Timing & trends

Markets have entered a state of flux. Without a doubt, one of the clearest trends in recent times has been the breakdown of the commodities super-cycle and a surging US dollar, a trend that now seems to be reversing. Further, the correlation and patterns witnessed in the markets over the last 9 to 12 months no longer seem to hold. Investors are without a clear safe haven as German Bunds, U.S. Treasuries, and the Dollar remain volatile, and tensions in the Middle East are maintaining a premium in the oil market. More importantly for investors, however, is determining their best guess for what the next action will be from the world’s major central banks, particularly the US Fed.

Markets have entered a state of flux. Without a doubt, one of the clearest trends in recent times has been the breakdown of the commodities super-cycle and a surging US dollar, a trend that now seems to be reversing. Further, the correlation and patterns witnessed in the markets over the last 9 to 12 months no longer seem to hold. Investors are without a clear safe haven as German Bunds, U.S. Treasuries, and the Dollar remain volatile, and tensions in the Middle East are maintaining a premium in the oil market. More importantly for investors, however, is determining their best guess for what the next action will be from the world’s major central banks, particularly the US Fed.

As legendary investor Stanley Druckenmiller recently remarked, you have to “focus on central banks and focus on the movement of liquidity… most people in the market are looking for earnings and conventional measures. It’s liquidity that moves markets.”

Liquidity seems to be the major factor concerning those invested right now. Large gyrations in bond markets and even precious metals have led to some significant moves over the past week with silver rising 6.25 per cent. But it’s the lack of liquidity that can see a wave of trades adjust prices significantly in a matter of minutes. The trend of a strong Dollar that witnessed steady appreciation with confidence the Fed would be first to tighten policy is currently on hold. And it continues to dissipate with the prospects for the US economy, which is looking questionable in the short term.

The probability of a June interest rate hike by the US Federal Reserve is diminishing with economic indicators that continue to show the US economy is failing to recover from the weak first quarter. The soft GDP indicators reported over the last few weeks and the mediocre payroll numbers reported for April have economists delaying their forecasts for when we finally begin to gain traction. As a result, the steam is coming out of one of the strongest US dollar rallies since the financial crisis, and before that, the tech bubble.

Ultimately, it is the lack of confidence south of the border that is affecting the resumption of the US dollar rally. If the economy, as now anticipated, is to pick up steam in the summer months and payrolls continue to advance with a jobless rate nearing 5 per cent, then talks will resume regarding a likely rate hike from the US Fed and the dollar rally can resume. However, if the US economy continues to exhibit mere mediocrity, uncertainty and directionless volatility seem the likely result. If so, this will be a benefactor for the precious metals, particularly with the lack of other safe haven opportunities.

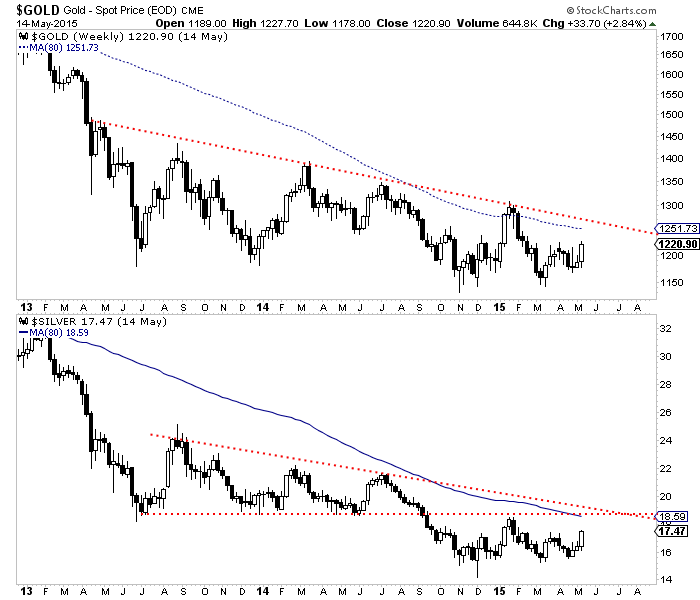

There is some talk among traders about precious metals breaking out. Silver broke a trendline dating back to summer 2011 and will make its highest weekly close in more than three months. Gold will make its highest weekly close in three months and gold miners had a very strong week. However, do these moves really register as breakouts? Not quite yet say the charts.

First lets start with the miners. The weekly candle charts for GDX and GDXJ are shown below along with their 80-week moving averages (in blue) and lateral resistance (in red). For GDX and other indices, the 80-week moving average has perfectly defined bull and bear markets going back five years. If GDX can sustain this strength then it should test the 80-wma in the weeks ahead for the third time in the past 10 months. There is a major confluence of resistance at $22. Meanwhile, GDXJ could rally up to $30 or a bit higher before testing major resistance. Miners have more room to rally but there are no breakouts until they takeout their 80-week moving averages.

GDX & GDXJ Weekly Candles

Meanwhile, both metals had strong weeks and will make their highest weekly close in several months. While Silver broke a downtrend line dating back to 2011, the real resistance figures to be around $19 where there is a confluence of resistance. For Gold, the confluence of resistance is around $1250. Ultimately, it is hard to see any major breakout in the metals until they surpass their January highs on a weekly or monthly basis. That would be a significant breakout.

Gold & Silver Weekly Candles

The gold miners (because they peaked first and are extremely oversold) can certainly diverge and perform okay if the metals don’t breakout. However, we get the sense that they won’t perform really well until the market thinks the metals have bottomed. Note what happened during the 2000 to 2001 bottom. Gold against foreign currencies bottomed first followed by gold miners in Q4 2000. Note that after Gold bottomed at the end of Q1 2001, the miners surged by 60% in two months and took out that pesky 400-day moving average (equal to the 80-wma).

While the immediate outlook looks constructive, the entire complex has a lot of work to do before we can get really excited. The miners could test their 80-week moving averages but it is unlikely they can advance farther unless the metals takeout their January highs. I’m skeptical metals will do that on this rebound as their relative performance is weak considering the big drop in the US$. The worst is likely over for the miners but if Gold can’t reach or takeout its January high then the miners are at risk for remaining in the range they have been in for the past eight months. Until something changes, buying support and oversold conditions works better than chasing strength.

Good Luck!

Jordan Roy-Byrne, CMT

I have been discussing over the last couple of months the potential resolution of the consolidation pattern that has confined the markets to a fairly narrow trading range, to wit:

“Despite the recent weakness seen since the beginning of this year, the market has remained solidly in its uptrend that began in December of 2013. Since that time, the markets have proceeded in one of the longest stretches in history without a 10% correction or more. This is abnormal by any measure and has been a function of investor exuberance and continued hopes of ongoing Central Bank interventions globally.

The daily chart of the S&P 500 below clearly shows that the 150-day moving average has formulated the underlying support of the current bull trend. The break of that support this past October should have culminated in a much bigger decline. However, that V-shaped recovery back into the bull trend, spurred by Federal Reserve member Bullard’s comments and Japan’s expansion of its QE program, kept the overall momentum alive.”

…..read much more HERE

Why are governments rushing to eliminate cash?

During previous recoveries following the recessionary declines, the central banks were able to build up their credibility and ammunition so to speak by raising interest rates during the recovery. This time, ever since we began moving toward Transactional Banking with the repeal of Glass Steagall in 1999, banks have looked at profits rather than their role within the economic landscape.

They shifted to structuring products and no longer was there any relationship with the client. This reduced capital formation for it has been followed by rising unemployment among the youth and/or their inability to find jobs within their fields of study. The VELOCITY of money peaked with our Economic Confidence Model 1998.55 turning point from which we warned of the pending crash in Russia.

The damage inflicted with the collapse of Russia and the implosion of Long-Term Capital Management in the end of 1998, has demonstrated that the VELOCITY of money has continued to decline.

….read more HERE

When we think of investor fraud, many of us will automatically conger images of infamous stories such as Enron and WorldCom. While fraud can be very difficult to identify in foresight, if we adhere to a few fundamental rules, we can substantially reduce our susceptibility to the dangers of financial trickery and mismanagement of fiduciary duty.

When we think of investor fraud, many of us will automatically conger images of infamous stories such as Enron and WorldCom. While fraud can be very difficult to identify in foresight, if we adhere to a few fundamental rules, we can substantially reduce our susceptibility to the dangers of financial trickery and mismanagement of fiduciary duty.

Follow the Cash Flow

We have long been proponents of limiting investments to profitable companies. But when people hear the word profit, they automatically think of net earnings. The problem is that net earnings are an accounting figure

and can be subject to manipulation. Cash flow on the other hand, is less subject to misstatement. Often we will see companies that report a history of net profit on the income statement but routinely fail to generate cash flow on the cash flow statement. A significant and prolonged differential between accounting profit and cash flow is an indication of poor earnings quality. While this does not necessarily indicate outright fraud it should be viewed with skepticism.

Invest In What You Understand

The greatest investor of all time, Mr. Warren Buffett, routinely discusses his adherence to the “simple and understandable business” tenant as fundamental and to his investment strategy. He will not invest in any company that he does not fully understand. At times (notably during the dotcom bubble) he has been criticized for missing opportunities, but in the long run his focused discipline has made fools of his critics. More than just the business, it is also important to understand the financial statements. Highly complex financials with nebulous accounting items make it easier for unscrupulous managers to hide facts or inflate figures.

Don’t Overexposure Yourself to Speculative Regions

In the recent past, we have seen fraudulent activities and scandals uncovered in companies whose base of operations are in emerging markets – notably China. There are two issues at work here. One is that in emerging markets, the regulatory framework and oversight has not had as long to develop as it has in the developed world. Secondly, when a company’s operations are located entirely in emerging market, it makes it more difficult for our regulators to monitor them effectively. We are not trying to say that fraudulent activities are exclusive to emerging markets – they absolutely are not. But we do believe that structurally there is a greater chance that fraud can be developed and concealed at a larger magnitude and longer amount of time in the emerging world. For this reason, we strongly suggest that investors confine the majority of their activities to developed regions.

Read the Footnotes

Many investors, and even analysts, confine their analysis strictly to the financial statements (income statement, balance sheet, and cash flow statement) and ignore the financial footnotes. However, the financial footnotes, which are typically provided after the financial statements, provide a wide range of information and clues about the assumptions and policies used by management (e.g. revenue recognition, depreciation and amortization policy, treatment of derivatives, off balance sheet items, financial covenants, etc). Understanding the information beneath the headline numbers makes those numbers more meaningful and allows the investor to develop a better comparison amongst companies in the same industry. It is also a little known fact that if a management team is trying to hide a piece of information then they will probably put it in the middle or at the end of a long document. Remember… if these notes are impossible to understand then maybe you should question whether or not this is a company you want to invest in.

Diversify your Stock Holdings

For most typical investors, diversification may be the best defense against fraud. The fact of the matter is that fraud does exist in the world of investing and it can be extremely difficult to uncover. By spreading your capital amongst a group of quality companies that adhere to these principles you substantially reduce your susceptibility to both fraud and poor financial performance. This is not to say that we think investors should over diversify into dozens of companies. Such a strategy could make your portfolio unmanageable. But we do strongly suggest that you hold enough companies so that your overall success does not hinge on one or two individual stocks – no matter how good they may look.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair