Currency

The strong rally in the US Dollar since the past year has led to commodity markets selling off as investors pursued the equity markets led by years of accommodative monetary policy in a search for higher yielding assets. However, what goes up must eventually come down and the US Dollar is no different. With the markets trading at extremes the markets are likely to see a correction in the near term as the US Fed prepares for interest rate liftoff this December. Given the current monetary policy conditions and the markets being prepped for a rate hike, there is further upside to the UUP while the price of Gold continues to decline to new multi-year lows.

Many people think that they ring a bell at the top of a bull market. Ding-a-ling-a-ling.

That is indeed often the case. The bell was rung in 2000 at the top of the dot-com bubble—I like to think it was 3Com spinning off Palm that broke its back.

But sometimes there is no bell, no catalyst, no story to tell. A bull market becomes a bear market, and it happens just like that.

Silicon Valley has been in a food fight for about three years now. Everyone knows it’s going to end, except for the folks in Silicon Valley. These guys are funny. I met a few of them in the last cycle. They really thought it was going to go on forever.

There are now 145 unicorn companies (private companies with a valuation of $1 billion or more), with a total combined valuation of $506 billion.

We are watching the top happen right before our eyes.

Square

If you were paying attention a couple of weeks ago, you might have read the news about a company called Square going public. Jack Dorsey is the CEO of Square. He is also the CEO of Twitter. I think of this sometimes whenever I complain that I’m too busy.

Square got a round of financing in 2014 at a $6 billion valuation, and now it’s a public company. If you pull up SQ on Yahoo! Finance, you will see that the market cap is $4 billion.

As Square was making the rounds in the roadshow, investors decided they didn’t want to overpay just to make the mezzanine round investors rich. So there wasn’t much demand for Square at a $6 billion market cap. It eventually went public at a $3 billion market cap, or $9/share. (The deal performed well in the aftermarket, at least. The stock is trading at $12.)

No catalyst. No bell ringing. The price simply got too high, and people pulled back. But you know what this means. If one deal can trade below private valuations, they can all trade below private valuations.

On to the next data point…

Fidelity

You may not know this, but Fidelity owns shares of private companies in some of its funds (like Contrafund). Fidelity has to figure out how to value these things.

In general, venture capital firms have to mark their investments to “market,” whatever that means. To do this, they use the services of third party valuation firms. Those valuation guesses are probably subject to mood or opinion, and as you can imagine, there are a lot of bad guesses. The valuations don’t mean much—if you’re an LP (limited partner), at the end of the day, you care about cash in and cash out. But mark-to-market creates some interesting short-term incentives.

As for Fidelity, they also have to mark things to market, and they also use valuation firms. But valuation firm A that Sequoia is using is different than valuation firm B that Fidelity is using. And Fidelity perhaps wants its valuation firm to be more conservative.

So Fidelity has been marking its private investments to market at levels that are below the most recent funding rounds. This puts the VCs in a bit of a pickle. Do they copy Fidelity or do they press on with their own, higher valuations in the face of dissenting opinions?

None of this makes people very bullish on startups.

Uber

Uber is the biggest unicorn of all, with a $50 billion valuation. Side note: they don’t make any money.

Uber is trying to raise another billion—at a $70 billion valuation.

Now, the only reason you would invest in Uber at a $70 billion valuation is if you thought they would go public at $80 billion or more. But looking at what happened to Square, that will almost definitely not happen.

And why would you pay $70 billion for Uber when Fidelity is going to mark it in your mush? Another great question.

I don’t think anyone is in the mood to pay $70 billion for Uber. Uber is stuck. They will have to go public or take a down round if they really need the cash.

And this, folks, is how bear markets start.

Brainstorming Session

So let’s do some brainstorming on what this could mean if it really were the end of the line for Silicon Valley (at least in the medium term).

- Since tech has been going up while energy/mining has been going down, could this trend reverse?

- Could value start to outperform growth? (If I’m not mistaken, it already is.)

- Could large cap start to outperform small cap? (Boy, is it ever.)

- If you lived in the Bay Area, would you want to sell your house and rent?

- As new tech is in the process of topping, have you seen what old tech has been doing? Check out the chart of Microsoft, at 15-year highs:

For full disclosure, I started calling the top (or at least asking hard questions) on Silicon Valley about a year and a half ago. But I think most dedicated observers saw what happened with the Square IPO and said, “Yep, that might be the top.”

The other thing I’ve learned is that even when people recognize the top, they vastly underestimate how bad the pain is going to be on the downside. “Oh, it’ll just be a quick correction.” Never is.

One last riposte: Anyone who invested at these valuations will richly deserve what’s coming to them. Those prices were cuckoo.

Jared Dillian

Jared’s premium investment service, Street Freak, is available now. Click here for our introductory offer. Jared Dillian, former head of ETF Trading at one of the biggest Wall Street firms and author of the highly acclaimed book, Street Freak: Money and Madness at Lehman Brothers, shows you how to pick and trade trends, and master your inner instincts. Learn how to use “Angry Analytics” as a leading indicator of budding trends you can profit from… and how to view any market situation through the lens of a trader. Jared’s keen insight into market psychology combined with an edgy, provocative voice make Street Freak an investment advisory like no other. Follow Jared on Twitter at @dailydirtnap.

Most FOMC folks keep telling us that economic conditions are strong enough to warrant a December hike. What gives? Two possible explanations for the strength in bonds. First, the feedback loop between the Fed and the US$ is such that a significant tightening in monetary conditions is already at play and could impair US growth in H1/16. Second, the Fed is at the mercy of the ECB. The Fed is well aware of the US$ drag on growth but Mr. Draghi will be on stage first next week, while he keeps hinting at more policy stimulus. This is driving foreign investors to buy US$ bonds. Next week is a key week. Further US$ strength once the ECB has delivered could be upsetting. Stay tuned!

Today’s the big day…

Today’s the big day…

Mario “whatever it takes” Draghi is expected to goose up stock markets with more stimulus measures.

On the table is more QE… and further cuts to the key lending rate.

The Chinese feds are also supposed to come forward with another gift to asset holders.

According to the Wall Street Journal, the expectation is for something targeting property purchases and another interest rate cut (which would make it cut No. 7 since last November).

And yesterday, Fed chair Janet Yellen told the Economic Club of Washington:

|

In Europe, Asia, and America, central bankers, we are told, have the situation in hand.

Fools or Knaves?

But these policies – in fact ALL central bank policies for the last 30 years – are either a mistake or flimflam.

…they are perpetrated by either fools or knaves… depending on how you look at it.

…and they are either an intentional transfer of wealth from the people who earned it to the world’s elite insiders. Or the transfer of wealth is an unintended consequence of botched policy.

We lean toward the larceny explanation.

QE may have been a mistake when it was first tried by Japan 20 years ago. But after so many years of trial and error, we now know how it works: It takes wealth from some people (mostly middle-class savers) and gives it to others (mostly wealthy speculators).

This is a problem. Because we know from both theory and experience that trying to rob the rich to make the poor better off doesn’t work. The rich duck and dodge. And the poor lose the incentive to make it on their own.

Now, we’re discovering that the opposite approach doesn’t work either. You can’t rob the poor, give to the rich, and expect the economy to improve.

Already, the European Central Bank’s key lending rate is MINUS 0.2%. We have been amazed and befuddled by these negative rates for a long time. They suggest an impossibility: That the value of money is less than nothing. And if that is so, the value of everything money buys – including labor – must also be less than zero…

…which is such a strange and preposterous thought that it can’t be correct.

But after a few nights of light meditation and heavy drinking – aided by insights from Charles Gave, the chairman of Gavekal Research – we think we have a better understanding of it.

An Affront to Nature

First, says Charles, negative rates are an affront to nature… and an insult to the gods.

Money today is inherently worth more than the same amount of money a year from now. Because something could happen in the intervening period. Someone else could buy the house you wanted. The borrower might die and not pay you back. Or you might die, without ever seeing your money again.

That’s why lenders need to be paid for the risk that something will go wrong…

Meanwhile, the Old Testament tells us that God chased Adam and Eve from the Garden of Eden, with this curse: From now on, “you will earn your bread from the sweat of your brow.”

But the goal of central bank demand management is to upset God’s applecart. The feds want people to consume their bread before they even put on their work gloves.

In the long run, this clearly won’t work. Spending credit is essentially spending someone else’s money. And sooner or later you will run out of other people’s money.

Lord Keynes – from whom the feds draw inspiration – said not to worry. In the long run, he said, we’re all dead anyway.

Keynes is dead. And we are in the long run now.

Regards,

Bill

Further Reading: Bill says that spending credit is spending someone else’s money… and sooner or later you will run out. In his latest investor presentation, Bill reveals the frightening truth of what will happen when the feds finally do run out of other people’s money to spend. It’s going to happen sooner than you think… and the consequences will be worse than anything the world has ever seen. Watch Bill’s warning now.

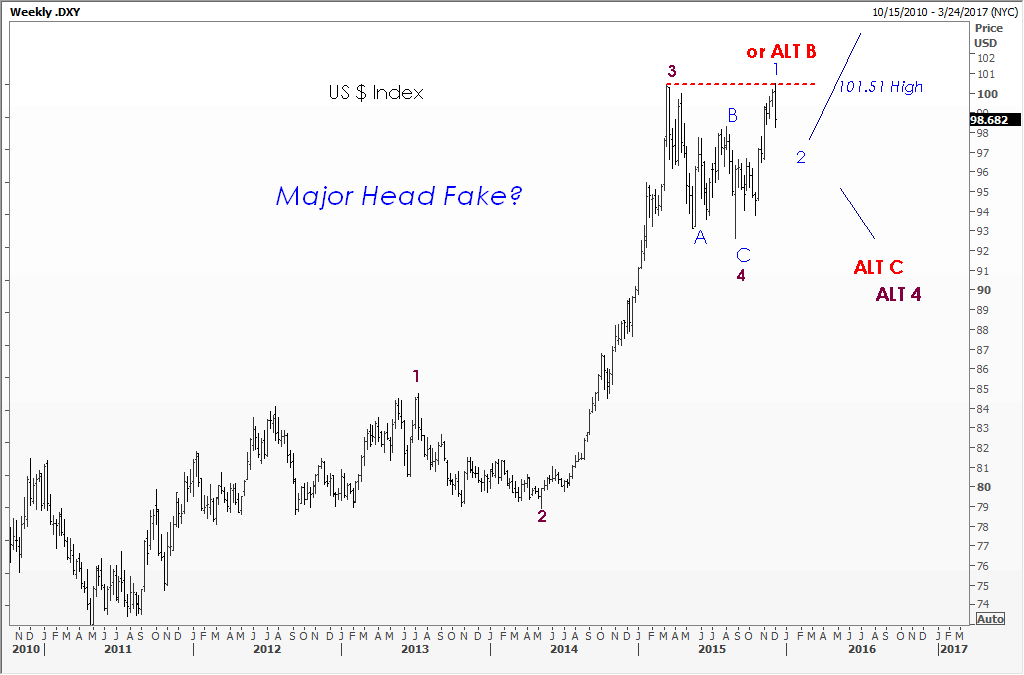

A bunch of dollar bulls, euro bears, have been hammered so far today (time left of course). Did we just see a major head fake from Mr. Market? There were a lot of one-way bets…Is the price action also telling us Fed Chairman Yellen will disappoint in some way? I guess we shouldn’t try to get cute with that stuff and stick to our knitting which, in a sentence is this: Trade what the market gives us and don’t try to forecast price action based on fundamental events.

That said, I have shown an alternative setup in this chart showing the potential for a correction lower in the dollar, back toward 92.00 [about 7% which is big when calculated in pips]…

Regards,

Jack Crooks

Black Swan Capital

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair