Economic Outlook

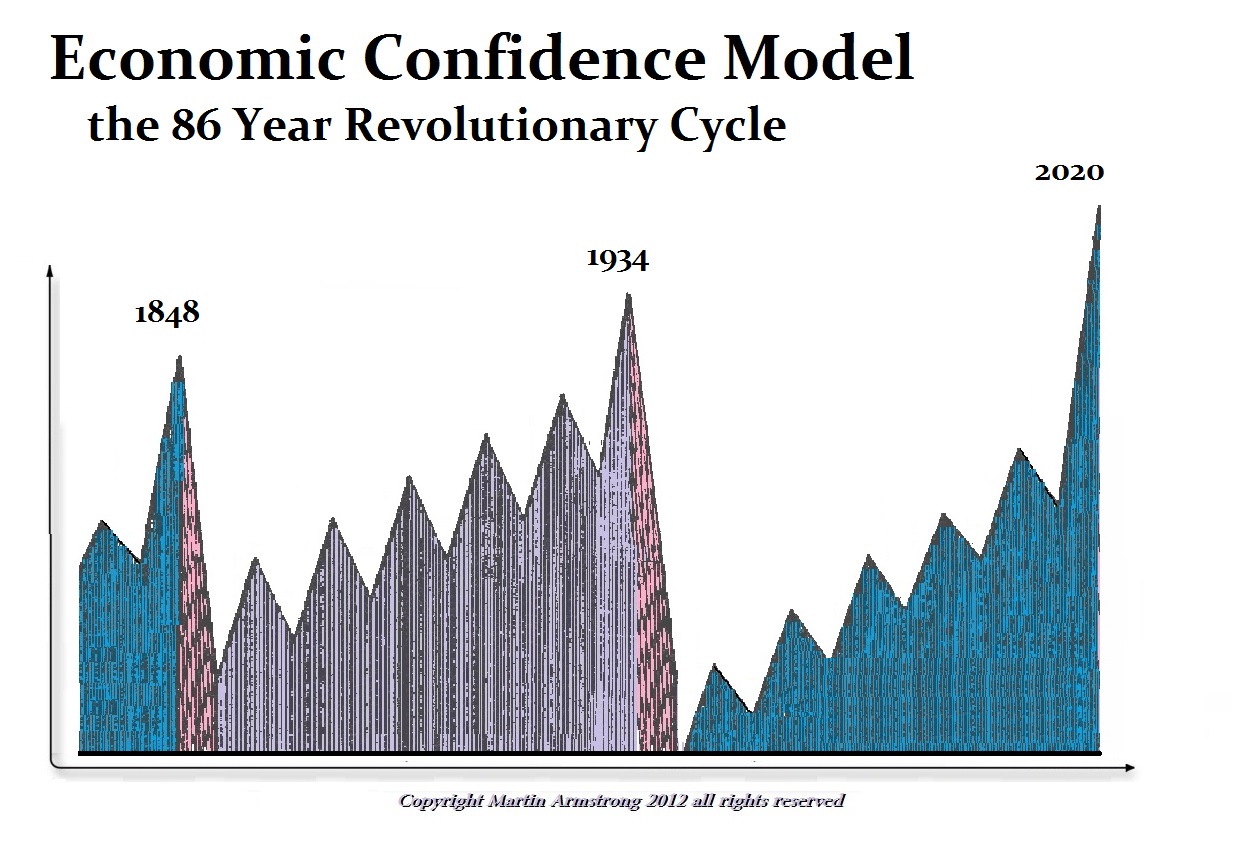

I have warned that 2017 will be the political year from hell. What I am illustrating here is the link between a sovereign debt crisis and the Revolutionary Cycle. In 1933, Roosevelt came to power in the USA and turned the country toward socialism. That same year, 1933, brought Hitler and Mao to power. So 1934 was the revolutionary year. Such revolutions do not always bring blood in the streets. The next one is due in 2020 and we should see the system we currently live under go completely upside-down.

The movie “The Big Short” features Michael Burry. His statement from Zerohedge:

The movie “The Big Short” features Michael Burry. His statement from Zerohedge:

“It seems the world is headed toward negative real interest rates on a global scale. This is toxic. Interest rates are used to price risk, and so in the current environment, the risk pricing mechanism is broken.”

Repeat: “THE RISK PRICING MECHANISM IS BROKEN.”

What risks could be mispriced? A few come to mind.

- The world is saturated in debt – over $200 Trillion. Does anyone expect that debt to be repaid? What are the risks when over $200 Trillion in debt can be counted as an asset ONLY if that massive and increasing debt can be rolled over and replaced with say $300 Trillion in debt? What are the risks this exponentially increasing debt nonsense will be acknowledged for what it is – a train wreck in progress?

- The US stock market looks like it is rolling over, just as it did 7+ years ago in 2008, and 15 years ago in 2000, and 1994, and 1987. What are the risks that the S&P 500 is overvalued, that the P/E and a dozen other measures are overvalued, and the stock market will correct/crash? Think back to 2008, 2000, 1994, and 1987. Read: Tread Lightly – 2016 Technical Outlook.

- People and countries in the Middle East are not playing nice with each other. Regardless of whether the problems are religious, a 2,000 year feud, outside interference, control over gas and oil pipelines, or foreign policy stupidity, the region appears ripe for turmoil and more violence. Have risks been properly assessed? What happens if WWIII is born out of the fires of Middle East hatred, energy markets, and political posturing? Has that risk been properly priced into bond markets with negative yields, or stock markets with historically high P/E ratios, or crude oil prices at multi-year lows?

- Silver (paper) prices have been crushed by nearly five years of paper selling, derivatives, central bank manipulations, support for stock and bond markets, and more. Have the risks of financial turmoil, economic catastrophe, and escalating war been properly priced into paper COMEX silver prices?

- Actual physical gold has left the vaults in the western world and moved east into private and public vaults in Russia, India, and China. Have the risks of paper gold defaults (cash settlement) been priced into the COMEX paper price of gold? What if much of the gold supposedly vaulted in London, New York, and Fort Knox has mysteriously been replaced by “IOU gold” paper promises? Have the risks of missing gold and increasing demand for real physical gold been properly priced into the paper gold market?

- What is the risk of nuclear confrontation between Russia and the US? If we believe the bond markets, the risk is exceptionally low, since the prices of money (interest rates), are at multi-decade or perhaps multi-century lows. Have the risks of major war, or nuclear war, been mispriced in the bond market?

But looking on the silly side of a broken risk pricing mechanism … (SARCASM ALERT)

- Wall Street financial firms are doing “God’s Work” here on earth and will take care of the rest of us.

- Social Security recipients will receive no cost of living increase in 2016 because, per the Social Security Administration, “The law does not permit an increase in benefits when there is no increase in the cost of living.” Good to know there has been no increase in the cost of living during 2015! Apparently the Obamacare price INCREASES in premiums and deductibles compensated for other price increases…. (reminder – sarcasm alert).

- The Presidential race is heating up, but good things might happen in a single party political system masquerading as a two party process. Vote for the least offensive candidate and tell yourself there is a difference, not in the candidates, but in the policies that will be implemented.

- But don’t worry, be happy, trust debt based fiat currencies with no intrinsic value, and spend, spend, spend, because “deficits don’t matter.” Frankly, what could go wrong? Remember – sarcasm alert!

Silver thrives, paper dies! That mantra will serve us well in 2016 and 2017 since paper silver prices are currently very low compared to ratios to the US national debt, the S&P 500 Index, total global debt, fiscal and monetary silliness, and political stupidity (graphs not shown). If risk has been mispriced because the “risk pricing mechanism is broken” as Michael Burry says, then we should expect a volatile and traumatic year in 2016 as risk pricing adjusts.

Rig for stormy weather, expect surprises, markets regressing to the mean, pricing mechanisms failing, political systems collapsing, and Middle-East politics exploding. There will be blood and trauma. Do not trust the supposed value of paper assets and find security in real assets such as silver and gold bars and coins stored outside the financial system.

Silver thrives, paper dies!

Gary Christenson

The Deviant Investor

While there is no doubt that access to growth capital is the fuel that grows a business, there is an alternative method to access capital and postpone an external financing round completely. For later stage companies, I strongly believe in an intense focus on the cash flow aspects of your business to raise internal capital first, before going to the outside. At a minimum, this approach can postpone an external financing, freeing up time and resources to grow the business; at a maximum, this approach may negate the need to raise external capital altogether.

A good business leader will fully leverage these three critical areas before considering an external financing:

Maximizing Sales: While the technology may be the heart of your business, if you can`t sell it, you have a hobby or a science experiment, not a business. If you are the Founder or CEO, at least 50% of your time should be spent on sales, either lead generation, prospecting or with current customers. The entire company should be aligned and focused on the revenue, including: a rigorous sales funnel process, clear sales accountabilities, regular review of sales metrics and actions on how to improve, and flawless execution of the product or service delivery. Everyone should be eating, sleeping and breathing customer service and revenue.

Maximizing Gross Margins: Your gross margin will tell you, whether you are digging a financial hole to oblivion or a creating a mountain of cash to success. Only by having a precise and firm understanding of your gross margins, by product and customer segment, for today and the future, will you know whether you are competitive, have a sustainable business and are producing the capital for growth. Maximizing gross margins will occur when you constantly incorporate market feedback to improve your pricing, while simultaneously driving cost out of your product through product redesign and leveraging low cost technologies.

Working Capital: Your gross margin will tell you, whether you are digging a financial hole to oblivion or building a mountain of cash to success. For any later stage technology business, working capital should invested in areas that significantly leverage the scalability of the company, such as: stream lining business systems (sales, product delivery and product development), fulfilling high gross margin orders, and promising / proven new market channels. Watch A/R and A/P closely and assign one individual with responsibility for this area.

If your market is growing fast and external capital can get you there even faster, by all means get it! However, self-financing is a great option for many companies. While it may be difficult, requiring a focus on the customer (revenue) and a relentless dedication to execution, the payback is worth every ounce of effort.

For full Image (much longer) and analysis go HERE

In a Warren Buffett note from 2006, he credits the famous value investor Benjamin Graham as the co-creator of the first-ever hedge fund in the mid-1920s.

“It involved a partnership structure, a percentage-of-profits compensation arrangement for Ben as general partner, a number of limited partners and a variety of long and short positions,” Buffett’s letter says.

That means that hedge funds have been around for nearly a century – and they have almost exclusively existed as a vehicle for institutions and wealthy, private investors…..continue reading HERE

My parents were hard-working vegetable famers in western Washington, but making ends meet was always a struggle.

My parents were hard-working vegetable famers in western Washington, but making ends meet was always a struggle.

My classmates laughed at my hand-me-down clothes and logger boots with holes in the soles, but I never went to bed hungry and my mother kissed me goodnight every night until I left for college.

Farm work was hard and I hated it—I mean really hated it—at the time, but I now think that those years on the farm were the foundation of the success that I enjoy today.

Moreover, there’s a surprising number of investment lessons that I learned as the son of a farmer.

Boring Work Is the Most Important Work

Farming is far from glamorous, but some of the work was dreadfully boring.

In the spring, my father would have me pick rocks out of the fringes of the farm, and in the summer, I spent thousands of hours on my hands and knees pulling up weeds. It was boring and seemed meaningless at the time, but every successful business needs a strong foundation, and the basic building blocks of preparing the soil is crucial.

The same is true of investing. Reading annual reports, financial statements, and balance sheets can be boring, but it is that fundamental, time-consuming research that sets you up for long-term success.

Summer Profits Come from Winter Efforts

My non-farmer friends assumed farmers took it easy during the winter. Wrong! Even when snow covered the ground, my father still worked a minimum of 12 hours a day. There may not have been any crops to harvest in winter, but there was always plenty of off-season work to do on the farm, such as repairing the farm machinery and mending fences.

My high school basketball coach used to scream at us that December games are actually won during the off-season workouts, and the same is true of investing. You make your profits before you buy a stock; not after you sell it.

Core and Explore

The most important decision any farmer makes is what to plant. The price of vegetables could vary widely from year to year, and many farmers would play a Green Acres version of roulette by trying to anticipate what the “hot” vegetable of the year would be.

Not my father; he stuck to red radishes and green onions for roughly 80% of our farm and gambled with the last 20% of our land on what crops he thought could deliver big payoffs.

I do the same with my portfolio today; I keep the vast majority of my portfolio in stable, established blue-chip companies that pay generous dividends and use the last 20% or so for more speculative bets (including shorts and put options).

Profits, Not Revenues

What makes one farmer more successful than the other? Many of our neighboring farmers also grew radishes and onions, but what made my father more successful than others was that he knew it isn’t how much you harvest, but how much profit you make on what you do grow.

My father was a very frugal man, and he seldom bought anything if it wasn’t on sale, so his cost was lower than most of his competitors’.

I’m a cheapskate too, so I seldom buy stocks unless they go on sale. You’ve probably heard the warning, “Don’t try to catch falling knives.” Well, I love falling knives, and I think that I’m one of the best falling-knife catchers in the world, so you won’t see me buying stocks at 52-week highs.

Plow Under Your Mistakes

Sometimes things just went wrong on the farm. Insects would infest our crops, some months were too wet and triggered mold outbreaks, and some years frost would come too early or too late and damage the crops. Instead of spending too much time and/or too much money on rescuing the damaged crops, my father would often plow them under and start over.

My father was a big believer in cutting your losses and moving on. The same applies to investing, but I find that many investors are too stubborn to admit a mistake or want to wait until they “break even” before selling.

Expect Storms

Whether or not my father had a good year depended on three things: (1) no late frosts, (2) no early frosts, and (3) no natural disasters like hail storms, tornados, droughts, or massive insect infestations.

While you can’t avoid disasters, you can plan for them and run for cover when they do come. The wise investor diversifies in anticipation of those things that are beyond his control and buys insurance to protect against catastrophic losses.

If the stock market turns ugly (which I believe it will), how prepared is your portfolio for catastrophe? If you’re worried, you might want to check out my monthly newsletter, Rational Bear (try it for 3 months with money-back guarantee).

Tony Sagami![]()

30-year market expert Tony Sagami leads the Yield Shark and Rational Bear advisories at Mauldin Economics. To learn more about Yield Shark and how it helps you maximize dividend income, click here. To learn more about Rational Bear and how you can use it to benefit from falling stocks and sectors, click here.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair