Gold & Precious Metals

One (perhaps the only) bright spot in the past few years’ gold market has been Chinese and Indian demand for the metal. Here’s a chart, courtesy of Ed Steer’s Gold & Silver Daily, showing that the two countries have imported a cumulative 15,000 tonnes since 2008, which is not far from the total production of the world’s gold mines in that period.

But physical bullion is only part of the story, and may not be the biggest one going…..continue reading HERE

EVERY single long-term market indicator has now broken down and send signals that have ONLY occurred at prior major market peaks.

EVERY single long-term market indicator has now broken down and send signals that have ONLY occurred at prior major market peaks.

However, despite the deterioration in the underlying momentum, asset prices remain near all-time highs as investors remain convinced that Central Banks will continue to “bail them out.”

Furthermore, as I discussed with Evenlyn Chang at CNBC early Friday morning:

“As we have discussed previously, the markets are starved for liquidity. The stronger than expected jobs report, which doesn’t jive with the economic data, paves the way for the Fed to hike rates in June or September.

This is a further restriction in liquidity. Remember, the markets have been rallying on BAD news because it pushes out Fed rate hikes. Good news – is technically bad for stocks at this late stage of the economic and market cycle.”

The unorthodox specificity found in the International Monetary Fund’s latest forecasts for the US economy reintroduces a level of confusion and uncertainty for investors surrounding when the Federal Reserve will raise interest rates. News out of Washington last Thursday threw an absolute curveball at the Fed’s escape plan from zero interest rate policy. As a topic that was previously over-discussed and framed by the financial media, the IMF as the de facto global monetary policy authority has entered the discussion. Previous statements from the US Fed and their Federal Open Market Committee (FOMC) ensured for investors that the data dependency of the US Fed would dictate when we would see higher interest rates. The plea from the IMF Thursday could reshape this debate.

The unorthodox specificity found in the International Monetary Fund’s latest forecasts for the US economy reintroduces a level of confusion and uncertainty for investors surrounding when the Federal Reserve will raise interest rates. News out of Washington last Thursday threw an absolute curveball at the Fed’s escape plan from zero interest rate policy. As a topic that was previously over-discussed and framed by the financial media, the IMF as the de facto global monetary policy authority has entered the discussion. Previous statements from the US Fed and their Federal Open Market Committee (FOMC) ensured for investors that the data dependency of the US Fed would dictate when we would see higher interest rates. The plea from the IMF Thursday could reshape this debate.

Ultimately, the typical investor has to question whether the Fed raising rates in the second half of 2015 or the beginning

of 2016 would really make any material difference. And the assumption is a very likely, no. But it is important to discuss the motivation behind the IMF speaking out in this nature and entering an arena they typically stay absent from, which is imposing their view on US monetary policy. Furthermore, what are the risks they are implying, which really centres on the uncertainties in the global economy at present time?

PIMCO founder Bill Gross made the strongest argument for why the IMF made this recommendation to Chair Yellen and the FOMC. Gross suggests that in a post gold standard world where the US dollar is the world’s reserve currency, the global economy looks to it for stability. Thus, the IMF makes their case to the US Fed to remember to move slowly because as we see liquidity taken away from the global markets, US policy shocks have far reaching effects as witnessed over the last 8 years.

The problem this creates for the US Federal Reserve is their mandate to the US congress is to make policy decisions based on domestic employment and inflation. Global financial stability, which is arguably in their realm of interest, doesn’t dictate when they should raise rates. And as many economists have argued this week, waiting until 2016 with the jobless rate trending lower and expected to be below 5 per cent, is waiting too long to raise rates. As St. Louis Fed President Jim Bullard discussed last week, the Fed will be proactive in raising rates, not reactionary.

One could argue in many instances the Fed’s policy is aligned with the interests of the global economy, but this decoupling notion (of US and global growth) that was introduced in September of last year is once again exhibiting its challenges. If the Fed were to wait, they are giving credence to the IMF’s implied concerns.

It circles back to the earlier question of does it really make a difference when the Fed raises rates? No, not when. It’s clearer, however, a reputable institution doesn’t so much see trouble with when the Fed acts, but the effects of raising rates. It’s a liquidity issue for markets that risk the readjustments, like a 40 basis point swing in US treasuries in a moment’s time which we saw in October, 2014, or the German 10 year bund yield moving from one twentieth of a per cent to eight tenths of a percent in less than week.

The IMF has warned. Now we wait and see.

Back in the early 1960s, then University of Chicago PHD candidate, Eugene Fama published a thesis which was later developed into a theory called the Efficient Market Hypothesis (EMH). This theory gained widespread acceptance in the finance industry (at least among academics) for several decades afterwards and is still commonly referenced to this day. Essentially what Professor Fama was postulating is that stock markets, or most markets for that matter, were efficiently priced at any point in time and that it was inherently impossible to outperform the market on a risk adjusted basis outside of the aid of pure luck, thus making individual stock selection a futile pursuit.

Back in the early 1960s, then University of Chicago PHD candidate, Eugene Fama published a thesis which was later developed into a theory called the Efficient Market Hypothesis (EMH). This theory gained widespread acceptance in the finance industry (at least among academics) for several decades afterwards and is still commonly referenced to this day. Essentially what Professor Fama was postulating is that stock markets, or most markets for that matter, were efficiently priced at any point in time and that it was inherently impossible to outperform the market on a risk adjusted basis outside of the aid of pure luck, thus making individual stock selection a futile pursuit.

Around the 1990s, Fama’s theory started to lose its appeal among the mainstream finance community. Empirical evidence and research did not support the EMH’s conclusion that capital markets were perfectly efficient and select investment strategies, such as buying stocks with low price-to-earnings and cash flow multiples, did demonstrate an ability to outperform the market on a risk-adjusted basis over time. Providing an explanation of the short-comings of the Efficient Market Hypothesis was a relatively new field known as Behavioral Finance. This new field sought to study the emotional traits of investors and the impact they had on investment decisions and market activity. EMH was largely based on the assumption that humans were perfectly rationale beings and that decisions were made instantaneously with full knowledge of all potential outcomes in an unbiased and emotionless process. However, studies in both psychology and finance have demonstrated that this perfectly rationale investor was largely a myth. Human beings in fact rely on emotion to a large extent when making important decisions and are subject to a wide variety of potential biases. An objective of Behavioural Finance is to integrate these real world human biases into modern day financial theory to create a more realistic explanation of how the markets work.

Behavioral finance and psychology have defined numerous biases that can lead to poor investment decisions. We have provided a few examples below.

Bias: Bandwagon Effect

Definition: This occurs when a certain idea, investment type, or investment style starts to become more popular. As popularity increases, more and more people adopt the groupthink mentality and adopt the mentality themselves which further accelerates popularity, and in the case of investing, asset overvaluation.

Example: Alex has been looking at the market for potential investment opportunities. He has noticed that many small-cap tech companies have been doing well. A few of his friends have started to invest heavily in the sector, with good results, but Alex is worried about the high risk nature of the securities. As time passes, more of Alex’s friends have gravitated towards the sector and he is starting to see more portfolio managers and experts talk about it on the financial news. More time passes and the popularity increases. Finally, Alex has grown tired of missing out on the returns and decides to make some significant purchase of these stocks. Unfortunately, the growing popularity of the asset class has pushed valuation far beyond reasonable levels and the sector is now in serious risk of a crash.

Bias: Recallability Trap

Definition: This occurs when an individual’s opinions and decisions are overly influenced by large scale (and often dramatic) events that have taken place in the past.

Example: John receives a call from his financial advisor informing him that he has compiled a report of several successful technology companies that offer strong investment value. All of the companies in the report are profitable, growing, maintain healthy financial positions, and are trading at attractive value. John tells his advisor that he has no interest in receiving the report as he was heavily invested in tech stocks shortly before the market crashed 2001. His opinion is that the sector is far too volatile and he has decided to stay out of it completely. Although John’s decision is understandable, he is now limiting the flexibility of his portfolio based on an irrational bias. The tech market crashed in 2001 because it was substantially overvalued – but that does not mean that current opportunities do not exist in that space.

Bias: Confirmation Bias

Definition: When people have an existing belief, such as an opinion on an individual stock or the movement of the economy, we tend to overweight evidence that supports our original view and underweight, or even disregard, evidence that that conflicts with this view.

Example: Jane recently made a purchase of Company B which is advancing a new technology. She spent a great deal of time reading the company reports and speaking to management. About a week after the initial purchase, she hears an analyst on the news reiterate what the company said about the technology. Pleased to see more people taking notice of the company, Jane increases her position that day. About a week later, she hears another analyst with a respected background in science discuss the technology and conclude that it is not as commercially viable and the company suggests. Although somewhat concerned with the statements, Jane takes no action.

Bias: Anchoring and Adjustment

Definition: Very similar to confirmation bias, anchoring and adjustment is a tendency to not fully reflect and adjust for new information when reviewing an existing opinion or forecast. This is a very common bias in the professional analyst community but can also been seen regularly with retail investors.

Example: Jim owns shares in Company C and believes that the stock price will appreciate from $5.00 to $9.00 in 12 months as a result of increased sales from a new product offered by the company. Company C releases a statement later on indicating that sales of the new product are falling significantly short of initial expectations. Disappointed, Jim decides that the stock is probably only worth $7.00 over the next 12 months and cuts his price expectation by $2.00. Considering the lack of visibility going forward, a large reduction is the price expectation is justified but Jim is still being influenced (he is anchored) to this original target.

Bias: Overconfidence

Definition: This is when investors tend to place too much confidence in their ability to pick stocks or make investment decisions. It is typically the result of a past success, or successes, which may or may not have been the result of luck. Overconfidence can be dangerous because it can cause investors to underestimate risk, under-diversify their portfolio, and even disregard relevant information.

Example: Garth has been a buyer and seller of speculative junior mining stocks for the last several years with mixed success. But recently he bought shares in Company E which made a notable discovery and appreciated in price substantially. Garth also noticed that many of his other junior mining stocks had been doing well over the past year but that his diversified portfolio had underperformed. Garth concluded that his experience in identifying opportunities in the sector had started to pay off. He was also ignoring the fact that many of his stocks were doing well as a result of a generally strong market over that period. The problem was that Garth didn’t buy enough of Company E to really boost his portfolio value. Confident in his abilities, Garth decides that he is going to search hard for another stock like Company E, only this time he plans to concentrate a large portion of this portfolio in the stock so that he can make a huge return.

Bias: Mental Accounting

Definition: This refers to the way that the people have a tendency to mentally compartmentalize their finances and separate capital to psychological accounts.

Example: Taylor is reviewing his finances and deciding how much money he can contribute to his investment account, which is currently worth $20,000 and has been generating a 6% annual return. Taylor also noticed that his credit card balance was a hefty $10,000 on which he is paying 18% interest. Taylor understands the importance of paying down debt as well as saving for retirement so he splits his $5,000 annual contribution 50/50% to debt repayment and investment. While this may seem appropriate, it is actually highly irrational. For this to be a rational decision, Taylor would need to generate a minimum return of 18% in his investment account which is highly unrealistic. Taylor’s investment portfolio would be better long term if he were to use both his annual contribution and his investment portfolio to completely pay down the high interest debt.

Now that we are aware of a few of the common investor biases we can start to evaluate whether or not our own decisions are impacted by irrational tendencies and counterproductive habits. The first step is simply awareness. While it may be asking too much of ourselves to be perfectly rational at all times, simply being aware of the common biases and reviewing our behaviour in that context can be highly beneficial with respect to making better investment decisions in the future.

KeyStone’s Latest Reports Section

5/29/2015

UNDERVALUED SPECIALTY PHARMA MAKES SOLID PRODUCT ACQUISITIONS, MORE-TO-FOLLOW? – MAINTAIN BUY

Money Talks Radio Special Offers – Click read more below for Income Stock and Small-Cap Rate Codes …

…..Read More

by Graham Summers

The War on Cash is now going into hyper-drive.

In the last 24 months, Canada, Cyprus, New Zealand, the US, the UK, and now Germany have all implemented legislation that would allow them to first FREEZE and then SEIZE bank assets during the next crisis.

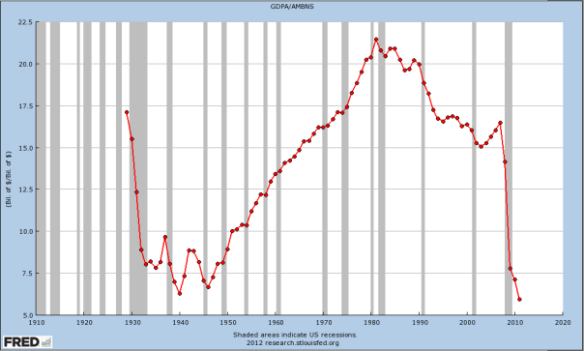

2. VELOCITY of Money Collapses Below Great Depression Levels

2. VELOCITY of Money Collapses Below Great Depression Levelsby Martin Armstrong

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair