Mike's Content

Victor points out that money is starting to move into the sold out Commodity sector which relative to stocks is down 75% in the last 7 years to an 18 year low. He also see the US Dollar oversold and due for a bounce. Transcript below:

The key aspect of market psychology so far this year has been a willingness to aggressively take on risk. We have seen aggressive buying of stocks and aggressive selling of bonds and the US Dollar.

The leading global stock market indices keep rising as risk appetite keeps rising and FOMO seems to be the driving force. Bank of America reports that the latest 4 week inflows into equities was the largest ever at $58 billion. The Investor’s Intelligence survey reports the Bull / Bear spread is 67% / 13% the highest since 1986. The DJIA rallied over 1000 points in 8 consecutive days…a record clip. There hasn’t been so much as a 3% correction in over a year. A weak USD helps support American stocks as ½ of the sales by the S+P 500 companies come from outside the USA. This is the Euphoric Stage of a rally and it could go a lot higher but I’m not jumping aboard. As Bob Farrell says, “The public buys the most at the top and the least at the bottom.”

Interest rates are also rising with the 2 year Treasury yield above 2% for the first time in 10 years and the 10 year Treasury yield at a 4 year high of 2.64%. (That’s a double from the 1.3% yields hit during the Brexit period, June 2016.) Last year saw a record sized flow of money ($2 Trillion) into the markets from the G4 Central Banks…the forecast for this year is that Central Banks will inject WAY LESS capital while governments are issuing more debt…therefore, this year the private sector is going to have to buy bonds…and that may mean interest rates will have to go higher to attract capital. The bond market “Kings” (Gross and Gundlach) predict that the 10 year Treasury yield will go higher and will cause (at least) a correction in the stock market. The Guarded Opportunity managed futures program that my son Drew manages has been short T-Notes since the end of November.

The American Financial Conditions Index is at its easiest in 10 years courtesy of a weak USD, strong stock markets and tight credit spreads. This may contribute to the FOMC raising s/t interest rates more in 2018 than the market is currently pricing.

The US Dollar Index hit 14 year highs a year ago, fell for most of 2017 and has made fresh 3 year lows YTD as the Euro makes 3 year highs (up 16% from a year ago)…despite the 2 year interest rate spread between the USA and Germany at a record wide >2.6%. Futures market speculators have an All Time Record large net long position in Euro against the USD. Trends in the FX markets often go WAY further than seems to make any sense…and then turn on a dime and go the other way. I think part of the weakness in the USD is an expression of the risk appetite trade. When the market is willing to take on risk capital moves away from the center (New York) and goes to the periphery (say, emerging markets.) If risk appetite gets “spooked” I expect the USD to rise sharply.

The Canadian Dollar “big event” for this week was the Bank of Canada meeting. They raised rates as expected but sounded a strong note of caution over NAFTA uncertainties. CAD traded through a 1 ¼ cent range on Wednesday and closed unchanged. I’ve been suspicious about the very strong December employment number reported by StatsCan…I’d look for a much weaker number for January if not an outright downward revision to the December number. I think it’s possible to see the Bank of Canada fall well behind the Fed this year in terms of raising interest rates. Western Canada Select oil continues to trade around $40 and Canadian NatGas is WAY cheaper than New York benchmarks. The NAFTA negotiating teams meet again in Montreal this coming week. Interestingly the Mexican Peso has risen about 7% since Christmas…apparently not worried about Trump pulling the plug on NAFTA.

I think CAD rallied from 7750 in mid-December to the January highs of 8100 because of a generally weak USD. I think USD is oversold and if it bounces back then the best candidate to short against USD is CAD. I’m short CAD.

Crude oil prices hit 3 year highs this week with WTI ~$65. Futures market speculators are massively net long crude. OPEC and IEA forecasts this week both predicted substantial increases in non-OPEC production this year…with the IEA predicting that “explosive” growth in American production together with substantial increases in Canada and Brazil will more than make up for any declines in Venezuela and Mexico. I think the crude oil market is about, “As Good As It Gets” and I’m short.

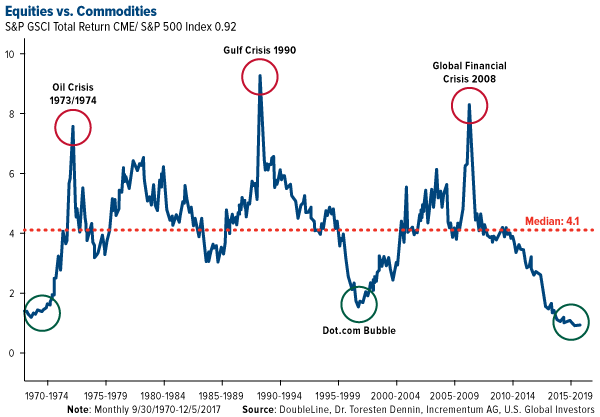

Commodity Indices are rising with the (energy heavy) Goldman Sacs commodity index up ~63% from the January 2016 lows at a 3 year high. The venerable Thompson Reuters Commodity Research Bureau Index (with a much greater weighting to the AG sector) is up ~26% from the January 2016 lows. Both indices are 40 to 50% below their All Time Highs. Despite these “decent” 2 year rallies the commodity indices have continued to fall relative to the major stock market indices. The CRB Index hit its All Time High in 2011 and, relative to the S+P 500 Stock Index it has fallen ~74% in the past 7 years to an 18 year low! The gold/S+P500 ratio has fallen ~70% in the same time period to an 11 year low.

I think “some” of the buying we’ve seen in the commodity and commodity currency sector over the past 2 years may have come from “some” rebalancing by macro asset allocators…they’ve taken money away from their big gains in the stock markets and re-positioned it in the relatively “really cheap” commodity sector.

Keep track of Victor at http://www.polarfuturesgroup.com

In Live from the trading desk, Michael Campbell gets Victor Adair’s core expectation for 2018. Also Victor delinates areas where danger lies.

…also from Michael: They Chose Rape, Beheadings and Murder

Mark Liebovit’s top recommendation at last year’s World Outlook Financial Conference was Bitcoin Trust @$110 – traded last friday today @ $1,990 – 17.9 times

Mark Liebovit’s top recommendation at last year’s World Outlook Financial Conference was Bitcoin Trust @$110 – traded last friday today @ $1,990 – 17.9 times- Jim Dines recommended Canopy Growth @ $13 – traded last friday @ $23.12

- James Thorne shockingly recommended Bombardier @ $2.00 – traded last friday@$3.03 – up 51%

- Ryan Irvine recommended International Road Dynamics @ $2.50 – taken over 3 months later at $4.25 – up 70%

Those are great results but that’s the whole point of inviting some of the top analysts in the English speaking world to the World Outlook Financial Conference for the past 29 years. Obviously past performance is not a guarantee of future success but the results we have achieved over the years have not been by accident. Our analysts have been chosen precisely because they have strong track records.

No, they are not right every time, but their uncanny ability to read the various investment markets while employing proven risk management techniques has clearly raised their probability of success dramatically. Whether you’re interested in stocks, gold, oil, real estate, interest rates or currencies – we bring in the top analysts to the World Outlook Financial Conference to cover them all.

It’s an incredible line-up for Feb 2nd & 3rd, 2018. Martin Armstrong has been called the highest paid financial advisor on the planet. Heck, I’ve called him the top economic forecaster in the world. Let me give you just a couple of examples. At the Outlook in 2013 he correctly predicted the date of the Russian invasion of Ukraine and the accompanying massive outflow of capital that would push the US dollar and stocks higher. More importantly he clearly predicted the rise of the Dow Jones Index through 18,000 and told the audience to buy every dip because the next stop was 23,700. We came within a quarter of a percent of his target this month so I can’t wait to hear what he has to say now.

Mark Leibovit will also be at the 2018 Outlook. Mark has been Timer’s Digest Timer of the Year, Gold Market Timer of the Year and Long Term Timer of the year. While he’s been great in all those areas – my favourite of his forecasts came at the 2014 Conference where he told us to start to invest in marijuana stocks starting with GW Pharmaceuticals at $67. Mark has repeated his recommendation of the marijuana industry every year. I think it’s safe to say that was a good call but I’ll be interested in what he has to say this year as the industry and the stocks become more mainstream.

I won’t go through all the 2018 speakers right now (they’re available HERE) but let me give you just one more example of the quality of analyst featured at the World Outlook Conference. Keystone Financial’s Ryan Irvine has been producing a World Outlook Small Cap Portfolio for the past 8 years – and as I said past performance is no guarantee of future success but I like my chances. The Small Cap Portfolio has returned double digits every single year – no exceptions.

Obviously I want to hear Ryan’s picks at this year’s conference. I’m worried it will cost me too much money if I don’t!

What Will Happen in 2018

The easiest prediction is that the rate of change will continue to increase, which will produce big price swings in a variety of investments.

Goldman Sachs just predicted four more interest rate hikes in the States in 2018. If they’re right, it will have a huge impact on the US dollar. The loonie will go down as a result unless the Bank of Canada raises our rates with them. And if they do what will be the impact on real estate and Canadian stocks?

Currency moves are going to provide a huge opportunity for those who position themselves properly. I’m pleased to say that the currency recommendations at the Outlook Conference have made a lot of people money but I think 2018 will be an even bigger year.

I continue to be most worried about the government bond market. If rates rise, bonds will certainly go down, which is why I’ve been telling people to get rid of government bonds with maturities of 3 years and longer. At the 2018 Outlook we’ll talk a lot more about the vulnerability of government bonds.

The Pension crisis in Europe and the States will also be a big story in 2018 with major financial implications, as well as social and political ones. We’ll talk more about how to position yourself to both protect and profit from the pension problems.

The Bottom Line

The level of volatility and the violence of the moves in all markets necessitates taking advantage of the best possible research and analysis available. While financial programs and conferences often feature cheerleaders for a variety of products or industries, we focus on top flight independent analysis. The bottom line is that I am confident that our analysts can make you back the price of admission many times over.

Periods of historic change provide incredible opportunities and incredible danger.

At the 2018 World Outlook Financial Conference and on MoneyTalks, I’m trying to help you avoid the danger and take advantage of the opportunities.

I hope to see you there.

Sincerely

Mike

PS – The 2018 World Outlook Conference is Friday night Feb 2nd and Saturday Feb 3rd at the Westin Bayshore in Vancouver. For tickets and other details go to www.moneytalks.net and click on the events button.

…also from Michael: BC Message to Investors “Don’t Invest In BC”

Last year we told you the 5000 year bottom in interest rates was in.

Last year we told you the 5000 year bottom in interest rates was in.And that meant the 35 year bull market in bonds was over.

Bitcoin Trust was a top recommendation at last year’s World Outlook Financial Conference. Why? Because confidence in government and paper currencies is falling

Since March, 2009 we’ve predicted massive new highs in the Dow Jones. Guess what? It’s not over. Most don’t know why.

The pension crisis has just started and will become obvious in 2018.

Hi ,

I’m sure you’re busy. I certainly am given all that’s happening in the economy and markets but what’s going on is so incredible that it merits my time in bringing it to your attention. From Volvo’s contract to deliver 24,000 self driving cars to Uber in 12 months – to the mindblowing rise in Bitcoin. And then there’s the 50 year low in US oil imports while production hits record highs. (Message to the Middle East – the US doesn’t need you anymore.)

Last year Donald Trump’s victory was just one more sign of the kind of historical changes we’ve predicted at the World Outlook Financial Conference and on Moneytalks since 2009. Everything’s on schedule – lots of money is to be made and lost.

What’s Coming

My bet is that we are on the cusp of the next stage of the world’s monetary crisis – and we all better be ready. This is not for the faint of heart. What’s about to happen is going to make the last five years seem tame. (Let that sink in for a moment.)

My goal is to make sure you’re protected and profit financially. Unfortunately the vast majority of people won’t be ready. In 2018, the pension problems at the city and state level are going to be more obvious. Consider that Illinois’ pension liability is now 280% of its entire annual tax revenues. Teachers in Kentucky are demanding each Kentucky household pay $3,200 for each of the next two years in order to top up their pension plan. (Good luck with that). This is not going to end well.

Neither are the banking problems in European and they, in turn, will exacerbate the strains on the European Union. Catalonia’s independence movement, the election last Sunday in Corsica of anti-EU advocate, Gilles Simeoni, the election in the Czech Republic of Eurosceptic Andrej Babis, and the vote in late October of two of Italy’s wealthiest regions, Lombardy and Veneto, to separate illustrate the problem.

As we’ve been predicting on Moneytalks since 2010, the European Union will come apart and the financial repercussions are huge – including a major boost to the US stock market. We’ve been saying that playing the euro to go down (first recommended at 1.54 to the dollar, now 1.17) was a fundamental long term position – hence it was to be sold on any rally.

The euro recommendation illustrates the approach we take at the World Outlook Financial Conference and on Moneytalks. You start by getting the big picture right and then devise strategies to take advantage of it.

And our record at the World Outlook speaks for itself.

Our #1 recommendation since October, 2012 has been to put between 30% and 50% of your money into the US dollar. At the same time we recommended quality dividend paying US stocks, real estate in the Phoenix area and Vancouver.

We warned of the drop in commodities including gold when it was still $1800.

At the Conference in early 2014 our energy analyst, Josef Schachter warned when oil was well over $100 that it was about to decline to the $32-$34 level. In what was a first anywhere, Mark Liebovit recommended the marijuana industry.

While that was a great call, Mark surpassed that last year with one of his top recommendations, Bitcoin Trust – now up 1500% – (obviously that doesn’t happen very often.)

My Point

Maybe we’ve been lucky that every year our specific recommendations have paid for the price of a ticket several times over. To that end, Keystone’s Ryan Irvine will be back to present his 2018 World Outlook Small Cap Portfolio. While past performance is not a guarantee of future results, it is impressive that the Outlook Small Cap portfolio has achieved double digit returns every single year. We’ll talk the loonie, gold and the markets with Martin Armstrong and James Thorne, real estate opportunities with Vision Capital’s Jeff Olin, and the marijuana industry with Mark Leibovit.

And after years of trying, I’m really excited to say that I finally got BT Global’s terrific stock picker, Paul Beattie to agree to speak.

No Surprise

As you probably guessed, I want you to come to the 2018 World Outlook Financial Conference. Why? Because we’re living in a time of historical change and people who don’t understand what’s going on are going to get killed financially. Of course a lot of people already are but conference attendees who followed our recommendations into the US dollar, US stocks, real estate in Vancouver, Phoenix and Victoria, and have bought the World Outlook Small Cap Portfolio have done well.

I understand that not everyone is interested in their personal finances – and I respect that. (Heck, I’ve got friends who I have to force to come because it conflicts with something on tv.) Maybe you’re already are on top of things. May you have other things on the go.

All I’m saying is that periods of historic change provide incredible opportunities and incredible danger. Simply put, at the World Outlook Financial Conference our goal is to help you avoid the danger part and take advantage of the opportunities.

I hope to see you there.

Sincerely

Mike

PS – The 2018 World Outlook Financial Conference is Friday night Feb 2nd and Saturday, Feb 3rd at the Westin Bayshore. For tickets and other details go to www.moneytalks.net and click on the EVENTS button.

PPS As you probably know I’m big on educating our younger generation – goodness knows I go on about it enough. To that end we have a special offer – if you buy a ticket – you can bring a student or some other young person in your life, absolutely free. The only thing is that we ask you to let us know that you want a student ticket when you purchase your ticket. We have a limited number set aside and we want to be able to accommodate you.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair