Bonds & Interest Rates

The Check and Balance is the Debt Itself

QUESTION:

Today it appears that we will first eliminate the paper currencies and move to a new electronic version to make avoiding taxes impossible. Hence people will flee to tangible assets and the velocity of money will decline taking the economy with it. That will most likely then result in civil unrest/war and then we will see a new type of Bretton Woods rebuilding the global economy adopting some new electronic world reserve currency.

Why will the governments not print new fiat money to infinity to delay the civil unrest/war?

Regards

FK

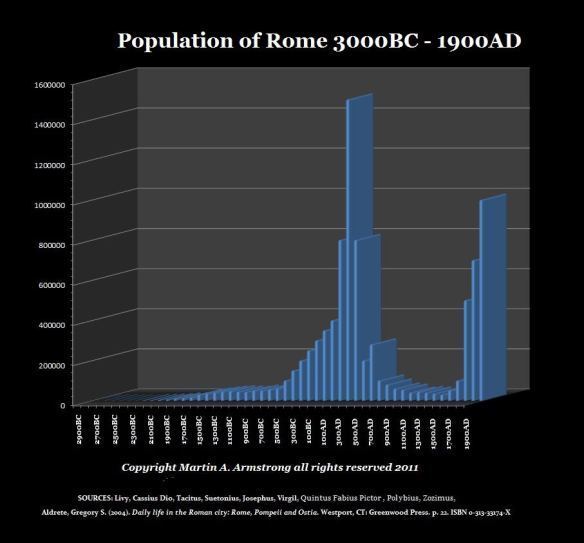

ANSWER: Besides hyperinflation has only taken place in a post-revolutionary government or one that has NO BOND market, the core economy has ALWAYS collapsed by deflation WITHOUT EXCEPTION. It is war upon the people which causes society to collapse. The population of Rome collapsed because taxes kept rising and people just walked away from their property and that began the Dark Age and serfdom.

This story of hyperinflation has been the greatest bullshit sales job I have ever seen. It has zero basis in fact and it is simply a fraud upon the people to sell them gold. This nonsense has been used as the primary sales tool since the 1970s. It works unbelievably for it is purely sophistry.

There is the check and balance in a viable economy. Politicians will not turn to hyperinflation but default on obligations (pensions) because they understand the debt must be maintained or they lose power. I have explained numerous times that this absurd nonsense of hyperinflation is propaganda just to sell gold. It is factually incorrect as to the cause, and it is a complete distortion of history. Hyperinflation followed the German communist revolution where they DEFAULTED on all debt of the previous government and wanted to join Russia. They could not sell bonds and capital withdrew from the banks.ALL tangible assets rose in value against fictional money. It was real estate that ultimately became the backing of the new currency in the aftermath.

In our case, there is no wholesale default on debt. That would wipe out pensions including the Social Security system that has bonds in the drawer. It is the debt that is the check and balance. They will raise taxes trying to hold the system together. You will get war if you default both internationally and domestically. As they say – damned no matter what we do.

DEFLATION is the ONLY way empires, nations, and city states collapse. That is a historical fact! You can count the hyperinflations on one hand historically – you need a computer to count the defaults by deflation of numerous government since 6000 BC. Those in power shake-down the people to retain power. This is what they do! We have massive debt at the state and local levels that cannot print money. They can only default and that is the second force behind deflation as we saw in the City of Detroit.

No government has ever survived indefinitely. It has been debt that is ALWAYS the great destroyer.

also:

EU Wants to seize money from All European Banks on a Flat Rate Basis

Hamilton, Bermuda

Like most people, I love the beach. And Bermuda has plenty of really great beaches.

It’s lovely here– advanced, civilized, and friendly. But let’s be honest, there are a lot of places in the world with great beaches. What really sets Bermuda apart– what makes it unique– is its favorable banking system.

In Europe and the United States, they seem to be going out of their way to destroy their banking systems.

In Europe and the United States, they seem to be going out of their way to destroy their banking systems.

The European Central Bank yesterday announced that they were even taking a key deposit rate NEGATIVE.

In doing so, they basically acknowledged that everything else they have been trying over the last several years isn’t working. And now they’re really desperate.

Just think of what this means to banks in Europe.

Conservative banks hold substantial cash balances. As responsible custodians, they safeguard their customers’ money by maintaining plentiful reserves.

Now, banks in Europe will be penalized for doing this, and instead have a massive financial incentive to deplete their reserves and destroy their balance sheets with risky loans.

And as if they weren’t screwing depositers enough already, interest rates are now going to fall even more.

It’s not much different in the United States.

The average rate on a 1-year certificate of deposit in the Land of the Free, for example, is 0.88%. And of course you have to pay taxes on that. At a tax rate of 25%, that leave an after-tax interest rate of 0.66%

But based on the Labor Department’s most recently released figures, the April 2014 CPI data showed the annualized rate of inflation to be 2%.

So if you believe the government data, you’d have to make at LEAST 2% just to ensure your savings doesn’t lose any purchasing power.

If you’re only making 0.66% interest (after taxes), you are losing over 1.3% annually if you hold your savings in a bank.

This provides a huge incentive to be reckless. Why bother saving money if you’re just going to lose? Might as well go blow it all on a new car.

Of course, that’s precisely what they want you to do. They want you to go out and spend all your money in order to prop up the economy. They want you to borrow money so that you can spend even more.

These policies make for very dangerous banking systems.

Banks now have big incentives to stuff their books full of idiotic, destructive loans… just like they did a few years ago during the US housing boom where they were giving mortgages to dead people.

JP Morgan holds a dangerously low 2% of cash equivalents as a percentage of customer deposits. Citigroup has failed its Fed-mandated stress tests. And Bank of America has had to make embarrassing corrections to its overstated levels of capital.

Ironically, most people simply assume that banks are safe. They’re regulated by the government, after all… so nobody questions the sanctity of their balance sheets.

Candidly, where you hold your money should be a major decision, and it certainly bears a modicum of analysis.

In today’s world, you no longer need to hold your savings in the same place that you live. Geography is irrelevant.

Just as you might move to a new city for the employment opportunities or to put your children in better schools, you can move your savings to a stronger, better banking jurisdiction.

Here in Bermuda, the entire banking system is extremely well-capitalized… and very liquid.*

On average, banks here maintain almost 30% of their customers’ deposits in cash equivalents. And their margins of safety exceed 10% on average.

This stuff matters. Banks in the US and Europe are getting weaker by the month. And a prudent person would consider this trend, and the world of options available, when deciding where to hold his/her savings.

This, above just about anything else, is an essential part of having a Plan B.

You certainly won’t be worse off for holding some savings at a stable bank overseas. But if the worst happens, it might end up being one of the smartest moves you’ve ever made.

Simon

* Premium members– stay tuned for an actionable banking recommendation

If you look at the many charts and read many of the articles being published today you couldn’t be faulted for thinking the rise in food prices is a fairly recent phenomena.

The Food and Agriculture Organization (FAO) of the United Nations publishes the FAO Food Price Index, a measure of the monthly change in international prices of a basket of food commodities.

In 2002 FAO’s Food Price Index stood at 89.6, in May of 2014 it’s at 207.8. In 2002 meat was 89.9, dairy 80.9 and cereals 93.7. In May 2014 the three individual index’s stood at:

- Meat 189.1

- Dairy 238.9

- Cereals 204.4

The International Monetary Fund (IMF) recently published its Index of Primary Commodity Prices.

The reality is food has been soaring in price for decades. Look at this eye popping chart from the St. Louis Fed.

The next time you are in the supermarket play this game – compare today’s prices for the following items to 1970’s prices:

- Apples – .15lb

- Ham – $2.29lb

- Campbells Tomato Soup – .10

- Crest Toothpaste – .77

- Folgers Coffee – $1.90lb

- Turkey – .43lb

- Ground Round – .79lb

- Potatoes – .98 for 10lb

- Large Eggs – .59 dozen

- Pork Chops – .59lb

- Sliced bread – .16 loaf

- Sugar – .39 5lb

- Rump Roast – $1.69lb

- Bacon – $1.29lb

Experts and industry insiders often agree about some of the basic underlying causes of the recent jump in prices – drought, disease, climate change, loss of arable land and soaring input costs, such as diesel and fertilizers. It’s pretty obvious they all have an impact on the price of what eventually reach’s your supermarket shelves.

But most pundits don’t get it, fortunately we at ahead of the herd do – in the agricultural industry today, as it has been for the past 70 some years, it’s all about supply and demand.

And supply isn’t keeping up with demand. Food prices have been on an upwards march for a very long time. That’s what happens when demand outpaces supply.

Why is demand outpacing supply?

- Growing global population – The global population is increasing by over 75 million people a year. Impacts from weather and natural disasters will ebb and flow but population growth is a constant driver of demand.

- Climbing the protein ladder – Many people in emerging/developing economies have increasing discretionary income, they are becoming richer. As income increases people move up the protein ladder, from staples such as rice they climb the ladder and demand more protein in the form of meat and dairy.

Food prices will have to climb ever higher over the coming decades as billions more people are born further increasing demand and stretching the Earth’s limited resources.

By 2050, the world’s population is expected to reach around nine billion -maximum projections range up to 10.6 billion. By the mid 2060s it’s possible that as many as 11.4 billion people will inhabit this planet.

The term Green Revolution refers to a series of research, development, and technology transfers (the shift to high-yielding rice, wheat and corn varieties that are dependent on irrigation and heavy fertilization) that happened between the 1940s and the late 1960s.

The initiatives involved:

- Development of high yielding varieties of cereal grains

- Expansion of irrigation infrastructure

- Modernization of management techniques

- Mechanization

- Distribution of hybridized seeds, synthetic fertilizers, and pesticides to farmers

All these new technologies increased global agriculture production with the full effects starting to be felt in the 1960s.

The Green Revolution’s use of hybrid seeds, irrigation, chemical fertilizers, pesticides, fossil fuels, farm machinery, and high-tech growing and processing systems combined to greatly increase agriculture yields. The Green Revolution is responsible for feeding billions – and likely enabling the birth of billions more people.

“When wheat is ripening properly, when the wind is blowing across the field, you can hear the beards of the wheat rubbing together. They sound like the pine needles in a forest. It is a sweet, whispering music that once you hear, you never forget.” Norman Borlaug, father of the Green Revolution

Cereal production more than doubled in developing nations – yields of rice, maize, and wheat increased steadily. Between 1950 and 1984 world grain production increased by over 250% – and the world added a couple more billion people to the dinner table.

Many experts believe technological advancements in agriculture, energy & water use, manufacturing, disease control, fertilizers, information management and transportation will always keep crop production ahead of the population growth curve.

That’s a lot to ask as over the next fifty years we add another 4 billion people to the world’s population. Global demand for food will increase almost 70% if population growth predictions are correct.

What many of these ‘experts’ don’t get is the Green Revolution’s reality. It wasn’t about the fertilizers, pesticides or irrigation etc. These were all secondary players, add on technologies or basically derivatives to the main technology – dwarfing. By breeding plants to invest less energy in producing stems more energy goes to grain.

“In 1953, Dr. Borlaug began working with a wheat strain containing an unusual gene. It had the effect of shrinking the wheat plant, creating a stubby, compact variety. Yet crucially, the seed heads did not shrink, meaning a small plant could still produce a large amount of wheat.

Dr. Borlaug and his team transferred the gene into tropical wheats. When high fertilizer levels were applied to these new “semidwarf” plants, the results were nothing short of astonishing.

The plants would produce enormous heads of grain, yet their stiff, short bodies could support the weight without falling over. On the same amount of land, wheat output could be tripled or quadrupled. Later, the idea was applied to rice, the staple crop for nearly half the world’s population, with yields jumping several-fold compared with some traditional varieties.

This strange principle of increasing yields by shrinking plants was the central insight of the Green Revolution, and its impact was enormous.” Justin Gillis,Norman Borlaug, Plant Scientist Who Fought Famine, Dies at 95

Conclusion

Well, we’ve been there done that dwarfing thing. So what’s next? What’s going to save us this time round the mulberry bush? Nada, zilch, nothing, zip. We’ll have to keep dumping increasing amounts of fertilizer on a decreasing arable land base while trying to increase irrigation using our rapidly depleting fresh water aquifers. All the while suffering from the effects of climate change, rising transport costs and increasing geo-political risks.

Already over one billion people, or a seventh of the world’s population, goes to bed hungry each night.

Somewhere in the world someone starves to death every 3.6 seconds – most of the names on starvation’s role call are children under the age of five.

Rising agricultural yields have always outpaced population growth, perhaps today that is no longer the case. ‘Been there, done that’ should be on all our radar screens. It’s definitely on mine. Is it on yours?

If not, maybe it should be.

Richard (Rick) Mills

Richard lives with his family on a 160 acre ranch in northern British Columbia. He invests in the resource and biotechnology/pharmaceutical sectors and is the owner of Aheadoftheherd.com. His articles have been published on over 400 websites, including:

WallStreetJournal, USAToday, NationalPost, Lewrockwell, MontrealGazette, VancouverSun, CBSnews, HuffingtonPost, Beforeitsnews, Londonthenews, Wealthwire, CalgaryHerald, Forbes, Dallasnews, SGTreport, Vantagewire, Indiatimes, Ninemsn, Ibtimes, Businessweek, HongKongHerald, Moneytalks, SeekingAlpha, BusinessInsider, Investing.com and the Association of Mining Analysts.

Please visit www.aheadoftheherd.com

If you are interested in advertising on Richard’s site please contact him for more information, rick@aheadoftheherd.com

***

Legal Notice / Disclaimer

This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified.

Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

|

1| |

2|

|

Quotable

Quotable

Be near me when my light is low,

When the blood creeps, and the nerves prick

And tingle; and the heart is sick,

And all the wheels of Being slow….

Tennyson

The Eurozone movie we’ve been watching is starting to look eerily familiar.

Of course, I am referring to the similarity between the economic and monetary path in the Eurozone to that of Japan during its many years of deflation. Mr. Draghi has strenuously argued the Eurozone is not at all like Japan and inflation will indeed pick up, especially now given the ECB’s decision to move to negative interest rates on bank deposits and lowered benchmark rates.

But are deflationary pressures in the Eurozone really all about money?

I don’t think so. I think the problems are structural and go much deeper than merely creating more liquidity. But what I am most concerned about is this: How will Europe’s single currency react if the zone is following down the path Japan has blazed?

Jack Crooks

President, Black Swan Capital

Two full work weeks per year in traffic delays!

A recent study says that if your Vancouver commute is only 30 minutes, that over the course of a year you will spend a total 87 hours in traffic delays……

{mp3}/mikesdailycomment/mcbuscom14jun06{/mp3}

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair