Asset protection

One of the early signs that a cycle is about to turn down is disorder in junk bonds. That’s because the companies that issue such bonds are by definition financially and/or operationally weak and therefore ultra-sensitive to changes in their environment. A modest drop in, say, consumer spending or the price of wind turbines will hardly be noticed by an Apple or GE but might threaten the survival of those companies’ weakest competitors. And as credit bubbles inflate, the weak in every field tend to proliferate as overexcited bankers and bond funds offer them plenty of rope with which to hang themselves.

So when such bonds start falling — which is to say when their yields start rising — that’s a sign of broad-based trouble ahead. From Tuesday’s Wall Street Journal:

Today’s Big Number: 15.7% of high-yield bonds trading at distressed levels

The commodity -price crunch fueled by China’s economic slow-down is taking a toll on the bond market.

Bonds from debt-laden companies in the metals, mining and steel industries are driving up distress ratios, an indicator that a wave of debt defaults could be on the horizon.

As of mid-September, nearly 15.7% of the roughly 1,720 bonds rated below investment grade traded at distressed levels, the biggest share since 2011, according to Standard & Poor’s Ratings Services. Such bonds were trading with yields at least 10 percentage points over comparable U.S. Treasurys. Yields on bonds rise when prices fall.

Companies with distressed bonds may not be able to refinance or access other forms of capita, said Diane Vazza, an S&P managing director.

The numbers suggest that many companies could default in the next seven to nine months. “There’s a very strong correlation” between bonds that fall into the distressed category and defaults, she said.

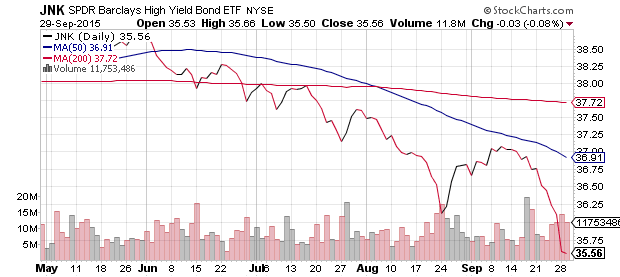

It’s not surprising that the commodities crash would impact the bonds of coal and oil companies. The big question is whether the carnage spreads to other kinds of junk. And over the last couple of months it has. The chart below shows the price of a junk bond ETF that last week plunged through the lows of the August mini-panic.

Wolf Richter and Zero Hedge just posted long, very enlightening pieces on this subject. See, respectively, This is When Bonds Go Kaboom! and BofA issues dramatic junk bond meltdown warning.

The short version of the story is that if things play out as they have in past down-cycles, junk defaults will spike from here and capital will flow out of this and other volatile markets and into the safest havens, which historically have been high-grade government bonds, the shares of rock-solid, non-cyclical companies, and, frequently, precious metals.

Governments, meanwhile, will respond with lower interest rates, big deficits and tax cuts. Which is where our story departs from the standard script: With money already extremely easy in most places and sovereign debt at record levels, the government response will have to be either non-traditional or numerically extreme. That is, negative interest rates and helicopter money. So today’s junk implosion differs from those of 1990, 2000 and 2007 not in itself but in the changes it might set off in the broader economy.

Today’s infographic covers five reasons to stay bullish on bitcoin and cryptocurrency.

One of those reasons? Resilience. Bitcoin has been declared to be “dead” 72 times by the media.

We call on central banks to abolish their zero interest rate policy (ZIRP) framework before more harm is done. In our assessment, ZIRP is bad for all stakeholders and may even lead to war.

We call on central banks to abolish their zero interest rate policy (ZIRP) framework before more harm is done. In our assessment, ZIRP is bad for all stakeholders and may even lead to war.

ZIRP: Bad for Business?

At first blush, it may appear great for business to have access to cheap financing. But what may be good for any one business is not necessarily good for the economy. When interest rates are artificially depressed, it can subsidize struggling enterprises that might otherwise be driven out of business. As a result, productive capital can be locked into zombie enterprises. If ailing businesses were allowed to fail, those laid off would need to look for new jobs at firms that have a better chance of succeeding. As such, the core tenant of capitalism: creative destruction, may be undermined through ZIRP. In our assessment, the result is that an economy grows at substantially below its potential.

ZIRP: Bad for Investors?

Investors may have enjoyed the rush of rising asset prices as a result of ZIRP. However, this may well have been a Faustian bargain as the Federal Reserve (Fed) and other central banks have masked, but not eliminated, the risks that come with investing. Complacency has been rampant, as asset prices rose on the backdrop of low volatility. When volatility is low (more broadly speaking, we refer to “compressed risk premia”), rational investors tend to allocate more money to historically risky assets. While that may be exactly what central banks want – at least for the real economy – investors may bail out when volatility spikes, as they realize they didn’t sign up for this (“I didn’t know the markets were risky!”).

We believe that until early August this year, investors generally “bought the dips” out of concern of missing out on rallies. Now, they may be “selling the rallies” as they scramble to preserve their paper gains. This process is driven by the Fed’s desire to pursue an “exit.” For more details on this, please see our recent Merk Insight “Lowdown on Rate Hikes.”

But it’s not just bad because asset prices might crumble again after their meteoric rise; it’s bad because, in our analysis, ZIRP has driven fundamental analysts to the sideline. For anecdotal evidence, look no further than the decision by Barron’s Magazine to kick Fred Hickey (who may well be one of the best analysts of our era) out of the Barron’s Roundtable. Instead, money looks to be flocking towards investment strategies based on momentum investing, a strategy that works until it doesn’t. Again, ZIRP gives capitalism a bad name because we feel it disrupts efficient capital allocation.

ZIRP: Bad for Main Street?

Excessively low interest rates are also bad for Main Street. In our analysis, excessively low interest rates are a key driver of the growing wealth gap in the U.S. and abroad. Hedge funds and sophisticated investors seemed to thrive as they engaged in highly levered bets; at the other end of the spectrum are everyday people that may not get any interest on their savings, but are lured into taking out loans they may not be able to afford. We believe ever more people are vulnerable to “fall through the cracks” as they encounter financial shocks, such as the loss of a job or medical expenses; hardship may be exacerbated because people had been incentivized to load up on debt even before they encountered a financial emergency. Again, we believe ZIRP gives capitalism a bad name, although ZIRP has nothing to do with capitalism.

Low interest rates may not even be good for home buyers: it may sound attractive to have low financing cost, but the public appears to slowly wake up to the fact that when rates are low, prices are higher: be that the prices of college tuition or homes. It’s all great to have high home prices when you are a home owner, but it’s not so great when you are trying to buy your first home.

ZIRP: Bad for Price Stability?

While we believe inflation may ultimately be a problem if interest rates are kept too low for too long, ZIRP may temporarily suppress inflation. While this may sound counter-intuitive, it is precisely because of the aforementioned capital misallocation ZIRP may be fostering: when inefficient businesses are being subsidized, as we believe ZIRP does, inflation dynamics may not follow classical rulebooks. That’s because an economy with inefficient capital resource allocation experiences shifts in supply of goods and services that may not match demand leading to what may appear to be erratic price shifts. The most notable example may be commodity prices, where the extreme price moves in recent years are a symptom that not all is right.

ZIRP: Bad for Politics?

In our assessment, Congress has increasingly outsourced its duties to the Fed (the same applies to politicians and central bankers to many other parts of the world). The Fed now ought to look after inflation, employment, and financial stability. The Fed, in our humble opinion, is not only ill suited to tackle most of these, but invites political backlash as they step on fiscal turf. Let me explain: monetary policy focuses on the amount of credit available in the economy; in contrast, fiscal policy – through tax and regulatory policy – focuses on how this credit gets allocated. If the Fed now allocates money to a specific sector of the economy, say, the mortgage market by buying Mortgage Backed Securities (MBS), they meddle in politics. Calls to “audit the Fed” are likely a direct result of the Fed having overstepped their authority, increasingly blurring the lines between the Fed and Congress.

More importantly, the U.S., just like Europe and Japan, face important challenges that in our opinion can neither be outsourced, nor solved by central banks in general or ZIRP in particular.

ZIRP: Bad for Peace?

In 2008 and subsequent years, you likely heard the phrase, “Central banks can provide liquidity, but not solvency.” In essence, it means central banks can buy time. But what happens when central banks buy a lot of time and underlying problems are not fixed? In our assessment, it means that the public gets antsy, gets upset. When problems persist for many years the public demands new solutions. But because monetary policy is too abstract of an issue for most, they look for solutions elsewhere, providing fertile ground for populist politicians. Here are just a few prominent political figures that have thrived due to public frustration with the status quo: Presidential candidate Donald Trump; Senator and Presidential candidate Bernie Sanders; Greek Prime Minister Tsipras; Ukrainian Prime Minister Yatsenyuk; Japanese Prime Minister Abe; and most recently the new leader of UK’s Labor Party Jeremy Corbyn.

And what do just about all politicians – not just the ones mentioned above – have in common? They rarely ever blame themselves; instead, they seem to blame the wealthy, minorities or foreigners for any problems.

We believe the key problem many countries have is debt. I allege that if countries had their fiscal house in order, they would rarely see the rise of populist politicians. While there are exceptions to this simplified view, Ukraine may not be one of them: would Ukraine be in the situation it is in today if the country were able to balance its books?

Central banks are clearly not appointing populist politicians, but we allege ZIRP provides a key ingredient that allows such politicians to rise and thrive. ZIRP has allowed governments to carry what we believe are excessive debt burdens though ZIRPs cousin quantitative easing (“QE”). QE is essentially government debt monetization in our view. Take the Fed’s U.S. treasury buying QE program. Those Treasuries (or new Treasuries that the Fed rolls into) might be held indefinitely by the Fed (despite claims of balance sheet normalization) – meaning that US Government will never pay the principle, and the U.S. Government effectively pays zero interest on that debt because the profits of the Fed flow back to the US Treasury. ZIRP allows governments to engage on spending sprees, such as a boost of military spending Prime Minister Abe might pursue.

The Great Depression ultimately ended in World War II. I’m not suggesting that the policies of any one politician currently in office or running for office will lead to World War III. However, I am rather concerned that the longer we continue on the current path, the more political instability will be fostered that could ultimately lead to a major international conflict.

How to get out of this mess

It’s about time we embrace what we have been lobbying for since the onset of the financial crisis: the best short-term policy is a good long-term policy. We have to realize that when faced with a credit bust, there will be losers, and that printing money cannot change that. In that spirit, we must not be afraid of normalizing policy in fear of causing an economic setback. When rates rise, businesses that should have failed long ago, are likely to fail. Rather than merely rising rates, though, policy makers must provide a long-term vision of the principles that guides their long-term policy. In our humble opinion, “data dependency” is an inadequate principle, if it is one at all.

The Fed needs to have the guts to tell Congress that it is not their role to fix their problems. It requires guts because they must be willing to accept a recession in making their point.

To continue this discussion, please register to join us for our upcoming quarterly Webinar. If you haven’t already done so, ensure you don’t miss it by signing up to receive Merk Insights. If you believe this analysis might be of value to your friends, please share it with them.

###

Sep 29, 2015

Axel Merk

Contact Merk

This report was prepared by Merk Investments LLC, and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Merk Investments LLC makes no representation regarding the advisability of investing in the products herein. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute investment advice and is not intended as an endorsement of any specific investment. The information contained herein is general in nature and is provided solely for educational and informational purposes. The information provided does not constitute legal, financial or tax advice. You should obtain advice specific to your circumstances from your own legal, financial and tax advisors. Past performance is no guarantee of future results.

©2005-2015 Merk Investments LLC. All Rights Reserved.

If you’re like most investors, you believe the worst of the 2008 debt crisis — and the Great Recession that followed — are over.

If you’re like most investors, you believe the worst of the 2008 debt crisis — and the Great Recession that followed — are over.

You believe America is now solidly on the road to economic recovery, her greatest struggles behind her.

But if you’ve been following my work, you know it’s nothing but a mirage; bought and paid for by the very people who triggered these great calamities.

The reality is, America’s fate has already been sealed; sacrificed on the altar of power and greed by those who swore an oath to defend her — with the blood of every man, woman and child they swore to defend.

The fact is that America is on the decline, destined to go the way of the many great empires that came before us. Like Rome. Byzantium. France. Spain. And Great Britain.

No, the U.S. won’t disappear. But we will slip to number two, and ultimately to number three in the world, behind China and Southeast Asia.

And the thing is, America’s demise will NOT be triggered by hyperinflation … or a bond market collapse … or a stock market crash … or

any single catastrophic event, as some may have you believe.

In fact, even though the equity market correction I have been expecting is now here, long-term, the U.S. stock markets remain poised for very substantial gains.

And yes, even if the U.S. economy just muddles through. Why?

It’s simple:

A. Europe is in worse shape than the United Sates. So is Japan. And …

B. Our own government in Washington is the most indebted of them all, lighting a fuse under savvy investors who are already starting to pull their money out of the sovereign U.S. bond market and putting it right into stocks.

If you understand those two forces, you will not only be able to protect your wealth in the months and years ahead, you’ll also be able to profit, very well indeed.

Yes, I know, it makes no sense. If America is on the decline, how can stocks go higher?

We’ve seen the forces I speak of above before. It’s what I call the other side of the Great Depression that no one seems to ever want to talk about.

It’s when 17 countries in Europe failed and Great Britain was quickly losing its superpower status, yet between 1932 and 1937, the Dow Jones Industrials exploded 387% higher, even as the U.S. economy sunk further into a depression.

So once the current correction in U.S. equities plays out, get ready to load up on stocks.

And not only because the parallels to the above will soon be in play …

But also because most companies in America are in better financial shape that our own government. And, importantly, stocks are considered largely non-confiscatable.

That’s important, because on its way down, Washington will seek to nationalize part or all of your retirement assets, confiscate gold, and certainly tax you more and more.

Yet, they will never subpoena Apple for a list of its shareholders. They will never confiscate your shares in a publicly traded company.

Also keep in mind that history tells us that when governments and empires start to decline, they regularly unravel with terrifying speed.

17 years for the British Empire …

11 years for the Ottomans …

8 years for France …

2 years for the Soviet Union …

In every case … the people ignored the writing on the wall, thinking it couldn’t happen to them.

In every case … the government feigned ignorance, swearing on a stack of Bibles that the worst was over.

In every case … the majority failed to prepare for what was coming.

One need only look to Europe for the tragic results, where rioting, civil unrest, and depression-like conditions are now a way of life.

Jobs are being hemorrhaged. Personal income is falling. Social services are deteriorating. Home values are plunging. Crime is soaring.

It’s virtually impossible to put into words the nightmare of poverty, hunger, and homelessness jobless workers throughout Europe are feeling. While ironically, hundreds of thousands of others seek refuge in Europe’s dying empire.

All this as the European aristocracy preserves their own wealth by looting the economy, while slashing wages and social services for the working class at the same time. Imposing life-suffocating austerity measures on virtually every country and people but themselves.

It’s easy to see these as isolated events. It’s easy to bury your head in the sand and ignore, because it’s happening “somewhere else” …

It’s easy to forget if you listen to all the government-rigged economic numbers …

Yet millions of real people, and real families, in Europe and Japan are suffering very real consequences; quickly finding themselves living in total desperation — with little hope of having a “normal” life.

It’s even easier to think we’re immune; that it can’t happen in America.

Yet the frightening reality is that …

-

Some 94 million working age Americans are not in the labor force …

-

The average duration of unemployment has soared since January 2009 – from 19.8 weeks to 28.4 weeks …

-

39% of those lucky enough to have a job earn less than $20,000 a year …

-

46.7 million Americans – or 15% of the U.S. population – are now living in poverty, according to the U.S. Census Bureau …

-

45.9 million Americans are now on food stamps …

-

The rate of homeownership has declined eight years in a row.

This is the new reality.

But there is a silver lining in this grim cloud of reality; important lessons to be learned by studying the history of failing empires.

First, understand the lessons of history and you will not only be better prepared to protect your wealth, but stand to grow it substantially as well. Just like many of the titans of the Great Depression, who saw the capital fleeing the bond markets of other countries around the world and who knew that there was no other place for that capital to go than into the deepest most liquid markets on the planet — U.S. stocks.

Second, open your mind to new possibilities, new ways to protect and grow your wealth.For as the above illustrations of what happened to U.S. stock markets between 1932 and 1937 clearly shows — is that during times of sovereign crisis …

Which is what is brewing now in Europe, Japan and the United States …

Everything you thought you knew about investing can be turned inside out and upside down.

Third, the tangible asset sector, commodities, natural resources, precious metals — will be amongst the biggest winners.

We’re not there quite yet, as most commodities have not yet bottomed. So build your stash of ammo for commodities …

Because when they do bottom, fortunes bigger than you can imagine can be had by you and I — lay people who will embrace what’s happening, and protect and grow our finances as sovereign empires start dying.

Best wishes,

Larry

erx

Why ETFs Are the First Step on the Road to Wealth

Ask me to name the greatest retail product to ever come out of Wall Street and I’ll point to exchange-traded funds – better known as ETFs.

ETFs are great for lots of reasons, but mostly because they are supreme Disruptors.

Their introduction in 1993 disrupted the staid, overly hyped, unnecessarily expensive, inefficient, self-serving, and much-too-opaque mutual fund industry.

Besides being financial-sector Disruptors, ETFs are extraordinary personal Disruptors. And as I’ll be showing you in the months to come, whenever you find a spot where two or more Disruptors/catalysts converge, you’ve also identified your biggest Extreme Profit opportunities.

Today I want to show you how to employ this Disruptanomics “one-two punch” to your maximum personal advantage.

It will uncomplicate your financial life by establishing a foundation for your Extreme Profit investments.

And that will set you up for Extreme Wealth.

We’ll set you up for all of this… one step at a time…

Why I Dig ETFs

Why I Dig ETFs

Let me start by openly admitting my bias: I love ETFs… even more than I’ve always disliked conventional mutual funds.

That “bias” is actually a big part of the reason I view ETFs as such a foundation for meaningful wealth.

During my time as a professional trader, you see, I would never place my money where I couldn’t see what someone was doing with it, where it was expensive to park, or where I couldn’t – during market hours – turn my shares into cash when my indicators told me it was time to “take cover.”

In describing all those shortcomings, I’ve just described conventional mutual funds.

Lots of investors own mutual funds – because that’s what they were “sold” for many years by the industry that tried to enslave them.

The upshot: Those fund holders have no concept about how badly they’re being exploited.

Most mutual fund are way too expensive. Some also have sales charges and exit charges (called front and rear “loads” in broker parlance) and so-called 12b-1 fees and transaction charges.

Unless it’s an index fund, you’re only told what’s in your mutual fund portfolio every quarter – and even then there’s a 30-day time lag. With mutual funds, it’s possible to lose money on your investment and still have to pay capital-gains taxes.

And there’s the whole price realization uncertainty thing: Even if you sell a fund early in the trading day, you’re still going to get that evening’s closing price. That doesn’t do us a damn bit of good if we see the market slipping – and sell – only to have stocks plunge a few thousand points afterward.

No thank you.

Anatomy of a Winner

You have none of these issues with ETFs.

(I did detail some pricing issues in a report I shared last week, but those issues were limited to major “down” markets. And let’s face it: In a market that bad, you’ll have problems with investments of all types – not just ETFs.)

Exchange-traded funds are just better products.

ETF expense ratios are, on average, about half those of most managed mutual funds. According to Morningstar, the average expense ratio on a managed mutual fund is 1.42%. On an ETF, the average is 0.53%… but on most ETFs, the expense ratio is closer to 0.40%.

With ETFs, you know what’s in the underlying portfolio. Almost all ETF sponsors have product websites where you can see what’s in the fund portfolios. Even “managed ETFs” – which trade in and out of stocks – have to post their holdings every day.

You will have capital gains when you sell your ETFs – if you bought them at a lower price. So you won’t get socked with a capital-gains tax bill if you haven’t sold them, which happens too often with mutual funds.

Most important, for me, is that I can sell my ETFs any time during the day and know what price I’ve gotten. Sometimes you can trade ETFs before and after hours if there are buyers or sellers on the other side of your trade when the exchanges are closed.

There are all kinds of offerings, but one basic theme.

There are more than 1,500 ETFs in the market. Another 150 are introduced every year. Not all ETFs that make it to market live forever. More than a few die off every year – for different reasons – but mostly from lack of investor interest in them.

What makes the great majority of ETFs so valuable is that most of them are basically indexed products.

And they’re indexed in unique ways.

There are baskets of stocks, or futures, or bonds, or derivatives – or hard assets, such as physical gold – which make up underlying portfolios and represent an industry, an asset class, a country’s stock market… or even fixed-income securities of different yields, risk profiles, and maturities. Whatever the underlying “stuff” is in the portfolio, an ETF gives you specific exposure to what you want to trade or invest in.

The best examples of ETFs being mostly indexed products are the major market benchmark indexes. Those three ETF products are, in my professional opinion, the most important for investors and traders.

The “Big Three” ETFs

Although there may be different ETF products that track the same benchmarks, the ones that have the most assets under management – meaning the biggest, most liquid ETFs that have huge daily trading volumes – are the ones you should look at.

They’re always your best bet.

The best ETF to track and trade the benchmark Standard & Poor’s 500 Index happens to be the first ETF ever introduced – the SPDR S&P 500 Trust (NYSE: SPY), which made its debut back in 1993.

With $176 billion under management, SPY is huge. It’s also liquid – trading an average of more than 144 million shares daily. And it has a microscopic expense ratio of only 0.09%.

That makes it a winner in my book.

The best ETF to track and trade the Dow Jones Industrial Average is the SPDR Dow JonesIndustrial Average ETF (NYSE: DIA). DIA has $10.89 billion under management, trades more than 7 million shares a day, and has a 0.17% expense ratio.

The best ETF to track and trade the tech-focused Nasdaq Composite Index is the PowerShares QQQ Trust Series 1 (Nasdaq: QQQ). QQQ controls $38.32 billion, trades an average of nearly 40 million shares a day, and has a 0.20% expense ratio. QQQ is more than 60% technology stocks, with Apple Inc. (Nasdaq: AAPL) making up about 13% of its total weight.

Starting out, as everyday trading vehicles – as a way to invest long term in the market or as a hedge against falling stocks – these big benchmark index “stocks” are my go-to ETFs.

When I watch the market, I watch the Dow first (because that’s the index most news shows talk about and it’s the one the typical investor is the most in tune with), the S&P 500 second, and the Nasdaq third. These benchmarks are the U.S. market in most everybody’s mind. They’re all different, but all important.

Because the easiest and cheapest way to play the market – for you and for institutional money managers – is to buy one of these ETFs (depending which stock index you are interested in), they are super important to watch. I watch and trade all three ETFs.

I’m a big-picture trader. Because I trade a lot of money, the most important thing to me is being on the right side of the market. These three indexes and ETFs are “the stock market” to me – and to the money managers who trade U.S. stocks.

If you are on the right side of the market, it’s hard not to make money. The simplest way to make money is by buying one or all three of these cheap ETFs… when the market is going up. As a trader, that’s what I do. And if I don’t believe the trend will continue to go higher, I’ll sell.

And if I think the markets are headed lower, I’ll short these three ETFs.

The Simple Things…

Making money really is simple if you don’t complicate things. That’s why these ETFs, in particular, are so valuable. You’re watching the market and trading the same thing you’re watching. There’s no disconnect.

While there’s no disconnect between watching the market and trading an ETF that tracks it, ETFs can face intraday pricing disconnects when any of the underlying stocks or futures that make up the portfolio stop trading for any reason. I wrote about that last week and offered a solution.

Trading these big ETFs is easier than trading any stock because you’re trading the market. And the market is a lot easier to understand (as a giant entity) than a single public company that has products, management, and all kinds of “firm-specific” issues – including how its stock trades relative to other stocks in its industry and relative to the market.

Trading individual stocks is great, and, of course, I do that.

But there’s nothing easier than trading the market. That’s what I do most and make the most money doing.

If you want to make a lot of money and set yourself up to trade a lot more stocks a lot more successfully, start here. I promise you’ll become a much more profitable investor.

We’ll trade these ETFs together from now on. I’ll tell you exactly what I’m looking at, what I’m seeing, and how to make the same trades I would make.

This will serve as a foundation for other “Extreme Profit” trades that I’ll ferret out for you. In fact, having this base will make it easier to identify these other opportunities.

Consider it the first step on the road to wealth.

That’s why I love ETFs.

Follow us on Twitter @moneymorning.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair