Stocks & Equities

Courtesy of Stephen Todd Market Forecast for Thursday July 2, 2015

Available Mon- Friday after 6:00 P.M. Eastern, 3:00 Pacific.

DOW – 28 on flat breadth

NASDAQ COMP – 4 on 750 net declines

SHORT TERM TREND Bullish

INTERMEDIATE TERM TREND Bullish

Special notice. The U.S. markets are closed on Friday for the July 4th holiday. We’ll talk to you on Monday.

STOCKS: The market greeted a slightly worse than expected employment report with an initial surge based on the idea that this would dissuade the Fed from tightening monetary conditions.

Then we seem to have begun to worry about the Greek vote on Sunday. A no vote would probably cause some selling as this would hasten the Greek exit from the EU.

Goldman Sachs didn’t help when they lowered estimates for S&P earnings.

GOLD: Gold lost $3. Gold just keeps inching down, probably on the assumption that the Greeks would vote to stay in the EU.

NEXT DAY: Monday. No prediction. It all hinges on the Greek vote on Sunday.

CHART: Five day RSI has just turned up from an oversold condition. This is normally good for at least a few days on the upside.

BOTTOM LINE: (Trading)

Our intermediate term system is on a buy.

System 7 We are long the SSO from 65.70. Let’s hang in here. We had a tough execution break with the sharp up opening on Wednesday. Hold through Monday.

System 8 We are in cash. Stay there.

GOLD We are in cash. Stay there.

News and fundamentals: Non farm payrolls showed an additional 223,000 jobs added. This was less than the expected 230,000. Jobless claims were 281,000 more than the consensus 270,000. Factory orders dropped 1.0%, The expectation was for a drop of 0.3%. On Monday we get the ISM services index.

Interesting Stuff “I never buy at the bottom and I always sell too soon”. Barron Nathan Rothschild.—— This was suggested by a client. Barron Rothschild was a 19th century investor and heir to a great banking house. Some investing thoughts are very old—and quite valid—-We encourage ideas from subscribers.

TORONTO EXCHANGE: Toronto was up 85.

S&P/TSX VENTURE COMP: The TSX was flat.

BONDS: Bonds had a slight rebound.

THE REST: The dollar pulled back. Silver bounced. Crude oil tried to rally then fell back to close lower.

We’re on a buy for bonds as of June 11.

We’re on a buy for the dollar and a sell for the euro as of June 23.

We’re moving to a sell for gold as of today July 2.

We’re on a sell for silver as of June 23.

We’re on a sell for crude oil as of June 4.

We’re on a sell for the Toronto Stock Exchange as of May 6.

We’re on a sell for the S&P\TSX Venture Fund as of October 30.

We are on a long term buy signal for the markets of the U.S., Canada, Britain, Germany and France.

|

Wed. |

Thu. |

Fri. |

Mon. |

Tue. |

Wed. |

Thu. |

Evaluation |

|

|

Monetary conditions |

+ |

+ |

+ |

+ |

+ |

+ |

+ |

+ |

|

5 day RSI S&P 500 |

48 |

42 |

41 |

18 |

24 |

40 |

40 |

0 |

|

5 day RSI NASDAQ |

55 |

50 |

38 |

17 |

29 |

38 |

37 |

0 |

|

McCl- lAN OSC. |

-7 |

-45 |

-61 |

-178 |

-110 |

-50 |

-36 |

0 |

|

Composite Gauge |

15 |

17 |

12 |

17 |

11 |

9 |

11 |

0 |

|

Comp. Gauge, 5 day m.a. |

10.0 |

12.4 |

12.0 |

13.8 |

14.4 |

13.2 |

12.0 |

0 |

|

CBOE Put Call Ratio |

.88 |

1.08 |

1.06 |

1.40 |

1.12 |

1.13 |

1.02 |

+ |

|

VIX |

13.26 |

14.01 |

14.02 |

18.85 |

18.36 |

16.19 |

16.79 |

0 |

|

VIX % change |

+10 |

+6 |

0 |

+34 |

-3 |

-11 |

+4 |

0 |

|

VIX % change 5 day m.a. |

-1.40 |

+1.6 |

+0.4 |

+9.0 |

+9.4 |

+5.2 |

+4.8 |

0 |

|

Adv – Dec 3 day m.a. |

-39 |

-526 |

-891 |

-1344 |

-832 |

-401 |

+469 |

0 |

|

Supply Demand 5 day m.a. |

.39 |

.24 |

.33 |

.21 |

.18 |

.31 |

.39 |

+ |

|

Trading Index (TRIN) |

1.79 |

1.31 |

.79 |

1.96 |

1.35 |

1.32 |

1.11 |

0 |

|

S&P 500 |

2109 |

2102 |

2102 |

2058 |

2063 |

2077 |

2077 |

Plurality +3 |

INDICATOR PARAMETERS

Monetary conditions (+2 means the Fed is actively dropping rates; +1 means a bias toward easing. 0 means neutral, -1 means a bias toward tightening, -2 means actively raising rates). RSI (30 or below is oversold, 80 or above is overbought). McClellan Oscillator ( minus 100 is oversold. Plus 100 is overbought). Composite Gauge (5 or below is negative, 13 or above is positive). Composite Gauge five day m.a. (8.0 or below is overbought. 13.0 or above is oversold). CBOE Put Call Ratio ( .80 or below is a negative. 1.00 or above is a positive). Volatility Index, VIX (low teens bearish, high twenties bullish), VIX % single day change. + 5 or greater bullish. -5 or less, bearish. VIX % change 5 day m.a. +3.0 or above bullish, -3.0 or below, bearish. Advances minus declines three day m.a.( +500 is bearish. – 500 is bullish). Supply Demand 5 day m.a. (.45 or below is a positive. .80 or above is a negative). Trading Index (TRIN) 1.40 or above bullish. No level for bearish.

No guarantees are made. Traders can and do lose money. The publisher may take positions in recommended securities.

The idea of creating one unified European government to prevent European wars has grown out of a lesson learned from the disaster of World War II and German Nazi dictatorship. The Nazi movement wanted to rule Europe in part as retribution for the oppression of the German people following World War I, with the harsh reparation payments that even Keynes objected. This extraction of wealth opened the door for Adolf Hitler to come to power on the heels of oppressing the German people for the mistakes of their political leaders. Today, Greece faces the same fate.

The idea of creating one unified European government to prevent European wars has grown out of a lesson learned from the disaster of World War II and German Nazi dictatorship. The Nazi movement wanted to rule Europe in part as retribution for the oppression of the German people following World War I, with the harsh reparation payments that even Keynes objected. This extraction of wealth opened the door for Adolf Hitler to come to power on the heels of oppressing the German people for the mistakes of their political leaders. Today, Greece faces the same fate.

The Troika wrongly believes that if they compromise with a left-wing government in Greece, they will encourage such a movement to rise in Portugal and Spain, no less Italy and France. Yet the whole idea of a new European Union with a single currency was indeed the same goal maintained by both Hitler and Napoleon. Political leaders in Europe adopted this idea of one government to eliminate war at the Treaty of Rome to create peace, further democracy, social welfare, economic development, and environmental sustainability. Europe should stand for these common values, but not at the price of economic totalitarianism.

You cannot achieve peace by means of oppression. It was often a common practice to kill the family of one’s political opponent for the offspring might rise to avenge their father’s murder. Oppressing the people of Greece, in the manner that we ground the Germans into the dirt, will lead to civil unrest that will further civil war by rigging the referendum.

Now, the Troika is afraid to compromise and places all the blame entirely upon Greece. The Troika truly despises the new government in Greece for they fear any conciliation will result in encouraging more left-wing political governments who stand-up against austerity in other member states. The Troika has the same goal as Obama did in Russia – oppress the people to force them to overthrow their government. This policy only made Putin stronger. The Troika runs the same risk in Greece by refusing to compromise on anything with the Greek government. The Troika’s plan to overthrow the Greek government may haunt them in the years ahead and spark other nations to rise up as well. This policy of you can check-in, but you can never leave will be exposed for its totalitarian nature and the death of any real democratic foundation in Europe.

There is simply no resolution to the Euro Crisis with the Troika in charge; what info we are getting from behind the curtain shows a dangerous attitude akin to “we do not negotiate with terrorists.” The Troika feels yielding to any opposition will lead to the demise of their euro dream. This economic design of a single currency, leaving nations with their debts intact, is just unsupportable. We are going to see a very serious crack in the political system of Europe over the next four years.

Make no mistake; the European Central Bank (ECB) has decisively been the game changer for how events are unfolding in Greece. The decision by the ECB to limit the emergency liquidity assistance provided to Greek financial institutions prompted the bank closures which if they remain will have devastating and escalating effects on their economy. This is forcing the Greek government to reveal their hand, and their lack of experience in negotiations with the Troika is showing that they are as much concerned with remaining in power as they are with getting a bailout agreement. For a crisis that has been five years in the making, the introduction of capital controls has taken events to the new level.

Make no mistake; the European Central Bank (ECB) has decisively been the game changer for how events are unfolding in Greece. The decision by the ECB to limit the emergency liquidity assistance provided to Greek financial institutions prompted the bank closures which if they remain will have devastating and escalating effects on their economy. This is forcing the Greek government to reveal their hand, and their lack of experience in negotiations with the Troika is showing that they are as much concerned with remaining in power as they are with getting a bailout agreement. For a crisis that has been five years in the making, the introduction of capital controls has taken events to the new level.

Since Prime Minister Alex Tsipras blindsided his creditors last Friday in announcing a referendum on the terms of the proposed bailout, he has looked to avoid the vote he called for on multiple occasions. This is because a “yes” vote would ultimately cost him his job. In pre-empting that Greece would miss the 1.55 billion euro repayment to the IMF, the Greek Prime Minister in disregard to 5 months of discussions proposed terms for a brand new two year bail out agreement. This was quickly discarded by EU members.

Following being the first western nation to miss a payment to the IMF in their 70 year history, Tsipras conceded his demands to the creditors with only slight concessions for a discounted Value Added Tax for the Greek islands (a popular tourist destination) and less stringent pension reforms. Again the creditors didn’t blink. And it’s the leadership of Germany’s Angela Merkel, whether too stubborn or not, that has not shifted from the standpoint that they will await the result of the referendum as quite simply, the deadline was missed and the offer is now off the table.

The Greeks have backed themselves into a corner, and the results will range from financial hardship to devastating. Hardship as the result of continued recession in accepting the creditors demands for reforms to stay in the euro, and the potential devastation of a Greek exit, reintroduction of a new currency, and depreciation and rampant inflation. It currently remains unclear whether there is a third option and where a no vote prompts a new round of bargaining, and what will be the result.

By missing a payment to the IMF, they have technically not “defaulted.” Rating agency Standard and Poor’s justified this by saying the IMF is not a private creditor, thus the missed payment was not a credit altering event. Investors took another view, however, as the market for Two Year Greek Bonds over the past week have seen their yields surge to over 37 per cent. This then leading us to where we are today as the European Central Bank as well conceded they are lending money in what has become too risky of a scenario and limiting the liquidity assistance to Greek banks.

Capital Controls are very rarely removed as quickly as they are implemented. Iceland, hit by the financial crisis in 2008 is finally beginning plans to remove the imposed barriers 7 years later. In very simple terms, by imposing these limits to Greek account holders to withdraw only 60 euros a day, and not permitting transfers to financial institutions outside of Greece, it is an admission by policy makers that there is no longer confidence in their financial system.

There are a number of themes to draw on with the crisis in Greece, but the most astonishing is simply that a westernized economy now joins the ranks of Somalia and Zimbabwe in purposely missing a payment to the International Monetary Fund. Not only does this redraw the potential framework for the international lender of last resort should other economies face financial hardship, but demonstrates the course followed by populism and brinkmanship and the resulting fallout from bad to ugly.

Robert Levy

Border Gold Corp | www.bordergold.com

15234 North Bluff Road, White Rock, BC V4B 3E6

(Tel) 1-604-535-3287

(TF) 1-888-312-2288

(Fax) 1-604-535-3259

American industrialist J. Paul Getty once said: “If you owe the bank $100, that’s your problem. If you owe the bank $100 million, that’s the bank’s problem.”

And when the amount is $1.73 billion, it’s everyone’s problem. Greece is officially in arrears for missing its scheduled payment Tuesday to the International Monetary Fund (IMF). Expecting this, American stocks had their largest one-day drop of 2015 on Monday. Market volatility, as measured by the VIX, spiked sharply.

Investors responded by seeking safe-haven investments such as Treasuries, gold and municipal bonds.

This Sunday, Greece plans to vote on whether to comply with their creditors’ present conditions or to reject the terms, a choice some think could lead to a so-called Grexit from the eurozone. Currently, there’s no such exit clause written into the legal fabric of the currency system other than leaving the entire European Union, an extreme “solution.” No matter how this particular act plays out, there are still more (and even larger) loan payments waiting in the wings, the next one owed to the European Central Bank (ECB) and totaling nearly $4 billion.

German Chancellor Angela Merkel, whose country holds the greatest total amount of Greek debt, officially refused to renegotiate the bailout terms until after the referendum.

In many ways, the unfolding Greek drama is playing out like a sequel to the Cyprus banking crisis two years ago, which also had far-reaching ripple effects in world markets. But the present situation could potentially have much larger ramifications.

How Cyprus Prevented Capital Flight and Saved Its Economy

Cyprus has climbed most of the way out of its financial hole after making bad loans to—wouldn’t you know it?—Greece, following the 2008 crisis. One of the ways the Cypriot government managed to do this was by implementing capital controls. Cyprus imposed restrictions on how many euros could be withdrawn per day or taken out of the country, and ATMs rationed cash.

Similar capital controls are now in place in Greece. Banks are closed until at least next Monday—the day after the referendum—and no more than 60 euros may be withdrawn from ATMs per day, per account. Greeks traveling abroad also face restrictions. Even parents who have children studying abroad will need to apply for permission to send them money. These inconveniences are forcing citizens to realize the possible, and potentially very unpleasant, consequences of a no vote in the upcoming referendum.

Similar capital controls are now in place in Greece. Banks are closed until at least next Monday—the day after the referendum—and no more than 60 euros may be withdrawn from ATMs per day, per account. Greeks traveling abroad also face restrictions. Even parents who have children studying abroad will need to apply for permission to send them money. These inconveniences are forcing citizens to realize the possible, and potentially very unpleasant, consequences of a no vote in the upcoming referendum.

One opinion poll right now shows that a slim majority of Greek respondents are in favor of working out a deal with the IMF and other lenders. Former Cypriot Minister of Finance Michael Sarris—who’s had plenty of experience with debt negotiations—agrees. He urges Greece to vote yes, stating that to do so “takes [them] back to the negotiating table with the chance of a better outcome.”

Among the Greek voters, of course, are pensioners and low-income Greeks who receive government benefits. Fed up with austerity, such voters seem much more likely to vote no. But this way of thinking is precisely what landed Greece in its current situation to begin with. For years the country has been financing its ever-expanding budget with loans from European banks and the IMF, with no plan in place on how to repay them. In fact, Greece has spent 90 of the last 192 years in one financial crisis or another, according to Bank of America Merrill Lynch.

For this reason and more, MSCI, global index provider, is seriously considering demoting Greece from the emerging market category to the solitary, windswept “standalone” category, which includes Venezuela, Ghana, Zimbabwe and other outliers.

This past April, Cyprus lifted the last of its capital controls. Although it was a painful process, things are moving in a positive direction. Let’s hope the people of Greece make the right decision so that their country can likewise begin the recovery process.

Greece Unlikely to Leave the Eurozone

Obviously this topic is of interest to our investors, so I’ll be sure to update you on how our investment team is handling the situation. For now, it’s important to know that a Grexit is unlikely to happen. Such a move would be a huge, symbolic blow not only to Greece, one of the earliest members of the fledgling European Community, but also the monetary experiment known as the euro. Even Greek Prime Minister Alexis Tsipras admits that the cost to the EU for kicking Greece out of the eurozone would be too immense.

The uncertainty has sent shockwaves through world markets, prompting investors to seek safety in core investment assets, including municipal bonds.

Soft data and softer oil prices undermine Loonie

USDCAD Canada Day Range 1.2490-1.2595

Overnight Range 1.2565-1.2630

The Loonie got spanked while Canadians got tanked (some of them anyway) and the rest were singing O’ Canada. A perfect storm combining weak GDP data, a resurgent US dollar on interest rate divergence and a steep drop in oil prices caused a stampeded to buy USDCAD. The move was exacerbated by poor liquidity and the break of key resistance levels. Today’s US nonfarm payrolls report was widely expected to come out on the strong side of forecasts due to improvements in the employment components of other data. That didn’t happen and early (and overnight) US dollar gains were quickly erased. US NFP showed a gain of 223K vs forecasts of 233K and 0 for the average hourly earnings s component. The sting of these misses was eased by the drop in the unemployment rate to 5.3% from 5.5% last month. The US dollar is still jockeying for position following the data but once the intraday positioning gets cleaned up, the underlying bullish bias will reassert itself.

Yesterday and overnight, the Loonie wasn’t the only currency to get whacked. All the G-10 currencies suffered the same fate. Soft data from Australia and rate cut fever in New Zealand drove the antipodeans lower. A report that three large Japanese pension funds were shifting their asset allocations to a more aggressive strategy, helped drive USDJPY higher.

The upcoming Greek referendum has pushed the EU/Greece story to the sidelines in FX trading, at least until late Sunday.

USDCAD technical outlook

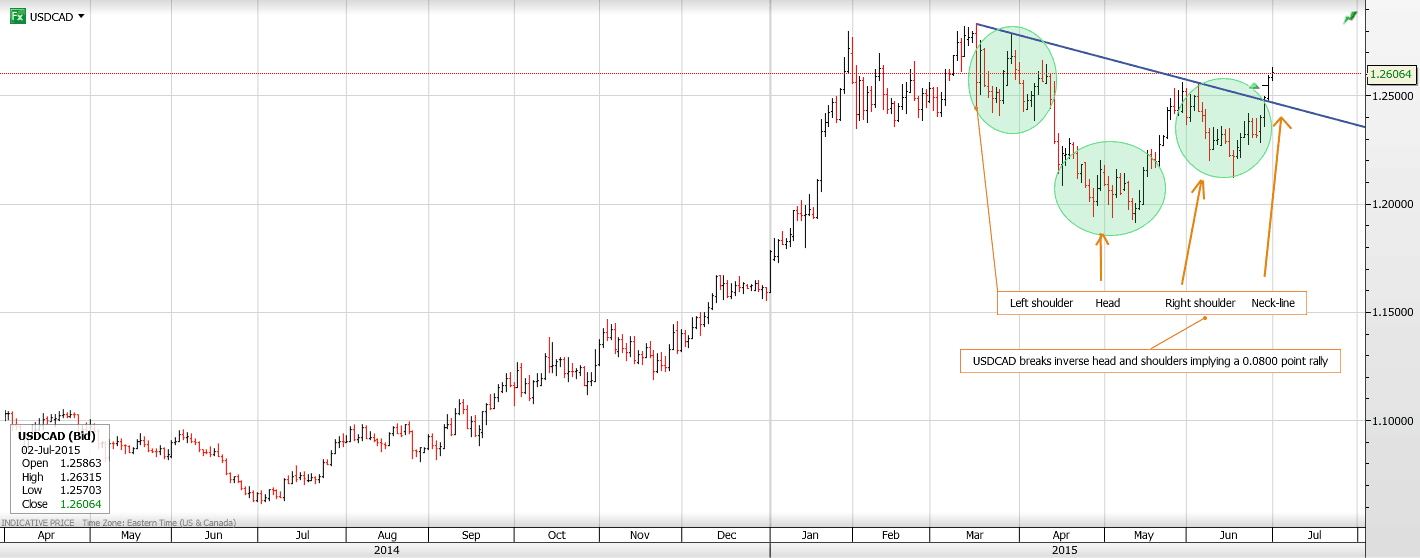

The intraday and short term USDCAD technicals are bullish. The downtrend from the March peak of 1.2820 was snapped with yesterday’s break above resistance in the 1.2490-1.2505 area which was also the neckline of an inverse head and shoulders pattern. This break implies further gains to the 1.3300 area in the medium term.

The intraday USDCAD technicals are bullish while trading above 1.2580, looking for a break of 1.2630 (overnight high) to extend gains to 1.2880 and then 1.2940. A move below 1.2570 would lead to a test of support at 1.2520.

Today’s Range 1.2560-1.2630

Chart: USDCAD daily with neckline break of inverted head and shoulders

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair