Market Opinion

India’s central bank taking 200 tonnes (6.4 million oz) of gold from the IMF in an off market trade has certainly lit a fire under the yellow metal. While a trade of that nature was anticipated, India, which is about the savviest of commercial gold players, was not atop the expected buyers’ list. Given the greenback was steady and that gold’s chart went near vertical when the overnight rumor became official, it is likely that the big long position that came into the market forced some covering on the short side. Is this more than a spike?

We think India’s move could be, in part, a signal it should have a bigger chair at economic tables, which we agree with. Since Indians are the biggest gold buyers on the planet, lifting a perceived overhang from its market has the side benefit of protecting an existing wealth pool of its citizens. And the near US $7 billion price tag is not large against India’s $260 billion foreign reserve holdings.

However, it does have a bigger impact on gold’s market (about $115 billion annually, now) and that got noticed. Also, it will further establish the notion of a currency basket that includes gold as a global trading medium, and conversely a weaker greenback. That should continue the move of capital into gold as $ hedge.

In saying that, we realize that it would be tough for gold to replace the oil market as a home for dollar hedge trades simply because of the oil markets much larger scale. But oil can not continue to gain without causing major problems for the near term economy, nor can oil rise if other energy components are not doing the same. Scale aside; gold makes sense as a place to place anti-dollar bets, and especially for players worried about longer term wealth preservation. But so too do other metals.

If copper does truly have a PhD in economics (not that that title has quite the allure of a few years ago), our take has to be that the Doctor is mulling over an extended lunch. The red metal’s price continues to bounce against the $3/lb ($6600/t) level even while available stockpiles have grown. There has been a slight decline of stockpiles in the past few days, but that was after having recouped 60% of the drawn down earlier in the year.

Clearly, new metrics are at work. We and others have already pointed at Dollar roulette as one. In fact that is a big part of the whole market these days, and it’s an issue that will grow in the telling. There has also been a build up of small supply disruptions in copper, such as the shut down of most output from BHP’s Olympic Dam mine in South Australia. The mine’s capacity is less than 1% of global copper supply (but a big chunk of uranium output), but this isn’t the only mine at reduced capacity.

The psychology of relatively minor supply disruptions when new mine development is still limited may be adding some price support. The other base metals are similarly in a neural pose these days. Rumblings about a better market are most prominent around zinc, as are concerns about maintaining concentrate streams to smelters outside of China. That would be next year’s story, but it is worth noting. For the past century or so mines were dictated to by smelters, but now smelters are worried about keeping their market shares and the balance of power has been shifting.

As with most things in this changing market landscape, it is tough to make assumptions about the next six months. That simple truism is driving things right now, if being in neutral could be called “driving”. Producers’ share prices are shifting down with the market, but still finding support. It may well be the balance of the year will mostly be about ensuring gains after a strong uptick, and making cash for future events.

There has been more weakness due to profits taking in some of the early exploration gainers. Conversely, former laggards have been able to pick up steam by showing project advancement. There is a general sense of rotation out of strength and into future potential, at least in our part of the playground. That is meaningful.

As broader stock market gains began to peel away, we have been struck by a consistent lift in one measure. While other North American equity markets saw share turn over slide along with prices, the TSX Venture exchange has actually seen daily volumes as strong as they have ever been. This is not dollar-volume, and some of it can be accounted for by share issuances that are bloated by historic standards. It does however indicate that there are still punters out there.

While we think of the Venture exchange as a proxy of the junior resource sector, other sectors are obviously part of it. Funding for the Tech space is reviving a decade after that bubble burst, and green energy concepts are growing in number. However, on checking volume leaders most days the lists are at least nominally composed primarily of resource deals.

Bears might argue this is desperate averaging down ahead of the next major down shift in the market. It doesn’t look to us like the random buying during the bounce of a bear market rally. That type of buying typically comes in spurts, and focused on companies based on their previous market strength. Nor frankly do we think such buying is very likely after last year’s market drubbing.

This is a sustained turn over that relates to broader markets only in terms of showing patience on weak days. It is focused on companies that do have underlying assets, regardless of how well they made markets in the past. We see a concerted effort to own resource assets in juniors while they are still in the bargain bin. And we believe this is being done by folks who have been around the sector long enough to recognize that US$ roll over and supply constraints are still near and mid term factors.

To anyone who thinks we are drinking our own bathwater we can only say, you’re right. We are not suggesting that simply because “the usual suspects” are coming to the venture side of mining that prices will go up. Nor does this buying mean they all expect immediate gratification. However, there is a mood building for significant gains for the sector this coming year. Even market watchers with large concerns about the broader economy are recognizing that the resource sector has good fundamental potential. Both supply-demand against Asian growth and the shifting currencies market favour it.

We do expect the balance of the year to have a significant cash generating ethic. After the roller coaster ride we have had that kind of prudence is to be expected. Despite base metal prices holding up, that kind of thinking is evident by consolidation amongst the producers in that space. Gold producers have been doing better, and for the time being we continue to expect this to be the preferred subsector in the metals market.

There may be some frustration with explorers who seem not to be living up to their results, relative to peers, after putting in strong performances. Taking gains along the way will continue to be important, but we also expect rebalancing that will include stronger recognition for undervalued assets. That is usually a question of moving through volume, and the market shifts that take place through year end.

Barring an “event” of some magnitude, it will take an accumulation of stats indicating how well economies are doing as their government stimuli slow down to shift the market too far off its current groove. That is will be next year’s story, and we think it’s too soon to make assumptions on the outcome

For the time being we will remain on volume watch, both in terms of metals directly and the equities that deal with them. We continue to favour speculations that can generate drilling success, while accumulating those that are still waiting for a mood shift in the market that will lead traders to recognize their already established values.

Ω

Gain access to potential gains of hundreds or even thousands of percent! From March to June, HRA introduced four new gold explorers to subscribers. Those four companies have generated an average gain of 205%, to date! SPECIAL HRA OFFER: For a limited time only, HRA is offering free reports and subscription savings. Click HERE for more information or here http://www.hraadvisory.com/sh2009.html

Click on image or HERE. for the above, read more for Picks

Interesting comments start at 1:57, for actual picks advance to 13:33.

Click on image or HERE.

Dr Marc Faber was born in Zurich, Switzerland. He went to school in Geneva and Zurich and finished high school with the Matura. He studied Economics at the University of Zurich and, at the age of 24, obtained a PhD in Economics magna cum laude.

Between 1970 and 1978, Dr Faber worked for White Weld & Company Limited in New York, Zurich and Hong Kong.

Since 1973, he has lived in Hong Kong. From 1978 to February 1990, he was the Managing Director of Drexel Burnham Lambert (HK) Ltd. In June 1990, he set up his own business, MARC FABER LIMITED which acts as an investment advisor and fund manager.

Dr Faber publishes a widely read monthly investment newsletter “The Gloom Boom & Doom Report” report which highlights unusual investment opportunities, and is the author of several books including “ TOMORROW’S GOLD – Asia’s Age of Discovery” which was first published in 2002 and highlights future investment opportunities around the world. “ TOMORROW’S GOLD ” was for several weeks on Amazon’s best seller list and is being translated into Japanese, Chinese, Korean, Thai and German. Dr. Faber is also a regular contributor to several leading financial publications around the world.

A book on Dr Faber, “RIDING THE MILLENNIAL STORM”, by Nury Vittachi, was published in 1998.

A regular speaker at various investment seminars, Dr Faber is well known for his “contrarian” investment approach.

He is also associated with a variety of funds and is a member of the Board of Directors of numerous companies.

Robert Prechter Jr. has an independent streak that puts him at odds with the crowd at times. A case in point….

his resolute refusal to join the bullish stampede into gold (GC-FT1,089.702.400.22%) that has driven its price above $1,000 (U.S.) an ounce in recent months.

Shunning the herd is perhaps what one would expect of Mr. Prechter, a member of the Triple Nine Society (open only to persons who have scored above the 99.9th percentile in IQ tests, higher than Mensa). Following his own star is indeed what he has always done, as is apparent in the route he took to become an expert in the technical analysis of financial markets and the publisher and editor of the Elliott Wave Theorist newsletter, based in Gainesville, Ga.

After graduating from Yale University in 1971 with a psychology degree (and deciding the life of a psychologist was not the path for him), he played the drums professionally in a rock band and, of all things, studied stock charts. Then he talked his way into a job as a technical analyst at Merrill Lynch in 1975 and branched out on his own as publisher and editor of an investment newsletter in 1979.

Mr. Prechter just doesn’t see the U.S. government’s Mount Everest of financial obligations precipitating a tsunami of hyperinflation, as the gold bugs envision. Neither does he see the U.S. dollar spiralling downward against other currencies and giving up its status as the world’s most used and held currency.

Not yet anyway because Mr. Prechter first expects a deflationary vortex to emerge from the ocean of credit on which the world economy floats – by as early as 2010. An environment where nearly all prices are falling is not conducive to the price of gold taking off. Its primary appeal to investors, after all, is as a hedge against inflation.

While gold bugs are convinced the U.S. government will ignite hyperinflation by paying off debt via the printing press, Mr. Prechter thinks we are at a critical juncture where the issuance of new quantities of paper money has lost its customary stimulative impact on prices. “The Fed will be pushing on a string,” he says; it will be powerless to halt a general decline in prices at this stage.

For one thing, the U.S. bond market stands in the way. If more concrete signs do emerge that the U.S. government intends to devalue its debt, bond holders can be counted on to dispose of substantial portions of their holdings, which will cause bond yields and interest rates to escalate. Rising rates are, of course, deflationary since they dampen private sector demand for loans.

Another thing that will neutralize the Fed is “a change in psychology,” says Mr. Prechter. As Elliott Wave patterns – the patterns of market price trends – are signalling, the social mood in the U.S. and elsewhere is transitioning from optimism to pessimism. A more conservative attitude toward debt will lead lenders to supply less credit and borrowers to demand less. End result: a halt and even a reversal in the credit expansion process.

The Oct. 18 edition of the Elliott Wave Theorist newsletter calls for gold to top out near current prices. Reasons Mr. Prechter offered:

Silver continues to lag and provide “non-confirmations” in its failure to break above its all-time high and its March, 2008, high (both of which gold has done).

If gold were to match inflation since 1933, it would have risen by 25 times instead of the current 50 times.

Gold is beginning to look like a crowded trade – even the Wall Street Journal, CNBC, and the Washington Post “tell you to buy.”

Virtually everyone at the New Orleans Investment Conference he recently attended “expressed super bearish views on the U.S. dollar.”

But saying Mr. Prechter is bearish on gold may be putting it too strongly. The bearish label may have fit in past years but in a September interview withFinancial Sense News Hour host Jim Puplava, he seemed to soften his stance somewhat.

Mr. Puplava asked if he wished he had changed anything in the second edition due out this month for his bestselling 2002 book, Conquer the Crash (all that’s new is the addition of over 150 pages containing Elliott Wave Theorist commentary from 2003 to 2007 and updated lists of U.S. financial institutions and contact services). He replied:

“If I were to reconsider one comment it is the idea that gold would have difficulties during the [deflationary period] ….there was so much inflation from 2002 to 2008 that it ignited all the markets, most of which have since collapsed …. But gold is [now] holding up. It went up the least relative to everything else and so it’s probably going to hold up pretty well during the deflationary drop. But I think it’s going to disappoint the people who think its going to $5,000 or $10,000 an ounce. That may happen after deflation is over.”

Elliott Wave International (EWI) is the world’s largest market forecasting firm. EWI’s 20-plus analysts provide around-the-clock forecasts of every major market in the world via the internet and proprietary web systems like Reuters and Bloomberg. EWI’s educational services include conferences, workshops, webinars, video tapes, special reports, books and one of the internet’s richest free content programs, Club EWI.

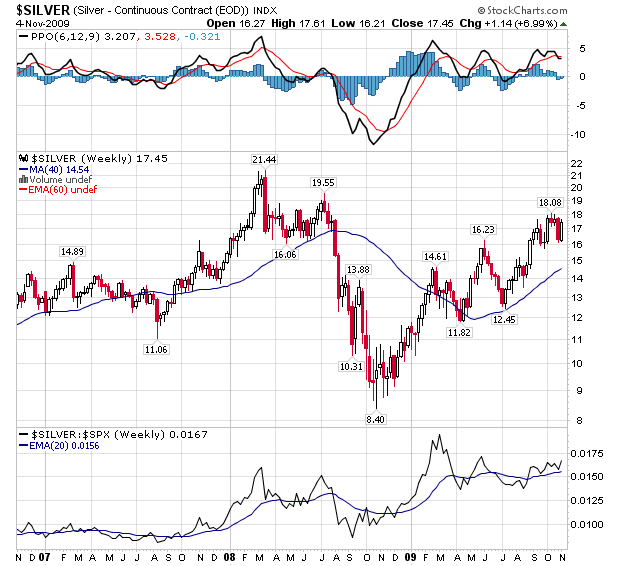

One ounce of gold now buys a huge 62 ounces of silver. Silver is dirt cheap compared with gold. Dec. silver closed up .06 to 17.40

A brief excerpt of the lengthy daily internet comment by Richard Russell of Dow theory Letters a man who has made his subriber’s fortunes (at least those that follow his advice). One of the best values anywhere in the financial world at only a $300 subscription to get his report daily for a year. HERE to subscribe.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair