Currency

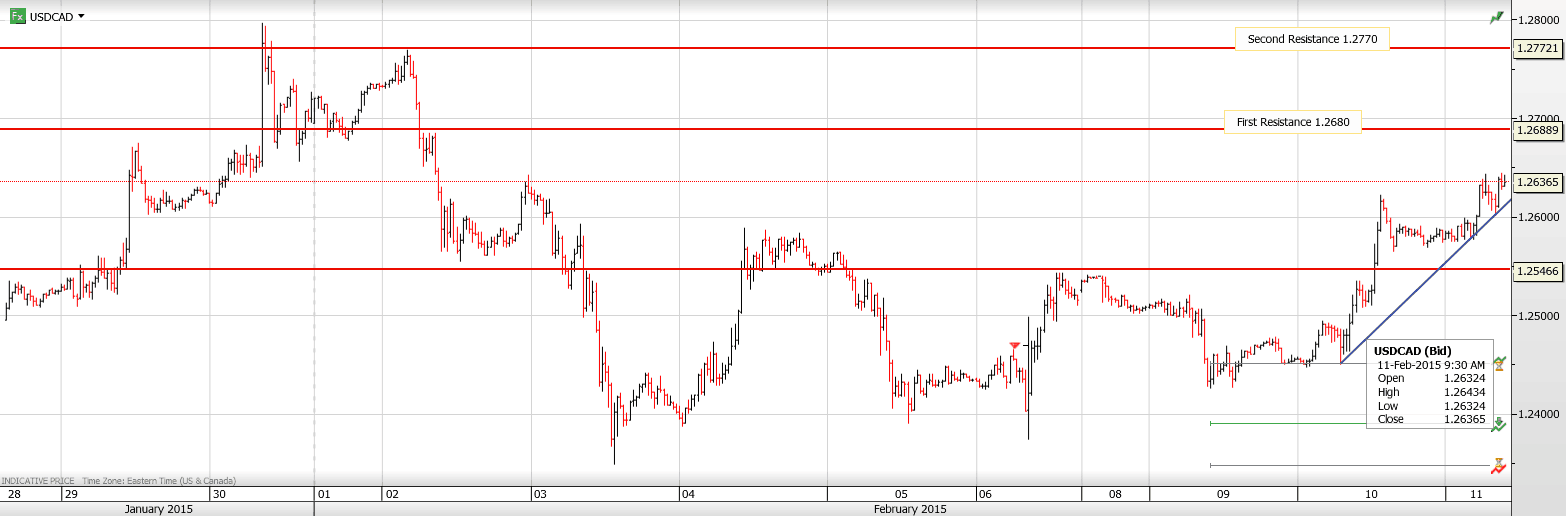

USD/CAD never really recovered from yesterday’s very dovish sounding speech by Bank of Canada Deputy Governor, Carolyn Wilkins. She stated that “Given the destructive recession Canada experienced, measures of economic slack that focus on the labour market show greater unused capacity than broader measures do”. USDCAD traders interpreted that line to mean that another rate cut was not just on the table but on the horizon as well and USDCAD soared. At the same time, oil traders were rethinking their conclusion that oil prices were heading higher. The US Energy Institute (EIA) issue a report projecting US oil supply growth until 2020. The slide in WTI prices added fuel to USDCAD demand. Soft oil prices and negative Canadian dollar sentiment will keep USDCAD in demand today.

Overnight, Japan was closed for a holiday but that did not stop USDJPY climbing to levels not seen since the beginning of the year. AUD and Kiwi both drifted lower on softer commodity prices. In Europe, EURUSD went nowhere ahead of the EU leaders summit on Greece. A press conference occurs sometime around 2 pm EST.

USDCAD technical Outlook

The intraday USDCAD technicals are bullish while trading above 1.2590 with a break above 1.2635-40 extending gains to 1.2730. A move below 1.2570 targets 1.2530 and then 1.2480. The short term uptrend remains intact above 1.2380

Today’s Range 1.2610-1.2680

![]()

One of the reasons we’ve all heard of George Soros is that back in 1992 he pulled off an epic financial coup by “breaking” the Bank of England. At the time the UK was trying to maintain a loose peg with the German Deutsche Mark, despite the fact that the two countries had very different rates of inflation (UK’s high, Germany’s low).

One of the reasons we’ve all heard of George Soros is that back in 1992 he pulled off an epic financial coup by “breaking” the Bank of England. At the time the UK was trying to maintain a loose peg with the German Deutsche Mark, despite the fact that the two countries had very different rates of inflation (UK’s high, Germany’s low).

To Soros’ practiced eye, this imbalance was clearly unsustainable and would eventually force the UK to devalue its currency to reflect the fact that it was living beyond its means and printing way too many pounds. Soros placed a big bet against the pound and sat back while the fundamentals won out. When Britain gave in and devalued, Soros made a billion dollars and became a household name.

Ever since, currency traders have dreamed of such conjunctions of government mismanagement and central bank cluelessness, hoping for their own Soros-level killings. But during the past couple of decades such sure things have been rare because currencies have floated more or less freely, which prevented huge imbalances from building up.

Now, however, thanks to the mess that is the eurozone and several other countries’ ill-advised dollar pegs, the world is once again a target-rich environment for speculators. The Swiss, for instance, have been going a little crazy trying to decide whether and/or how to peg the franc to the euro. And China, which runs a loose peg to the dollar, is looking like it might have to adjust its thinking in the not too distant future.

But right now the juiciest target is Denmark. A generally well-run country, it finds itself on the wrong side of the currency war, with the European Central Bank actively devaluing the euro against which the Danish krone is pegged. Capital has been flowing into Danish bonds seeking the relative safety of low inflation and stable state finances, which is pushing up the value of the krone. Maintaining the peg thus requires the Danes to create a lot of new kroner and use them to buy euros.

A soaring supply of national currency is inherently inflationary and destabilizing, which is the opposite of “well-run”. So just as the Swiss did last year, the Danes are both promising to maintain the peg and stressing out over the cost of doing so. Now the speculators smell blood:

Speculation Against Danish Euro Peg Proving Relentless

(Bloomberg) — Less than a week after Denmark resorted to its deepest rate cut ever amid historic currency interventions, forward rates suggest some traders and investors still aren’t convinced the central bank can save its euro peg.

SEB AB, the largest Nordic currency trader, says capital flows into AAA-rated Denmark forced the central bank to dump about $4.6 billion in kroner in the first three days of February alone, almost a third the record amount it sold in all of January. Nordea Bank AB, Scandinavia’s biggest lender, says Denmark will need to deliver another 25 basis-point cut to fight back demand for kroner, bringing the benchmark deposit rate to minus 1 percent.

“The pressure on the krone hasn’t eased yet,” Jens Naervig Pedersen, an economist at Danske Bank A/S in Copenhagen, said by phone. “We can see from the forward rates that the market views the current upward pressure on the krone as the greatest ever.”

Governor Lars Rohde addressed speculators last week in what he characterized as a verbal intervention to persuade them he won’t let the krone’s peg to the euro collapse. Such a scenario is “unthinkable” and the central bank will do “whatever it takes” to avoid it, he said after delivering a fourth rate cut in less than three weeks.

Denmark’s largest institutional investor, ATP, sent a clear message of trust in the peg the same day, revealing it hasn’t bothered to hedge its $110 billion in assets against the possibility that the nation’s currency regime might break.

Make no mistake, the Danes are the victims here. They’re behaving the way a country should behave, with an eye to long term stability. But the rest of the world — the eurozone in particular — is so indebted that its only choice is to inflate or die.

Which leaves solid countries like Denmark and Switzerland with a similar choice: inflate and throw decades of prudent management out the window, or watch their currencies soar against those of a profligate world, causing their export sectors to go extinct and their economies to slip into Depression.

The speculators, meanwhile, are not the villains in this story. They’re just pointing out the truth with their capital. And their honesty will be rewarded very soon.

In December 2014, the deteriorating market for metals and a suddenly floundering oil price pulled the resource-heavy TSX Venture Index to an all-time low.

Big board indices such as the S&P 500 are still reaching new highs each week, yet this is the second longest bear market since 1932 for gold stocks according to Barron’s Gold Mining Index (BGMI).

While it is difficult to discern if today’s market is truly the absolute bottom, the similarities in media headlines, the tone of discussion, and overall sentiment are reminiscent of bear markets past. That is why, in this infographic, we look at some of the major headlines at market bottoms over the past 35 years including those from the most recent downturn.

When it comes to companies such as those that make up the TSX Venture, it can be incredibly hard to judge fundamentals as there are no earnings or steady revenue growth for most companies. As a result, these markets are driven by greed and fear even more so than other sectors.

It’s important to be a contrarian and to go against the herd mentality. This doesn’t mean going against the grain no matter what, but it means thinking and acting with conviction based on fundamental market truths – regardless of what other people say.

We know that markets, especially those tied to natural resources, tend to be highly cyclical. With the large capital investments and timelines required to advance projects, massive supply challenges must be corrected in subsequent cycles. This can lead to either a rush to buy or sell, and therefore bull and bear markets.

We also know that investor sentiment is largely a psychological phenomenon that can be tied highly with emotions rather than fundamentals. The media can be a big part in echoing or reinforcing this sentiment.

Take a look at the headlines in bear markets bottoms over the last 35 years – do you think we’ve reached a similar place yet in this cycle?

• Citigroup predicts oil at $20 a barrel

• Citigroup predicts oil at $20 a barrel• Peaceful solutions to Ukraine crisis falling on deaf ears.

• Libya going up in flames.

OPEC’s strategy of choking off North American shale appears to be going according to plan. Baker Hughes reported another significant decline in the rig count for the week ending on February 6. The oil services firm reported that 87 rigs were pulled out of operations last week, which followed a record-breaking 94 rig decline the week before. The number of active rigs is now at its lowest level since 2011, and is down 29 percent since October.

This suggests that Saudi Arabia’s plan of making North American shale producers “sweat” is bearing some fruit. Oil prices have started to rise, and on February 9, OPEC published a report projecting an increase in demand for its oil by an estimated 430,000 additional barrels per day, which will come largely at the expense of rival producers. OPEC revised its projection for non-OPEC supply down by 420,000 barrels per day as a result of shale producers pulling back. Under this scenario, OPEC goes a long way to achieving its goal of reestablishing order in the oil markets, putting the pain of adjustment on the backs of shale drillers. With a contraction in North American shale, OPEC restores its primacy as a major market mover.

The International Energy Agency (IEA) largely agrees, at least on the short-term. The Paris-based organization released a parallel report forecasting a price rise in 2015 as North American shale producers begin to cut back on production, mostly beginning in the second half of the year. As a result, a “price rebound…seems inevitable,” the report concluded. On the other hand, the IEA is much more sanguine than OPEC about the longevity of the shale revolution. As soon as prices begin to rise, U.S. shale producers will bounce back, jumping from 3.6 million barrels per day in production from shale to 5.2 million barrels per day in 2020. The current bust is merely temporary. Complicating the price outlook, the IEA says, prices rise, causing shale to bounce back, which will in turn keep a lid on the extent of the price rise.

Both the IEA and OPEC could be way off the mark, however. According to Citigroup’s Ed Morse, who came a lot closer to predicting the oil bust than almost anyone else, oil prices may crash once again. The recent uptick in prices is more of a “head fake” than a real rally. In fact, the oil price recovery may chart a “W”-shaped course: crash, recover, crash, recover. That is because oil traders are putting too much weight on the rapid decline in oil rigs, expecting a swifter turnaround than Morse thinks is justified. Meanwhile, U.S. oil production is many months away from actually contracting. Citigroup thinks that oil prices could fall to $20 per barrel before it is all said and done.

That stands in sharp contrast to the $200 per barrel that OPEC’s Secretary-General thinks might be a possibility due to a lack of investment in new sources of production. Although it is unclear what happens next, one thing is for certain: oil price projections are all over the map. As of this week, oil prices have hit the pause button on the rally, pairing back some of the gains. WTI traded just below $51 per barrel on February 10, with Brent right around $57.

Of course, there is no shortage of geopolitical flashpoints that could influence the trajectory of oil price fluctuations in 2015. Libya, one of Africa’s most prolific oil producers, is disintegrating into a sea of flames. Rival factions are fighting over territory and political power, including control over Libya’s major oil fields and oil export terminals. Libya’s oil output has fallen precipitously to just 325,000 barrels per day.

But the oil markets could hit a major inflection point by mid-year. The negotiations between the west and Iran over its nuclear program will reach its denouement, culminating in either an historic deal or the breakdown of talks. The two sides have narrowed their differences considerably, but the final push may be the most difficult. Even if the U.S. and Iranian Presidents can come to terms, both sides would need to sell a deal to more hawkish and hardline elites back home. If Iran is brought back into the fold with a major deal sealed, oil markets could see a flood of oil come online just as the supply and demand picture begin to balance out, potentially causing prices to crater once again. On the other hand, if the discussions falter or derail, relations could deteriorate between Iran and the west, putting upward pressure on the price of crude. Time will tell, but both the American and Iranian sides have suggested that they are unwilling to extend the negotiations any further. It will be deal or no deal in the coming months.

The prospects for a peaceful solution to the crisis in Ukraine look even more daunting, if that is possible. German Chancellor Angela Merkel and French President Francois Hollande are conducting urgent diplomacy with Ukraine and Russia to try to calm the violence. Merkel and Hollande hope to meet with Russian President Vladimir Putin and Ukrainian President Petro Poroshenko in Minsk on Wednesday with the intention of reaching a ceasefire. Meanwhile, fighting continues as the Ukrainian military pushes back against rebel advancements in disputed territory in Ukraine’s east. The negotiations are set against a looming backdrop – the U.S. is moving towards providing Ukraine with military assistance, but appears to be awaiting the outcome of Merkel’s and Hollande’s diplomatic efforts.

Looking further east, China announced that it has made a major natural gas discovery in disputed waters in the South China Sea. The Lingshui 17-2 gas field could hold 100 billion cubic meters, equivalent to about 7 months of Chinese gas supply. Located about 150 kilometers south of the island of Hainan, the gas field could feed into existing tensions in the region.

Back in the U.S., the steelworkers strike at oil refineries entered its second week and even expanded to include several more locations. Workers in northwest Ohio and Indiana walked off the job, affecting two BP refineries. Negotiations with Shell, which is in talks with steelworkers on behalf of the oil industry, are ongoing. Refinery owners insist that the work stoppages will not affect output.

In the meantime, we invite you to read several of the most recent articles we have published which may be of interest to you:

Alaska May Provide Solution To Tar Sands Issue

Inefficiencies Abound In U.S. Shale

Ukraine To Disappear From EU Energy Picture By 2019

Another 5,000 Victims Of The Plunge In Oil Prices

Gazprom Confident In European Future Despite ‘New Cold War’

Oil Prices Most Volatile Since 2009

Rise Of The Vulture Investing Class

That’s all from your midweek intelligence report, we hope you enjoyed it and we´ll be back on Friday, with your latest energy market update, industry intelligence and special report.

Best regards,

Evan Kelly

News Editor, Oilprice.com

“Imagine some national (and probably global) volcanic eruption, initially flowing along channels of distress that were created during the Unraveling era and further widened by the catalyst. Trying to foresee where the eruption will go once it bursts free of the channels is like trying to predict the exact fault line of an earthquake. All you know in advance is something about the molten ingredients of the climax, which could include the following:

- Economic distress, with public debt in default, entitlement trust funds in bankruptcy, mounting poverty and unemployment, trade wars, collapsing financial markets, and hyperinflation (or deflation)

- Social distress, with violence fueled by class, race, nativism, or religion and abetted by armed gangs, underground militias, and mercenaries hired by walled communities

- Political distress, with institutional collapse, open tax revolts, one-party hegemony, major constitutional change, secessionism, authoritarianism, and altered national borders

- Military distress, with war against terrorists or foreign regimes equipped with weapons of mass destruction”

The Fourth Turning – Strauss & Howe – 1997

When you read pertinent passages from Strauss & Howe’s prophetic assessment of history from a generational perspective, eighteen years after its publication and seven years into the Crisis they forecasted with uncanny accuracy, you find yourself shaking your head and appreciating their visionary generational appraisal of antiquity. Those who scorn The Fourth Turning either haven’t read it, are ignorant of the cyclical nature of history, blindly believe in never ending human progress, or their salary is dependent upon not acknowledging the truth. A year consists of four seasons – Spring, Summer, Fall, and Winter. A long human life of 80 years consists of four phases – childhood, young adulthood, mid-life, and old age. Human beings tend to associate themselves with the cohort born within the roughly 20 year period that makes up one phase of life.

Members of a generation share an age location in history, tend to share some common beliefs and behaviors, including basic attitudes about risk taking, culture and values, civic engagement, family life, and tend to have a sense of common perceived membership in that generation. The generational attitudes, moods, leaders, and events that occur during recurring 80 year cycles drive the pathway of history. Strauss & Howe have been able to document the Turnings of Anglo-American history back to 1435. Like the seasons in a year, there have been cyclical turnings every twenty years or so for centuries. They can be described as High (Spring), Awakening (Summer), Unraveling (Fall), Crisis (Winter). Each turning is a reflection of generational interactions, moods, and attitudes. We are now seven years into a Crisis that will likely not climax until the late 2020’s.

The beginning of the new year has seen the usual avalanche of 2015 forecasts from mainstream media pundits, Wall Street gurus, Ivy League economists, journalists and bloggers. Most are paid to produce forecasts which promote their employer’s agenda; convince readers to buy their investment products, newsletters, or service; propagandize the government storyline; or validate their Ivy League academic theories. Those in the employ of the Deep State always produce forecasts of economic growth, positive developments, and never ending progress. They’ve never seen a recession coming, the stock market declining, or war looming. None of these people saw the 2008 Financial Crisis coming. They all believe 2015 will be a great year. They are narrow minded linear thinkers who are willfully ignorant of history or purposefully peddling propaganda for a paycheck.

Making annual forecasts in the midst of a 20 year Fourth Turning Crisis is rather pointless. Predicting improvement or progress in the midst of a Crisis is nothing but a futile exercise in mental masturbation. Fourth Turnings, like a protracted, brutal, frigid, gloomy, stormy winter of discontent, may have an occasional let up in intensity, but will rapidly revert back to turbulence, danger, and volatility. When I wrote Fourth Turning Accelerating in June of last year, I made the case that core elements of this Crisis – debt, civic decay, and global disorder – were combining to provide an impetus to the next dire phase of this relentless blizzard of pain, suffering, chaos and war.

“Reflect on what happens when a terrible winter blizzard strikes. You hear the weather warning but probably fail to act on it. The sky darkens. Then the storm hits with full fury, and the air is a howling whiteness. One by one, your links to the machine age break down. Electricity flickers out, cutting off the TV. Batteries fade, cutting off the radio. Phones go dead. Roads become impossible, and cars get stuck. Food supplies dwindle. Day to day vestiges of modern civilization – bank machines, mutual funds, mass retailers, computers, satellites, airplanes, governments – all recede into irrelevance.

Picture yourself and your loved ones in the midst of a howling blizzard that lasts several years. Think about what you would need, who could help you, and why your fate might matter to anybody other than yourself. That is how to plan for a saecular winter. Don’t think you can escape the Fourth Turning. History warns that a Crisis will reshape the basic social and economic environment that you now take for granted.” – Strauss & Howe – The Fourth Turning

Putting forecasting into perspective during Fourth Turnings is easy when you have a grasp on history. Imagine there were pundits pontificating on CNBC or CNN in 1936, the seventh year of the Great Depression Crisis or 1780, the seventh year of the American Revolution Crisis. Most historians refer to the Great Depression as the period from the Great Crash of 1929 until our entry into World War II in 1941. Annual forecasts of improvement would be meaningless to people living through this brutal period in our history.

If Jim Cramer was assessing the period from 1934 through 1936 on his daily radio show, he would have been gushing about GDP growth of 10.8%, 8.9% and 12.9%. He would have been effusive about the 300% surge in the Dow Jones Index from the 1933 low to the 1936 high. CNN would be doing special reports about the tremendous success of New Deal programs, as Federal spending and handouts accounted for the entire surge in GDP. But, in reality the average American continued to struggle to survive, as unemployment ranged between 17% and 22% during this time and only the rich owned stocks. Another 10 years of hardship, war, and death on a grand scale awaited them. Perspective and context are essential when attempting to assess periods in history. You get no context from the entertainers passing for journalists in today’s world.

The beginning of 1780 saw Washington and his troops surviving the harshest winter of the 18th Century in Morristown, NJ as the 5th year of war still left the outcome highly in doubt. CNN would have blamed the polar vortex for the temporary lull in patriot fortunes. Defeats in battles against the British in South Carolina and the uncovering of Benedict Arnold’s plot to surrender West Point to the British would have been spun as minor setbacks. Cornwallis’ surrender at Yorktown was almost two years away. The Articles of Confederation hadn’t yet been signed and the U.S. Constitution wouldn’t be signed until 1787. The Crisis wouldn’t end for another fourteen years, in 1794.

Fourth Turnings have their own rhythm and pace. The reactions to events and mood changes of generational cohorts interact to provide the dynamic that drives Fourth Turnings. The specific events are not foreseeable but human weaknesses, faults, flaws, failings, strengths, intellect, and emotions are consistent across the ages. Human nature does not change, therefore it is predictable. Those who wish for this Fourth Turning to accelerate and get to the climax sooner may want to rethink their desire. The Civil War Crisis was accelerated because all parties were intransigent and unwilling to compromise or pause. The result was 700,000 Americans killed in four years, representing 5% of the entire male population. This Fourth Turning could be accelerated with the push of a button and millions killed in an instant. I don’t think anyone wants that kind of climax. We are entering a banquet of consequences where our choices will make a difference.

“A Fourth Turning harnesses the seasons of life to bring about a renewal in the seasons of time. In so doing, it provides passage through the great discontinuities of history and closes the full circle of the saeculum. The Fourth Turning is when the Spirit of America reappears, rousing courage and fortitude from the people. History is seasonal, but its outcomes are not foreordained. Much will depend on how tall we stand in the trials to come.” – Strauss & Howe – The Fourth Turning

The Shadow of Crisis

“Don’t think you can escape the Fourth Turning the way you might today distance yourself from news, national politics, or even taxes you don’t feel like paying. History warns that a Crisis will reshape the basic social and economic environment that you now take for granted. The Fourth Turning necessitates the death and rebirth of the social order. It is the ultimate rite of passage for an entire people, requiring a luminal state of sheer chaos whose nature and duration no one can predict in advance.” – Strauss & Howe – The Fourth Turning

Just as you can’t turn the clock back to the glorious warm days of Summer or the delightfully pleasant cool days of Fall, the dark, foreboding, bitter days of Winter will bring forth raging blizzards, dangerous sub-zero temperatures, and vicious gale force winds. And there is no way to avoid, sidestep, or escape the trials and tribulations which will sweep away the existing social order and replace it with something better or possibly far worse. There are no guarantees this Crisis will resolve itself in a positive manner. The spark that catalyzed the Crisis mood in 2008 was the global financial implosion caused by Wall Street bankers committing the greatest control fraud in world history, corrupt captured politicians’ spineless failure to address the nation’s spending and debt problems, and the Federal Reserve creating a housing and stock bubble through their loose monetary policies and complete failure to regulate the Too Big To Trust Wall Street banks.

The inability of the linear thinking ruling class to acknowledge the seriousness of our current circumstances and the implications of the era of depression and violence the country is about to experience can be witnessed on a daily basis by listening to mainstream media talking heads or politicians of all stripes who bloviate about economic improvement and progress just ahead. Could there be a better example of myopia, delusion and willful ignorance than the theme and opening line of Obama’s State of the Union speech:

“THE SHADOW OF CRISIS HAS PASSED”

Do Obama and his advisors actually believe this Crisis is over? Or is he purposely misleading the American people about the seriousness of our circumstances because he has been instructed to do so by the men who really pull the levers of this country – Wall Street bankers, shadowy billionaires, and the military industrial complex. If the Crisis has passed, why has the 30 year bond yield fallen to an all-time low? Why does the Fed maintain an emergency stance by continuing to keep interest rates at 0% if the economy is really growing at over 4%, unemployment has really fallen from 10% to 5.7%, corporate profits are at all-time highs, and the stock market has risen by 200% to record highs?

In Part Two of this article I’ll prove the shadow of crisis has not passed, and the core elements of Crisis – debt, civic decay, and global disorder – get worse by the hour.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair