. He stated, “A quick way to tell if a stock is overpriced is to compare the price line to the earnings line. If you bought familiar growth companies – such as Shoney’s, The Limited, or Marriott – when the stock price fell well below the earnings line, and sold them when the stock price rose dramatically above it, the chances are you’d do pretty well.”

PEG Ratio

Lynch was a firm believer that investors should only buy stocks when the P/E ratio was below the company’s historical growth rate. This equates to a PEG ratio below 1 and ensures that investors do not overpay for stocks. We should be willing to “pay up” for fast growing companies, but not to absurd levels that will inhibit future returns.

Debt to Equity

The primary cause of business failures is an unsustainable debt load. Mr. Lynch maintained that companies should carry as little debt as possible and remain below the corporate average of 35%.

Inventory to Sales

For producers of physical goods, one of the early warning signs of diminishing returns is a buildup of excess inventory. By monitoring the inventory to sales ratio’s change on a year to year basis, investors have a better chance of identifying enterprises suffering a deterioration of their supply/demand curve.

Net Cash Position

Companies holding large cash reserves offer a greater margin of safety during economic hardships. Calculated by subtracting total liabilities from cash and equivalents, Lynch viewed the net cash position as a bonus. While not a necessity for favorable results, it adds an additional level of security to any common stock investment.

Charlie Tian, Ph.D.

Founder, GuruFocus.com

The Monthy Peter Lynch Portfolio 29 newsletter offer is HERE (scroll down to read the offer)

Separate and Unequal

In a note last week, I discussed the danger in assessing all critical metals together rather than individually. I am just back from Montreal where I chaired the 6th Annual Lithium Supply and Markets Conference hosted by Industrial Minerals.

Of the many takeaways, this idea of analyzing the prospects for these metals individually is evident in the case of lithium.

In the wake of Tesla’s (TSLA:NASDAQ) Gigafactory announcement, many lithium junior companies, who were left for dead, have been given a new lease on life. There are challenges that must be overcome to make the Gigafactory a reality, and am still unconvinced that a junior mining company not close to production can participate and benefit its shareholders, but we shall see. On the other hand, I try and make a habit of betting on successful visionaries like Elon Musk.

It is clear that the automotive sector is the real growth driver for lithium, as David Merriman of Roskill pointed out in his remarks:

It is important to remember that although electrified vehicles accounted for just 2% of global auto sales in 2013, this number was 1% as recently as 2011. Anyone who has driven any type of EV knows that this technology could gain widespread adoption subject to better economics (or higher gas prices).

What Happened to Leverage?

It is most surprising that despite the bloodbath in the junior lithium sector, lithium prices have held steady (roughly $6,000 per tonne depending on the purity for battery grade). Demand has continued to increase on an annualized basis to approximately 168,000 tpy in 2013. According to Dr. Jon Hykaway of Stormcrow, one of the conference speakers and a widely followed expert in the critical metals space, demand has grown by 80% in the past 5 years.

Unfortunately most lithium juniors haven’t benefitted from this stability and growth. Their share prices have collapsed by 72% as a group since 2011 according to Luis Santillana, CFO of Li3 Energy (LIEG:OTCBB).

It is a widely held view that junior mining companies gain from their discoveries and from leverage associated with higher raw materials (in this case lithium) prices. Why then can’t most lithium juniors seem to get back on their feet without the help of Elon Musk?

This likely has to do with a point I have made in the past regarding the lithium markets. The lithium market is an oligopoly. Realistically, this is a market well supplied by a small number of participants and despite the growth projections for the industry (something which I believe in over the long term), it is also a well supplied market.

Talison Lithium, a company that performed very well for our subscribers, has tailings at its Greenbushes mine with a reported higher grade than many other hard rock projects throughout the world. Facts like these give end users and other participants along the value chain pause when considering which early stage plays to fund. It is for reasons such as this that lithium juniors have suffered in the face of a healthy lithium market; while demand is steady, current supply is ample.

Another complicating factor is that an exorbitant amount of R&D dollars are being allocated towards battery technology calling into question exactly what the “winning” battery chemistry will be. It is clearly a challenge for end users or battery manufacturers to make large capital budgeting decisions when a question of this magnitude looms large. That said, the general consensus from the conference was that lithium ion battery technology is currently the best available. Nobody in attendance saw this changing anytime soon. Even if it were to, the time it would take for new supply chains to be built and new materials to be integrated into them is substantial, confirming the steady growth profile for lithium in the coming years.

I Have Said this Before: Don’t Throw the Baby Out With the Bathwater

Despite the uncertainties I mentioned above, avoiding lithium juniors altogether would be a mistake. We are still at the bottom of this cycle with an inflection point perhaps two years away. Lithium is an exciting commodity with a number of additional avenues of demand. This hedge against a fall off in demand from one sector is a very important benefit.

Given our focus on disruptive discovery, lithium must be viewed in this context. Now is not the time to indiscriminately begin acquiring a basket of lithium junior mining companies, but I do believe there are those in the sector that are well positioned for success.

Strong balance sheets and projects in stable political jurisdictions coupled with strategic alliances or potential for lowering production costs are the keys at this stage of the cycle.

During the conference, we learned about several technologies including solvent extraction which can help achieve lower costs. In addition to this, POSCO (005490:KRX, PKX:NYSE) one of the largest global players in the steel business, has made significant inroads into dominating the downstream lithium industry. POSCO has relationships with several lithium junior mining companies and one in particular I am conducting advanced due diligence on as the combination of this company’s management, balance sheet, asset, and POSCO’s potential low cost lithium production technology make it unique amongst its peers.

Takeaways

With or without the Gigafactory, the future for lithium across multiple industries appears sound. Everyone who has experienced driving an EV (as I have) knows that this technology can become a more widespread commercial reality in the future, although calls for the death of the internal combustion engine are certainly premature. That doesn’t mean that every lithium junior will succeed (or deserves to). Given ample supply of the commodity itself, investors must find those stories which have the right blend of sustainability and upside catalysts as the global economy works through the current disinflationary environment.

The material herein is for informational purposes only and is not intended to and does not constitute the rendering of investment advice or the solicitation of an offer to buy securities. The foregoing discussion contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 (The Act). In particular when used in the preceding discussion the words “plan,” confident that, believe, scheduled, expect, or intend to, and similar conditional expressions are intended to identify forward-looking statements subject to the safe harbor created by the ACT. Such statements are subject to certain risks and uncertainties and actual results could differ materially from those expressed in any of the forward looking statements. Such risks and uncertainties include, but are not limited to future events and financial performance of the company which are inherently uncertain and actual events and / or results may differ materially. In addition we may review investments that are not registered in the U.S. We cannot attest to nor certify the correctness of any information in this note. Please consult your financial advisor and perform your own due diligence before considering any companies mentioned in this informational bulletin.

The information in this note is provided solely for users’ general knowledge and is provided “as is”. We at the Disruptive Discoveries Journal make no warranties, expressed or implied, and disclaim and negate all other warranties, including without limitation, implied warranties or conditions of merchantability, fitness for a particular purpose or non-infringement of intellectual property or other violation of rights. Further, we do not warrant or make any representations concerning the use, validity, accuracy, completeness, likely results or reliability of any claims, statements or information in this note or otherwise relating to such materials or on any websites linked to this note. I own no shares in any company mentioned in this note.

The content in this note is not intended to be a comprehensive review of all matters and developments, and we assume no responsibility as to its completeness or accuracy. Furthermore, the information in no way should be construed or interpreted as – or as part of – an offering or solicitation of securities. No securities commission or other regulatory authority has in any way passed upon this information and no representation or warranty is made by us to that effect. For a more detailed disclaimer, please see the disclaimer on our website.

Briefly: In our opinion speculative short positions (half) in gold, silver, and mining stocks are justified from the risk/reward perspective.

The history repeats itself and we have just seen another example confirming this statement. Gold once again moved higher initially but failed to hold its gains even until the end of the session. This made yesterday’s session very similar to May 19. The intra-day high was once again lower. Before discussing this situation, let’s take a look at the USD Index:

The USD Index moved a bit higher yesterday, which made the situation more bullish – that was a first daily close above the declining resistance line. We don’t think that this move makes the breakout confirmed yet – we’ll wait for 2 more consecutive closes above this line before saying that. However, it’s some kind of improvement and the implications for the precious metals market are a bit more bearish. They will likely be much more bearish once the breakout in the USD is confirmed.

Yesterday we wrote that the intra-day reversal that had taken place on relatively big volume was much less significant than it appeared at the first sight because it was not confirmed by spot gold and because gold was simply reflecting the U.S. dollar’s movement. We wrote that the strength that we could see here would likely be temporary. It turned out that the rally that this reversal generated was indeed very small and temporary.

We saw another lower intra-day high in gold, and the move higher materialized on low volume. We’re once again seeing this bearish combination. If the USD Index confirms its breakout, gold might finally break below the short-term support.

How far can it go initially? Our best guess at this particular moment (this might change as the situation develops) is the $1,200 level or close to it. One of the ways to estimate the size of a given move is to assume that the move following the consolidation (which we’ve been seeing since the beginning of April) will be similar to the one preceding it. In this case, the move following the breakdown could be similar to the March decline, and such a move would take gold close to the $1,200 level. This level is very close to the 2013 lows, so we expect gold to pause there (but not to end the decline).

There’s one more sign that suggests that we may not have to wait much longer for the next move lower.

Silver’s cyclical turning point is just around the corner and the most recent short-term move was up thanks to Thursday’s rally. Consequently, reversing direction means a decline in this case. The turning points work on a near-to basis, so we can expect the next move lower in the following days (even if it doesn’t happen right away).

Summing up, the outlook for gold, silver, and mining stocks remains bearish, but not extremely bearish, which means that we don’t increase the size of the short position just yet. Precious metals are not responding strongly to the dollar’s rallies so far, but it seems that investors and traders are simply waiting for a confirmation of the breakout in the USD Index (there have been cases when the metals’ reaction was delayed in the past). Plus, silver’s strong performance and the lack thereof in the case of mining stocks, plus lower highs in gold and mining stocks, are a bearish combination.

To summarize:

Trading capital (our opinion): Short positions (half) in: gold, silver, and mining stocks with the following stop-loss orders:

- Gold: $1,326

- Silver: $20.30

- GDX ETF: $25.20

Long-term capital: No positions.

Insurance capital: Full position.

Please note that a full speculative position doesn’t mean using all of the speculative capital for this trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

The trading position presented above is the netted version of positions based on subjective signals (opinion) from your Editor, and the automated tools (SP Indicators and the upcoming self-similarity-based tool).

As always, we’ll keep our subscribers updated should our views on the market change. We will continue to send them our Gold & Silver Trading Alerts on each trading day and we will send additional ones whenever appropriate. If you’d like to receive them, please Subscribe today.. If you’re not ready to subscribe yet, we encourage you to join our free mailing list – you will be notified when we post an alert free of charge.

Thank you.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief

Gold & Silver Trading Alerts

Forex Trading Alerts

Oil Investment Updates

Oil Trading Alerts

Gold has not closed outside the range of 1,282 to 1,311 US per oz. since April 14, 2014. It has made the market action over the last six weeks decisively boring. That being said, the low level of volatility in the metals market has been accompanied by seesawing equities. Fridays close on the S&P500 above 1900, despite sitting on record levels, marks the fourth time since March the benchmark US index has attempted to breakout past that physiological barrier. Nonetheless, the one market that has made a significant move in one direction has been US treasuries. While it remains difficult to draw conclusions from passive metal prices or volatile stock markets, it’s the bond market that highlights the perplexities of the western economies stalling economic recoveries. Additionally, it questions whether the outlook for increasing long term interest rates is still intact.

The prospect of the US economic recovery yet again losing pace seems to be what has brought investors back into the US bond market. This too is what has prompted many analysts and money managers to suggest the equity markets are long overdue for a correction; however, the inflation story is what is retarding the earlier notion of an all but certain rise in interest rates. Minutes from the US Federal Reserve’s most recent April meeting even revealed that inflation expectations still remain relatively low for the remainder of 2014, and markets were left indecisive as to whether policy will return to normal perhaps sooner than later.

To make matters even more complex, New York Fed District President William Dudley (who may be one of the more recognized voting members amongst the FOMC) suggested this past week that the Fed keeps their 4.3 trillion dollar balance sheet status quo (see chart below). Quantitative easing was accomplished by expanding the Fed’s balance sheet to purchase Mortgage backed securities and treasury bonds. As these debt instruments mature, instead of removing the proceeds from the Fed’s balance sheet, Dudley suggests they reinvest in what is still a struggling mortgage market. Thus, the question of the long term implications or consequences of an inflated Federal Reserve balance sheet hangs over financial markets.

Famed bond investors have grabbed headlines over the last year for the comments on the end of the bull market in bonds. Most memorable was a tweet from Bill Gross of PIMCO, which read, “The secular 30-yr bull market in bonds likely ended 4/29/2013…” The misconception might have been that bonds were now entering a bear market as the economy springs back to life, but this leaves out another scenario, and perhaps the one currently playing out. And that is that interest rates are at historical lows, but they will remain at historical lows for some time. There is no question that is what a country like Canada has seen, when our 10 year yields recently touched a level not seen since June of last year. Furthermore, maybe some of the forecasts for 2014 like an 85 cent Canadian dollar, 3 percent GDP growth in the US, or US investment banks calling for $1,000 gold prices have to be rethought.

All investments contain risks and may lose value. This material is the opinion of its author(s) and is not the opinion of Border Gold Corp. This material is shared for informational purposes only. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission. Border Gold Corp. (BGC) is a privately owned company located near Vancouver, BC. ©2012, BGC.

“You cannot create wealth out of little slips of paper.”

Ludwig von Mises

I suspect the US public is really running out of money. I note the restaurants here in La Jolla are lacking customers. Last night I ate at one of my favorite restaurants, and I was the only one in the room. This lack of money seems to be affecting the big retailers. As proof, glance at the charts of the popular big retailers below.

Target appears to be fading and breaking down below its 200-day MA.

The word is that Walmart’s same store sales are slipping behind last year’s sales, and the stock has suddenly taken a dive.

Costco is super-competitive, but even this stock appears to be going nowhere.

As for gold, the spring and summer months tend to be negative for gold, ending with an extreme low for gold in July. Therefore, once we get past July, I expect better action from silver and gold. Although gold is in a bearish descending triangle, it is holding above support.

………………………………….

I’ve been thinking about the whole idea of the Federal Reserve and the government openly lying to the American people. It’s unbelievable that our representatives would have the unmitigated gall to feed us obvious lies. In the end the truth will come out, and the liars will (I hope) pay the price.

We have been fed lies about the US economy for months on end. We’ve listened to lies about inflation; we’ve been told lies about our “healthy economy.” As far as I’m concerned, manipulation of the markets is tantamount to lying. Manipulating the markets (as per QE) is forcing the markets to behave in an unnatural way, thereby destroying the normal action of free markets and thwarting the forces of supply and demand. And I ask myself, what’s behind these endless lies?

It’s always a matter of money, position, and power. Thousands of men and women depend for their livelihood on employment at the Federal Reserve. They live in fear of losing their jobs. So naturally, one of their objectives is to preserve or endure their jobs. This means keeping the Fed alive at all costs. Underlying all this is fear. The fear in this case is that Congress may, one day, vote the Fed out of existence. So fear is really behind the lies, and thus the system perpetuates itself. Who, I ask, dares to tell the truth? The truth-teller in the end is too often squashed, and the lies go on.

It’s up to the private media to expose the lies. But, for instance, when the media faces the question of US gold, the media is somehow silenced. So the ever-present possibility that the truth will come out — hangs in the balance.”

To subscribe to Richard Russell’s Dow Theory Letters CLICK HERE.

About Richard Russell

Russell began publishing Dow Theory Letters in 1958, and he has been writing the Letters ever since (never once having skipped a Letter). Dow Theory Letters is the oldest service continuously written by one person in the business.

Russell gained wide recognition via a series of over 30 Dow Theory and technical articles that he wrote for Barron’s during the late-’50s through the ’90s. Through Barron’s and via word of mouth, he gained a wide following. Russell was the first (in 1960) to recommend gold stocks. He called the top of the 1949-’66 bull market. And almost to the day he called the bottom of the great 1972-’74 bear market, and the beginning of the great bull market which started in December 1974.

The Letters, published every three weeks, cover the US stock market, foreign markets, bonds, precious metals, commodities, economics –plus Russell’s widely-followed comments and observations and stock market philosophy.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair