Energy & Commodities

2.Maison Universe High Impact Drilling Watch List

3.Top Picks: No Top Picks This Month

4.Recommended Buy List

5.Coverage List

Click HERE for entire artice with larger images

Click HERE for entire artice with larger images

Gold had its best single day performance since September of 2013 on Thursday of this week. It begs the question, what contributed or led to the 50-dollar rally as it was not triggered by a single piece of economic news, geopolitical action, or policy announcements. One thing that is clear, however, is there has been a shift in investor sentiment and speculators no longer feel as comfortable with their short positions in the futures market. The advances on Thursday, made largely on the back of technical trading confirm this.

Gold had its best single day performance since September of 2013 on Thursday of this week. It begs the question, what contributed or led to the 50-dollar rally as it was not triggered by a single piece of economic news, geopolitical action, or policy announcements. One thing that is clear, however, is there has been a shift in investor sentiment and speculators no longer feel as comfortable with their short positions in the futures market. The advances on Thursday, made largely on the back of technical trading confirm this.

Wednesday brought the typical FOMC announcement, to which gold coincidentally has become accustom to not react to. It was perhaps Janet Yellen’s comments during her press conference later on Wednesday that pre-empted the weak dollar trade that in turn was positive for precious metals. Despite the Fed continuing their pace of tapering their monetary stimulus, it was the outlooks for the Fed Funds Rate that were analogous to comments from the IMF earlier last week, that low rates will ensue until at least the beginning of 2017.

The closest piece of contradictory evidence to this is that North American economies, particularly the US and Canada, are beginning to see signs of inflation. Still nowhere near levels that would prompt policy response as of yet, but it’s been the lack of inflation that’s been the concern of both Bank of Canada and the US Fed, thus these drastic upticks have caught their attention. To give context, in the US, core inflation has been 2 per cent or above in 10 of the 65 months since the recession of 2008. A few consecutive months like we’ve seen certainly don’t make a trend; it’s the fact that key components like rising food and energy prices could very well be sustained.

And it is the rise in energy prices, triggered by geopolitical concerns that have been another positive for gold. Tensions around violence in Iraq have investors worldwide keeping a close eye on crude oil prices. As crude prices elevate to higher levels, consumers face higher energy costs and that means less expenditure elsewhere. Gold once again is participating in a fear trade, which history tells us in not usually sustainable for the market on its own, but paired with other factors could be a different story.

The materialization of an increase in the rate of inflation (which investors who questioned the Feds experimental policies have been waiting for since the onslaught of quantitative easing) provides support for metal prices in here. The question becomes will it last, or once again be more transitory in nature.

It’s difficult to try and forecast this rally and the strength and breadth of it. But one thing is for sure, the move in gold this past week was impressive, and if conditions continue to manifest as they were, this rally could be for real.

As per usual, it’s a wait and see game.

With the confiscating of personal bank accounts going on in Argentina, Hungary, France, Portugal, & Ireland (full story HERE), and the debt in the US that has just been discovered to be 4 times higher than the 16 trillion that the US Government states it is, Peter’s essay below is worth the time to read – Editor Money Talks

The Bond Trap

The Bond TrapThe American financial establishment has an incredible ability to celebrate the inconsequential while ignoring the vital. Last week, while the Wall Street Journal pondered how the Fed may set interest rates three to four years in the future (an exercise that David Stockman rightly compared to debating how many angels could dance on the head of a pin), the media almost completely ignored one of the most chilling pieces of financial news that I have ever seen. According to a small story in the Financial Times, some Fed officials would like to require retail owners of bond mutual funds to pay an “exit fee” to liquidate their positions. Come again? That such a policy would even be considered tells us much about the current fragility of our bond market and the collective insanity of layers of unnecessary regulation.

Recently Federal Reserve Governor Jeremy Stein commented on what has become obvious to many investors: the bond market has become too large and too illiquid, exposing the market to crisis and seizure if a large portion of investors decide to sell at the same time. Such an event occurred back in 2008 when the money market funds briefly fell below par and “broke the buck.” To prevent such a possibility in the larger bond market, the Fed wants to slow any potential panic selling by constructing a barrier to exit. Since it would be outrageous and unconstitutional to pass a law banning sales (although in this day and age anything may be possible) an exit fee could provide the brakes the Fed is looking for. Fortunately, the rules governing securities transactions are not imposed by the Fed, but are the prerogative of the SEC. (But if you are like me, that fact offers little in the way of relief.) How did it come to this?

For the past six years it has been the policy of the Federal Reserve to push down interest rates to record low levels. In has done so effectively on the “short end of the curve” by setting the Fed Funds rate at zero since 2008. The resulting lack of yield in short term debt has encouraged more investors to buy riskier long-term debt. This has created a bull market in long bonds. The Fed’s QE purchases have extended the run beyond what even most bond bulls had anticipated, making “risk-free” long-term debt far too attractive for far too long. As a result, mutual fund holdings of long term government and corporate debt have swelled to more $7 trillion as of the end of 2013, a whopping 109% increase from 2008 levels.

Compounding the problem is that many of these funds are leveraged, meaning they have borrowed on the short-end to buy on the long end. This has artificially goosed yields in an otherwise low-rate environment. But that means when liquidations occur, leveraged funds will have to sell even more long-term bonds to raise cash than the dollar amount of the liquidations being requested.

But now that Fed policies have herded investors out on the long end of the curve, they want to take steps to make sure they don’t come scurrying back to safety. They hope to construct the bond equivalent of a roach motel, where investors check in but they don’t check out. How high the exit fee would need to be is open to speculation. But clearly, it would have to be high enough to be effective, and would have to increase with the desire of the owners to sell. If everyone panicked at once, it’s possible that the fee would have to be utterly prohibitive.

As we reach the point where the Fed is supposed to wind down its monthly bond purchases and begin trimming the size of its balance sheet, the talk of an exit fee is an admission that the market could turn very ugly if the Fed were to no longer provide limitless liquidity. (See my prior commentaries on this, including may 2014’s Too Big To Pop)

Irrespective of the rule’s callous disregard for property rights and contracts (investors did not agree to an exit fee when they bought the bond funds),the implementation of the rule would illustrate how bad government regulation can build on itself to create a pile of counterproductive incentives leading to possible market chaos.

In this case, the problems started back in the 1930s when the Roosevelt Administration created the FDIC to provide federal insurance to bank deposits. Prior to this, consumers had to pay attention to a bank’s reputation, and decide for themselves if an institution was worthy of their money. The free market system worked surprisingly well in banking, and could even work better today based on the power of the internet to spread information. But the FDIC insurance has transferred the risk of bank deposits from bank customers to taxpayers. The vast majority of bank depositors now have little regard for what banks actually do with their money. This moral hazard partially set the stage for the financial catastrophe of 2008 and led to the current era of “too big to fail.”

In an attempt to reduce the risks that the banking system imposed on taxpayers, the Dodd/Frank legislation passed in the aftermath of the crisis made it much more difficult for banks and other large institutions to trade bonds actively for their own accounts. This is a big reason why the bond market is much less liquid now than it had been in the past. But the lack of liquidity exposes the swollen market to seizure and failure when things get rough. This has led to calls for a third level of regulation (exit fees) to correct the distortions created by the first two. The cycle is likely to continue.

The most disappointing thing is not that the Fed would be in favor of such an exit fee, but that the financial media and the investing public would be so sanguine about it. If the authorities consider an exit fee on bond funds, why not equity funds, or even individual equities? Once that Rubicon is crossed, there is really no turning back. I believe it to be very revealing that when asked about the exit fees at her press conference last week, Janet Yellen offered no comment other than a professed unawareness that the policy had been discussed at the Fed, and that such matters were the purview of the SEC. The answer seemed to be too canned to offer much comfort. A forceful rejection would have been appreciated.

But the Fed’s policy appears to be to pump up asset prices and to keep them high no matter what. This does little for the actual economy but it makes their co-conspirators on Wall Street very happy. After all, what motel owner would oppose rules that prevent guests from leaving? The sad fact is that if investors hold bond long enough to be exposed to a potential exit fee, then the fee may prove to be the least of their problems.

Peter Schiff is Chairman of Euro Pacific Precious Metals, which sells high-quality physical platinum, gold, and silver coins and bars.

Click here for a free subscription to Peter Schiff’s Gold Letter, a monthly newsletter featuring the latest gold and silver market analysis from Peter Schiff, Casey Research, and other leading experts.

And now, investors can stay up-to-the-minute on precious metals news and Peter’s latest thoughts by visiting Peter Schiff’s Official Gold Blog.

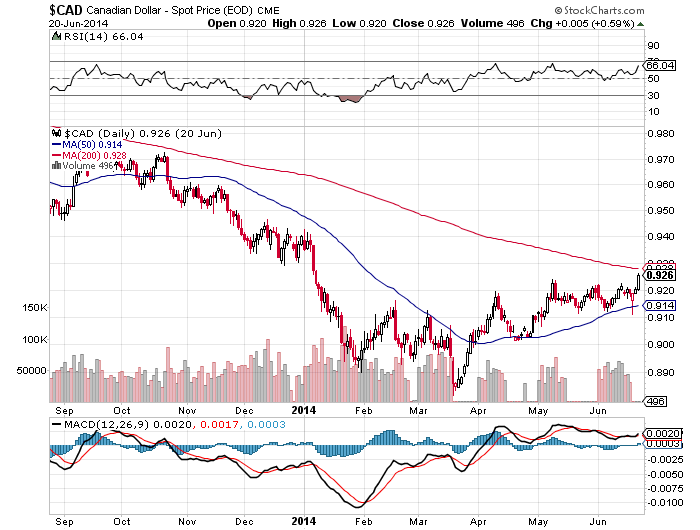

It wasn’t that long ago that the Canadian dollar was being left for dead. After trading above par in late 2012 and early 2013, the currency had fallen to just US88.94¢ by March 20, 2014.

But just two months later, the loonie has rallied more than 3.5% and David Rosenberg knows why.

The chief economist at strategist at Gluskin Sheff + Associates Inc. listed the reasons in his daily Breakfast with Dave report…continue reading HERE

…continue reading HERE

We Americans are watching the events unfold in Iraq with great trepidation. Rising terrorism and rising energy prices. Déjà vu all over again.

And gold is reacting, soaring like a bat out of hell. Up more than $50 last Thursday alone.

A huge move reminiscent of the blastoff phase in late 1978 when gold exploded from a low of $193.40 in November to a high of $875 in January 1980 — a parabolic 352 percent move higher in the price of gold in a tad over two short years.

Thus far for June, gold is up an amazing $82, almost 6.7 percent. Mining shares are doing even better, with the ARCA Gold Bugs Index up 16.7 percent.

The chart shows Basket of gold miners up 16.7% in 20 days— while some of my favorite miners are up even more, as much as 40% in 20 days.

These are real moves. More importantly, they are market moves that tell you that it’s not just us Americans who are worried about the world and starting to buy gold again. The entire investment community — and anyone in their right mind — is worried.

That’s not surprising, considering the sorry state of affairs the world is embarking upon.

It’s not surprising, considering that I have warned you repeatedly of the ramping up of the war cycles. Cycles that govern human social interaction on a grand scale, cycles that can be quantified and used to forecast periods of peace and war, periods of civil unrest and international conflict.

And those cycles are now ramping up and converging in the worst possible combination of forces not seen since the late 1800s.

These are the cycles that are responsible for all that you are now seeing …

– Russia versus Ukraine and other former Soviet satellites, versus Europe and the U.S.

– The reign of terror by the Islamic State in Iraq and Syria (ISIS) in Iraq. This group of terrorists is so violent andextreme that they were kicked out of Al-Qaeda. And now they are the most well-funded terror group in the world with nearly $500 million in the bank and they are ravaging Iraq and headed on to Jordan and other Middle Eastern countries.

– Nigeria, where Boko Haram Islamists have killed hundreds of villagers and kidnapped hundreds of women by posing as Nigerian soldiers, rounding everyone up, and opening fire.

– Kenya, where the Al-Qaeda affiliate Al-Shabab terrorist group is responsible for the recent bloodbath that took place in Mpekeoni, a well-known tourist area. And where nine more people have been massacred by Islamic extremists and Al-Shabab in the coastal areas … and an additional 48 World Cup fans were killed in Mpeketoni.

– Pakistan, where more than 70,000 civilians are now homeless refugees, fleeing from government troops who killed 105 militants in North Waziristan’s Shawal area.

– Canada, where a Calgary suicide bomber who killed 19 Iraqis has become a propaganda tool for jihadists, who are urging Muslims to follow his “great example” and threatening Canada to change its “oppressive” foreign policies.

– China, where the Chinese government recently executed 13 people in the Xinjiang region who were found guilty of organizing and leading terrorist groups, as well as murder, arson, theft and other crimes.

– China versus Japan, Vietnam, Indonesia, Malaysia, the Philippines, in an international dispute over the Spratly and Senkaku Islands and their vast oil and gas reserves … and where China is claiming territorial jurisdiction, seizing land and waters away from countries, a dispute that will ultimately lead to an international war.

– Then there’s Syria, Yemen, Egypt, Turkey, Iran, North Korea, Venezuela, Myanmar, Libya, and a host of other countries where violence is rapidly rising.

All told, there are now a record 61 countries involved in wars and 540 militia, anarchist, religious and separatist groups.

And lest you think the turmoil you are seeing is all terrorist-related, or isolated events that do not impact you, think again:

The rising war cycles are also about bankrupt, destitute governments that are now acting like caged animals, striking out against their own people …

By raising taxes, engaging in confiscatory wealth measures and capital controls, by spying on their own citizens and more.

Consider:

– Last March’s Cyprus confiscation of depositor wealth to bail out Cyprus’ banks, a policy that has now been embraced and legalized for all of Europe. Have money in a European bank? Good luck, if it goes under, your money is at risk of being confiscated.

– Last September’s confiscation of retirement accounts by Poland’s government. Fully half of all private retirement assets transferred to the state without offering retirees any compensation whatsoever.

– France’s SEVENTY-FIVE percent income tax. And to counter, where France’s Marine Le Pen’s Front National is championing a recent report by well-known French economists that concluded that 60 percent of French public debt is illegitimate, sowing the seeds for a French sovereign debt default down the road.

– Argentina, where massive sovereign debts are now unpayable, and confiscatory measures against pensions are now in the planning stage by President Cristina Kirchner.

– Or Washington’s incessant spying on YOU, all designed to track everything you do, every penny you spend or squirrel away.

In short, all over the globe the rising tide of geo-political unrest is occurring at a pace at which even I underestimated.

You may think all these conflicts are unrelated … or the

result of religious extremists … or that they have no impact on you.

But mark my words: Look closely, as I have done, at all of the conflicts around the world — whether religiously inspired or not — and you will see two common threads:

1. Private sector groups rising up against authoritarian, unjust, corrupt and imperialist governments.

2. Private sector groups rising up against governments that want to increase taxes or even confiscate wealth while, at the same time, levying austerity measures on its people to slash previously promised benefits.

In lesser developed countries, it’s the result of government corruption, imperialistic actions taken by developed countries, pillaging of natural resources, and more. Yes, they are shrouded in religious, especially Islamic extremism …

But when distilled down to the truth, the forces driving them are no different than the forces that are driving the civil and international unrest you are now seeing in developed countries.

It’s merely a matter of degree. Yet an impartial and objective study of the forces that are driving the war cycles higher — wherever in the world they are playing themselves out …

Can all be distilled down to a great battle between the public and the private sectors.

These are the chief reasons gold and

silver are now starting to explode higher.

And why gold will likely fetch well over $5,000 an ounce a few years from now … silver to more than $125 an ounce … and mining shares, to the moon.

Best wishes and stay tuned,

Larry

The post War Cycles Sending Gold, Mining Shares SOARING! appeared first on Money and Markets – Financial Advice | Financial Investment Newsletter.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair