Currency

In 1967 the Jefferson Airplane sang:

“When the truth is found to be lies,

And all the joy within you dies…”

Restating this for economies and global currencies, one might say:

When the truth is found to be lies,

When the truth is found to be lies,

Confidence in currency dies.

WHAT LIES? Really? There have been so many. Here are a few examples specific to the United States (the lies in other countries are probably similar):

Lyndon Johnson: In 1965, after decades of excessive government expenditures which caused rising consumer price inflation and rising gold and silver prices, Johnson removed silver from U.S. coins. He stated,

“If anybody has any idea of hoarding our silver coins, let me say this. Treasury has a lot of silver on hand, and it can be, and it will be used to keep the price of silver in line with its value in our present silver coin. There will be no profit in holding them out of circulation for the value of their silver content.”

He lied. One hundred dollars purchased 77 ounces of silver in 1965. A decade later $100 purchased 24 ounces of silver. Four decades later $100 purchased 13 ounces of silver. In 2025 $100 will probably purchase less than one ounce of silver.

Richard Nixon, the gold window, and Watergate: In 1971 President Nixon “temporarily” rescinded the agreement to convert US dollars submitted by foreign governments for gold. He stated,

“Let me lay to rest the bugaboo of what is called devaluation… But if you are among the overwhelming majority of Americans who buy American-made products in America, your dollar will be worth just as much tomorrow as it is today. The effect of this action, in other words, will be to stabilize the dollar.”

On Watergate: He stated:

“I had no prior knowledge of the Watergate operation.I took no part in, nor was I aware of, any subsequent efforts that may have been made to cover up Watergate.”

He lied regarding both topics. One thousand dollars purchased 24 ounces of gold in 1971. A decade later $1,000 purchased 2.2 ounces of gold. Four decades later $1,000 purchased 0.6 ounces of gold. In 2025 $1,000 will probably purchase about 0.1 ounces of gold.

Devaluing currencies are normal for our debt based fiat currency financial system. But, when leaders, especially Presidents, are caught in lies, the populace is more inclined to “wake up” and see the reality of corporate and banking control over government policies. Those lies weakened the narrative that the government is run by the people, for the people, and is beneficial to the people. A loss of confidence in leaders leads to a loss of confidence in the country, its institutions, and accelerates the decline of the currency.

When the truth is found to be lies,

Confidence in currency dies.

Political Lies:

- Kennedy Assassination: There were so many lies, cover-ups, and strange deaths that hundreds of books have been written on the subject.

- Lyndon Johnson and the Vietnam War: He escalated the Vietnam War based on the “Gulf of Tonkin Incident,” a story that was fabricated.

- Edward Kennedy’s role in Chappaquiddick: More of the same…

- Bill Clinton regarding Monica Lewinsky and other infidelities: “I did not have sexual relations with that woman.” The House impeached him for perjury but the Senate did not convict. Politics as usual…

- Hillary Clinton: Oh my, let’s not go there.

- President Obama regarding Obamacare: “If you like your health plan you can keep it.” Clearly not true … and confidence in the Presidency has decreased, for this and many other reasons.

WHAT IS THE POINT?

- Of course politicians lie to protect their re-elections, reputations, positions, assets, and cronies. If politics did not “pay” so well, we would seldom hear about politicians, their lies, and the corruption, which will continue.

- Of course central bankers and Wall Street “manage” the narrative. They have $trillions to protect and they want their skim from the economy to continue. Not likely to change …

- Of course politicians and central bankers will distract the populace with “free stuff” rather than adult discussion. Politicians and central bankers will not discuss massive and unpayable debts, higher taxes, decreased military spending, reduced entitlements, and pervasive corruption. One does not get elected by telling voters they will have less and their “sacred cows” must be sacrificed to benefit the military and banking interests. Expect more promises, distractions, scandals, and a higher cost of living.

But we can change our understanding of the process and our actions to protect ourselves.

- If the President’s actions are largely dictated by corporate, banking, and military interests, does it really matter who is elected? Of course it matters to those on the receiving end of the money distributed by the government. Otherwise politicians and corporations would not spend $ billions to purchase the Presidency.

- The US dollar has lost approximately 98% of its purchasing power since 1913, and the dollar will continue to weaken, not strengthen, following more devaluations and lies (and we will have more lies). Given the necessity of devaluation and the ongoing lies, we should expect a much weaker dollar during the next decade. Would gold, silver, diamonds, hard assets, land, and fine art be preferable to unbacked paper currencies or bonds yielding negative interest rates?

- Hemmingway: “The first panacea for a mismanaged nation is inflation of the currency; the second is war. Both bring a temporary prosperity; both bring a permanent ruin.”

Our former Presidents have warned us by obviously lying about the dollar, gold, silver, health care, sexual indiscretions, unemployment, inflation, and wars. More revelations are coming …

When the truth is found to be lies, Confidence in currency dies.

Gary Christenson

The Deviant Investor

Related: What Gold Does In A Currency Crisis Canadian Edition

Consensus Forming: China Heading Back Into Financial Crisis

China’s historic post-2009 debt binge flew largely under the radar — fooling most observers into thinking the global economy was recovering rather than just re-leveraging.

Now Beijing is back at it, borrowing over $1 trillion in this year’s first quarter, buying up commodities and creating the illusion of global growth. But this time the scam hasn’t gone unnoticed. Reporters, editors and money managers seem, at last, to be catching on. Some representative headlines:

George Soros warns of credit crisis in China

Chinese cities dive back into debt to fuel growth even as defaults rise

China debt climbs to US$25 trillion

China’s banks cut bad debt buffer as profits flatline

Doug Noland, meanwhile, goes to the heart of the problem in last night’s Credit Bubble Bulletin:

I recall an early-1998 Financial Times article highlighting the explosive growth in Russian ruble and bond derivatives. Not only had the “insurance” market for risk protection grown phenomenally, Russian banks had become major operators in what had evolved into a huge speculative Bubble in Russian debt exposures. That was never going to end well.

There was ample evidence suggesting Russia was a house of cards. Yet underpinning this Bubble was the market perception that the West would not allow a Russian collapse. With such faith and the accompanying explosion in speculative trading, leverage and a resulting massive derivatives overhang, any break in confidence would lead to illiquidity, panic and a devastating bust. Just such an outcome unfolded in August/September 1998.

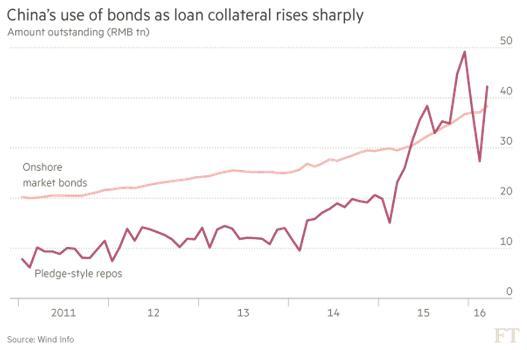

From a recent Financial Times article: “The [Chinese] market for pledge-style repos — short-term, bond-backed loans — is currently bigger than the stock of outstanding debt”. Within this undramatic sentence exists the potential for a rather dramatic global financial crisis. And, to be sure, seemingly the entire world has operated under the assumption that Chinese officials (and global policymakers in general) have zero tolerance for crisis – let alone a collapse. So Credit, speculation and leverage have been accommodated – and they combined to run absolute roughshod.

The Financial Times article includes a chart worthy of color printing and thumbtacking to the wall: “China’s Use of Bonds as Loan Collateral Rises Sharply”. The pink line shows “Onshore Market Bonds” having almost doubled since mid-2011 to about 40 TN rmb ($6.17 TN). The Red Line – “Pledge-Style Repos” – has ballooned four-fold since just early 2014 to surpass 40 TN rmb. So basically, in this popular market for inter-bank borrowings, borrowing banks have pledged bond positions larger than the entire market as collateral for their (perceived safe) short-term borrowing needs.

China has an historic Credit problem. It as well suffers from an unfolding “money” fiasco of epic proportions. My analytical framework attempts to differentiate the two, as each comes with its own set of (related) issues. A Credit Bubble is a self-reinforcing but inevitably unsustainable expansion of debt. Money (the contemporary variety) is a financial claim perceived as a safe and liquid “store of nominal value.” Importantly, systemic risk expands exponentially when risky borrowings are financed by an expansion of “money-like” instruments/financial claims. This typically occurs late (“terminal phase”) in the Credit Bubble Cycle.

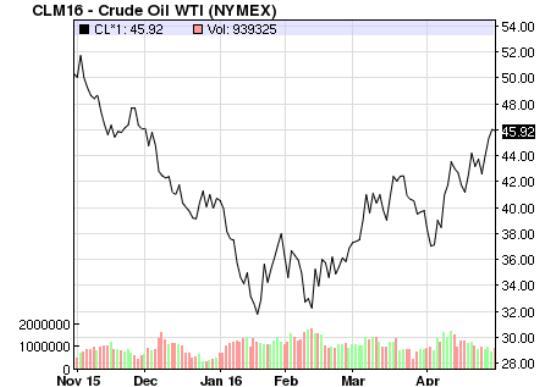

If the critics of China’s recent let-it-all-hang-out financial excess are right, a crisis of some sort is coming to a market near you. For instance, a fair bit of that Q1 $1 trillion went to boosting Chinese stockpiles — and therefore the price of — oil…

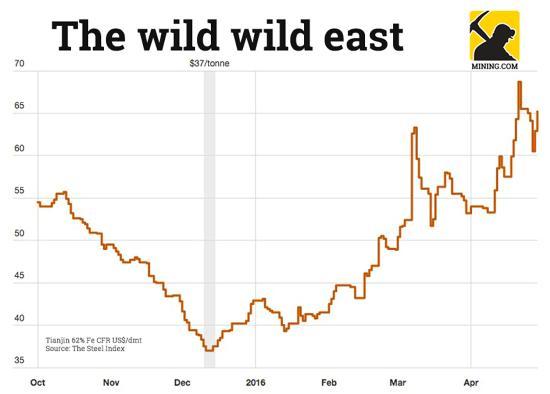

…and other commodities like iron ore. From More iron ore price madness as China’s mom-and-pops pile in:

On Friday the Northern China benchmark iron ore price jumped to $65.20 per dry metric tonne (62% Fe CFR Tianjin port) bringing gains since Wednesday to 7.8% as commodity investment fever grips Chinese investors. Last week iron ore hit a 16-month high following an 11% jump over just two trading days according to data supplied by The Steel Index.

The steelmaking raw material has enjoyed a 52% rise in 2016 and a 76%-plus recovery from nine-year lows reached mid-December. On the Dalian Commodities Exchange the price swings are much wilder.

Despite a clampdown on rogue traders, higher margin requirements and trading fees, circuit breakers on Dalian iron ore futures to curb excessive price movement were triggered for the umpteenth time on Friday. That’s despite the exchange in northeast China “temporarily” upping the daily price change limit to 6%. The most traded contract ended Friday at its highs, exchanging hands for 462 yuan or $71.40 a tonne, duly up 5.97% on the day.

Based on supply/demand fundamentals, oil and iron ore remain in massive gluts. So when China’s stockpiling ends — as it mathematically must — these markets will lose a lot of their exuberance. The question then becomes, how many speculators will default on their loans, and what kind of banking trouble will ensue? That’s unknowable, but it’s safe to assume, given the numbers involved, that the rest of the world will find it distressing.

So think of today’s relative calm as the eye of yet another storm, and what’s coming as a return to the hyper-leveraged new normal.

Mark Leibovit, the man who called the massive rally in the Cannabis stocks long before it happened, tells Michael Campbell the opportunities are “fabulous” with pending legislation in the US, and the Canadian Federal Government rolling out plans for decriminalizing marijuana. With nearly unprecedented demand pending, Mark enlightens us on who are all the players are from suppliers, distributors, retailers and regulators.

Mark Leibovit, the man who called the massive rally in the Cannabis stocks long before it happened, tells Michael Campbell the opportunities are “fabulous” with pending legislation in the US, and the Canadian Federal Government rolling out plans for decriminalizing marijuana. With nearly unprecedented demand pending, Mark enlightens us on who are all the players are from suppliers, distributors, retailers and regulators.

Mark also updates his very popular Annual Model Forecast as well as gives his forecasts on Silver and the US Dollar.

{mp3}grant/043016y{/mp3}

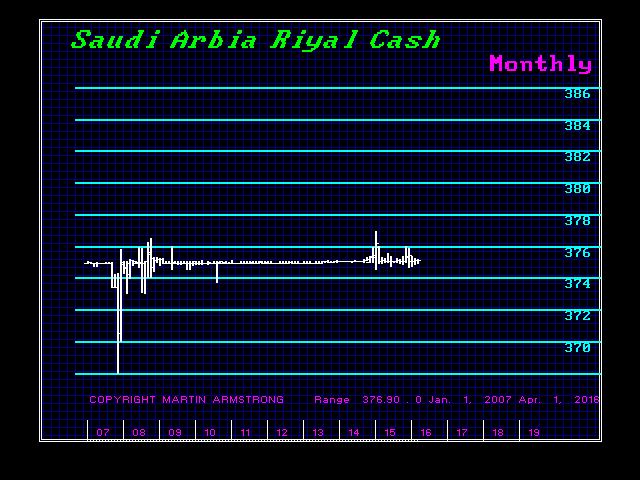

There is serious trouble brewing in Saudi Arabia. They have been dumping oil increasing their output by 3.5%. However, the cash is being kept offshore. Rumors have been flight that members of the Royal family may be creating a stash just in case there is major civil unrest which forces them to flee into exile. Obama on his recent trip told the Saudis they should adopt democratic reform. Make no mistake about it. There is trouble brewing in the Middle East. There is no way Obama would have made such a statement publicly if the situation were not grave.

May – August – October are being highlighted as key periods ahead.

related:

Joseph Schachter: Where Oil is Going Next

The bankruptcies are continuing fast and furious across the energy sector. With the ill-effects spreading beyond just the oil and gas business — evidenced by major renewables firm SunEdison filing for Chapter 11 last month.

But the U.S. E&P sector still remains one of the biggest unknowns when it comes to bad loans. With numerous observers having recently warned about a big wave of defaults coming in this space.

And a new data point late last week suggests we may be reaching a tipping point.

That came from leading American investment bank JPMorgan. Which said in an SEC filing Friday that its holdings of potentially bad loans took a major jump over the past quarter.

JPMorgan reported on its holdings of “criticized” loans — a term used in the banking industry to refer to “substandard or doubtful” debts. With the bank saying that its criticized loan portfolio leapt by 45% over the last quarter — to $21.2 billion as of March 31, up from just $14.6 billion at December 31, 2015.

The 3-month increase of $6.6 billion was driven mainly by one sector — oil and gas. With the value of JPMorgan’s criticized oil and gas loans rising $5.2 billion over the last quarter. (Criticized loans to the mining and metals sector also jumped 55% during the quarter — although the total increase was much smaller, at just over $600 million.)

All told, JPMorgan’s exposure to criticized oil and gas loans now totals $9.7 billion — up from $4.5 billion at the end of 2015.

The bank did note most of these loan holders are still paying their bills. With “only” $1.7 billion worth of criticized oil and gas debt being categorized as “non-performing”. However, that was a 665% rise from the previous quarter — when only $222 million in loans were declared non-performing.

All of which confirms what we’ve been seeing anecdotally the last few months: the E&P sector is hitting the wall when it comes to debt. Watch for more bankruptcies coming — as well as issues emerging at U.S. banks due to growing exposure to bad energy loans.

Here’s to taking cover,

Dave Forest

related:

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair