Stocks & Equities

Some think that we are in a secular bull market that began in March 2009. I disagree because that would mean that the secular bear market only lasted for 9 years, Mar-00-Mar’09, when 17 years is more typical. Also, as of now the inflation adjusted S&P 500 has not made a new high reached in March 2000 (it is close, though). Warren Buffet seems to have been aware of this 17-year secular bull & bear cycles when he commented in 1999 that the next 17 years for the US stock market would not be the same as the last 17 years. Here is how I date the last two secular bull and bear markets in the current longwave cycle that began in the middle of 1949, including the probable outcome of the current secular bear market: Prior to 1995 there were periods of mostly sideways moves during a secular bull or bear market, with cyclical market moves, e.g., Feb’66-Jan’73, but since then we only have relatively long cyclical bull markets followed by very sharp bear markets and that is expected to be the case when the current cyclical bull market ends.

Prior to 1995 there were periods of mostly sideways moves during a secular bull or bear market, with cyclical market moves, e.g., Feb’66-Jan’73, but since then we only have relatively long cyclical bull markets followed by very sharp bear markets and that is expected to be the case when the current cyclical bull market ends.

Fig. 1 above shows the current cyclical bull market, approximately 6 years in duration, and the cyclical bull market of Nov’94-Mar’00, 64 months in duration, both over-valued compared to the cyclical bull market of 2003-07. Interestingly, the last 33 months of the current market are following an identical trend line, shown in brown, with slightly over 20% per year gain, as the bull market of the late 1990s.

Most cyclical bear markets take place in the context of the economic cycle, i.e., a recession follows downturn in the stock market. This has been the norm since 1995 and there couldn’t be any doubt that the end of the current bull market would foreshadow the next recession. If the current bull market is nearing the end then the recession couldn’t be far behind.

Extremes of Over-Valuation

Using all the well-known measures of valuation of the US stock market, the current market is the most over-valued except for the bull market of the late 1990s, and probably the late 1920s. I posit that the current market is more over-valued than the market of 1990s. What is my valuation criterion? The economic growth, the mother’s milk of the growth of the stock prices.

Looking at the economic data over a 7-year period smoothes out most of the cyclicality in the data due to the economic cycles. The annual GDP growth and the annual employment growth for the past 7 years is 1.21% and 0.31%, respectively. The same numbers 15 years ago were 3.7% and 2.6%! The economic and the employment growth is less than 1/3rd of the growth 15 years ago that was fueling the bull market of late 1990s. I rest my case.

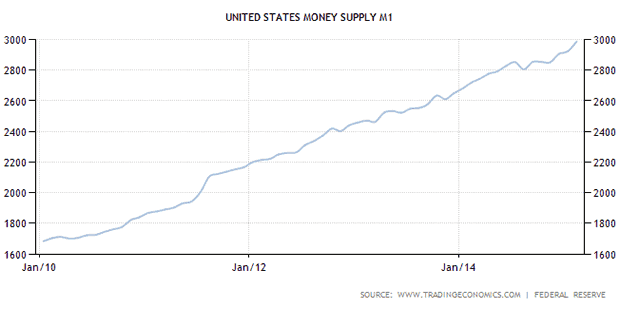

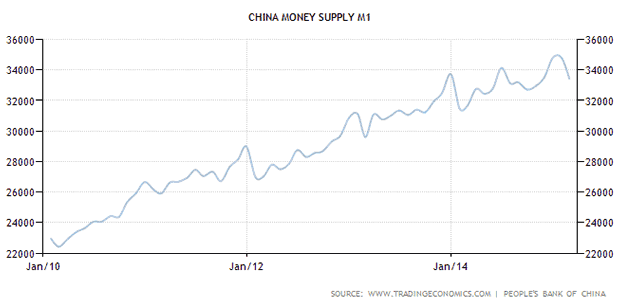

That stats just keep getting stranger and, if you’re a policymaker or an investor, scarier. According to a (now widely publicized) McKinsey & Co study, instead of deleveraging after the debt-induced crisis of 2008-2009, the world borrowed another $57 trillion. And most of the advanced economies ran their monetary printing presses flat-out. The next couple of charts show what the US and China, for instance, have been up to since 2010:

Now, conventional economic theory says that double-digit growth in debt and money creation should produce a boom, and that today our biggest problem should be too many people getting big raises at work. Yet that’s not the case at all:

Weak Japan business confidence highlights recovery doubts

(Daily Mail) — Doubts about a rebound in Japan’s economy are rippling through boardrooms across the country, a key central bank survey suggested Wednesday, as efforts to revive growth falter. The Bank of Japan’s closely watched Tankan report showed confidence among big manufacturers stood at plus 12 in March, flat from the previous survey and missing expectations that the level would come in at 14.

While sentiment among non-manufacturers was more upbeat, they pared profit expectations while Japan’s increasingly pessimistic corporate titans trim their spending plans.

The survey of more than 10,000 companies — which shows the difference between the percentage of firms that are optimistic and those that see conditions as unfavourable — is the most comprehensive indicator of how Japan Inc. is faring.

“A weak yen and lower oil prices has provided some support (to the economy) but the Tankan showed that firms, particularly manufacturers, are now acutely aware that overseas demand is softening,” SMBC Nikko Securities said in a report.

The tepid survey comes days after separate data showed output from Japanese factories shrank by a worse-than-expected 3.4 percent in February, while inflation stalled as a key measure of prices was flat for the first time in nearly two years. “Japanese companies aren’t convinced the economy is going to get stronger,” said Atsushi Takeda, an economist at Itochu Corp. “Without an improvement in business confidence, it’s hard to imagine Japan will achieve a full-fledged recovery.”

Chinese government admits that things aren’t going so well

(Business Insider) — A high-level Chinese official on Sunday made the government’s first admission that the country’s economic slowdown was not going as planned. China’s top banker, Zhou Xiaochuan, told a meeting of regional leaders that his country’s growth rate had tumbled “a bit too much.”

“China’s inflation is also declining, so we need to be vigilant to see if the disinflation trend will continue, and if deflation will happen or not,” said Zhou, governor of the People’s Bank of China. His remarks were made at the Boao Forum for Asia, an annual conference on the island of Hainan in southern China.

For many, the way he described China’s health was no surprise. The country’s economy has not been growing this slowly since the 1990s. Debt-laden corporations are seeing sickly profit margins. Banks are carrying loads of debt, too, and the housing market is slowing. China’s official 2015 GDP growth target is 7%, but that seems shaky.

U.S. job growth brakes sharply, clouds Fed rate hike timing

(Reuters) — U.S. employers added the fewest number of jobs in more than a year in March, the latest sign of weakness in the economy and one likely to further delay an anticipated interest rate increase by the Federal Reserve.

Nonfarm payrolls rose 126,000 last month, less than half February’s pace and the smallest gain since December 2013, the Labor Department said on Friday.

The weakness was concentrated in the goods-producing sector, which has been hurt by a strong dollar and lower crude oil prices. Leisure and hospitality also saw a sharp slowdown in jobs growth, suggesting harsh winter weather could have dragged on hiring.

While the jobless rate held at a more than 6-1/2-year low of 5.5 percent, the workforce shrank. The labor force participation rate returned to a more than 36-year low reached late last year.

“The report confirms the emerging narrative of slowing growth momentum seen in the other economic indicators. It will weaken the argument for a mid-year (rate) hike,” said Millan Mulraine, deputy chief economist at TD Securities in New York.

The tepid increase in payrolls ended 12 straight months of job gains above 200,000 – the longest streak since 1994. In addition, data for January and February were revised to show 69,000 fewer jobs created than previously reported, giving the report an even weaker tone.

After its robust stretch, the jobs figures now appear more in line with other signals from consumer spending to housing starts and manufacturing that have suggested the economy grew at a sub-1 percent annual rate in the first quarter. Economists had forecast that payrolls would rise 245,000 last month.

So is anybody out there doing okay? Well, yes, sort of. In relative terms at least, Europe is suddenly a bit of a success story:

Eurozone Q4 Growth Reflects Broad-Based Recovery

(RT) — The Eurozone economy expanded as initially estimated in the fourth quarter on broad-based support from spending, investment and exports.

Gross domestic product grew 0.3 percent sequentially, slightly faster than the third quarter’s 0.2 percent expansion, second estimates from Eurostat showed Friday. The statistical office confirmed the estimate released on February 13.

All components on the expenditure side of GDP expanded in the fourth quarter. While the growth in household spending moderated to 0.4 percent from 0.5 percent, government spending growth remained unchanged at 0.2 percent.

Investment increased by 0.4 percent, after staying flat a quarter ago. At the same time, growth in exports eased to 0.8 percent from 1.5 percent and that in imports to 0.4 percent from 1.7 percent.

Year-on-year, the economy expanded 0.9 percent as estimated, which was marginally above the 0.8 percent growth posted in the third quarter. Over the whole year of 2014, the 19-nation currency bloc expanded 0.9 percent versus a 0.5 percent contraction in 2013.

What lessons are we supposed to draw from this? One would be that if you borrow too much money it’s hard to generate growth by borrowing even more. Austrian economics, still the only branch of the discipline that pays attention to debt levels, holds that a boom has to be followed by a deleveraging in order to wipe the slate clean. You literally can’t have a boom without a bust.

Another lesson is that currency devaluation works, at least in the short run. Here’s the euro versus the dollar over the past year:

It’s down by nearly a third and by lesser but still considerable amounts versus the yen and yuan. And low and behold, the eurozone is doing better than its trading partners. This is what the currency war script says should happen, and leads to an obvious conclusion: If the other big economies are going to avoid dropping into a unique kind of recession — one in which interest rates start out at historically low levels — then they’ll have to fight back with devaluations of their own. Either Japan has to cheapen the yen some more (it has already devalued versus the dollar in the past year) and China has to break its link to the dollar and let the yuan fall, or the US has to stop talking about raising rates, get serious about growth and do something to bring down all the non-euro currencies simultaneously. Otherwise, today’s bad numbers will turn into tomorrow’s catastrophic ones.

But of course while all this is going on debt will keep rising and leverage will become even more extreme. The deleveraging, when it comes, will be epic.

We live in a time of unprecedented financial repression. As I have continued writing about this, I have become increasingly angry about the fact that central banks almost everywhere have decided to address the economic woes of the world by driving down the returns on the savings of those who can least afford it – retirees and pensioners.

This week’s Outside the Box, from my good friend Chris Whalen of Kroll Bond Rating Agency, goes farther and outlines how a low-interest-rate and massive QE environment is also destructive of other parts of the economy. Counterintuitively, the policies pursued by central banks are actually driving the deflationary environment rather than fighting it.

This is a short but very powerful Outside the Box. And to further Chris’s point I want to share with you a graph that he sent me, from a later essay he wrote. It shows that the cost of funds for US banks has dropped over $100 billion since the financial crisis, but their net interest income is almost exactly the same. What changed? Banks are now paying you and me and businesses $100 billion less. The Fed’s interest-rate policy has meant a great deal less income for US savers.

Central Banks, Credit Expansion, and the Importance of Being Impatient

This research note is based on the presentation given by Christopher Whalen, Kroll Bond Rating Agency (KBRA) Senior Managing Director and Head of Research, at the Banque de France on Monday, March 23, 2015, for an event organized by the Global Interdependence Center (GIC) entitled “New Policies for the Post Crisis Era.” KBRA is pleased to be a sponsor of the GIC.

Summary

Investors are keenly focused on the Federal Open Market Committee (FOMC) to see whether the U.S. central bank is prepared to raise interest rates later this year – or next. The attention of the markets has been focused on a single word, “patience,” which has been a key indicator of whether the Fed is going to shift policy after nearly 15 years of maintaining extraordinarily low interest rates. This week, the Fed dropped the word “patience” from its written policy guidance, but KBRA does not believe that the rhetorical change will be meaningful to fixed income investors. We do not expect that the Fed will attempt to raise interest rates for the balance of 2015.

This long anticipated shift in policy guidance by the Fed comes even as interest rates in the EU are negative and the European Central Bank has begun to buy securities in open market operations mimicking those conducted by the FOMC over the past several years. Investors and markets need to appreciate that, regardless of what the FOMC decides this month or next, the global economy continues to suffer from the effects of the financial excesses of the 2000s.

The decision by the ECB to finally begin U.S. style “quantitative easing” (QE) almost eight years after the start of the subprime financial crisis in 2007 speaks directly to the failure of policy to address both the causes and the terrible effects of the financial crisis. Consider several points:

- QE by the ECB must be seen in the context of a decade long period of abnormally low interest rates. U.S. interest rate policy has been essentially unchanged since 2001, when interest rates were cut following the 9/11 attack. The addition of QE 1-3 was an effort at further monetary stimulus beyond zero interest rate policy (ZIRP) meant to boost asset prices and thereby change investor tolerance for risk.

- QE makes sense only from a Keynesian/socialist perspective, however, and ignores the long-term cost of low interest rate policies to individual investors and financial institutions. Indeed, in the present interest rate environment, to paraphrase John Dizard of the Financial Times, it has become mathematically impossible for fiduciaries to meet the beneficiaries’ future investment return target needs through the prudent buying of securities. (See John Dizard, “Embrace the contradictions of QE and sell all the good stuff,” Financial Times, March 14, 2015.)

- The downside of QE in the U.S. and EU is that it does not address the core problems of hidden off- balance sheet debt that caused the massive “run on liquidity” in 2008. That is, banks and markets in the U.S. globally face tens of trillions of dollars in “off-balance sheet” debt that has not been resolved. The bad debt which is visible on the books of U.S. and EU banks is also a burden in the sense that bank managers know that it must eventually be resolved. Whether we talk of loans by German banks to Greece or home equity loans in the U.S. for homes that are underwater on the first mortgage, bad debt is a drag on economic growth.

- Despite the fact that many of these debts are uncollectible, governments in the U.S. and EU refuse to restructure because doing so implies capital losses for banks and further expenses for cash- strapped governments. In effect, the Fed and ECB have decided to address the issue of debt by slowly confiscating value from investors via negative rates, this because the fiscal authorities in the respective industrial nations cannot or will not address the problem directly.

- ZIRP and QE as practiced by the Fed and ECB are not boosting, but instead depressing, private sector economic activity. By using bank reserves to acquire government and agency securities, the FOMC has actually been retarding private economic growth, even while pushing up the prices of financial assets around the world.

- ZIRP has reduced the cost of funds for the $15 trillion asset U.S. banking system from roughly half a trillion dollars annually to less than $50 billion in 2014. This decrease in the interest expense for banks comes directly out of the pockets of savers and financial institutions. While the Fed pays banks 25bp for their reserve deposits, the remaining spread earned on the Fed’s massive securities portfolio is transferred to the U.S. Treasury – a policy that does nothing to support credit creation or growth. The income taken from bond investors due to ZIRP and QE is far larger.

- No matter how low interest rates go and how much debt central banks buy, the fact of financial repression where savers are penalized to advantage debtors has an overall deflationary impact on the global economy. Without a commensurate increase in national income, the elevated asset prices resulting from ZIRP and QE cannot be validated and sustained. Thus with the end of QE in the U.S. and the possibility of higher interest rates, global investors face the decline of valuations for both debt and equity securities.

- In opposition to the intended goal of low interest rate and QE policies, we also have a regressive framework of regulations and higher bank capital requirements via Basel III and other policies that are actually limiting the leverage of the global financial system. The fact that banks cannot or will not lend to many parts of society because of harsh new financial regulations only exacerbates the impact of financial repression. Thus we take income from savers to advantage debtors, while limiting credit to society as a whole. Only large private corporations and government sponsored enterprises with access to equally large banks and global capital markets are able to function and grow in this environment.

So what is to be done? KBRA believes that the FOMC and policy makers in the U.S. and EU need to refocus their efforts on first addressing the issue of excessive debt and secondly rebalancing fiscal policies so as to boost private sector economic activity. Low or even negative interest rate policies which punish savers in order to pretend that bad debts are actually good are only making things worse and accelerate global deflation. Around the globe, nations from China to Brazil and Greece are all feeling the adverse effects of excessive debt and the related decline in commodity prices and overall economic activity. This decline, in turn, is being felt via lower prices for both commodities and traded goods – that is, deflation.

In the U.S., sectors such as housing and energy, the effects of weak consumer activity and oversupply are combining into a perfect storm of deflation. For example, The Atlanta Fed forecast for real GDP has been falling steadily as the underlying Blue Chip economic forecasts have also declined. The drop in capital expenditures related to oil and gas have resulted in a sharp decline in related economic activity and employment. Falling prices for oil and other key industrial commodities, weak private sector credit creation, falling transaction volumes in the U.S. housing sector, and other macroeconomic indicators all suggest that economic growth remains quite fragile.

To deal with this dangerous situation, the FOMC should move to gradually increase interest rates to restore cash flow to the financial system, following the famous dictum of Adam Smith that the “Great Wheel” of circulation is the means by which the flow of goods and services moves through the economy:

“The great wheel of circulation is altogether different from the goods which are circulated by means of it. The revenue of the society consists altogether in those goods, and not in the wheel which circulates them” (Smith 1811: 202).

Increased regulation and a decrease in the effective leverage in many sectors of banking and commerce have contributed to a slowing of credit creation and economic activity overall. And most importantly, the issue of unresolved debt, on and off balance sheet, remains a dead weight retarding economic growth. For this reason, KBRA believes that investors ought to become impatient with policy makers and encourage new approaches to boosting economic growth.

Related Publications:

- U.S. Real Estate Prices Show Signs of Rising Again (Published February 23, 2015)

- GSE Litigation Affirms that Fannie Mae and Freddie Mac are Sovereign Credits(Published February 19, 2015)

- Swiss Francs & Global Debt Deflation (Published January 21, 2015)

Every few centuries or so, an amazing new technology comes along that fundamentally changes human civilization.

Every few centuries or so, an amazing new technology comes along that fundamentally changes human civilization.

There are so many other examples throughout history. The Agricultural Revolution. The Industrial Revolution. The invention of the printing press.

The printing press was a particularly interesting parallel for what’s happening today.

Before the printing press, people were living in the dark. Their information was heavily controlled, and they were forced to rely on the ‘authorities’ for personal, financial, educational, and spiritual guidance.

The printing press changed everything. It was an extraordinarily powerful social technology that spawned entire political revolutions and the rapid advance of human education.

In Europe, the number of printed books went from millions to literally billions.

….continue reading HERE

Recognized as the world’s single biggest attraction for high rollers at the gambling tables, Macau is the only location in the People’s Republic of China where betting on the Roll of the dice is legal. Macau is a just short ferry ride from Hong Kong, through which many mainlanders travel to get to the casinos. As such, the former Portuguese colony saw its annual casino and entertainment revenues soar to a combined $44-billion in 2014; or 7-times that of the Las Vegas Strip. For Macau, the boom times began in 2010 when casino revenues increased +58% and was followed by a +42% gain in 2011.

However, the share prices of the biggest gaming operators in Macau suffered their worst year ever in 2014, as Beijing launched a major crackdown on corruption and money laundering in the colony. Chinese President Xi Jinping’s bid to catch the mobsters scared off many of the high rollers, – the so-called “VIP segment” that accounts for about two-thirds of Macau’s casino receipts. Operators such as Macau Legend Development<1680.hk>, owners of The Landmark, MGM China Holdings <2282.hk>, Galaxy Entertainment <0027.hk>, which is building Galaxy I, Galaxy II and Galaxy III casinos on the Cotai strip, and multi-national casino operators, Wynn China <1128.hk> and Sands China <1928.hk>, lost a combined $73-billion of market value last year.

Macau is dependent on big spenders from the mainland, and in the month of December ’14, the results of the crackdown were starting to show up on the casinos’ top line; revenues had fallen to $2.9-billion, posting a stunning -30% year-on-year decline. It was the seventh consecutive month of decline and the biggest drop since Macau began recording monthly revenues 10-years earlier. Casino operators had plans to expand their operations on the Cotai Strip, and transform it into a mass market of resorts. However, the VIP heyday in Macau appears to be over. Instead, much of the “hot money” that used to flow through Macau began sweeping through Hong Kong and into the Chinese stock markets.

While Beijing was busy cracking down on money laundering in Macau, it was also sanctioning its securities regulators, stock brokerage firms, overseers of the stock exchanges, and hundreds of high-tech engineers, to begin working night and day to launch the world’s third biggest casino, – dubbed “Shanghai – Hong Kong -Stock Connect.” It would allow global investors to trade Chinese Shanghai “A-shares” for the first time, through brokers located in Hong Kong, and mainland Chinese investors could trade Hong Kong’s “H-shares” index via the Shanghai Stock Exchange, subject to quotas both ways. The combined size of the Chinese and Hong Kong markets is roughly $10.5-trillion today, behind only the combined $27-trillion size of New York Stock Exchange and Nasdaq.

Since April ’14, when the HK-Shanghai “Connect” was first announced to the public, there’s been an unprecedented level of coordination between multiple parties – including 100 banks and brokers, asset managers, the two exchanges, their clearing and settlement providers, data providers, technology firms and several regulators. The trading link has been hailed as a milestone in the opening up of China’s capital markets, allowing foreign investors to trade in and out of Chinese stocks in real time.

The HK/Shanghai stock-connect has added 855-companies with $1-billion+ (market cap) to the global investable universe, and has created the world’s 3rd largest equity market global by market-cap & turnover, only behind the NYSE and the Nasdaq. The southbound link of “Stock Connect” allows Chinese investors to trade 266 stocks of companies listed in the Hang Seng Composite Large-Cap and Mid-Cap Indexes that includes some “H-share” companies. Foreign investors with brokerage accounts in Hong Kong can now trade 568 Shanghai “A-shares,” through the northbound link.

By chasing the high rollers out of Macau and steering them into the Chinese stock markets, the fortunes of shareholders in Chinese casino and brokerage stocks was turned upside down. The share price of HK- Hong Kong Exchanges and Clearing (HK-Ex) <0388.HK> has soared by +63% compared with a year ago to HK$195 /share. HK-Ex is the sole operator of the stock market and futures market in Hong Kong, and also provide integrated clearing, settlement, and depository services. Its OTC Clear provides interest rate derivatives and non-deliverable forwards clearing and settlement services to its members. HKEx provides market data through its data dissemination entity, and also owns the London Metal Exchange. Stock Connect has boosted the average daily value of trading on the HKEx by +38% to HK$93-billion and its Empire has a total market capitalization of around $30.5-billion today.

On the flip side, the share price of Galaxy Entertainment <0027.hk> has lost more than half of its peak value to $20-billion today. Galaxy owns and operates the Star World Hotel and Casino – a luxury 5-star property on the Macau peninsula, and operates four City Club casinos in Macau. On March 23rd, the Macau government forecasted gaming revenue would fall -32% this year, compared with 2014. Worse yet, Macau’s Chief executive Fernando Chui, warned of a “New Normal” in which government regulation of the gaming sector would only increase. A full smoking ban in 2016 could weigh on VIP revenues.

Retail Investors Stampede into Shanghai Red-chips; According to the Chinese Zodiac, the year 2015 is called the “Year of the Goat.” People born in a Year of the Goat are generally believed to be gentle mild-mannered, shy, stable, sympathetic, amicable, and brimming with a strong sense of kindheartedness and justice. Although they look gentle on the surface, they are tough on the inside, always insisting on their own opinions. They have strong inner resilience and excellent defensive instincts. Though they prefer to be in groups, they do not want to be the center of attention. They are reserved and quiet, most likely because they like spending much time in their thoughts.

However, the share of good fortune for those born in a “Year of the Goat,” is not be very good. Instead, they often get involved in financial difficulties. Therefore, it’s advised that they should adopt conservative strategies when dealing with investments. They should try their best to increase their income, decrease their expenditure, and live within their means. They are advised to restrain themselves from gambling too much in order to avoid big losses.

However, the vast majority of traders that are operating in the Chinese markets these days, have no such inhibitions about gambling. Instead, they are feverishly bidding up red-chip shares on the China-300 Index, which has nearly doubled in value since the start of July ’14. Chinese retail investors are flocking to the stock market, and they’re using margin loans to amplify (ie; leverage) the size of their investments. Buying on margin accounts for a fifth of daily turnover. Retail participation in Shanghai was always high. Over the last five years, retail investors accounted for 80% of A-share market turnover. This ratio hit 90% this year. About 4-million new account were opened in March, bringing the total to 182-million. Two-thirds of new investors have never attended or graduated from high school.

Many Chinese companies have dually listed shares in Shanghai (A-shares) and in Hong Kong (H-shares). Today, the A-shares are trading at a premium of +32%, on average, above their H-share counterparts (and above ETF’s on the US-exchanges). This indicates that arbitrageurs are not yet able to buy the cheaper shares in Hong Kong and sell those shares into the more expensive Shanghai market, thereby driving the premium to zero. One company’s A-shares and H-shares, while representing the same underlying assets and cash flows, are not yet interchangeable. To track this, the Hang Seng China A/H Premium Index measures the price spread between the Top-57 companies domiciled in Mainland China, and with A-shares listed in Shanghai and H-shares in the Hang Seng China Enterprises Index.

The superior performance of A-shares over H-shares since the launch of Stock Connect on Nov 17th, can also be seen by the price differential between the shares of China’s biggest stock broker, Citic Securities, traded in Shanghai under ticker symbol; <600030.ss,> and in Hong Kong, traded under symbol <6030.hk>. When converting Citic Securities H-shares into the yuan, – it’s easy to see the Shanghai price is nearly 10-yuan /share higher (ie about +50% higher). Trying to level the playing field, China’s Securities Regulatory Commission agreed on March 26th to allow mainland-based mutual funds to use “Stock Connect” to invest in the Hong Kong market. The Bullish news spurred risk loving traders to scoop up Hong Kong-listed H-shares, driving the index to its highest level in four years.

On Dec 29th, Citic Securities said it would issue of up to 1.5-billion of Hong Kong-listed H-shares to raise capital and help expand its businesses including margin trading in Shanghai. Haitong Securities, China’s second-biggest listed broker, has also announced a plan to raise HK$30-billion in a private share placement in Hong Kong, also mainly to expand margin loans. Citic says up to 70% of proceeds will be used for margin loans. On the Shanghai Stock Exchange alone, the amount of margin loans reached 684-billion yuan ($110-billion) more than double July’s 284-billion yuan.

No Replay of Shanghai Stock Bubble of 2006-07; It seems like déjà vu all over again, with memories of the Jan-2006– October 2007 Shanghai Bubble, still fresh in many traders’ minds. However, one dynamic that is very different this time around, – the PBoC is not trying to burst the Shanghai rally in 2015 with a tighter monetary policy. In fact, – it’s doing just the opposite, – it’s inflating the 2014-15 bubble with an easier money policy. It’s for this basic reason that many Chinese traders believe the recent doubling of the China-300 Index is sustainable over the longer term. That’s because the PBoC is currently fighting deflation, or steadily declining prices at the producer level, (-4.8% from a year ago), and can afford to inject more liquidity into the markets. The near doubling of the China-300 stock index is also the mirror image of the -50% “Crash in Crude Oil’ prices that began at the start of July ’14. Sharply lower prices for crude oil, petrol, grains, industrial metals, and other commodities are delivering a huge windfall to China’s economy, – the world’s biggest importer of natural resources, and Chinese households are enjoying the benefits of increased purchasing power.

By some estimates, Beijing will save as much as $200-billion this year on imports, even while it steps-up purchases of crude oil, copper, soybeans, rubber, and iron ore, –much of it piling up at the northeastern Dalian port and other trade gateways. China is saving over $600-million per day on its oil import bill, following the -50% plunge in crude oil prices since last summer. The windfall comes on top of China’s steady trade surpluses and $4.2-trillion in foreign currency reserves, that makes it easy for Beijing to spend $25-billion this year building up its reserves of grains, edible oils, and “other materials, ” a +33% rise over 2014 when stockpile-spending rose +22%.

The Commerce Ministry confirmed in a recent briefing that Beijing is boosting commodity imports to take advantage of lower global prices. Ramped-up purchases of oil are helping China reach its goal of a 90-day supply in its strategic petroleum reserve. Imports of iron ore rose +14% last year over 2013 levels, while prices plummeted -50%, for a saving of $30-billion. For copper, China increased its purchases +7% last year, while prices declined -20%. Some 400,000-tons of the copper purchased was stashed in its strategic reserve. Unlike other countries, China’s hasn’t depreciated its currency, so it gets the full benefit from buying less expensive commodities priced in US$’s.

Ironically, one reason for the 4-year Bearish trend in the commodities markets has been the notable slowdown in China’s economy, – from a +10% growth rate, on average, for the past few decades, to less than +7% this year. Officially, Beijing set a +7% growth target for 2015, which would mark the slowest expansion in a quarter of a century, if it came to pass. However, on March 15th, China’s Premier Li Keqiang admitted it would be a big challenge to meet that target. Yet in today’s markets, a sharp slowdown in China’s economy, and shrinking company profits, is no reason to sell Chinese equities.

Beijing Shifts to Easier Credit and Liquidity stance; On March 15th, China’s Premier Li Keqiang issued a rare “hot-tip” of advice, saying the ruling Politburo can do much more to allay fears about a stumbling economy. Li assured traders that policymakers would prop up the Chinese stock market, especially if economic growth is at risk of breaching a “lower limit.” “In recent years, we have not taken any strong, short-term stimulus policies, so we can say our room for policy maneuver is relatively big, the tools in our toolbox comparatively many. If the slowdown in growth approaches the lower-limit of a reasonable range, we will stabilize policies in the market, and at the same time, we will increase the intensity of targeted policy control,” Li said. Traders interpreted these remarks to mean that further cuts in interest rates and bank reserve requirements would be on their way in 2015.

“China needs to be on alert for deflation,” PBoC chief Zhou Xiaochuan warned on March 30th, adding the central bank was also on the watch for deflation around the world, and falling commodity prices. “China’s inflation is declining. We need to be vigilant to see if this trend continues, and if it will lead to deflation.” On Feb 28th, the PBoC lowered its 1-year loan rate -25-basis-points to 5.35%, – its second rate cut in just over three months. The PBoC also made a system-wide -50-bps cut to bank reserve requirements to 19.5%, the first time it has done so in over two years, to unleash a fresh flood of liquidity to fight off economic slowdown and deflation. The reduction of -50-basis points can free up 600-billion yuan ($96-billion) or more held in reserve at Chinese banks – which could then mushroom into 2-to-3-trillion yuan of added liquidity floating in the economy due to the multiplying effect of bank loans.

On March 30th, the PBoC took additional measures to boost the local economy, it lowered the amount of money needed for a down payment to buy a house to 40%. The PBoC said on its website that all banks “are encouraged to offer commercial support to families to buy their own home with the down payment not lower than 40%.” All these measures – unleashed by the PBoC – helped to power Chinese stock indexes to a seven-year high. Real estate stocks included in the Shanghai composite property sub-index closed at all-time highs, even after Chinese property sales in the first two months of 2015 plunged -16% against January-February last year, amid a glut of housing supply. In other words, bad news on the economy is good news for stocks, if its leads to fresh liquidity injections.

Just how high can Chinese Red-chip stocks fly? It’s not wise to stand in front of a raging Bull in a China shop. But if history is any guide to the future, Shanghai A-shares did soar to a +95% premium over H-shares at the peak of the Chinese stock market rally in Oct-2007, before succumbing to the PBoC’s tightening of its monetary policy. This time around, Shanghai red-chips are +32% above H-shares, on average, and have the wind of PBoC easing at its back, so it wouldn’t be surprising to see the China-300 index climb above the 5,000-level in the year ahead, up from around 4,125 today

About Gary Dorsch

Mr Dorsch worked on the trading floor of the Chicago Mercantile Exchange for nine years as the chief Financial Futures Analyst for three clearing firms, Oppenheimer Rouse Futures Inc, GH Miller and Company, and a commodity fund at the LNS Financial Group.

As a transactional broker for Charles Schwab’s Global Investment Services department, Mr Dorsch handled thousands of customer trades in 45 stock exchanges around the world, including Australia, Canada, Japan, Hong Kong, the Euro zone, London, Toronto, South Africa, Mexico, and New Zealand, and Canadian oil trusts, ADR’s and Exchange Traded Funds.

He wrote a weekly newsletter from 2000 thru September 2005 called, “Foreign Currency Trends” for Charles Schwab’s Global Investment department, featuring inter-market technical analysis, to understand the dynamic inter-relationships between the foreign exchange, global bond and stock markets, and key industrial commodities.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair