Timing & trends

Perspective

The above list chronicles the sudden discovery of a highly speculative blow-off gone suddenly bad. Such headlines could have been recorded in New York in early October 1929 or in 1873. Instead it was recorded in China at the conclusion of a truly magnificent financial mania.

On the way up, the action generated many quotations about the wonders of run-a-way speculation that peaked on June 12th. In a couple of steps the SSEC has plunged more than 30 percent. An index of new issues has crashed.

Although quick, there seems enough pattern to conclude that China’s great bubble has blown out. As with historically great bubbles outside of New York it climaxed in the May-June window.

In the completing frenzy of the Nikkei Bubble at the end of 1989, there were official attempts to talk the speculation down. After some weeks of serious decline, policymakers talked about easing margin requirements. China’s current easing of “lending rules” could be as effective as those offered in Tokyo in early 1990.

The plunge is much faster and steeper than the initial break in 2007. Another case of the “margin calls going out with the confirmations”. Using the pattern that got us this far, once the SSEC stabilizes it could churn around into August. This could lead to heavy liquidation in the fall.

Considering the Greek problem, it seems like another test of policymakers and their peculiar theories. At speculative extremes they never have had any control over credit spreads and the action since May has been a warning. Also at such extremes they have been many months behind the changes in market rates of interest.

Ironically, the chronic application of desperate measures created a bubble which consequent 2 contraction will not be prevented by more of the same desperate measures. This test of policymakers will likely mark their theories and practices as a massive failure.

Even worse, the public will eventually understand the failure as well. More alert politicians will pillory interventionist central bankers upon a cross of gold.

Stock Markets

There is a saying from the old and dreadful Vancouver Stock Exchange. “So long as the stock is going up, the public will believe the most preposterous story.” Once the promotion breaks, the belief is gone.

This also applies to modern central banking. So long as financial markets are rising the public, and particularly Wall Street, will believe in the preposterous story that a committee can manage the economy.

Overly inflated bond markets are deflating and overly inflated equity markets are coming under pressure.

Belief in the supernatural abilities of policymakers will likely be under serious review later in the year.

In the meantime, the venerable Dow Theory seems to have worked, once again. In February, Ross reviewed the theory and noted that the longer the non-confirmation ran, the more serious the sell-off. TRAN set its last high at the end of the year. DJI set its high in May and the non-confirmation high was set on June 22nd.

Commodities (DBC) set their bear market low at 16.71 earlier in the year.The “rotation” made it to 18.68 in May and it is now at 16.72. Under-inflated commodity prices are again deflating.

How much longer can overly-inflated equities remain inflated?

We will stay with the pattern that got us this far. Speculative peaks in May-June (). Speculative hit (). Churning around in the summer (??). And seasonal lows in October- November (??).

Motivated by ambition to save the world, policymakers will be “pulling out all of the stops”. Of course, the metaphor is playing a huge organ at full volume. The irony is that they have been playing at full volume since trouble was discovered at Bear Stearns in early June 2007.

One full business and one full credit cycle ago.

Perhaps many are beginning to realize that policy ambition is now down to just trying to prove that arbitrary intrusion really works.

In the meantime, some timing patterns should be reviewed.

Last week we suggested that NYSE margin debt had spiked on the April number. This week’s turmoil adds to the conclusion and the senior stock indexes usually peak some months later.

Also, Advance/Declines peaked in April and that usually leads the top by a number of months. The decline in the A/D line is now more extensive than the decline into last October.

The European STOXX could not get above the 50-Day and has now taken out the 200- Day, as well as the February low. The high was set in April and Europe often leads the NY high by some months.

On the bigger picture, the possibility of a Rounding Top in 2014 was negated by the Springboard Buy in October. Another Rounding Top pattern has been underway. This shows in the NYSE comp (NYA), which set highs at 11248 in April, at 11254 in May and at 11170 in June. The June rally was turned back by the 50-Day, which was Step One. Step Two was taking out the 200-Day. That was last week, and the bounce failed at the lower moving average.

This looks worse than going into last October.

On the positive side, Biotechs are on a good seasonal period from now and into September.

On the negative side, BKX has taken out the 50-Day. Step One.

Generally, financial conditions are becoming more precarious going into the time of year when seasonals become somewhat positive for NY senior stock indexes.

Commodities

This years “rotation” for commodities worked out reasonably well. Oversold in January turned into enough of an overbought in May to call the end of the rally. The July 1st ChartWorks looked for crude to decline to around 50.

Base metals (GYX) rallied from oversold at 299 in January to overbought at 345 in early May. Now at 280, it has set a new low for the bear that began at 503 in 2011. At 23 on the Daily RSI it is near-term oversold.

Some relief recovery seems possible.

Grains (GKX) were a late bloomer in rallying from 279 in early May to 327 at the end of June. This drove the Daily RSI up to 79, which was near-term overbought. A modest correction is underway.

Essentially the problem in energy and base metals is oversupply. Our work on the rallies in base metals into 2007 was that the advance in the real price of each base metal (deflated by the PPI) was the greatest in one hundred years. This price stayed real high for an unusually long time creating more than adequate capacity.

Then there was the Great Crash and Great Recession. The bull market into 2011 ended with the signal from our Peak Momentum Forecaster.

Much the same holds for crude oil which enjoyed the Middle East risk premium for an overly long time. In the second quarter of last year our view was that the usual post- bubble weakness in most commodities would eventually get crude oil prices. Within this, crude would get in line with the previous slump in natural gas prices to a new low regime.

The story about OPEC driving the global price down in order to curb the advance in US production seems fanciful. Political forces such as OPEC and the Middle East have been overwhelmed by market forces.

Deutsche Bank’s commodity index is representative and under the symbol DBC the price is available during the trading day. The extremely oversold low was 16.84 in January and it became somewhat overbought at 18.68 in May. At 16.95, it is now testing the low. It could take some weeks to take it out.

At the risk of a pun, iron ore also became a late bloomer. The April number was 521 and for May it was 60.23. The June number is 63.

Thermal coal set a high at 54 in March and is now at 40.82. Renewed weakness in industrial commodities does not suggest a firming global economy.

Currencies

On the Daily RSI the DX has had a big swing in momentum from the high of 100.71 in March to the low of 93.15 in the middle of May. The initial bounce made it to 97.88 and the correction test was set at 93.31 in mid-June. At 97 now, rising above 98 would be constructive in resuming the uptrend that started in June a year ago.

At close to neutral momentum now, the breakout could take some weeks.

Overwhelmed by weakening commodities, the Canadian unit has declined from the 83 level in May to the 78 level this week.

There is support at this level and the Daily RSI is down to 29. Some stability seems likely.

Precious Metals

Any port in a storm comes to mind. Meaning a refuge rather than an aged port with a fine Stilton cheese. Perhaps the latter alternative would provide an appropriate haven?

Without a doubt!

As this page has been reviewing, in a financial storm the serious money goes to the most liquid items. Hopefully liquid enough that it provides a place to park funds without pushing the price.

Treasury bills in the senior currency and gold are the best such instruments. Silver is not, even as the “poor man’s” gold.

Tuesday’s action showed, yet again, that when the financial world is suffering forced liquidation silver will plunge relative to gold. Forced liquidation of hitherto highly inflated assets has only just begun.

The important thing lately has been to monitor the gold/silver ratio. In a way, this is the longest-running credit spread in history and when it goes down it signals a financial party.

And when it turns up it says “The party’s over!”.

On this year’s exuberance it declined from 77 in December to 69 in the middle of May. That was from somewhat overbought to somewhat oversold. A few weeks ago we noted that breaking above 75 would mark the change to a rising trend, which would be a warning on potential speculative exhaustion. Rising above 76 would suggest financial pressures were becoming serious.

Yesterday it touched 78, which is the highest it’s been since late 2008. Moreover, in that fateful year the key breakout was accomplished at 57 in early August. The rebound high for the S&P was set in May at 1440.

The breakout in the gold/silver ratio is now a strident warning on most speculations.

Vignette

So, in having lunch with the “Ancient Miner” the other day an interesting story came up. It concluded with the reason to hold gold or gold coins as insurance.

As a young “Geo” in 1963, our story-teller was in Northern Greece evaluating historical mining sites for prospects that could be profitable with modern technology. One became encouraging enough that a “major” gold company optioned the property and as the work expanded “local” help went from a few to many. Over many months.

At the time, there was very little money in the local economy. Folks were spinning their own wool for home-made clothing.

As each new employee began to get his weekly wage in cash there would be a new dress for the wife and a few other essentials. And then the consumer spending would virtually stop. Brad, as we will call our young Geo, became curious and asked about where the money was going.

After gaining the confidence of the head guy, Brad was taken to the closest town and down a narrow street. At a door, the head guy knocked and after assuring the proprietor about Brad’s integrity they were let in. What was not needed after basic expenses was going into gold coins. Essentially British sovereigns, which were being put in a safe place.

As the head man explained “I hope we never need the gold”.

Link to July 10 Bob Hoye interview on TalkDigitalNetwork.com:

http://talkdigitalnetwork.com/2015/07/stock-market-crashes-stoppable/

Iron Ore Spot Price

-

The iron ore price we reviewed above is the monthly price.

-

This is the daily price and the plunge has been rapid.

-

Metals Bulletin noted that the 10.1% drop is the biggest one-day drop on record.

Gold Bumps & Grinds Video Analysis

GDXJ Overwhelms GDX Video Analysis

FXI (China Stock Market ETF) Gigantic Triangle Video Analysis

BitGold Let The Good Times Roll Video Analysis

Key Gold Stocks Price & Volume Video Analysis

Here is a further look at key precious metal sector stocks with important price and volume action:

More Key Junior Metal Stocks Video Analysis

Above are today’s videos and charts (double click to enlarge):

Thanks,

Morris

| Friday, Jul 17, 2015 Super Force Signals special offer for Money Talks Readers: Send an email to trading@superforcesignals.com and I’ll send you 3 of my next Super Force Surge Signals free of charge, as I send them to paid subscribers. Thank you! |

The SuperForce Proprietary SURGE index SIGNALS:

25 Surge Index Buy or 25 Surge Index Sell: Solid Power.

50 Surge Index Buy or 50 Surge Index Sell: Stronger Power.

75 Surge Index Buy or 75 Surge Index Sell: Maximum Power.

100 Surge Index Buy or 100 Surge Index Sell: “Over The Top” Power.

Stay alert for our surge signals, sent by email to subscribers, for both the daily charts on Super Force Signals at www.superforcesignals.com and for the 60 minute charts at www.superforce60.com

About Super Force Signals:

Our Surge Index Signals are created thru our proprietary blend of the highest quality technical analysis and many years of successful business building. We are two business owners with excellent synergy. We understand risk and reward. Our subscribers are generally successfully business owners, people like yourself with speculative funds, looking for serious management of your risk and reward in the market.

Frank Johnson: Executive Editor, Macro Risk Manager.

Morris Hubbartt: Chief Market Analyst, Trading Risk Specialist.

website: www.superforcesignals.com

email: trading@superforcesignals.com

email: trading@superforce60.com

SFS Web Services

1170 Bay Street, Suite #143

Toronto, Ontario, M5S 2B4

Canada

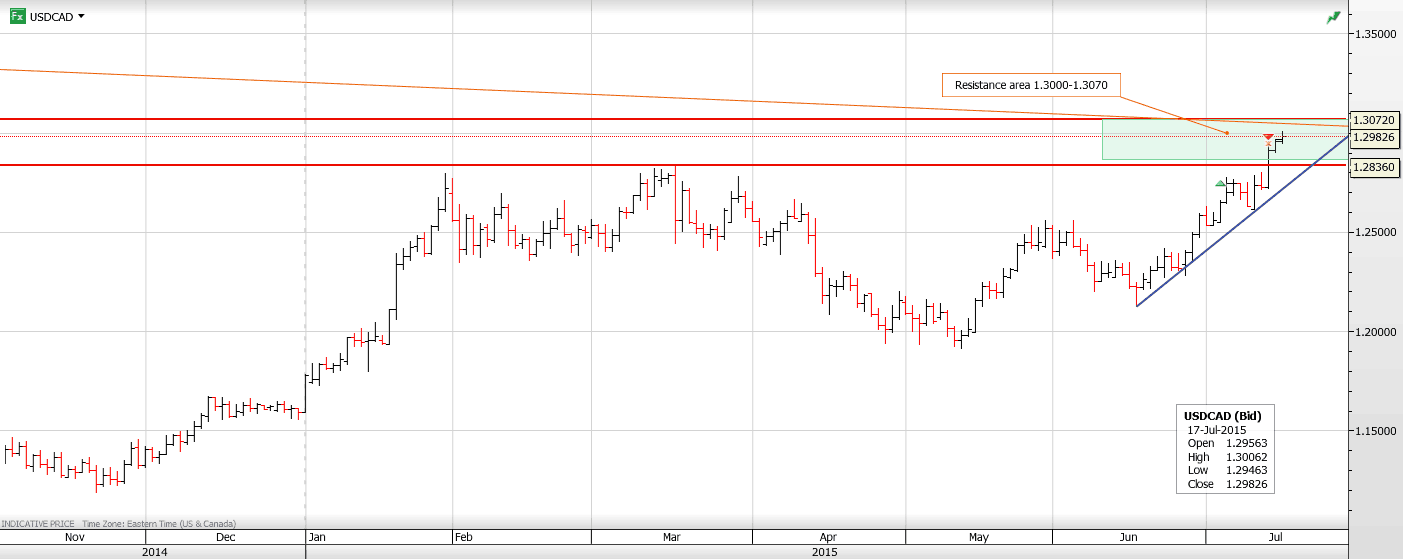

USDCAD Overnight Range 1.2952-1.3005

USDCAD dipped initially on the release of the CPI data (Actual 2.3%, Core 1.0% y/y) which was in-line with forecasts and a tad on the “ok” side. The move was exceedingly brief and within seconds the Loonie was ringing the 1.3000 bell, aided in part by better than expected US housing data. It has since retreated but the dip was shallow.

Overnight trading was subdued. The Loonie drifted quietly in Asia where a number of centers were closed for holidays to celebrate end of Ramadan. The markets weren’t much livelier in Europe, either. It appears that with the curtain coming down on the final act in the Greek/EU drama (or at least for intermission), the signing of a US and friends nuclear deal with Iran and Janet Yellen’s testimony out of the way, traders had nothing to worry about and nothing to do.

In the UK, Mark Carney tried to fill the void. He opened up a can of worms last Tuesday when he started talking about rate hikes. Those remarks were overshadowed by Greece, Iran, Yellen and China so he took another swing of the bat yesterday and hinted a rate hike around the “turn of the year”. This morning, he is tripping over his tongue trying to unsay what he said about the direction and timing of UK interest rate moves.

USDCAD is still bid and it wouldn’t be out of character for this currency pair to make a late day push and close above 1.3000

Technical Outlook

The intraday USDCAD technicals are bullish while trading above 1.2910 with minor support seen at 1.2950 and looking to extend gains to 1.3050. There is a lot of resistance between 1.3000 and 1.3050 dating back to 2008-2009. A move below 1.2950 will meet strong support in the 1.2880-1.2910 area. For today, USDCAD support is at 1.2950, 1.2920 and 1.2890. Resistance is at 1.3005 (intraday high) and 1.3050.

Today’s Range 1.2960-1.3030

Chart: USDCAD daily showing resistance zone above 1.3000 Larger Chart

Last Sunday, we arrived in Greece. We have interviewed since then more than 25 people across the country. We have selected ordinary people, with different jobs, from all ages, both in cities and rural areas. So our research is representative for the whole population. What people told us is staggering, and it becomes worse we compare this with the acts of the government. This is a live report about the government debt crisis.

Last Sunday, we arrived in Greece. We have interviewed since then more than 25 people across the country. We have selected ordinary people, with different jobs, from all ages, both in cities and rural areas. So our research is representative for the whole population. What people told us is staggering, and it becomes worse we compare this with the acts of the government. This is a live report about the government debt crisis.

In general, people describe the current economic situation as hopeless; there is no outlook for growth whatsoever. Everyone agrees that this crisis will go on for many years before the country can see any economic improvement.

If anything, people are extremely frustrated. That remains underexposed in the media. The frustration comes from the fact that the masses believe they are disadvantaged with the ongoing reforms. People understand they have to contribute (by paying taxes for instance) to fight the crisis, but it has to happen equally: the ones who benefited most during the years of excesses should contribute proportionately more. And that is not happening. Even with this extreme left government led by Syriza, it is simply not happening.

With the recent bank holiday (started July 5th) it became clear that the economic and political problem is not a far-flung event, a view which was shared by most people up until that point. The bank holiday has exhausted people financially, and the restriction of retrieving 60 EUR / day is extremely frustrating. Many ATM’s are not working, there is not always one nearby, so people often have a cost of 5 to 15 EUR simply to get to money out of an ATM.

Greek people were already in a very bad shape financially, but the bank holiday and ATM restriction is exhausting them. And everyone we interviewed was convinced that capital controls will be there to stay for many months, not a very healthy outlook.

Next to financial exhaustion, people are increasingly becoming psychologically exhausted. On the one hand, leaders proceed from one crisis meeting to another. Every meeting is announced as being a critical one. On the other hand, all local media are broadcasting all sorts of opinions and viewpoints, almost 24/7. People are at a point where they are confused, and don’t understand what is truly good or bad for them.

Everyone we interviewed said they desperately want “ a ” solution. The solution itself, whether it is in line with their view or not, has become of secondary importance. People simply want a direction, a path forward; they want to work towards a goal.

In that respect, most of the people we talked to had a lot of criticism about the referendum of July 5th as it has created even more confusion among people. First and foremost, because the people’s voice has been abused during political negotiations. People admit that they were not able to assess the documents that were proposed by the insitutions, which were technical in nature, long, and hence incomprehensive. The “OXI” votes were merely nationalistic. Second, the results have been misinterpreted. It remained quite underexposed that 39% of the citizens did NOT vote, so the majority vote was blank. Given that figure, the 61% “OXI” vote was in reality 36% in total, and so the remaining 25% voted “yes.” That’s a different story than the one propagated by the government and in the media. Third, all Greeks we interviewed agreed that the referendum left too much room for (mis)interpration. People admit that everyone has another interpretation, which adds to the confusion.

If anything, Greek people want justice. One of the big problems of the past was mismanagement of government money (think of subsidies, pensions, etc). The abuse was staggering, and the money has been distributed in an asymmetric way (in other words, a small group of people has benefited in a disproportionate way). Greek people want those issues to be solved. They want justice.

Case in point: one of the people we interviewed is running a cafeteria. The taxes for playing music were approx. 400 EUR per year. With a recent law, the tax increased to 1000 EUR. Apparently, that was the result of a ‘new’ law. However, only a few people have paid that tax in the past. The problem now is that those who did not pay it previously, are exempt because of the fact it is an ‘outdated’ law (replaced by ’new’ one). That is extremely frustrating for those who are paying taxes correctly.

That brings up the point of fraud and overpaid civil servants. In recent years, there were a lot of reports about “shadow pensions”, for instance pensions to people who were not alive. Similarly, a lot of pension plans included premiums as high as 100k EUR, unreasonably high. Also, we heard a lot of cases in which subsidies were greatly abused, maximizing the unproductiveness of the country. “That is the reason we are in such a bad shape today”, is the view of almost all people we interviewed.

Contrary to what some others report, we got a very clear picture about how Greece got into this situation. Greek people understand that structural reforms are an absolute must. The number of civil servants has to come down, the government has to crack down on fraud and corruption. What remains unclear, however, is how economic growth can be stimulated. Let’s consider that the biggest challenge of the government.

And that is where we see a big problem. The current government has promised an even bigger state, not a smaller one. They have promised hard measures against the ones who benefited most in the past, but haven’t executed any so far. They have promised economic improvements, but the country is an economic catastrophe since Syriza took over in January.

Here is the biggest mistery of them all. Although the government has promised to fight any bailout plan, Mr. Tsipras came up with Greece’s 3d big bailout plan this week. How do Greek people react on that?

Opponents of Syriza obviously are critizing Mr. Tsipras for that. They point out that the current government has brought false hopes, based on unrealistic promises. On the other hand, proponents of Syriza are still defending Mr. Tsipras, saying that he was “cornered”, and that the bailout plan was the only viable solution. They believe that he had a “plan B” but was somehow “prohibited” to implement it. They still believe Mr. Tsipras is a great politician as he is the only one who can bring justice and reforms.

Let us pause for a minute here, and add our own observation. Taking everything together, it is clear to us that today’s economic and monetary crisis is a politically induced one. Politicians can facilitate the way out. And that is where it potentially can go wrong. The country needs drastic measures which are, in nature, politically unpopular. Moreover, politicians have a track record of creating confusion to people, and bringing false hopes (as discussed earlier). The only way out, in our view, is one of increased pressure by European leaders.

That leads us to the European aspect. The current government has stimulated an anti-Europe preference. However, by far most of the people we interviewed have a pro-European viewpoint. Almost everyone believes it is a better thing for Greece to stay in the Eurozone, as it is a much stronger currency than a Greek currency. Hence, the economic outlook, in the very long term, would be better being part of Europe. Moreover, people admit that European leaders have the potential to force discipline, order and justice, something Greek governments will probably not realize themselves.

It is not a strange idea that Europe can help Greece, and it is clear that European leaders are aware of it as well. When we analyzed the bailout plan which was agreed last weekend, we see in the agreement 9 measures related to structural reforms, one of which being the following:

“To modernise and significantly strengthen the Greek administration, and to put in place a programme, under the auspices of the European Commission, for capacity-building and de-politicizing the Greek administration.”

At the end of the day, that is exactly what Greek people are asking for. So Europe can really help Greece in its need to reform structurally. And, obviously, European leaders know very well that is the weakest point of Greece.

The anti-Europeans we interviewed, although a minority, brought up the fact that Europe (read: Germany) is suppressing Greece. That idea is originated from the feeling that Greece is not a sovereign state anymore, which is fed by the current government.

Our conclusion is that Greece is a textbook “boom and bust” case. The country is today paying the price of two decades of excesses, based on unsound economic expansion (i.e., uncontrolled government spending). Contrary to what some report, we clearly see that Greek people realize this, and they desperately want to change this. Whether politicians will be able to bring change or not, is the trillion dollar question in our view. In any case, politicans hold the key to change, especially when it comes to legislation and taxes, corruption and fraud, productive economic stimulus.

It is really sad to see how the Greek people fell victim of an unfair economic system, created by previous governments, cheap money, and a big state. But it is exactly at this point where some Greeks hope that this crisis has the potential to bring real change. Greek people are so exhausted that they are willing to accept change. Politicians, however, have to do the right thing, which means focus on the interest of their country, not their personal votes.

We are preparing a report on “crisis investing in Greece.” Stay tuned by subscribing to our newsletter at SecularInvestor.com.

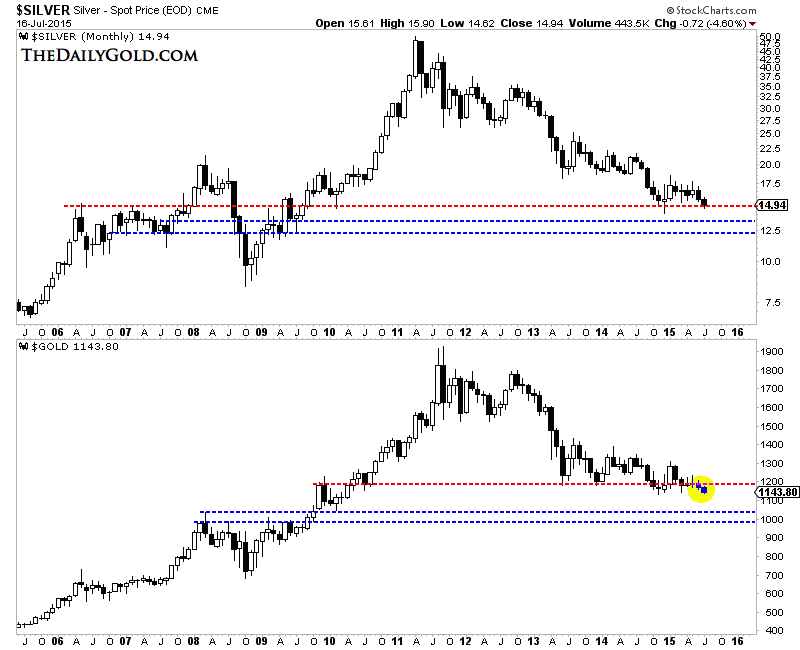

The gold miners have broken below their 2008 to 2014 support while Silver is essentially trading at a six year low. Gold looks set to make a new monthly low and weekly low but has yet to break its daily low at $1140/oz. Barring a sudden short squeeze Gold could be hours or days away from cracking in the way Silver and the miners have in recent weeks. The trend for the sector is obviously down and sentiment is following. However, the more important issue for long term bulls is where is the strong support for these markets.

The monthly candle charts of Silver and Gold are below. I’ll start with Silver. It is losing key support at $15/oz. The next key support levels are in the low $13s and low $12s. Moving to Gold, note that Gold appears to have lost $1180/oz which has been a key support level for two years. The monthly chart shows that the next strong support levels are $1040 and $1000.

Silver & Gold Monthly

Moving on, let’s look at the miners. We plot $GDM (essentially GDX) and the HUI Gold Bugs Index. This time we look at the weekly line charts. The picture remains clear. GDM has broken below key support (the 2008 and 2014 lows) of 500. It has about 11% downside to the next strong support at 400. The HUI is a much weaker index as unlike GDM it is comprised only of miners and not the stronger royalty companies. The HUI still has a whopping 25% downside to its next major support.

GDM (GDX) & HUI Weekly

GDXJ (not shown) is not performing as poorly as GDX and HUI because junior companies don’t have debt. In looking at the top five gold producers I found a combined market cap of roughly $40 Billion, $6.5 Billion in cash but $27 Billion in debt. Gold breaking below $1140 and $1100 could exacerbate the problems facing miners with significant debt. Hence, the GDXJ to GDX ratio should continue to rise.

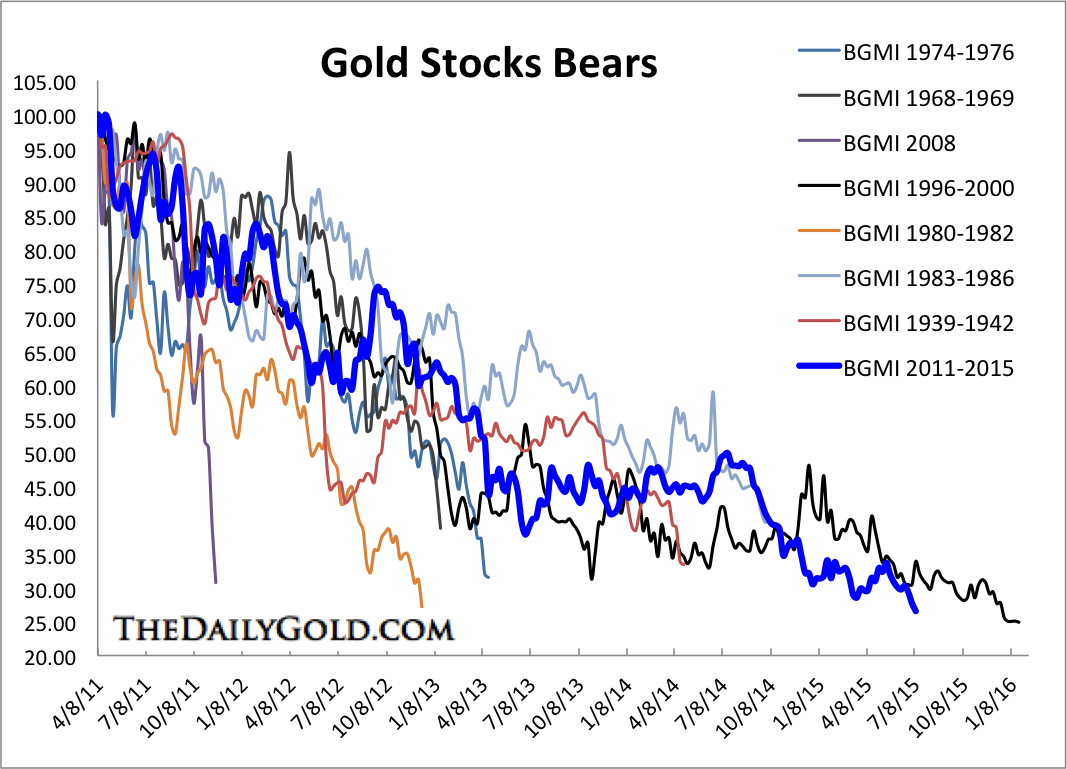

The bear market in the miners is on the cusp of matching the 1996-2000 bear market. If the Barron’s Gold Mining Index drops another 10% then it will match the decline from 1996-2000. If the HUI drops to 100 it will match the decline from 1996-2000. If GDM, which closed Thursday at 448, drops 7% then it would match its decline from 1996-2000. You get the point.

The gold stocks bear analog chart below puts this bear market into perspective.

Barron’s Gold Mining Index Bear Markets

Considering the support targets, it is too soon to be a buyer. We’d prefer to see Gold below $1100 and Silver below $14 before thinking about buying. We will also keep the targets for GDM and the HUI in mind. If Gold cracks $1140 and $1100 immediately thereafter it is possible a mini capitulation could develop and the sector could rally. In our view the bottom is likely to develop over a few months rather than a few days or weeks. Stay defensive and stay nimble with hedges and short positions. At somepoint within a few months, the switch will flip and we could have some epic buying opportunities in the precious metals complex. Consider learning more about our premium service including our favorite junior miners which we expect to outperform in the second half of 2015.

Jordan Roy-Byrne, CMT

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair