Timing & trends

A boom for American defense contractors:

“As the Middle East descends into proxy wars, sectarian conflicts and battles against terrorist networks, countries in the region that have stockpiled American military hardware are now actually using it and wanting more.”

“Saudi Arabia spent more than $80 billion on weaponry last year — the most ever, and more than either France or Britain”

“Qatar, another gulf country with bulging coffers and a desire to assert its influence around the Middle East, is on a shopping spree.”

Dow Jones US Aerospace & Defense Index

….read the whole riveting article HERE

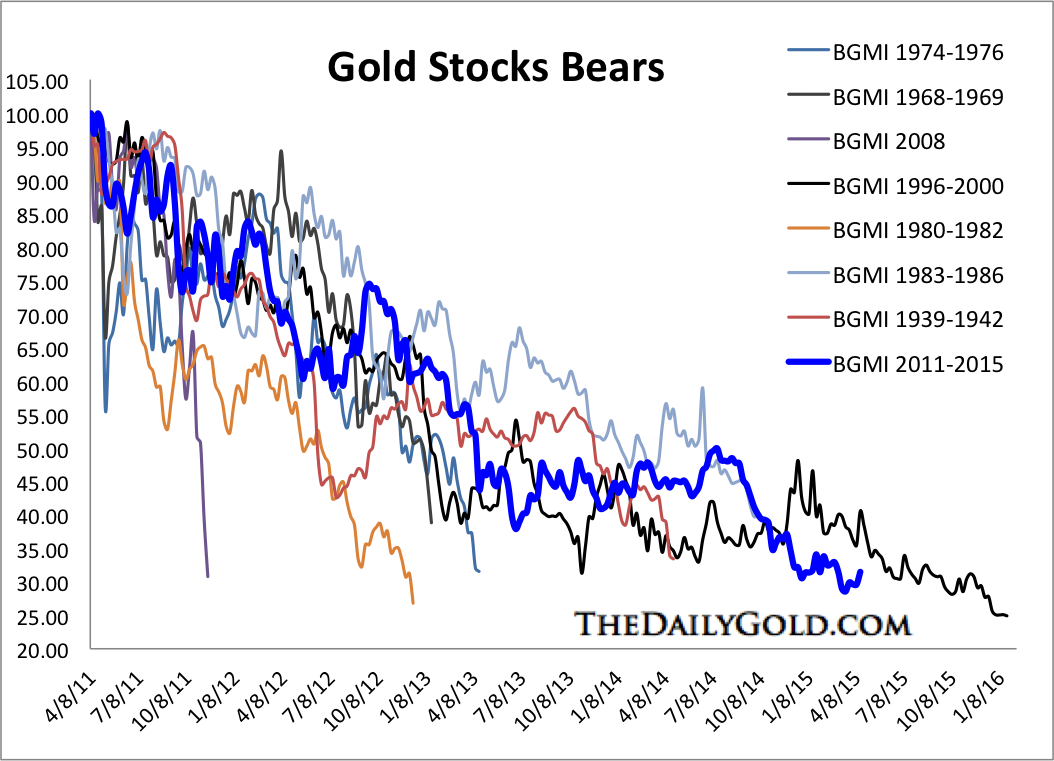

Everyone knows that this has been a devastating bear market for the gold mining sector. If you have followed our work you know that it is the second worst cyclical bear market in at least 80 years. Obviously, gold mining stocks have been crushed. Then they became cheaper, then cheaper and then really cheap. Yet, we may not realize just how cheap this sector has become both in nominal and relative terms.

Below we plot the Barron’s Gold Mining Index (BGMI) against Gold. The BGMI dates back to 1938. The ratio recently touched its lowest level in at least 77 years! There might not be anyone alive today who has seen gold stocks this cheap relative to Gold.

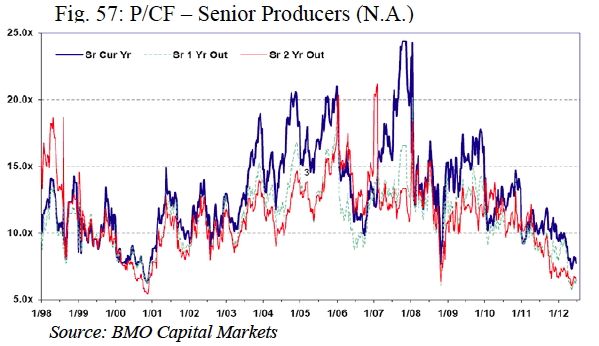

The next chart plots the price to cash flow valuation for senior gold miners. Twice in the past two years it touched a low of about 5. According to data from BMO, this is even lower than during the secular bottom of 2000 when senior miners traded at 6x-7x cash flow.

Gold stocks are also historically cheap relative to book value. A year or so ago I posted a chart from Datastream, a product of Thomson Reuters that showed gold stocks trading at their lowest book value since at least 1980. You can view that here. Here is another chart which shows the price to book ratio for the 10 largest miners. It is unsourced but shows price to book value at the lowest levels since at least 1993.

These spectacularly low valuations have resulted from arguably the second worst bear market ever. The updated bear analog chart is below.

{kind=link}

{kind=link}

{kind=link}

Could gold mining stocks get even cheaper in the weeks or months ahead? It is certainly possible, but only in the scenario of Gold trading to new lows. Even in that scenario, there is no guarantee that the various gold miner indices will make new lows.

While we lack data that precedes 1980, my guess is gold mining stocks relative to cash flow and book value are trading at valuations not seen since 1960 (a secular bottom) or even earlier. In the year 2000 the gold stocks were at the end of their worst cyclical bear market in history (and worst secular bear) and were trading at a 24-year low! Valuations recently surpassed (to the downside) where they were at that epic low.

In any event, the gold mining sector is primed for what should be a spectacular recovery. A big rise in margins/earnings and valuations is the one two punch that causes markets to rally substantially following a major bottom. Margins are starting to recover as evidenced by Newmont Mining’s earnings report. Miners have worked to cut costs and are now getting a boost from lower energy prices and weak local currencies. The only thing left is for metals prices to turnaround. Consider learning more about our premium service including our current favorite junior miners which we expect to outperform in the second half of 2015.

Jordan Roy-Byrne, CMT

Today the man who remarkably predicted the collapse of the euro against the Swiss franc warned King World News that the world is in for another major surprise.

Today the man who remarkably predicted the collapse of the euro against the Swiss franc warned King World News that the world is in for another major surprise.

Egon von Greyerz: “There is clearly apathy in the gold market now. Gold has essentially gone sideways for the last couple of years. Gold was at these levels in June of 2013. So for two years gold has been trading sideways with some volatility….

Continue reading the Egon von Greyerz interview HERE

to achieve superior results is harder than it looks.” – Benjamin Graham

After 15 years, it finally happened. On Thursday, the Nasdaq Composite closed at an all-time high. The index finished the day at 5,056.06. That’s 0.15% higher than the previous all-time high of 5,048.62, which came on March 10, 2000. Back then, the Nasdaq was going for 190 times earnings. Now it’s going for 30 times earnings.

Also on Thursday, the S&P 500 briefly touched a new all-time intra-day high of 2,120.49. But the S&P 500 couldn’t hold on. In the last 40 minutes of trading, the index pulled back to close at 2,112.93. It’s now been 37 days since the S&P 500 made a new high. That’s the longest “new high” drought in nearly two years.

This issue will be all about earnings. Due to the strong dollar, Wall Street analysts slashed their earnings estimates going into this earnings season. The good news is that the impact isn’t as bad as feared. So far, 76% of companies that have reported earnings have beaten expectations. Imagine a high jumper lowering the bar to one foot off the ground, then stepping over the bar and expecting raucous applause. That’s sort of where we are.

I’m happy to report that the earnings reports for our Buy List have been quite good. All nine of Buy List stocks have beaten Wall Street’s earnings estimates. Some like Signature Bank (SBNY) and eBay (EBAY) gapped up on the news. In this week’s CWS Market Review, I’ll run down all of our recent earnings reports. I’m raising Buy Below prices for five of our stocks. I’ll also highlight four more earnings reports we have coming next week.

Eight Buy List Earnings Reports

On Tuesday morning, Signature Bank (SBNY) reported Q1 earnings of $1.64 per share. That’s a very impressive number, five cents more than Wall Street had been expecting. Traders loved the news. Shares SBNY spiked 6% in Tuesday’s trading, and hit a new all-time high on Wednesday.

I like this bank a lot. Signature’s CEO, Joseph J. DePaolo, said, “2015 is off to an outstanding start as we again set records in both earnings and loan growth while also delivering very strong deposit growth.” Deposit growth is up 31.2% in the last year.

Signature is a great little bank that’s not so little anymore. Thanks to the excellent earnings report, I’m raising my Buy Below on Signature by $7. Signature Bank is a buy up to $140 per share.

Last week, I told you that I thought Stryker (SYK) was being conservative with its guidance, and I expected a modest earnings beat. That’s exactly what happened. On Tuesday, Stryker reported earnings of $1.11 per share. That beat estimates by three cents per share.

The orthopedic company also raised the low end of its full-year forecast by five cents. Stryker now expects full-year earnings to range between $4.95 and $5.10 per share.

“We are pleased with our first quarter results, with another strong quarter of nearly 6% organic sales growth and disciplined expense management,” said Kevin A. Lobo, Chairman and Chief Executive Officer. “We expect this momentum, which is balanced across segments and regions, to continue and are raising the low end of full-year sales and earnings guidance.”

I suspect that more Baby Boomers are gradually falling apart, blowing out their knees and hips, so that’s good news for us. For this year, Stryker said they expect constant-currency sales growth of 6% to 7%. They see Q2 earnings coming in between $1.15 and $1.20 per share. That’s in line with Wall Street’s consensus of $1.17 per share, but I expect the consensus will creep higher. Stryker should have little trouble hitting $5 per share this year.

Shares of SYK jumped nearly 2% on Wednesday and kept rallying into Thursday as well. The stock has gained exactly $5 total in the last five sessions, and it appears to have broken out of its trading range. I’m going to bump up my Buy Below price, but I’m keeping it fairly tight. Stryker is now a buy up to $101 per share.

Wabtec (WAB) did our favorite two-step, “the beat-and-raise shuffle.” On Wednesday, the company reported Q1 earnings of 99 cents per share, which was four cents better than estimates. The company also raised its full-year guidance from $4.05 to $4.10 per share.

Raymond T. Betler, Wabtec’s president and chief executive officer, said: “With a strong first quarter, we’re off to a good start for the year. We will continue to face challenges during the year, including global economic uncertainty and foreign currency-exchange headwinds, but we expect to benefit from our strong backlog, and from ongoing investment in freight-rail and passenger-transit projects around the world. We’re also pleased with our long-term growth prospects, which are driven by our diversified business model, balanced strategies and rigorous application of the Wabtec Performance System.”

In last week’s issue, I said a strong earnings report could push WAB over $100 per share, and that’s what happened. WAB even broke $105 before coming back down to $98.27 per share at Thursday’s close. This has been our second-best performing stock YTD. I’m raising my Buy Below on Wabtec to $103 per share.

Now for Qualcomm (QCOM), our most troublesome stock. On Wednesday, the company had another solid earnings report, but guidance was lousy. For the March quarter, which is the company’s fiscal Q2, Qualcomm earned $1.40 per share. That was seven cents better than expectations. Quarterly revenue came in at $6.89 billion, which was better than the Street’s expectations of $6.83 billion.

The problem was guidance. Wall Street had been expecting earnings of $1.14 per share on revenue of $6.5 billion. Not even close. Qualcomm said fiscal Q3 earnings should range between 85 cents and $1 per share, while revenue should range between $5.4 billion and $6.2 billion. That’s a big miss.

The good news for Qualcomm is that the issue with the Chinese government is now behind them. But they may have more investigations to face in the United States and in South Korea. Qualcomm is also dealing with increasing pressure as companies like Samsung and Apple make their own chips for their devices.

Qualcomm is our worst performer of the year (-8.1%). I think the activist pressure from Jana Partners is making an impact. The stock dropped on Thursday, but by less than 1%. Don’t give up on Qualcomm. There’s a lot of potential here. I’m keeping my Buy Below at $72 per share.

In last week’s CWS Market Review, I wrote:

Shares of eBay (EBAY) have been weak recently, and I think they’re a good value here. The online auction house gave weak guidance for Q1: 66 to 71 cents per share. I think that’s too low, and I expect a solid earnings beat.

Sometimes my own brilliance surprises even me. For Q1, eBay earned 77 cents per share, which topped estimates by seven cents per share. The stock jumped 3.8% on Thursday.

Unfortunately, this call wasn’t due to my brilliance. It’s been pretty obvious how well eBay’s business has been going.

“We had a strong first quarter, with eBay and PayPal off to a good start for the full year,” said eBay Inc. President and CEO John Donahoe. “I feel very good about the performance of our teams at eBay and PayPal. Each business is executing well with greater focus and operating discipline as we prepare to separate eBay and PayPal into independent publicly traded companies. We are moving forward with clarity and speed, with a smooth separation expected in the third quarter. We are deeply committed to setting up eBay and PayPal to succeed and to deliver sustainable value to our shareholders.”

Now for guidance. For Q2, eBay sees earnings ranging between 71 and 73 cents per share. For the whole year, they forecast earnings between $3.05 and $3.15 per share. Those are good numbers and very doable. I’m raising my Buy Below on eBay to $62 per share.

On Thursday morning, Snap-on (SNA) reported Q1 earnings of $1.87 per share. That was five cents better than estimates. Revenues rose 5.1% to $827.8 million, which was below consensus of $834.42 million. Despite that, I was particularly impressed with their organic sales growth of 10%. That’s very good, especially for a tool company.

Nick Pinchuk, Snap-on’s chairman and CEO, said, “We believe these results confirm Snap-on’s unique capabilities in providing valued productivity solutions to a growing range of professional customers performing critical tasks in workplaces of consequence. Additionally, we achieved a 120-basis-point improvement in operating margin before financial services, further demonstrating our ability to realize ongoing benefits from our Snap-on Value Creation Processes.“

The shares rose 2.4% on Thursday to reach a new 52-week high. I really like these dull stocks. Snap-on is up more than 520% since the Nasdaq peak 15 years ago. I’m raising my Buy Below on Snap-on to $159 per share.

Three months ago, CR Bard (BCR) said they see Q1 earnings coming in between $2.04 and $2.08 per share. After the bell on Thursday, Bard reported Q1 earnings of $2.10 per share. That topped estimates by three cents per share. Sales rose by 3%, but the number rises to 5% when you exclude the impact of forex. (Side note: Bard reported their earnings on Shakespeare’s birthday.)

Timothy M. Ring, Bard’s chairman and CEO, said, “Our results in the first quarter represented a good start to what is an important year of execution for us, as we once again exceeded our expectations for both sales and earnings per share. In 2015, we expect the returns from our strategic investment plan to begin to contribute to the improved long-term growth profile of the business.”

For Q2, Bard sees earnings ranging between $2.15 and $2.19 per share. Wall Street had been expecting $2.18 per share. The company kept its full-year guidance the same at $8.95 to $9.05 per share. Not much to say here, which is how I like it. CR Bard remains a good buy up to $184 per share.

I got another one right with Microsoft (MSFT). Last week, I said “I expect to see an earnings beat here.” Boy did they beat. For the March quarter, their fiscal Q3, Microsoft earned 61 cents per share. That beat estimates by 10 cents per share.

By the way, all investors should reflect on the fact that Microsoft is one of the largest and most-studied companies in the world. Yet the Wall Street consensus missed its profit forecast by 20%.

Quarterly revenue rose 6% to $21.7 billion, $630 million more than expectations. If it hadn’t been for those meddling currency costs, sales would have risen 9%. The details of the report look quite good. Amy Hood, Microsoft’s CFO, summed it up nicely: “We did a little bit better in lots of places.” One area that’s growing exceptionally well is their commercial cloud business. Sales jumped 106% last quarter. But like so many other companies, Microsoft got dinged by the strong dollar.

Shares of Microsoft were up 3.3% in Thursday’s after-hours market. That suggests the stock will open well on Friday. Since I’m writing this to you before Friday’s opening bell, I’m going to keep my Buy Below on Microsoft at $45 per share. But I may raise it soon. Microsoft continues to be an undervalued stock.

Let me again mention Moog’s (MOG-A) earnings report. As much as I like this company, I never know when the Q1 earnings report will come. It’s usually the last Friday in April, but I can’t say for certain. Don’t worry. Whenever the report comes, I’ll have full details on the blog. Wall Street expects earnings of 92 cents per share. Moog is a good, conservative stock.

Four Buy List Earnings Reports Next Week

More earnings reports are coming next week. On Tuesday, three Buy List stocks are due to report.

Shares of AFLAC (AFL) have perked up recently. Last week, the stock briefly pierced $65 per share and hit a new 52-week high. Since the yen has somewhat stabilized at 120, give or take, to the dollar, that bodes well for AFLAC. Roughly speaking, every one yen up in the yen/dollar ratio knocks off two cents per share on AFLAC’s full-year operating earnings. Right now, AFLAC is on track to earn between $5.90 and $6.20 per share. Wall Streets expect Q1 earnings of $1.54 per share.

Three months ago, Express Scripts (ESRX) missed earnings by a penny. Fortunately, they gave pretty good guidance for this year. ESRX expects earnings to range between $5.35 and $5.49 per share. That’s a 10% to 13% increase over last year’s earnings. The stock has been buoyed lately by deals in its sector. I’m always impressed by how steady their earnings growth is.

Ford Motor (F) continues to be one of the cheapest stocks on our Buy List. The shares can’t seem to get any momentum above $16 per share. The story for Ford is simple: The U.S. is doing well, but Europe is not. I won’t venture to guess how much that’s changed in their Q1 report, but the long term looks good for Ford. The automaker has stuck by its 2015 forecast for a pretax profit between $8.5 billion and $9.5 billion. Going by Thursday’s close, Ford yields 3.8%.

Last earnings season, Ball Corp. (BLL) was our big winner. But it wasn’t their earnings report—that was one penny below estimates. Instead, it was Ball’s announcement that they were in talks to buy Rexam. The stock jumped 9% on the news. A few days later, Ball and Rexam made it official as they announced a $6.8 billion merger deal. The stock jumped again, but has since settled in the low 70s.

That’s all for now. More earnings next week. The Federal Reserve also meets on Tuesday and Wednesday. They’ll release their policy statement on Wednesday afternoon. You can expect Wall Streeters to overanalyze every semicolon. On Wednesday morning, the government will release its first estimate for Q1 GDP growth. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Do you believe in God?

Do you believe in God?

Whoa, wait a minute, this is an investment newsletter, right?

Stay with me.

I’m an armchair philosopher, and I’ve always wished I’d had the opportunity to be a philosophy major, because I can navel gaze with the best of them. But since then, I’ve come to know some actual philosophy professors, and as it turns out, they tend to not get along with other philosophy professors, which makes departmental politics a little toxic.

I can’t remember exactly when it was that I learned about Pascal’s Wager. 17th-century French philosopher Blaise Pascal postulated that it is rational behavior to believe in God.

Why believe in something for which there is no evidence? The answer lies in decision theory.

If you believe in God and you’re right, you go to heaven. Let’s call this “infinite gain.”

If you believe in God and you’re wrong, the only thing you lose is whatever time you spent in church and/or money you donated. It’s a finite loss.

If you don’t believe in God and you’re right, there is no God, you get to be smug. That is a finite gain.

If you don’t believe in God and you’re wrong, you go to hell. Let’s call this infinite loss.

Here it is in table format:

I think most people who understand decision theory will recognize this immediately. So yes, it is indeed rational—meaning in our best interest—to believe in God.

As it turns out, Pascal’s Wager is all over the place in markets.

Best example: Japan in 2012.

There’s this new prime minister, Abe, and this new Bank of Japan governor, Kuroda. They’re going to do this thing called Abenomics. They say they want to print trillions of yen to buy all kinds of assets, which is going to reflate the markets and devalue the currency.

Now ever since the crash of the early 1990s, Japan has had numerous plans to get out of deflation. Japan being Japan, not much changes there, and they end up just getting bogged down in bureaucracy. This has happened at least a dozen times in the last 20 years. So why believe them this time?

Table again:

Boy, did some people have to learn this the hard way. For the record, I’m still long the WisdomTree Japan Hedged Equity Fund (DXJ) and short the yen (JPY) 2.5 years later. I’m still in the trade because it’s the only trade in the markets that literally has infinite upside.

The people who were yelling at me that Japan was going to zero have a lot in common with the very vocal atheists you see on Facebook. They have an overwhelming desire to be right all the time. I don’t care if I’m right—I just want to make money!

The Nikkei went from 40,000 to 8,000. If it goes from 8,000 to 7,000, I make 12.5%. If it goes from 8,000 to 20,000 (which it just did), that’s a 150% gain. But some people like to say, “I told you so.” It’s worth more to them than money.

I will also point out that if you’re short, the most you can make is 100%, but if you’re long, there’s no limit to how much you can make. It’s hard work being a short investor. I wouldn’t run a dedicated short fund no matter how much you paid me. I’d rather pump gas.

Belief and the Black Box

I don’t think anybody really understands China. I think even the people who say they understand China don’t understand China.

How can you understand China? It’s a black box spitting out bogus economic statistics. 7% GDP? We all know they were in recession.

Two things you need to know about China:

- They are very capitalist. Way more than us. It’s the new land of opportunity. There are surveys showing this.

- They really want someone to organize society. The Chinese people just aren’t into spontaneous order.

This is a new thing in the 21st century. We’re learning that it’s possible to be capitalist in the context of a command-and-control government.

Now, as recently as 2008, I believed this would never work. Capitalism, I thought, was incompatible with planning. The Chinese went and borrowed a ton of money to build ghost cities they plan to move 300 million people into. If we tried this here in America, it would be a disaster. We can’t even build a subway line on Second Avenue.

So back in March 2013, that 60 Minutes piece on China’s ghost cities got investors really nervous—and ever since then, people have been waiting for the debt bomb to blow up.

But as I said, it’s a black box.

Everyone knows what happened next: the fake economic data started getting worse, commodities markets crashed, and people were speculating that China pulled forward demand for things like steel and iron ore 50 years.

But then, abruptly:

The market went up 20% in a matter of weeks. And then, in unison, the financial media said: It’s a bubble!

I found that odd. Usually when something goes up 20%, it’s not a bubble, especially in the context of the longer-term chart.

So remember, nobody understands China. It’s a black box. There’s no way to tell if it’s a bubble or not.

Pascal’s Wager again:

Needless to say, I’m long China A-shares, through the Market Vectors ChinaAMC A-Share ETF (PEK).

In general, there is more money to be made believing in things than not believing in things.

But aren’t we taught to be skeptical? What about Enron? Or Lehman?

There’s a time for that too, but trades like that always seem to happen in bear markets (because in bull markets, nobody asks the hard questions). So it’s situational.

I hate China. Absolutely hate it. I think it’s smoke and mirrors. It’s all going to blow up someday. But I look at the chart, and I change my mind.

China is fixed.

They’re going to pull it off.

Bull market again.

I love China.

I will believe pretty much whatever you want me to believe as long as I think I can make money off it.

Jared Dillian

Editor, The 10th Man![]()

Jared’s premium investment service, Bull’s Eye Investor, is available now. Click here for our introductory offer. For Jared, no asset class or type of investment is off limits. From an iconic sports outfitter to a particularly liquid frontier-market ETF—Jared picks the best vehicles for his subscribers to profit from tomorrow’s trends today. Put Jared’s ingenious mix of market analysis and trader’s intuition to work in your portfolio today. Follow Jared on Twitter at @dailydirtnap.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair