One of the groups of investors that’s the most mistreated by Government is the millions who have responsibly saved for their retirement. This analysis is based on American figures but is relevent to Canadian investors just as well – Money Talks Editor

Income Inequality is a Problem – When Caused by Government Meddling

When I entered the investment business as a stock broker at Merrill Lynch in the 1980s, savers could routinely get 7-9% on their money with riskless CDs and short-term Treasury bonds.

In fact, I sold multimillions of dollars’ worth of 16-year zero-coupon Treasury bonds at the time. Zero-coupon bonds are debt instruments that don’t pay interest (a coupon) but is instead traded at a deep discount, rendering profit at maturity when the bond is redeemed for its full face value.

At the time, long-term interest rates were at 8%, so the zero-coupon Treasury bonds that I sold cost $250 each but matured at $1,000 in 16 years. A government-guaranteedquadruple!

Ah, those were the good old days for savers, largely thanks to the inflation-fighting tenacity of Paul Volcker, chairman of the Federal Reserve under Presidents Jimmy Carter and Ronald Reagan from August 1979 to August 1987.

Monetary policies couldn’t be more different under Alan “Mr. Magoo” Greenspan, “Helicopter” Ben Bernanke, and Janet Yellen. This trio of hear-see-speak-no-evilbureaucrats have never met an interest-rate cut that they didn’t like and have pushed interest rates to zero.

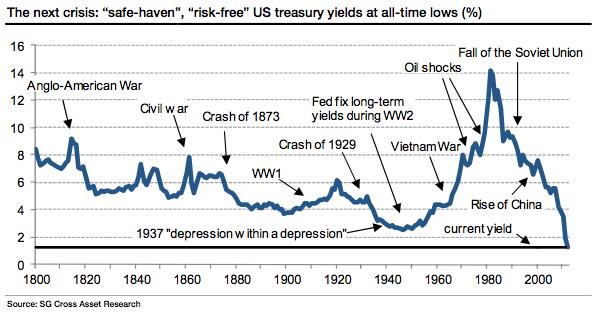

The yield on the 30-year Treasury bond hit an all-time record low last week at 2.45%. Yup, an all-time low that our country hasn’t seen in more than 300 years!

These low yields have made it increasingly difficult to earn a decent level of income from traditional fixed-income vehicles like money markets, CDs, and bonds.

Unless you’re content with near-zero return on your savings, you’ve got to adapt to the new era of ZIRP (zero-interest-rate policy). However, you cannot just dive into the income arena and buy the highest-paying investments you can find. Most are fraught with hidden risks and dangers.

So to fully understand how to truly and dramatically boost your investment income, you absolutely must look at your investments in a new light, fully understanding the new risks as well as the new opportunities.

There are really two challenges that all of us will face as we transition from employment to retirement: longer life expectancies; and lower investment yields.

Risk #1: Improved health care and nutrition have dramatically boosted life expectancies for both men and women. We will all enjoy a longer, healthier life, which means more time to enjoy retirement and spend with friends/family, but it also means that whatever money we’ve accumulated will have to work harder as well as longer.

Today, a 65-year-old man can expect to live until age 82, almost four years longer than 25 years ago; the life expectancy for a 65-year-old woman is also up—from 82 years in the early 1980s to 85 today.

The steady increase in life expectancy is definitely something to celebrate, but it also means we’ll need even bigger nest eggs.

Risk #2: Don’t forget about inflation. Prices for daily necessities are higher than they were just a few years ago and constantly erode the purchasing power of your savings.

The way I see it, your comfort in retirement has never been more threatened than it is today, and it doesn’t matter if you’re 20 or 70.

The rules are different, and you only have two choices:

#1. spend your retirement as a Walmart greeter (if you’re lucky enough to get a job!); or

#2. adapt to the new rules of income investing.

Today, the new rules of successful income investing consist of putting together a collection of income-focused assets, such as dividend-paying stocks, bonds, ETFs, and real estate, that generate the highest possible annual income at the lowest possible risk.

Even in an environment of near-zero interest rates and global uncertainty, there are many ways an investor can generate a healthy income while remaining in control. Income stocks should form the core of your income portfolio.

Income stocks are usually found in solid industries with established companies that generate reliable cash flow. Such companies have little need to reinvest their profits to help grow the business or fund research and development of new products, and are therefore able to pay sizeable dividends back to their investors.

What do I look for when evaluating income stocks?

• Macro picture. While it’s a subjective call, we want to invest in companies that have the big-picture macroeconomic wind at their backs and have long-term sustainable business models that can thrive in the current economic environment.

• Competitive advantage. Does the company have a competitive advantage within its own industry? Investing in industry leaders is generally more productive than investing in the laggards.

• Management. The company’s management should have a track record of returning value to shareholders.

• Growth strategy. What’s the company’s growth strategy? Is it a viable growth strategy given our forward view of the economy and markets?

• A dividend payout ratio of 80% or less, with the rest going back into the company’s business for future growth. If a business pays out too much of its profit, it can hurt the firm’s competitive position.

• A dividend yield of at least 3%. That means if a company has a $10 stock price, it pays annual cash dividends of at least $0.30 a year per share.

• The company should have generated positive cash flow in at least the last year. Income investing is about protecting your money, not hitting the ball out of the park with risky stock picks.

• A high return on equity, or ROE. A company that earns high returns on equity is usually a better than average business, which means that the dividend checks will keep flowing into our mailboxes.

This doesn’t mean that you should rush out and buy a bunch of dividend-paying stocks tomorrow morning. As always, timing is everything, and many—if not most—dividend stocks are vulnerably overpriced.

But make no mistake; interest rates aren’t rising anytime soon, and the solid, all-weather income stocks (like the ones in my Yield Shark service) will help you build and enjoy a prosperous retirement. In fact, you can click here to see the details on one of the strongest income stocks I’ve profiled in Yield Shark in months.

Tony Sagami

30-year market expert Tony Sagami leads the Yield Shark and Rational Bear advisories at Mauldin Economics. To learn more about Yield Shark and how it helps you maximize dividend income, click here. To learn more about Rational Bear and how you can use it to benefit from falling stocks and sectors, click here.

QE has Grossly inflated Asset Prices

QE has Grossly inflated Asset Prices

We’re not hearing a lot these days about investment in new petroleum projects.

We’re not hearing a lot these days about investment in new petroleum projects.