Economic Outlook

Forty-four percent. That’s the alarming unemployment rate for those aged 15 to 25 in Italy, where I traveled recently to  meet with other global chief executives and business leaders.

meet with other global chief executives and business leaders.

The reason for Italy’s high youth unemployment? Tortuous red tape, high taxation and thuggish unions. Many of the CEOs at the event I attended noted that Italy is mired in unionization. This has created a restrictive jobs market that crowds out well-educated, aspirational young people, many of whom are forced to flee their homes and seek work elsewhere.

But “elsewhere” within the European Union is currently not much of an improvement. Even in Germany, the EU’s most reliable economy, train and airline unionists have gone on strike, bringing the country to a near-standstill. Incredibly, both Italy and France–where the youth unemployment rate stands at 24 percent–want the EU to foot the bill for their joblessness woes. Global investors’ patience has been stretched thin as European Central Bank (ECB) President Mario Draghi and German Chancellor Angela Merkel continue to bicker over how to resolve the region’s slowdown.

As I told CNBC Asia’s Bernie Lo, the EU’s default policy is to tax anything that moves. Led by pro-taxation economists such as France’s Thomas Piketty, Europe’s policies have become a sort of contagion resonating throughout the rest of the world. The eurozone countries have an imbalanced approach to jumpstarting their economies, relying only on monetary policy but failing to address fiscal issues such as punitive taxation and over-bloated entitlement spending.

You can see how disastrous the results have been: France and Germany’s industrial production has turned down recently. Their purchasing managers’ index (PMI) numbers are below the 50-mark line, indicating contraction. This trend is especially worrisome because Europe is a bigger trading partner with China than the U.S. is.

So what’s the solution?

The EU would do well to look east, specifically to China.

China Handing over Its Economy’s Keys to Capital Markets

Last week senior Chinese officials met in Beijing to resolve the sorts of problems the EU can’t seem to fix, let alone acknowledge. On the chopping block were regulations–hundreds of them. According to Premier Li Keqiang, 416 lines of red tape have allegedly either been abolished or eased in order to facilitate business growth in important sectors such as transportation, logistics and telecommunications. In June, Li vowed to slash an additional 200 measures.

The Chinese government also plans to relax oversight of key areas such as utilities and natural resources, land and the pricing mechanism of money. Gone is the government’s control over shale gas, coal bed methane and imported liquefied natural gas (LNG). The mining sector’s tax code has been reformed. And for the first time, private companies have been granted the license to ship crude oil.

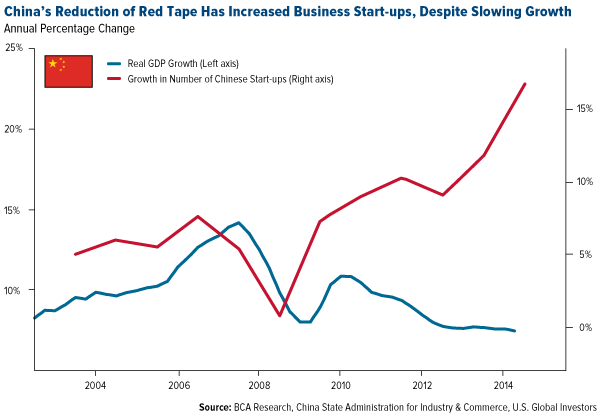

It appears as if China is starting to see the light. They’re introducing competition back into their capital markets instead of strangling it, as the eurozone has done. Between January and September, 10.97 million new jobs were created in China, exceeding the government’s goal of 10 million in 2014 and beating the benchmark by an entire quarter, according to China’s National Bureau of Statistics (NBS).

As you can see below, new business start-ups in China have skyrocketed.

These red tape-cutting measures, coupled with fiscal stimulus, are needed now more than ever. As promising as Premier Li’s promises are, China still faces deflation and declining real GDP growth. The Asian country’s economy is currently headed for its slowest expansion since 1990, the main culprit of which is the struggling real estate market.

Other problems also continue to hold China back, many of them deeply-rooted and systemic. The Ease of Doing Business Index ranks China 158 out of 189 economies in the “Starting a Business” category and an almost-dead-last 185 in the “Dealing with Construction Permits” category. According to the World Economic Forum’s most recent Global Competitiveness Report, the two most problematic factors for conducting business in China are access to financing and corruption, another issue Chinese officials are addressing this week.

These issues can’t and won’t be fixed overnight. But unlike the EU, China acknowledges them and is seeking innovative solutions. One of the only benefits to having a one-party system, as China does, is that you can’t shuffle off a set of problems to another party and then lay the blame at their feet when they go unresolved. You must think long-term.

Constructive Manufacturing News

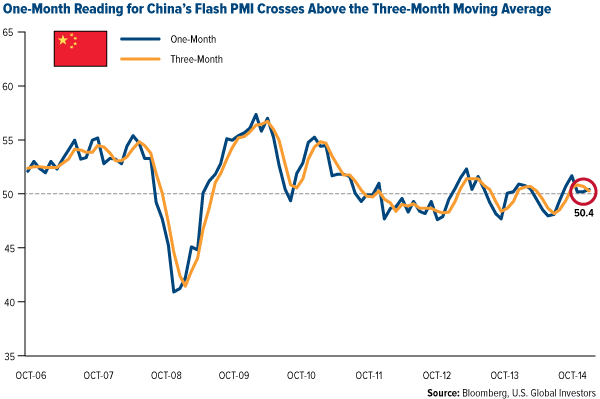

Last week we were relieved to learn that China’s flash PMI came in at 50.4. Anything over 50 indicates growth in the manufacturing sector, but as I’ve discussed on numerous occasions, what really matters is that the one-month reading crosses above the three-month moving average. Such a “cross-above” historically means that commodities and commodity stocks perform better in the coming months. Based on our research, three months following a cross-above, there’s a 73 percent chance that the S&P 500 Index will rise more than 2.4 percent and a 55 percent chance that the S&P 1500 Energy Index will rise more than 0.7 percent.

As you can see, this crossover did indeed occur, the first time it’s done so since May.

Of course, flash PMIs are merely preliminary, and we won’t know the final results until later. But for now this is certainly positive news.

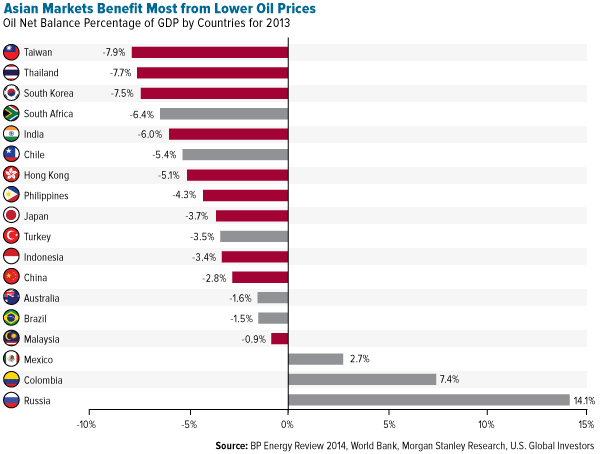

Emerging Asia Wins with Cheap Commodities

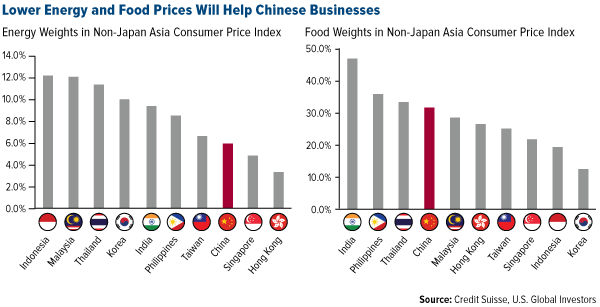

One of the reasons why Chinese manufacturing is picking up steam might be the recent collapse in commodity prices. Low commodity prices undeniably hurt certain stocks in the space, and we’ve felt the pain in some of our funds. The silver-lining, though, is that these low prices have helped non-Japan Asian companies get ahead, a tailwind for our China Region Fund (USCOX). Because labor continues to be relatively cheap in Asia, commodities tend to be the single-largest company expenditure.

Lower steel and aluminum costs benefit machinery, automobile and equipment manufacturers, as well as homebuilders, shipbuilders and oil and drilling equipment suppliers; falling corn and wheat prices are welcomed by food and beverage producers; cheap copper is good for construction and engineering, utilities and electrical equipment.

Then there’s oil and gas. Since June, Brent crude has corrected itself over 25 percent. Again, this is a headwind for petroleum companies and large net-oil-exporting nations such as Russia and Mexico, but cheap energy equates to huge savings for emerging Asian countries.

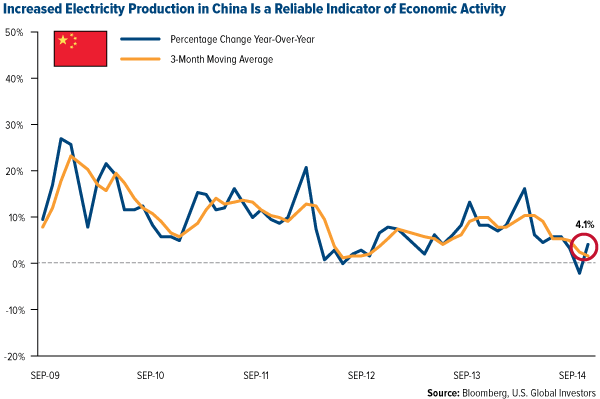

One final bellwether of economic growth I want to touch upon is accelerated electricity generation and usage. In the past, Chinese Premier Li Keqiang has cited this as one of the more reliable indicators of economic activity because electricity is not easily stored and the data is difficult to manipulate. This month, energy production improved 4.1 percent year-over-year–not a huge cause for celebration, but a step in the right direction nonetheless.

China Is a Long-Term Story

Compared to many eurozone nations, China is relatively young. Whereas the median age in Italy is 43 years, in China it’s 35. There’s huge growth potential in this region, especially now that Premier Li has resolved to cut red tape and balance monetary and fiscal policy. In 10 years’ time, the 35-to-45 cohort, a well-educated group with good salaries and credit, will expand dramatically.

Consider this: of the 1.35 billion Chinese citizens, about 618 million, nearly half, have access to the Internet. Of those, 302 million, nearly half again, shop online. These numbers will continue to grow, and with them, greater investment opportunity. Name one Western European company that, in recent years, has achieved the sort of success Alibaba, Tencent or Baidu has. Not in a Piketty economy.

In the last 3 years the US Dollar Index has rallied ~19% while major commodity indices have fallen ~30%. We think Market Psychology is sensing “trouble ahead” because massive Central Bank “money printing” has created a mountain of debt…but has failed to ignite sustainable global economic growth. We think smart money is therefore leaving peripheral markets and returning to the center…seeking safety. We think this trend will intensify in the months ahead.

The US Dollar Index is at 4 year highs while…

Commodity indices are at 4 year lows.

Short Term Trading:

Stocks:

We have previously written that September 19, 2014 may have been an inflection point in Market Psychology…a date when a number of markets reversed course as “risk off” sentiment intensified. We think that the stock market may have begun a multi-month “topping process” that will produce sharp price breaks and rallies…but not new highs.

The DJIA dropped ~1500 points from its September 19 All Time High to its October 15 lows…and then rallied back ~1000 points. We wrote last week that we wouldn’t be surprised to see it rally back 50 to 70% of the break…into the 16,600 to 16,900 range. Well…here we are at 16,800 and rising (while the DJT has rallied to New All Time Highs.) Our trading plan was to wait for the “bounce back” from the Oct 15 lows to run out of steam and then we would get short. We are still waiting. If the market rallies past the 17006 highs made October 8 (notice how the market reversed after the Oct 8 rally and fell over 1000 points in the next 5 trading sessions) then the October break was probably another “Buy The Dip” opportunity and new All Time Highs are likely. If the market fails to rally past 17000 and “rolls over” then we may get a challenge of the Oct 15 lows.

Currencies:

We stayed with our long US Dollar positions into September and then stood aside thinking that the rally had gone too far too fast ( up 12 weeks in a row.) We do NOT want to be short the US Dollar and are looking to re-enter long positions…we may have missed a good opportunity below 85 but we are still on the sidelines. Everyone and his dog is bearish the Euro (and so are we) and that makes us nervous…so we wait.

What was the biggest move this year…in a major country currency? The Russian Ruble…down ~20% (to All Time Lows) since July as crude oil tumbled, sanctions bit and capital fled the country…how did we miss that trade?

Longer term:

Last week we wondered if September 19 was what George Soros would have called an “Inflection Point”…a point at which “the trend” changes. The “trend” we were considering was the ebb and flow of market psychology as it ranges from aggressively embracing risk to desperately seeking safety. If capital really is starting to get defensive…and we think it is…then how does that play out in the markets?

Does capital, to some degree, see “trouble ahead” because fiscal and monetary policies since the credit crisis have been unable to “kick start” economic growth…but have instead created a mountain of debt?…and if there is no economic growth then how does that debt get repaid? Or, more to the point, who gets stuck with it? Does capital anticipate that governments will ramp up the “Pay Your Fair Share” campaign and raise taxes?

Perhaps the Really Big Inflection Point comes when the trend towards the lowest interest rates of our lifetime reverses…and not because Central Banks start to raise rates…but because people lose faith in the credit worthiness of the borrowers. We can imagine the initial sequence such a “loss of faith” would take…and we think that may have begun…credit spreads would widen and yield curves would steepen…but what happens after that? Do interest rates…across the credit quality spectrum…start to rise? Who defaults first?

We’ve written that the stock market drama may be the lead story on the nightly news…but the looming shakeout in the credit markets is WAY more important. Our KEY belief for our personal net worth is…stay liquid and DON’T reach for yield.

On October 21st, the BC Liberal government announced the province’s long awaited tax structure for Liquefied Natural Gas exports to Asia. Under this structure, companies processing and exporting LNGs from British Columbia’s west coast will pay a tax rate of 1.5% once production commences which will increase to 3.5% once after capital costs are recovered. This rate will then rise further to 5% at the start of 2037. This structure is lower than what the government originally discussed which would have been a straight 1.5% at the outset and 5% after the company’s recovered their capital costs of building LNG plants and supporting infrastructure. Responses from industry to the revised structure appear to be mixed.

On October 21st, the BC Liberal government announced the province’s long awaited tax structure for Liquefied Natural Gas exports to Asia. Under this structure, companies processing and exporting LNGs from British Columbia’s west coast will pay a tax rate of 1.5% once production commences which will increase to 3.5% once after capital costs are recovered. This rate will then rise further to 5% at the start of 2037. This structure is lower than what the government originally discussed which would have been a straight 1.5% at the outset and 5% after the company’s recovered their capital costs of building LNG plants and supporting infrastructure. Responses from industry to the revised structure appear to be mixed.

Currently in British Columbia there are 18 LNG project proposals in various stages of consideration with estimated construction budgets up to $16 billion. So far, about 9 of these projects have approval from the National Energy Board (NEB) to export LNG from Canada but none have yet made a final investment decision. Malaysia’s state-owned Petronas, who is spearheading the $11 billion Pacific NorthWest LNG project, threatened in September to cancel their plans in British Columbia if the government didn’t make an effort to create a more globally competitive and efficient operating environment for the sector. The Pacific NorthWest LNG project is considered by many analysts to be the project with the best chance of getting off the ground. Petronas is schedule to make a final investment decision on their multi-billion project by October 31st and so far has not provided any concrete comments on the disclosed tax regime in the province.

It would seem that the pressure is on BC’s Liberal Party who made LNG development and the accompanying economic benefits a focal point of their recent election campaign. Premier Christy Clark alluded to the creation of 100,000 jobs and eventually a debt free British Columbia if even a small handful of these projects were developed. These projections seem to be extremely optimistic by most measure and obviously politically motivated. But the government’s opponents are now attacking them with accusations that they have bowed to Petronas’ threat and are essentially giving B.C.’s natural resources away.

In our opinion, these views indicate an extreme lack of understanding of the issues facing B.C.’s LNG sector (or perhaps better put the possibility of the province having one). Firstly, B.C. will actually be alone in the world with respect to imposing a special tax on LNG exports. Other nations, such as Australia and the United States who appear to be eager to invite the LNG opportunity, have no such ‘special tax.’ Secondly, the province will also generate royalty revenues from natural gas that is produced within its borders as well as corporate income tax both from the producers and the exporters. Not to mention income taxes generated from these company’s employees and all of the economic activity that a thriving LNG sector would provide. So rather than being cowardice, perhaps the government’s strategy to maximum revenue from the sector should be viewed more as perilous since it potentially endangers this sector even getting off the ground.

But ultimately the future of B.C. LNG may not even come down to the tax regime. This is a globally competitive marketplace and there are other players who are moving quickly to contract exports of their own supplies of LNG. These include the United States and Australia but even lesser known players like Papa New Guinea where Exxon (in joint venture with other parties) just finished the completion of a US $19 billion LNG facility which is now exporting to Asian markets. In many jurisdictions, not only is the LNG sector unhindered with a special tax but environmental regulations are less stringent and the number of stakeholders to please less numerous. For better or for worse, all of this equates to an easier operating environment for companies who want to invest billions of dollars. Commodity prices are also becoming a factor with LNG prices declining over the last six months making the prospects for anyone less attractive than they were a year ago.

If there is one thing we know about commodities, whether oil, gas, gold, or LNG, it is that they are volatile, risky and speculative. At this point, it is difficult and maybe even impossible to predict the future of B.C. LNG. The next several months will be very telling as some companies either make, or fail to make, their final investment decisions.

KeyStone’s Latest Reports Section

When events “happen,” they happen in a directed way by the elite’s mainstream media outlets. News is presented in a way that is designed to appeal to mass emotions so as to discount reasoned thinking. You get government pimps, be they congressmen, heads of agencies, even presidents who add their fiat 2 cents in order to give some weight to an otherwise weightless argument. While the “news event” is largely untrue, there is a sufficient amount of plausibility added to disguise the misleading [never verified] facts. In other words, psychological manipulation is the main menu of options for the elites to keep the masses “informed,” while still very much uninformed.

As to gold and silver, there are two sides to the coin, as it were. One is well-covered, in fact overly covered, while the other receives coverage but with elite-imposed limitations.

One of the most basic truths in determining the value of anything is that of supply and demand: the availability of a particular product or service [supply], and the desirability [demand] for the product/service. It is an axiomatic rule that cannot be broken, but it can be distorted, as in the case for gold. The distortion via central bank manipulation has been so pervasive over such a long period of time, well over a half-century, that it has become perverse.

Supply for the physical has been replaced by paper. Demand for the physical has been replaced by [fiat and news]paper. Ever since elite-puppet FDR issued his Executive Order that all “persons” turn in their gold [the “news” portion], gold was replaced by the foreign-owned Federal Reserve central bank paper issue [the fiat portion], and demand was made to disappear from the minds of the [dis]informed public and world. Who needs gold when you can have the “almighty dollar?”

Gold coin, when in circulation, represented the greatest stability for medium of exchange conditions. As the duped American public turned in their gold coins, back in the 1930s, [decreasing one area of demand], the coins were melted down into larger bar form, never to return into circulation [supply]. The US was a country where a central bank did not previously exist. Once the privately owned Federal Reserve central banking system was “installed” by corrupt means in 1913, in just 30 years it had successfully withdrawn the use of gold as a means of measured wealth and replaced it with the Rothschild House of Paper. America has never been the same, since.

Financial stability disappeared, and financial dependence on a de facto federal fiat system began in earnest. Yet, if you were to take a poll in the federalized US today, almost none would make any link between the disappearance of gold and the Federal Reserve central bank. This is how successfully the elites work over a protracted period of time, changing the nature and character of things through words, using apparent authority, as in the entire US government, without ever exposing their “hidden hand” directing everything.

About one year after the Rothschild Federal Reserve banking system took over in 1913, there was just over $12 billion on deposit with non-fed member banks. By the end of 1929, these banks held just over $21 billion for a gain of about 75%. By contrast in 1914, Fed-member banks held $6.3 billion in reserves, and at the end of 1929, member reserves were almost $34 billion, an increase of 430%. Shortly after, by strong-arm power, non-member banks ceased to exist, reminiscent of the cuckoo bird.

A cuckoo bird will lay its eggs in the nest of another bird, leaving that unsuspecting other mother bird to raise the newly hatched cuckoo. Once hatched, the new cuckoo bird will get rid of any remaining eggs, and also push out any other newly hatched other-species bird. The Rothschild central banking system, with the US Fed being the most powerful, is the cuckoo bird of the financial world.

The so-called gold standard did not work primarily because the Rothschild banking system would not allow it to work. In order to maintain a gold standard, there are constraints on the factors by which money supply can be expanded, and that hampered the Rothschild formula for creating ever-increasing amounts of paper-issue fiat, with interest to be earned on its issue. With the gold standard, people bought and paid for that which they owned, owing no one. With the Federal Reserve eliminating the gold standard, substantially higher multiples of paper money could be issued in the form of credit expansion. “Buy now, pay later,”

Fast forward to today, almost everyone in the US is living on credit, well beyond their means, debt-serfs, if you will, to the Rothschild elite’s debt system. Very few Americans buy and pay for what they own unless it is on credit, to be repaid based on future earnings. This kind of economy did not exist in the US, over 100 years ago, prior to the insidious establishment of the Federal Reserve central banking system.

So successful has been the Rothschild banking system that gold has been all but erased from the American psyche. “A barbaric relic. You cannot eat gold. It earns no interest.” Can you eat Federal Reserve Notes? Do Federal Reserve Notes earn interest, anymore?

Everyone is aware [or should be] of the unprecedented demand for gold and silver from China and Russia to ordinary people who are buying as much gold and silver as possible. Stories about demand have been headliners for the past few years, with a large degree of accuracy. Not so much when it comes to supply, however. The real supply side of the Supply/Demand equation has been shrouded in secrecy, lest the Western central banking Ponzi scheme come unraveled, which it is now doing.

What you need to understand, as a precious metals buyer and holder, and that gold and silver confiscation have always been the highest priority for the elites, accomplished via their central banking system, for the most part, until the last decade or so when outright theft has been employed via CIA-led or sanctioned operations, like Libya, Ukraine.

This massive distortion of propaganda, mostly against gold, suppressing it as the time-tested store of wealth, along with silver, has served its purpose, and Newton’s Third Law of a reaction that is proportional to the action is getting ready to come into play. It is why our focus over the last several months has turned totally away from all considerations of the overblown and errant attention on the demand factors, and emphasis placed on what the Rothschild elites have been doing to the world economy: plundering its wealth and leaving worthless fiat and economic destruction behind.

Everyone not a part of the upper echelon elites has been financially duped by that parasitic group, robbed of wealth, freedom, property, dignity. While many knew that some kind of correction would follow the highs from 2011, no one, except maybe Jim Rogers, expected the depth of the correction down to current levels, an indication of just how much overly power this handful of people have.

The Western banking system, and particularly the Federal Reserve, have finally become a ticking bomb. At this point, you are either cognizant of the suppressed reality of events that have admittedly succeeded since the 1930s, or you should not be reading articles like this one. It is with incredible irony that the ultimate defeat of the West will be at the hands of the once, and still vilified “evil” nations of China and Russia. While they are building economic bridges around the world, fostering growth, the US/UK led West has only debt, financial destruction, and war, including human destruction as playing cards about to be trumped. Sadly, it may still get uglier as the West becomes more dangerously reactive, clearly demonstrating the elites know no other way.

Nothing, absolutely nothing will impel the price of gold and silver higher until the elites have lost total control over their deeply entrenched system. This means the loss in power of the no longer almighty Federal Reserve Note, better known as the “dollar. The never-ending War Against [insert any reason here] by the tenant of the White House, doing the bidding of his landlord, the New World Order banking elites, is ratcheting up as a sign of desperation that the end is near.

When it happens, it will likely be at a fast pace, perhaps faster than most are prepared, except for those already long the physical. Like many, we bought physical on the way up, held it, and added on the way down, some of which are almost half the value, in silver. At no time has there been any rear-view mirror regret. This is but a temporary phase of a seeming decline in value for taking a stance against an out-of-control Western banking system now closer to collapse than ever before.

Will it be by the end of the year, sometime next year, or sometime thereafter? We do not know or care, not to be cavalier, but instead from a position of comfortable preparation. If an unexpected jump in prices overnight occurs, as could happen, being a year early and not a day too late will have paid off.

We do not look at fundamentals, at all, but do have a general awareness that the “story” for silver can be more explosive to the upside than for gold. There is some credibility to that as found in the gold/silver ratio. If one knew little to nothing about silver, but was aware of this ratio, at 71+:1, gold over silver, odds favor an eventual reversal to a lower number, be it 40:1 or 25:1, or anywhere in between. This means silver would outperform gold. The point to make is how an awareness of what the market is “saying” in the charts is best and most current source available.

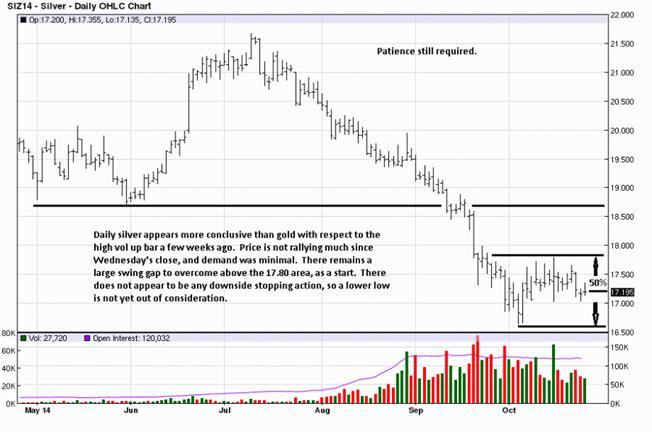

There has not been any large move lower since important support was broken 6 weeks ago. This could be a sign that the end of the decline is nearing, and even if that were true, there is still no indication that a bottom is in place.

One need not “guess” what to do when viewing a chart. The market provides ample information to suit any trader/investor style. For right now, the trend remains down, and that tells us the odds of making money from the long side in futures is slim. One need not be an astute chart reader to look back at the weekly and surmise an estimate as to how many longs are profitable over the last few years. [Long physical is viewed differently, at least from our perspective.]

The daily says the same thing. The mostly sideways activity for October is not a ringing endorsement for demand showing any degree of control. Price has not regained broken support, and it is far from retracing to the half-way area, 19 area, of the last swing high. There should not be any expectations for much upside, at this juncture.

There may be some increased attention being given to a triple-bottom-for-gold scenario, but any evidence for that conclusion is so far from consideration that it does not deserve much attention. The rally off the last low has been weak. That may change starting next week, or some weeks later, but one can only deal with what is known for right now. It is equally possible, maybe even more probable that price could be lower. Either way, it does not matter because the risk/reward factor is not supportive for either side.

Given the position for gold, near its lows, the likelihood of support holding above a 50% retracement, the 1219-1220 area, is not in keeping with the character of a down trending market. For sure, buying rallies, expecting yet a higher rally has not worked in gold, to which we can attest from a few trades some time back. Time is on the side of longs who are best served being on the sidelines, for now.

In a world filled with fiat currencies, how important is gold’s role in the financial system? Proponents often view the precious metal as a hedge against economic chaos, while critics typically claim gold is hardly more than an unproductive rock. Interestingly, some countries appear to believe gold is quite important, and one former Fed chair explains why.

In a world filled with fiat currencies, how important is gold’s role in the financial system? Proponents often view the precious metal as a hedge against economic chaos, while critics typically claim gold is hardly more than an unproductive rock. Interestingly, some countries appear to believe gold is quite important, and one former Fed chair explains why.

Alan Greenspan, who served at the helm of the Federal Reserve for nearly two decades, recently penned an op-ed for the Council on Foreign Relations discussing gold and its possible role in China, the world’s second-largest economy. He notes that if China converted only a “relatively modest part of its $4 trillion foreign exchange reserves into gold, the country’s currency could take on unexpected strength in today’s international financial system.”

Greenspan also believes the downside risks for China stockpiling gold are limited, at least from a pure investment point of view. “It would be a gamble, of course, for China to use part of its reserves to buy enough gold bullion to displace the United States from its position as the world’s largest holder of monetary gold,” he wrote. “But the penalty for being wrong, in terms of lost interest and the cost of storage, would be modest.”

……read page 2 HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair