Bonds & Interest Rates

The Federal Reserve bank and its owners, the largest banks on Wall Street, want badly to be able to charge you interest for the privilege of depositing your funds. The problem is getting you to stand for it.

The Federal Reserve bank and its owners, the largest banks on Wall Street, want badly to be able to charge you interest for the privilege of depositing your funds. The problem is getting you to stand for it.

Depositors already complain vigorously about zero percent returns on checking and savings accounts. If they must start actually paying the bank to hold funds on deposit, many will opt to simply withdraw the cash and stuff it under their mattress or into a safe deposit box. That simply won’t do.

The Goal Is to Force You to Deposit Cash and Charge YOU Interest

Bankers in the U.S. can learn something from the Swiss. The Swiss National Bank recently implemented negative interest rates without first solving the “problem” of how to prevent cash from fleeing the banks. Predictably, depositors started doing some math.

In one example, a sizable Swiss pension fund, calculated it would save 25,000 francs for every 10 million it held in the bank by simply withdrawing those millions and taking the bales of paper francs to be kept in a vault. The vault storage fees are less expensive than the negative interest rate.

Jumping the gun on the implementation of negative rates put the Swiss banks in an awkward situation. Like all fractional reserve lenders, they don’t have anywhere near enough cash to make good on the withdrawals that may be coming. The bank holding the pension money had little choice but to refuse the client’s demand for millions of francs – funds the client is contractually entitled to. Telling clients “sorry, you can’t make a withdrawal” never goes over too well!

Nevertheless, the Swiss National Bank is sticking to its guns. It is encouraging retail banks to be “restrictive” with regards to cash withdrawals. And it is berating actors such as the pension fund for trying to circumvent negative interest rates. Apparently no one should be questioning the wisdom behind the policy! But the bluster isn’t hiding the fact that bankers stand upon shaky legal ground. The potential for a run on the banks remains.

Insiders here look anxious to avoid a similar situation. Willem Buiter, the chief economist at CitiBank, thinks he’s got the answer to this banker’s quandary. Simply abolish cash. Or tax it punitively. He isn’t the only one supporting this radical solution. Other economists, including the prominent Harvard professor Kenneth Rogoff, also think banning cash is a grand idea.

If depositors’ response to negative interest rates is predictable, so is the reaction from central planners. Effective herding is all about limiting the escape routes for members of the herd.

Eliminating physical cash may well be a longer-term project, but it is not something the Fed can likely implement any time soon. In the meantime, there are other ways to prevent depositors from making their escape.

For starters, officials can criminalize the use of cash above certain amounts.

Banks can also implement new policies of their own. Joseph Salerno from the Mises Institute discovered JPMorgan Chase leading the way. The bank very recently began test driving new rules in Cleveland as well as other markets. The bank will no longer accept cash from customers who want to use it to make mortgage payments, pay credit card balances or to cover their automobile loan.

No Cash or Bullion Allowed in Safe Deposit Boxes

No Cash or Bullion Allowed in Safe Deposit Boxes

Chase also rolled out new restrictions on what can be put into safe deposit boxes. The “Updated Safe Deposit Box Lease Agreement” customers must sign states, “You agree not to store any cash or coins other than those found to have a collectible value.”

Expect other banks to follow suit shortly. The new rules go on top of decades of inflationary monetary policy, making paper currencies worth perpetually less over time. Clearly bankers are plumbing customers’ tolerance for pain.

More and more people will be looking for ways to make it stop. This is where things promise to get interesting for gold and silver investors.

Financial repression, the attempt to force citizens to accept the government shears, has long been a driver of demand for physical precious metals. This demand will accelerate as measures become more draconian. Some bank customers, perhaps even the Swiss pension fund mentioned above, will decide that bullion is a better option than sitting on bales of depreciating paper currency or paying banks to hold deposits.

Here in the U.S., the banks are central to just about all bureaucratic efforts at control. Look for droves of people to try and sidestep the banks and the dollar itself. The next decade or two is almost certain to see rapid innovation in alternative ways to store value and transact. Ways that preserve privacy and are beyond the reach of bureaucrats. As these new systems seek to gain trust and acceptance, precious metals are almost certain to play a much bigger role.

###

Clint Siegner is a Director at Money Metals Exchange, the national precious metals company named 2015 “Dealer of the Year” in the United States by an independent global ratings group. A graduate of Linfield College in Oregon, Siegner puts his experience in business management along with his passion for personal liberty, limited government, and honest money into the development of Money Metals’ brand and reach.

Clint Siegner is a Director at Money Metals Exchange, the national precious metals company named 2015 “Dealer of the Year” in the United States by an independent global ratings group. A graduate of Linfield College in Oregon, Siegner puts his experience in business management along with his passion for personal liberty, limited government, and honest money into the development of Money Metals’ brand and reach.

There are three financial hurricanes hurtling towards our country and most people are oblivious to the coming catastrophe. The time to prepare is now, not when the hurricane warnings are issued.

There are three financial hurricanes hurtling towards our country and most people are oblivious to the coming catastrophe. The time to prepare is now, not when the hurricane warnings are issued.

Hussman makes his usual solid case that stocks and bonds are as overvalued as they have ever been in the history of investing. People are under the false impression that bonds are always a safe investment. The fact that you are already getting a negative real return on bonds doesn’t seem to compute with math challenged Americans. Over the next ten years you will absolutely lose money in bonds.

Liquidity in both the stock and bond markets is thinning considerably. In bonds, quantitative easing by global central banks has resulted in a scarcity of available collateral, a collapse in repo liquidity, and increasing frequency of delivery failures, all of which is shorthand for a bond market that is becoming less liquid and more fragile to any credit event. Meanwhile, risk premiums are minuscule. Avoiding a negative total return on 10-year bonds now requires that interest rates must not rise by even one percentage point over the next three years. Bond yields have historically covered investors against a meaningful change in yields before resulting in negative total returns. On a one-year return horizon, bond yields presently cover investors for a yield change amounting to only about 0.25 standard deviations – matching mid-2012 as the lowest level of yield coverage in history.

The fragility of the economic, financial, and social systems of the U.S. is at extreme levels.

…continue reading HERE

It’s a huge morning for the US economy.

At 8:30 a.m. ET, the Bureau of Economic Analysis will release its first reading on first-quarter gross domestic product, which is expected to show the economy grew at just a 1% pace in the first quarter.

This announcement will be followed at 2 p.m. ET by the Federal Reserve’s latest monetary policy announcement.

In March at its most recent meeting, the Fed said it would not look to raise interest rates at the April meeting.

Moreover, Federal Reserve Chair Janet Yellen will not speak with reporters after the statement is released Wednesday afternoon, and so all the market will have to digest is the statement itself.

But the market will be looking for the Fed’s assessment of one thing in the statement: its outlook for the economy.

In a note to clients over the weekend, Bank of America’s Michael Hanson wrote that the Fed would most likely have a more “somber” outlook on the economy after a first quarter that saw economic data widely disappoint.

Hanson wrote:

At the March FOMC meeting, the Fed took any policy changes in April off the table. We don’t expect similar language about June policy at the April meeting. We do expect a more somber description of recent activity. This dovish shift in the nearterm view should translate into significantly lower odds of a June rate hike in our view. But any market participants who seek an explicit signal that June also is off the table are likely to be disappointed: the FOMC will want to maintain as much policy flexibility as possible.

During the quarter, first-quarter GDP growth was consistently revised down, and some measures like the Atlanta Fed’s GDP tracker indicates the economy may not have grown at all during the first quarter of 2015.

In a note to clients ahead of the GDP report, Joe LaVorgna at Deutsche Bank wrote: “It is possible that GDP growth (specifically productivity) is being understated, because the income side of the economy has not experienced the same degree of weakness evident in the output figures.”

Before the Fed gives its latest statement, however, it will have an answer.

Given that the Fed ruled out a rate hike in April and that Yellen will not speak with the news media after the announcement, markets have more or less been looking past the Fed meeting, or at least expecting to take it in stride with the week’s news flow. Treasury bonds, however, were selling off a bit ahead of Wednesday’s announcement, with the 10-year note rising above 2% for the first time in over a month.

Also, in addition to the big GDP number set for release Wednesday morning, the big data point for Fed policy is probably coming up Thursday with the release of the employment cost index. This report, which captures factors like employee benefits in addition to wages, is expected to show employer costs rose 0.6% in the first quarter, or 2.6% over the prior year.

Anecdotal evidence from the labor market, like the wage increases announced at Wal-Mart and Target in addition to commentary from economic surveys like the Beige Book and Monday’s Dallas Fed report, have hinted that wage pressures might be working their way through the economy. Thursday’s report will be a big test for this growing theme.

In a post ahead of Wednesday’s Fed announcement, Pimco’s Tony Crescenzi wrote that the firm still expected economic conditions would warrant a rate hike in September.

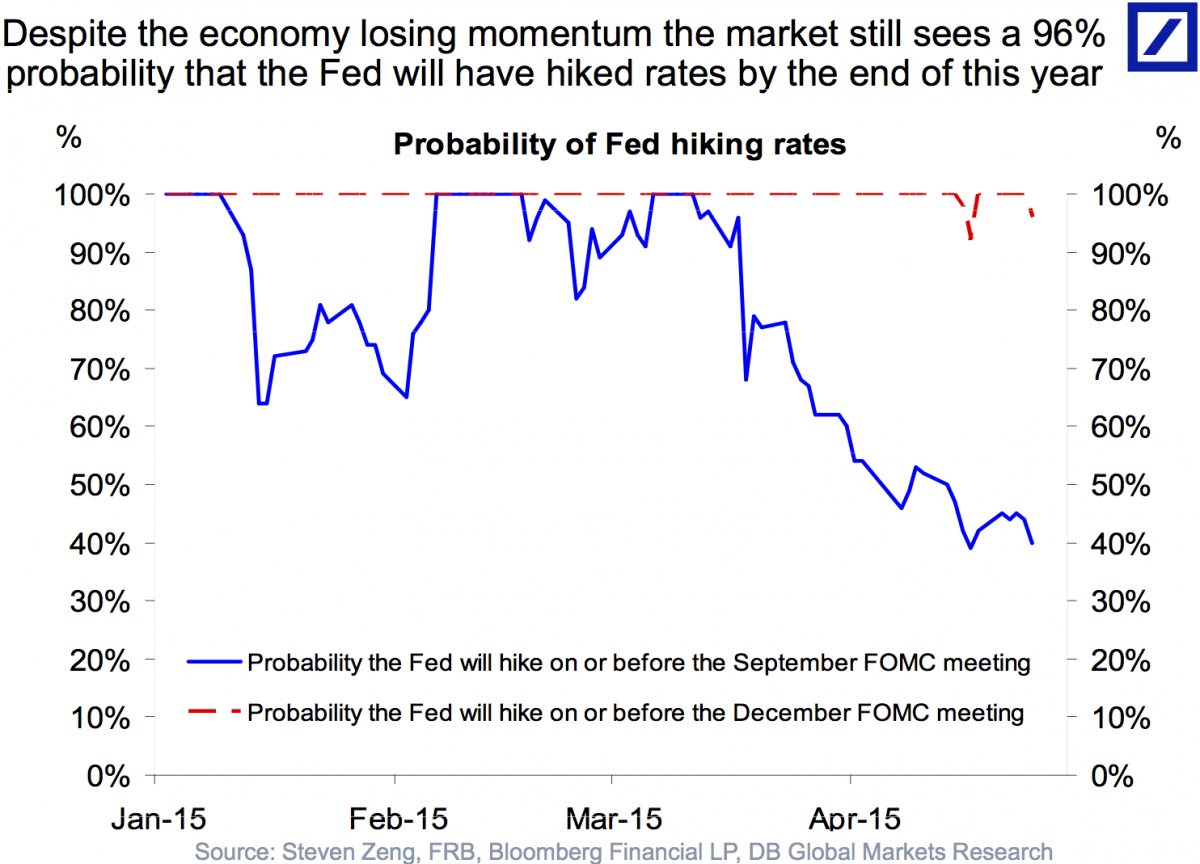

And in a chart circulated earlier this week, Deutsche Bank economist Torsten Sløk said most everyone in the market expected a rate hike by December.

I am not one of those people who believe that if the Fed is dramatically easing, you simply must own equities. I must admit, charts like the one below (source: Bloomberg), showing the S&P versus the monetary base, seem awfully persuasive.

But there are plenty of counter-examples. The easiest one is the 1970s, shown below (source: FRED, Bloomberg). Not only did stocks not rise on the geyser of liquidity – M2 growth averaged 9.6% per annum for the entire decade – but the real value of stocks was utterly crushed as the nominal price barely moved and inflation eroded the value of the currency.

If you do believe that the Fed’s loose reins are the main reason for equities’ great run over the last few years, then you might be concerned that the end of the Fed’s QE could spell trouble for stocks. For the monetary base is flattening out, as it has each of the prior times QE has been stopped (or, as it turns out, paused).

But for you bulls, I have happy news. The monetary base is not the right metric to be watching in this case. Indeed, it isn’t the right metric to be watching in virtually any case. The Fed’s balance sheet and the monetary base both consist significantly of sterile reserves. These reserves affect nothing, except (perhaps) the future money supply. But they affect nothing currently. The vast majority of this monetary base is as inert as if it was actually money sitting in an unopened crate in a bank vault.

What does matter liquidity-wise is transactional balances, such as M2. And as I have long pointed out, the end of QE does nothing to slow the growth of M2. There are plenty of reserves to support continued rapid growth of M2, which is still growing at 6% – roughly where it has been for the last 2.5 years. And those haven’t been a particularly bad couple of years for stocks.

So, if liquidity is the only story that matters, then the picture below of M2 versus stocks (source: Bloomberg) is more soothing to bulls.

Again, I think this is too simplistic. If ample liquidity is good today, why wasn’t it good back in the 1970s? You will say “it isn’t that simple.” And that’s exactly my point. It can’t be as easy as buying stocks because the Fed is adding liquidity. I believe one big difference is the presence of financial media transmitted to the mass affluent, and the fact that there is tremendous confidence in the Fed to arrest downward momentum in securities markets.

What central bankers have done to the general economy has not been successful. But, if you are one of the mass affluent, you may have a view of monetary policy as nearly omnipotent in terms of its effect on securities and on certain real assets such as residential real estate. What is different this time? The cult.

I am no equity bull. But if you are, because of the following wind the Fed has been providing, then the good news is: nothing important has changed.

You can follow me @inflation_guy!

Enduring Investments is a registered investment adviser that specializes in solving inflation-related problems. Fill out the contact form at http://www.EnduringInvestments.com/contact and we will send you our latest Quarterly Inflation Outlook. And if you make sure to put your physical mailing address in the “comment” section of the contact form, we will also send you a copy of Michael Ashton’s book “Maestro, My Ass!”

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair