Currency

The Japanese Yen has fallen dramatically during the past two months – developments in Japan have had a HUGE impact on markets around the world – a BIG market turn may be close.

The Yen has been rising against the US$ for 40 years…it began its last major rally in 2007…and despite forecasts from a number of high profile analysts (i.e. Kyle Bass) that it was going to take a big tumble it traded to All Time Highs in October 2011 before turning lower. It had an initial breakdown through the 5 year up-trend line in early 2012…rallied back to “kiss” the underside of the uptrend line…and then rolled over…gaining momentum to the downside around November 12, 2012…front-running the dramatic reflationary policies advocated by Abe as it became apparent that he was going to win the December elections.

The Japanese Yen has tumbled as Abe has implemented VERY DRAMATIC REFLATIONARY MEASURES in an attempt to end two decades of deflation in Japan. He has put the Bank of Japan under intense pressure to increase the money supply and target 2% inflation. He has legislated massive government spending programs…and talks of much more to come. These policies have had a powerful influence on markets around the world…it has been “Risk-On” in a BIG way.

Global Stock markets have been boosted by Japanese policies:

The S+P 500 closed this past week at 5 year highs…up ~10% from the Nov 16 lows. The higher beta small cap Russell 2000 is up ~15.5% during the same period to All Time Highs. The TSE is up ~7%, the UK FTSE is up ~9%, the German DAX is up ~11% and the Japanese Nikkei is up ~26% to its best levels in 3 years.

Mid-November Key Turn Date:

I often refer to Key Turn Dates in the market…dates when a number of major markets all reverse course on or around the same day……

……read more HERE

Economists who hold the popular view that expanding the money supply will provide the best medicine for our ailing economy dismiss the inflationary concerns of monetary hawks, like me, by pointing to the supposedly low inflation that has occurred during the current period of rampant Fed activism. In a recent blog post aimed specifically at me, Paul Krugman noted that the sub 2.5% increases in the Consumer Price Index (CPI) over the past few years are all that is needed to prove me wrong. In fact, Krugman and others have even suggested that the CPI itself overstates inflation and that the Fed would be better able to help the economy if less strict methodologies were used. However, there is plenty of evidence to suggest that the CPI is essentially meaningless as it woefully under reports rising prices.

Economists who hold the popular view that expanding the money supply will provide the best medicine for our ailing economy dismiss the inflationary concerns of monetary hawks, like me, by pointing to the supposedly low inflation that has occurred during the current period of rampant Fed activism. In a recent blog post aimed specifically at me, Paul Krugman noted that the sub 2.5% increases in the Consumer Price Index (CPI) over the past few years are all that is needed to prove me wrong. In fact, Krugman and others have even suggested that the CPI itself overstates inflation and that the Fed would be better able to help the economy if less strict methodologies were used. However, there is plenty of evidence to suggest that the CPI is essentially meaningless as it woefully under reports rising prices.

Magazines and newspapers provide a good case in point. The truth has not been exposed through the economic reporting that these outlets provide, but in the prices that are permanently fixed to their covers. For instance, from 1999 to 2002 the Bureau of Labor Statistic’s (BLS) “Newspaper and Magazine Index” (a component of the CPI) increased by 37.1%. But a perusal of the cover prices of the 10 most popular newspapers and magazines (WSJ, Washington Post, Time, Sports Illustrated, U.S. News & World Report, Newsweek, People, NY Times, USA Today, and the LA Times) over the same time frame showed an average cover price increase of 131.5% (3.5 times faster than the BLS’ stats). This is not even in the same ballpark.

Some defenders of the BLS may conclude that prices were held down by the availability of free online news content or the convenience of digital delivery. But that is beside the point. Prior to the digital age, the BLS could have claimed that newspaper costs were held down by public libraries that provided free access. It’s also true that online publications deliver less value on some fronts. Not only do many people enjoy the tactile process of reading physical newspapers or magazines, but they offer the secondary value in helping to kindle fires, housebreak puppies, pack dishes, and line birdcages.

Another stunning example is found in health insurance costs, which is a major line item for most families. According to the BLS we can all breathe easy on that front because their “Health Insurance Index” increased a mere 4.3% (total) in the four years between 2008 and 2012. Interestingly, over the same time, the Kaiser Survey of Employer Sponsored Health Insurance showed that the cost of family health insurance rose 24.2% (5.5 times faster). But even if the BLS had reported higher costs, it wouldn’t have made much of a difference in the CPI itself. Believe it or not, health insurance costs are assigned a weighting of less than one percent of the overall CPI. In contrast, the Kaiser Survey revealed that in 2012 the average total cost for family health insurance coverage was $15,745, or almost one third of the median family income.

If the BLS could be so blatantly wrong in reporting the prices of newspapers and health insurance, should we believe that they are more accurate on all other sectors? If the inaccuracy of these two components were consistent with the rest of the CPI’s components, inflation could now be reported in double-digits!

Even more egregious than the manner in which prices are currently reported is the way that CPI methods have been changed over the years to insure that most increases are factored out. Since the 1970’s, the CPI formula has changed so thoroughly that it bears scant resemblance to the one used during the “malaise days” of the Carter years. Main stream economists dismiss criticism of the changes as tin hat conspiracy theories. But given the huge stakes involved, it’s hard to believe that institutional bias plays no role. Government statisticians are responsible for coming up with the formulas, and their bosses catch huge breaks if the inflation numbers come in low. Human behavior is always influenced by such incentives.

The newer CPI methodologies are designed to report not just on price movements, but on spending patterns, consumer choices, substitution bias, and product changes. In other words, the metrics have been altered to track not so much the cost of things, but the cost of living (or more accurately, the cost of surviving). But if you simply focus on price, especially on those staple commodity goods and services that haven’t radically changed in quality over the years, the under reporting of inflation becomes more apparent.

As reported in our Global Investor Newsletter, we selected BLS price changes for twenty everyday goods and services over two separate ten-year periods, and then compared those changes to the reported changes in the Consumer Price Index (CPI) over the same period. (The twenty items we selected are: eggs, new cars, milk, gasoline, bread, rent of primary residence, coffee, dental services, potatoes, electricity, sugar, airline tickets, butter, store bought beer, apples, public transportation, cereal, tires, beef, and prescription drugs.)

We know that people do not spend equal amounts on the above items, and we know their share of income devoted to them has changed over the decades. But as we are only interested in how these prices have changed relative to the CPI, those issues don’t really matter. We chose to look at the period between 1970 and 1980 and then again between 2002 and 2012, because these time frames both had big deficits and loose monetary policy, and they straddle the time in which the most significant changes to the CPI methodology took effect. And while the CPI rose much faster in the 1970’s, the degree to which the prices of our 20 items outpaced the CPI was much higher more recently.

Between 1970 and 1980 the officially reported CPI rose a whopping 112%, and prices of our basket of goods and services rose by 117%, just 5% faster. In contrast between 2002 and 2012 the CPI rose just 27.5%, but our basket increased by 44.3%, a rate that was 61% faster. And remember, this is using the BLS’ own price data, which we have already shown can grossly under-estimate the true rate of increase. The difference can be explained by how CPI is weighted and mixed. The formula used in the 1970’s effectively captured the price movements of our twenty everyday products. But in the last ten years it has been quite a different story.

If these price changes in our experiments had been fully captured, CPI could currently be high enough to severely restrict Fed action to stimulate the economy. Instead, the Fed is operating as if inflation is extremely low. As a result, they are making a huge policy mistake that will come back to haunt us. During the last decade the Fed spent many years denying the existence of a housing bubble, even as a mountain of evidence piled up to the contrary. That error caused the Fed to hold interest rates too low for too long, blowing more air into the bubble and imposing enormous negative consequences on the economy. The Fed, now similarly blind to the inflation threat, is repeating its mistake, only this time the negative consequences will be even more dire.

Apart from the statistical problems that hide inflation, there are also macroeconomic factors that have helped keep prices down despite the quantitative easing. Massive U.S. trade deficits and foreign central bank dollar accumulation mean that much of the printed money winds up in foreign bank vaults, not U.S. shopping centers. As foreign consumer goods flow in, and dollars flow out, a lid is kept on domestic prices. In effect, our inflation is exported as foreign central banks monetize our deficits and recycle their surpluses into U.S. Treasuries. The demand has pushed down bond yields which has allowed the U.S. government to borrow inexpensively. Of course, when the flows reverse, bond prices will fall, yields will climb, and a tidal wave of dollars will wash up on American shores, drowning consumers in a sea of inflation.

Unlike Krugman and the Keynesians, I would argue that it is impossible to create something from nothing. I believe that printing a dollar diminishes the value of all existing dollars by an aggregate amount equal to the purchasing power of the new dollar. The other side takes the position that the new money creates tangible economic growth and that real economic value can therefore be created by putting zeroes onto a piece of paper. I think that those making such absurd claims should bear the burden of proof. For more on the interesting topic of hidden inflation, see my video that I just posted.

One of the handful of people I take the time to listen to at investment conferences and whenever he speaks is Frank Holmes – Peter Grandich

During these first days of January, many adopt an “out with the old, in with the new,” approach to shed bad habits or extra pounds. Washington opted for its same ol’ strategy when averting the “fiscal cliff,” as the addictive nature of “can-kicking is a transatlantic sport,” according to The Economist. The magazine suggests that the deal made in the 11th hour is “disturbingly similar to the eurozone’s.” The short-term fix did “nothing to control the unsustainable path of ‘entitlement’ spending on pensions and health care … nothing to rationalize America’s hideously complex and distorted tax code… and virtually nothing to close America’s big structural budget deficit.”

In the end, politicians agreed to end the payroll tax cut and raise taxes on the top earners; altogether, tax increases will total $162 billion in 2013. According to a Bloomberg article, it’s the first time since 1990 a Republican leader agreed to a boost on tax rates. The legislation also represents the largest tax increase in two decades, says the Wall Street Journal.

……..read more HERE

Creating and sustaining a nation of zombies is expensive.

Large sections of the US population have been turned into zombies. Retirees. Medicare dependents. Food stamp recipients. Disabled people. They are not necessarily bad people. They are not necessarily dishonest or lazy. But rather than add to wealth, they consume it. And when you have too many of them, your society consumes more wealth than it produces and you are on the road to The Downside.

But the feds are not only creating individual zombies, they are also creating corporatezombies. An obvious example: “green” energy. Without subsidies, loan guarantees, tax benefits and direct giveaways, the industry as we know it would not exist. Nor would the ethanol industry in the Midwest. Nor the security industry in the Northern Virginia suburbs of Washington, DC.

The financial industry too, as we know it, would not exist either. Much of it would have been swept away in the financial storm of 2008-09. That story is well-known, but not well understood. Most people believe the authorities acted heroically, saving the nation from a depression. But what the authorities really did was to take the public’s money and give it to cronies on Wall Street in order to prevent them from suffering the losses they deserved. The government transferred nearly $2 trillion in various forms from the public purse to the pockets of the financial industry. With that kind of backing, most of the old investment firms survived. The new ones that might have replaced them never saw the light of day.

Industries need to be sustained by the government when they cannot sustain themselves. This is practically the definition of “malinvestment” — putting capital and energy into investments that don’t pay off. When an industry is only profitable with government backing it means that the industry uses resources — labor, energy, raw materials — and turns them into finished products that are worth less than the inputs required to make them. The more of these zombie industries the government supports, the poorer the society becomes.

The Single Best Reason to Feel Good About America’s “Collapse”

What could possibly be the good news about America’s next financial meltdown?

I urge you to watch this eye-popping video.

You’ll see why the years ahead could actually be the richest, happiest, and healthiest years of your life… not just in spite of the impending new financial crisis, but because of it.

If that seems strange to you, click here to see why for yourself.

Before the French Revolution, favored groups were able to secure special privileges and monopolies giving them the right to income. For example, the people from whom we bought our first house in France had a monopoly on the importation of tobacco from the New World. I don’t know who granted this monopoly, but typically it was the monarchy. And typically, such monopolies were given away either to appease a potential adversary or simply to raise cash for the crown by selling off a stream of future income. “Rentier” is a French word that has leaked into English. It doesn’t mean zombie literally, but it describes people who have found a way to exploit the system for their own benefit — people who have legal entitlements to income streams. In other words, “rentier” describes a class of folks who contribute absolutely nothing to national prosperity — zombies.

The French crown was always short of funds. It found it could raise substantial sums by selling the right to earn a “rent.” It might sell the right to collect tolls on a highway or a river, for example. Or it might sell the right to collect taxes (thereby getting its own tax revenue up-front and letting the rentier deal with the hazards of collection).

Any official document needed an official stamp. Naturally, the crown sold off the right to stamp documents. If you wanted to make a business deal, buy or sell land, or get married, you had to pay the person with the stamp.

Over time, the rentier class grew larger and harder to support. More and more of the kingdom’s energy went to support what was essentially a group of parasites who produced nothing. This is part of the explanation for the French Revolution. The system became so inefficient and was made so fragile by waste that a relatively minor setback — a couple years of bad harvests — caused widespread hunger and revolt.

In modern, developed societies “rents” come in many forms. They are often granted to favored groups in exchange for political support. Old people vote, for example. Political parties seek their votes by promising ever-larger health and retirement benefits. Rich people make campaign contributions. Politicians typically grant them favors too.

By the close of 2012, there were zombies everywhere. Throw a cream pie from almost any street-corner and you were almost certain to hit one in the face. If the street-corner were in Washington, DC, you’d probably hit two or three of them.

A recent report in The Wall Street Journal confirmed that zombies don’t work very hard. The Bureau of Labor Statistics has been compiling detailed data on how people use their time. Researchers tracked how many hours people slept, ate, watched TV and worked. And guess what? They found that federal government employees put in 3.8 fewer 40-hour weeks than employees in the private sector. Here, the cost of zombification is clear: if the zombies were forced to work the same hours as people in the private sector, the government would save $130 billion a year.

Meanwhile, over in the pentagon, R. Jeffrey Smith had his eye on the zombies too:

Of the many facts that have come to light in the scandal involving former CIA director David H. Petraeus, among the most curious was that during his days as a four-star general, he was once escorted by 28 police motorcycles as he traveled from his Central Command headquarters in Tampa to socialite Jill Kelley’s mansion. Although most of his trips did not involve a presidential-size convoy, the scandal has prompted new scrutiny of the imperial trappings that come with a senior general’s lifestyle.

The commanders who lead the nation’s military services and those who oversee troops around the world enjoy an array of perquisites befitting a billionaire, including executive jets, palatial homes, drivers, security guards and aides to carry their bags, press their uniforms and track their schedules in 10-minute increments. Their food is prepared by gourmet chefs. If they want music with their dinner parties, their staff can summon a string quartet or a choir.

The elite regional commanders who preside over large swaths of the planet don’t have to settle for Gulfstream V jets. They each have a C-40, the military equivalent of a Boeing 737, some of which are configured with beds.

And then, even after they retire…the zombies keep feeding off the productive sector:

Updating a 2010 Boston Globe report that documented the practice, CREW found that over the last three years, 70 percent of the 108 three-and-four star generals and admirals who retired “took jobs with defense contractors or consultants.”

As Sen. Claire McCaskill, D-Mo., put it during a 2009 hearing on Obama’s nomination of former Raytheon executive William Lynn to become the deputy secretary of defense, “it’s an incestuous business, what’s going on in terms of the defense contractors and the Pentagon and the highest levels of our military.”

During the Presidential campaign, Mitt Romney mentioned that 47% of American households now receive some form of support from the government. In a better democracy, none of those people should vote. They all have a conflict of interest. They should admit that they find it difficult to separate their own personal interests from those of the nation and abstain from casting a ballot. Instead, they “vote their own pocketbooks” — usually coming down on the side of diverting more resources from the productive sector to their own personal consumption.

The zombies corrupt the system. The march to Stalingrad continues. And the Downside takes over.

Regards,

Bill Bonner

for The Daily Reckoning

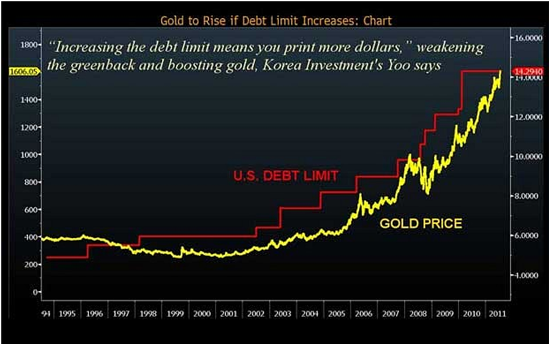

The Pieces Are In Place For A Gold Rally

Tom Cloud of National Numismatic Associates, he explains why the upcoming debt limit negotiations are a bigger deal than the fiscal cliff for precious metals.

DollarCollapse: Hi Tom. How’s business? Specifically, what are your customers thinking about?

Tom Cloud: The phone is ringing off the hook. Our customers are less concerned with the fiscal cliff being kicked down the road than with the fact that the debt ceiling is just a couple of months away. I’m also hearing a lot of complaints about president Obama cutting the fiscal cliff deal and then immediately charging taxpayers $3 million to take him and his family to Hawaii.

…..read more HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair