Gold & Precious Metals

Like a rock tumbling down hill, oil prices have broken 40 dollars per barrel and sustained their downward momentum. Bearish reports ranging from the outcome of the OPEC meeting in Vienna over a week ago to supply outlooks from the International Energy Agency continue to weigh on the global crude market and have further dampening effects on global financial markets. Particularly equity markets look troubled with the notion of a diminishing global growth picture, and the prospects of a global recession come 2016. Not just limited to the aforementioned reasons, but markets remain on a jittery footing heading into the Fed meeting this week. It is remarkable how much can change in one short week as market participants exhibit signs of discontent with what’s in the pipe for the year ahead.

Like a rock tumbling down hill, oil prices have broken 40 dollars per barrel and sustained their downward momentum. Bearish reports ranging from the outcome of the OPEC meeting in Vienna over a week ago to supply outlooks from the International Energy Agency continue to weigh on the global crude market and have further dampening effects on global financial markets. Particularly equity markets look troubled with the notion of a diminishing global growth picture, and the prospects of a global recession come 2016. Not just limited to the aforementioned reasons, but markets remain on a jittery footing heading into the Fed meeting this week. It is remarkable how much can change in one short week as market participants exhibit signs of discontent with what’s in the pipe for the year ahead.

The greater probability though is not so much a fear for how North American markets will react to Fed actions next week, but instead what will result in the world’s emerging markets. South Africa reminded us this week that there are greater fears for emerging market (EM) investors than simply the price of the US dollar and commodity markets. Simply put, the commodity markets slump has put downward pressure on some of the world’s EM’s as returns are depleted and pressure mounts on government revenues. A strong US dollar also inflates the burden of US dollar denominated debt many of the countries and residing corporations have issued to finance themselves. But with the pressure of inflated interest payments and depleted revenues comes political risk.

With South Africa as the example, the Treasury and the Central Bank have long been viewed as stable and independent institutions. The benefit of an independent treasury is that it is an added pressure to government to restrain their finances and keep government debt in check. This all changed for the Republic of South Africa this week when the President Jacob Zuma fired his finance minister and replaced him with an unknown party insider. The Economist Magazine actually cited a spike in Google searches of the man’s name as people were unfamiliar with who would be taking the helm of the country’s finances. As the fear is this was a politically motivated decision, the rand, South Africa’s currency, in a swift reaction sold off 5 per cent against the US dollar despite sitting on multi year lows.

This is a critical time for emerging market economies. Also, given the demand from EM’s for precious metals, it has direct implications for the gold market. At the beginning of December Fitch Rating Agency downgraded South Africa’s debt to one notch above junk status. This is as Debt-to-GDP rose from 2009 until present time from under 30 per cent to just above 45 per cent. Political risks, whether from South Africa or any other nation, become more prevalent for investors and can change the dynamic of global markets.

This will likely reinforce a theme for the beginning of 2016 that the dollar, if not for investment opportunity in US markets, will be attractive for its safe haven and even more so liquidity status. It’s a challenge for commodity markets to counter trend a strong US dollar and as long as the outlook for EM’s is bleak, a strong dollar may persist. The global economy will be challenged in 2016, and objectively, remains one of the bearish factors weighing on the gold market.

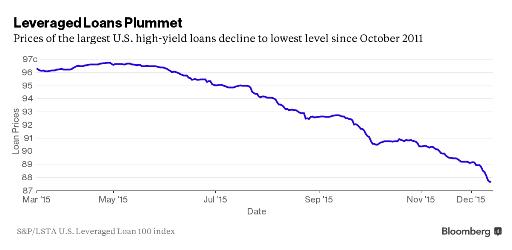

With junk bonds finally reverting to their intrinsic value, the question on everyone’s mind is “what blows up next?” Here’s the first in what might be a long, painful list:

CLOs Hammered as Energy Rout Plays Havoc With Other Markets

(Bloomberg) – The bust in commodities that’s roiling junk bonds is also taking its toll on funds that bundle corporate loans used to finance buyouts.

The riskiest slices of collateralized loan obligations raised after the financial crisis plunged 9 cents on the dollar since September to about 58 cents at the end of last month, down from 84 cents a year ago, according to JPMorgan Chase & Co. Intensifying price declines in recent months have led to one of the “more challenging years in recent memory,” JPMorgan analysts Rishad Ahluwalia and Jacob Kurosaki wrote in a Dec. 11 note to clients.

The massive bubble in US dollars is so obvious in this country

When I did the math in my head last week, I had to pull out my phone’s calculator just to make sure I hadn’t mentally misplaced the decimal point.

When I did the math in my head last week, I had to pull out my phone’s calculator just to make sure I hadn’t mentally misplaced the decimal point.

It turns out I was right. My rental car in Cape Town would cost me just $8/day. And that included all the silly taxes and fees and nonsense.

Eight bucks. I imagine that the car depreciates more than that.

The rest of my time here has been filled with similar awe.

Dinner for two at a high-class restaurant along the oceanfront promenade in one of Cape Town’s most luxurious neighborhoods set me back about $30.

And that included wine, multiple courses, taxes, tip, the whole nine yards.

Nearly everywhere I see here is shockingly cheap… when I convert to dollars.

Grocery stores sell giant bags of food—fresh plums and peaches, for less than a dollar per kilo, or about 40 cents per pound.

And of course, one of the reasons I came here to begin with is because Round-the-World flights starting in South Africa are dirt-cheap.

My itinerary has me traveling from here to Australia, Asia, South America, the US, Europe, and back to South Africa, all for about $5,500. In business class.

A deal like that is absolutely unheard of. And it all comes down to the local currency, the South African rand.

It wasn’t that long ago that the rand was valued at about 8 per dollar. I remember coming here not too long ago when the rand was 6.

Today it takes more than 15 rand to buy a single US dollar– record low territory for the South African currency.

And just last week, the rand lost more than 10% against the dollar.

In currency markets where price swings of 1% to 2% are considered chaotic, a 10% drop in a currency’s value is practically apocalyptic.

This makes South Africa one of the cheapest countries in the world right now, if you’re spending in US dollars.

What’s crazy is that South Africa is not alone. Currencies around the world are trading near record lows.

Colombia. Mexico. Kazakhstan. Nigeria. Indonesia. Turkey. Chile. Brazil. Sri Lanka. Iran.

This strikes me as truly bizarre. It’s not like the economic fundamentals of the United States, and the fundamentals backing the US dollar, are particularly strong.

The US dollar is issued by the Federal Reserve, a central bank that is nearly insolvent according to its own balance sheet.

And of course, the US economy is so ‘strong’ that the Fed has been agonizing for a year whether America is ‘ready’ for a 0.25% interest rate increase this week.

Moreover, the US government is in debt up to its eyeballs and also insolvent according to its own financial statements.

America’s national debt, in fact, exploded by $674 billion just last month. This is nearly twice the size of South Africa’s entire economy!

It’s pure madness to think that this is the ‘strong’ economy.

It makes no sense that a Big Mac costs $4.79 in the US, but the exact same Big Mac costs $1.60 in South Africa.

Or that a round-the-world ticket costs $14,000 in the US, but the exact same itinerary ticketed from South Africa costs only $5,500.

The US dollar is clearly in a massive bubble, while the rand is extremely undervalued.

And while it could take time, modern financial history shows this imbalance does tend to correct itself.

This does present a compelling opportunity right now to buy high quality assets overseas for next to nothing.

Or at a minimum, to enjoy an incredible lifestyle for a fraction of the cost, or to explore the world on a shoestring.

We have that ability today.

This valley where I spent the weekend about an hour from Cape Town was the destination of choice for French Huguenots who fled religious persecution.

When they came from France in the 1600s, they had to brave a treacherous journey across the world, risking disease, starvation, and pirates.

And that was just to get here.

Once they arrived they had nothing. Yet they built a brand new civilization from scratch, bringing with them all the best elements of their culture.

Just like in North American and Australia, early settlers realized that life wasn’t going to improve back home. And if they wanted access to better opportunities, they had to take big risks and look abroad.

Today we have it so much easier.

We can hop on an airplane and wake up on the other side of the world tomorrow morning.

We can access incredible financial opportunities and profit from the next great financial bubble, all without leaving our living rooms.

Despite all the idiots out there trying to start World War III, the world really is full of opportunity.

Whether you’re seeking a better, higher quality lifestyle at a fraction of the cost, or financial opportunities to make more money, it’s all out there.

And with much greater ease than our ancestors dreamed of. All it takes is the willingness to learn… and to take action.

Until tomorrow,

Simon Black

Founder, SovereignMan.com

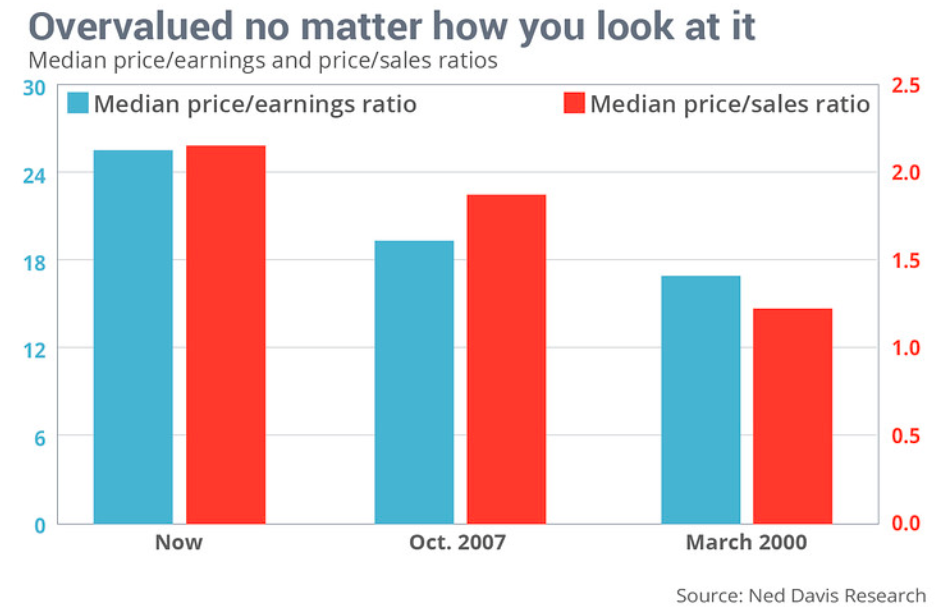

Currently, stocks are extremely overvalued by multiple methods.

- The first way is by looking at Cyclically Adjusted P/E Ratios commonly known as CAPE, Shiller P/E, or P/E 10 ratio.

- The second is by looking at median P/E and P/S (Price to Sales) measures

We will look at both, but here’s a description of CAPE.

CAPE is a valuation measure applied to stock market indexes. It’s defined as price divided by the average of ten years of earnings (Moving average), adjusted for inflation. The essential idea is earnings are mean-reverting making forward looking earnings frequently too optimistic, and current PEs too high following steep corrections.

Société Générale SA’s (EPA: GLE) (SocGen) recent quarterly Global Economic Outlook proposes a number of potential “black swan”-type events, how likely these are to occur and what kinds of effects they may have on the global economy.

Société Générale SA’s (EPA: GLE) (SocGen) recent quarterly Global Economic Outlook proposes a number of potential “black swan”-type events, how likely these are to occur and what kinds of effects they may have on the global economy.

Interestingly, SocGen sees more downside risks than possible upside surprises.

A look at SocGen’s forecasting and analysis of the risks, rewards, and possible impacts:

How to Safely Get Your Money Through Everything the Market Will Throw at You in 2016

Most of the time, when pundits say “black swan,” they really mean “a disruptive event that no one saw coming – much less had any idea how to deal with.”

So they’re manageable, but they can still be downright dangerous to your money. That means a broad perspective, a willingness to entertain all the possibilities, and robust asset protection strategies – like the ones I’m about to show you – go a long way in helping you avoid these events.

The best part is, you can even make some nice money while everyone else loses their shirt…

This Can Be a Very Profitable Exercise

Laying some of the groundwork for this exercise is Société Générale SA’s (EPA: GLE) (SocGen) recent quarterly Global Economic Outlook.

In this report, the international French bank proposes a number of potential “black swan”-type events, and then provides some detail on their thinking about how likely these are to occur and what kinds of effects they may have on the global economy.

Interestingly, SocGen sees more downside risks than possible upside surprises. That’s an outlook I’d have to agree on.

Let’s look at SocGen’s forecasting and analyze the risks, rewards, and possible impacts.

First, the disruptors…

SocGen Disruptors

No. 1. A “Brexit” (British Exit) from the European Union: 45%

From SocGen: The United Kingdom’s Prime Minister Cameron is likely to hold a referendum on whether the UK should exit the European Union. That’s likely to take place late next year. Expected impact: Low.

Now, the UK is part of the EU and already wields a fair degree of independence via its own pound sterling currency. With all the problems Greece has faced, it’s still part of the EU. So I don’t see the UK going anywhere, just negotiating a better deal. I peg the probability of a Brexit at 10%.

No. 2. A Hard Landing for China: 40%

From SocGen: Expect a 40% risk of seeing a lost decade scenario instead in the medium term. Risk of hard landing comes from credit crunch due to intensified capital outflows, bad loans, lack of central bank stimulus; failing housing demand could see developers fail, cutting development; capacity overhang means manufacturing could keep suffering, leading to bankruptcies and unemployment.

I believe China’s administration realizes the magnitude of the challenge in transitioning to a consumer economy. It’s likely to use its massive reserves and to stimulate through quantitative easing (QE) and lowering rates to ensure the smoothest transition possible, as not doing so carries huge risks to stability. I see the probability of a hard landing at 20%.

No. 3. The American Consumer Saves More: 25%

Hey, I guess it could happen, but with such low oil/gasoline prices, consumers are already saving more by default. I think the risk of more saving is closer to 15%. It’s sad to see that SocGen considers saving more to be a negative, too.

No. 4. A New Global Recession: 10%

Here I think SocGen has totally underestimated the odds. I believe they’re likely much closer to about 35%. But don’t forget – there would almost certainly be a worldwide coordinated mega-QE program to combat this.

No. 5. The Fed Hikes Rates Too Late: 10%

Is SocGen kidding? It’s already too late. So, I’d have to peg this at 100% probability, if that’s possible. But better late than never, I guess. Anyways, a rate hike is highly likely this month, so the next issue will be the size of the hike, then follow-through with subsequent hikes, their size and frequency. Of course, Yellen’s measured pace means don’t expect too much too fast.

Now, it has to be said that 2016 holds the possibility of a few positive surprises, too, though not as many as we’d like. These actually have the potential to improve the global economic outlook – and line our pockets, if we’re properly prepared.

SocGen “Upside Surprise”

No. 1. Stronger Investment and Trade: 20%

I’d agree there’s about a 20% probability of this, what with all the QE, ultra-low rates, and other massive stimulus that’s already taken place. This would help boost economic activity somewhat.

No. 2. More Fiscal Accommodation: 15%

Again… Hah! Fiscal accommodation has never ended even, unarguably, in the United States, where rates are still abnormally low. And consumer and government debt are dangerously high, so rates have to stay low. At this point, though, the effect is probably neutral, since economic activity is still too low to encourage any significant new borrowing.

No. 3. Fast-Track Reform: 10%

This is pretty laughable, too. Structural reforms are the right thing to do, so naturally they’re just about the last thing on central planners’ minds. Reforms have proven effective, but also painful and politically suicidal. My take? Zero percent probability. It’s not gonna happen.

How to Prepare for These Outcomes

Given all of these points and the fact that, by definition, there are black swans circling that we simply can’t even imagine (like Donald Rumsfeld’s “unknown unknowns”), the risk of exiting a state of relative complacency and hitting up against marked volatility is going to increase in 2016.

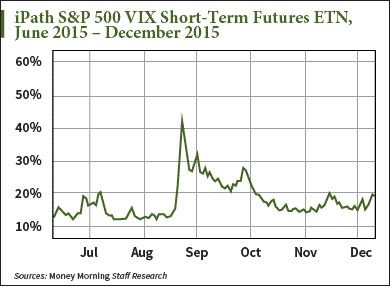

The Chicago Board of Options Exchange Volatility Index (VIX) was relatively calm over the last couple of months, but episodes of extreme spiking, like the flash sell-off we saw in August, are probably coming back – perhaps even with a vengeance – as the market tries to place odds on the pace of future Fed rate hikes and other unknowns, if any.

So one hedging idea might be to buy the iPath S&P 500 VIX Short-Term Futures TM ETN (NYSE Arca: VXX), but I’d only recommend holding this over a relatively short period of weeks to one or two months as insurance.

So one hedging idea might be to buy the iPath S&P 500 VIX Short-Term Futures TM ETN (NYSE Arca: VXX), but I’d only recommend holding this over a relatively short period of weeks to one or two months as insurance.

And don’t underestimate the value of cash as a longer-term hedge. But with the recent weakness in the U.S. Dollar Index telegraphing a possible end to its 18-month rise, consider a mix of normally stable currencies.

For example, I’d expect to see first and foremost the U.S. dollar, British pound sterling, and Swiss franc, but also the Canadian and Australian dollars, and now even the Chinese yuan all benefit from safe-haven attraction.

And thanks to exchange-traded funds (ETFs), you can easily gain exposure to any and all of these currencies with but a few keystrokes in your online brokerage account.

Here are the ETFs and their pertinent details:

- U.S. Dollar: PowerShares DB U.S. Dollar Index Bullish (NYSE Arca: UUP) ETF. As the world’s reserve currency, the U.S. dollar should be part of your cash mix.

- British Pound: Guggenheim CurrencyShares British (NYSE Arca: FXB) ETF. As part of the EU but not the currency union, the pound is a natural haven for Europeans.

- Swiss Franc: CurrencyShares Swiss (NYSE Arca: FXF) ETF. Long seen as a neutral haven within Europe yet remaining outside the EU, and after having dropped its peg to the euro in January, the franc is pricier but still attractive for safety.

- Canadian Dollar: Guggenheim CurrencyShares Canadian (NYSE Arca: FXC) ETF. Being neighbor to the United States and after a considerable decline along with oil over several months, the loonie looks like a fantastic bargain right now.

- Australian Dollar: Guggenheim CurrencyShares Australian (NYSE Arca: FXA) With a relatively strong economy and also viewed as a commodity currency, the Aussie dollar is attractive, especially with FXA yielding 1.6%.

- Chinese Yuan: WisdomTree Dreyfus Chinse Yuan Fd (NYSE Arca: CYB) ETF. As the dominant power in Asia (and way beyond) and a soft peg to the greenback, China’s currency is another haven of sorts. CYB has $112 million in assets and trades 22,000 shares daily.

Don’t discount the importance of cash in your portfolio, and that means seeking diversification even within this most basic of allocations.

Remember, even if we can’t actually predict black swans, that doesn’t mean we can’t protect against them.

Cash may not be exciting, but it sure feels good when everything’s going to hell in a handbasket.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair