Market Opinion

pecial offer from Mark Leibovit for Money Talks only: The intense analysis of Gold in the 10-12 page The VR Gold Letter is right now 75% off for the first month or $29.95 (regularly $125.00 a month). The weekly VR Gold Letter focuses on Gold and Gold shares.Go HERE and use the Money Talks promo code CBC12210

Ed Note: Partial comment on stocks from Mark’s Platinum service

STOCKS – ACTION ALERT –

As I mentioned in the Post-Market commentary, the first trading day of the month was predictably positive. Overall, sentiment still appears to be skewed to the negative, so despite historical precedent for a retracement in March, we have to keep out wits about us in that the opposite may occur instead. Today is ‘Turnaround Tuesday’, so my general expectation is for a retracement. But, absent increasing downside volume, the retracement could be minor. Regardless, I am current in cash for my trading positions. Overall, I remain on my ‘Buy’ signal, until we get a significant sign of a trend change.

The stock market rallied yesterday as merger activity, including the sale of American International Group’s Asia operations, brightened sentiment. Economic news was mixed yesterday with income and spending both rising, but incomes came in weaker than expected. The ISM index also showed an expanding economy, but this too was below expectations. Construction spending declined more than expected. But traders focused on the M&A activity, pushing the Dow up 78.53 to 10403.79, the S&P up 11.22 to 1115.71, and the NASDAQ up 35.31 to 2273.57.

We saw an across the board rally yesterday, though Financials (XLF +0.27%) lagged far behind the other sectors. Financials are underperforming as they remain exposed to bad debt over in Greece.

The broad indexes, such as the S&P 500, are back above their 50-day moving averages, a bullish sign if the market can stay over them. Meanwhile, the small and mid-cap indexes are nearing their recovery highs, as is the Dow Transportation Average.

As of January 25, 2009, TIMER DIGEST named Mark Leibovit the #2 Gold Timer for the 10 year period ending 12/31/09!

The weekly VR Gold Letter focuses on Gold and Gold shares. The letter is available to Platinum subscribers for only an additional $50 per month and to Silver subscribers for only $70 per month. Email me at mark.vrtrader@gmail.com.

Special offer from Mark Leibovit for Money Talks only: The intense analysis of Gold in the 10-12 page The VR Gold Letter is right now 75% off for the first month or $29.95 (regularly $125.00 a month). Go HERE and use the Money Talks promo code CBC12210

TIMER DIGEST signals for Stocks, Gold and Bonds are available to Platinum subscribers on the Home Page. TIMER DIGEST is an independent ranking service and newsletter. VRtrader.com, Inc. and TIMER DIGEST have no affiliation.

TIMER DIGEST has named Mark Leibovit of VRTrader.com ‘TIMER OF THE YEAR’ for 2006 and was named the #2 Timer for 2007.

As of January 25, 2010, TIMER DIGEST has named Mark Leibovit the 7th Market Timer for the 5 year period ending 12/31/09; the 3rd Market Timer for the 8 year period ending 12/31/09 and the #2 Market Timer for the 10 year period ending 12/31/09.

More kudos – Mark Leibovit was named the #1 Intermediate Market Timer for the 10 year period ending in 2007; the #1 Intermediate Market Timer for the 3 year period ending in 2007; the #1 Intermediate Market Timer for the 8 year period ending in 2007; and the #8 Intermediate Market Timer for the 5 year period ending in 2007. NO OTHER ANALYST SURVEYED APPEARED IN ALL FOUR CATEGORIES FOR INTERMEDIATE MARKET TIMING AS PUBLISHED IN TIMER DIGEST JANUARY 28, 2008!

Mark Leibovit was also named the #1 Gold Timer for the one-year period ending March 25, 2008. Most recently, from: 12/26/08 to: 03/27/2009, he is ranked in the #5 position for 3 month return.

For a trial Subscription of The VR Silver Newsletter covering Stocks, Bonds, Gold, US Dollar, Oil CLICK HERE

The VR Gold Letter is available to Platinum subscribers for only an additional $20 per month, while for Silver subscribers the price is only an additional $70.00 per month. Prices are going up very shortl, so act now! Separately, the VR Gold Letter retails for $1500 a year! The VR Gold Letter is published WEEKLY. It is 10 to 16 pages jam-packed with commentary and charts. Please call or email us right away. Tel: 928-282-1275. Email: mark.vrtrader@gmail.com .

Richard Russell snippet

Dow Theory Letters

Mar 1, 2010

March 1, 2010 — The IMF is about to sell its remaining hoard of 191 tonnes of gold.

China has far less in gold reserves than it would like, and I wonder whether China has

not already negotiated to gobble up the whole IMF offering.

The US has 8000 metric tons of gold. Some like Jeremy Siegel of Penn’s Wharton’s

School, think we should sell our gold. But even the thought of the US selling its gold

would drive the price down. It would also be blaring signal of US weakness. The

president can authorize the Treasury to sell US gold but that hasn’t happened since

1979. But even if Obama authorized the sale of US gold, he couldn’t spend the money

on health care or defense or anything else. US law requires that any funds received

from the sale of gold must go to paying down the national debt. Another thought is

that even if all US gold was sold, it wouldn’t make a dent in the US’s intimidating

$12.3 trillion debt.

….read more HERE

Chris Potter Eyes Opportunities in Appetites for Energy and Food

For environmental, financial and political reasons—not to mention to satisfy an energy-hungry world—Northern Border Capital Management founder Chris Potter sees some interesting opportunities for investors in alternative fuels on the horizon. One of his picks is a company using plasma gasification technology to produce clean-burning fuels. In this exclusive Energy Report interview, Chris also explains why he’s bullish on natural gas. Politically incorrect though natural gas may be, he isn’t overly worried about North America’s abundant supply finding a home. Agribusiness is yet another arena that appeals to Chris, from the potential for domestic potash production for Brazil’s huge agricultural sector to the extraction of protein from canola seeds to help feed the planet’s growing population.

The Energy Report: You focus on small-cap resource companies based in Canada. How did you come to specialize in that?

Chris Potter: I focus on Canada because the market there is less efficient. In general, I like to find companies that have small share structures, where there is a world-class product or asset, where management owns a lot of the stock and where there’s a compelling valuation. In my experience there are more opportunities in Canada that possess all of those characteristics. In the resource sector I like the exploration companies and early-stage producers because if you pick the right ones, you get a lot more leverage to rising commodity prices than you do with the larger companies.

TER: As I understand it, you consider the Canadian market somewhat less efficient than the U.S. market, thus making it easier to uncover attractively valued companies. What do you think accounts for the discrepancy, and is it specific to small caps or also true of large caps?

CP: It’s really true of both large caps and small but it’s not a permanent discrepancy. It’s more of a lag. What I mean is that U.S. investors take a lot longer to recognize and buy high-quality Canadian companies than U.S.-listed ones. I used to be concerned that this lag would somehow be arbitraged away, but I’ve been doing this now for 12 or 13 years, and it has not.

There are a lot of reasons behind that. For one thing, there seems to be an apathy or ignorance on the part of U.S. investors about almost everything Canadian. There’s also a perception that the Canadian securities laws are lax, that its investment community is run by mining promoters, and that U.S. investors won’t get a fair shake up there. While there are certainly landmines to look out for when investing in Canada, they are no more dangerous than those in the U.S.

To characterize the entire Canadian investment scene as corrupt because of parts of the Vancouver mining community and the Bre-X Scandal in the late ’90s is just silly and ignores the fact that the U.S. has had plenty of its own investment scandals such as Enron and a banking system that perpetrated the greatest financial fraud in history this past decade.

But I can’t tell you all of the reasons for the valuation lag that I continue to see between U.S. and Canadian companies.

TER: You just know it’s there.

CP: Let me tell you about the greatest example of that in my experience—and the reason I started investing in Canada. Back in 1997, Sprott Securities (now Cormark Securities) introduced me to Research In Motion Limited (TSX:RIM; NASDAQ:RIMM). No one other than Sprott and a few others understood what these guys had— I’m just glad I was in the right place at the right time to take the meeting. Here was this little Canadian company trading at $4 a share. Split-adjusted that would probably be $1 today. It had $2 a share in cash and $2 a share in backlog. But it had a technology that revolutionized the way people communicate.

TER: Right.

CP: They gave us the Blackberry—and no one was paying attention. Here was this little company in Waterloo, Ontario, developing this unbelievable technology. Its market capitalization was miniscule. Had Research In Motion been in Silicon Valley, its valuation would have changed very, very rapidly, but we had six months to do our homework on it before anyone really cared.

TER: Wow! That’s really a great story, like finding a Rembrandt in your garage.

CP: Exactly.

TER: You’ve been very positive on gold and precious metals. What other sectors do you think will do well for investors over the next couple of years?

CP: I think that many areas of alternative energy will do well. That does not mean that all the alternative energy companies whose stocks go up will be developing worthwhile, commercial products or resources. On the contrary, I suspect that many of them will end up being duds. It’s just that coal, oil and even natural gas have become so politically incorrect that the amount of money that will get thrown at the alternative energy sector will make most of those stocks go up, for a while at least.

I expect to see opportunities in the natural gas sector, too. Even though it’s not a politically correct fuel, I don’t see how it won’t take a greater share of the North American energy market going forward. What other fuel combines abundant availability and low production costs with an emissions profile that is palatable to even hard core environmentalists? As coal and oil get squeezed out on the margin I’m guessing natural gas will fill much of that gap. There is a lot of bearishness surrounding the massive increase in North America’s natural gas supply coming from shale plays. While I agree that shale gas supply will make it difficult for us to see sustainable double-digit gas prices for many years to come, the positive developments on the demand side that I just described can keep gas prices in the $5 to $7 range and there are a lot of gas explorers and producers that will do very well in that kind of price environment.

I also think we’ll continue to see lots of opportunity is the agricultural sector. This is for the reasons that we all know about—emerging market population migration, improvements in diet, a greater focus on investing in fertilizers and other crop inputs.

TER: Are you following any small-cap companies that represent some interesting investment options in these sectors—alternative energy, natural gas and agribusiness?

CP: In agriculture, I have an investment in Amazon Mining (TSX-V:AMZ). For anyone concerned about the rainforest, Amazon’s property is nowhere near the Amazon jungle. They are developing a potash fertilizer resource in Brazil, one of the world’s leading producers of all kinds of crops—soybeans, corn, wheat, coffee, oranges, sugar cane. Despite its reliance on agriculture, Brazil imports more than 90% of its domestic fertilizer needs from places such as Russia and Canada. This means high transportations costs, which is the reason Brazil pays more for potash than anywhere else in the world. This hurts farmers, increases food costs and is bad for the country. It’s not difficult to see why all of the players in the Brazilian agricultural space are intensely focused on securing a domestic source of production.

So along comes this little Canadian-listed company that stumbles across a very large potash resource in the heart of the Brazil’s growing area. Not only does is address the transportation cost issue but the particular kind of potash they found is much better suited to Brazil’s soil than the kind they have been importing. It has a slow release feature which means it stays in the soil longer than traditional potash. This is particularly important given Brazil’s heavy rains and its nutrient deficient ground. Finally, because the resource is at surface, the company believes it can develop a mine for one tenth of the $1 to $2 billion it would cost to build a mine in Canada.

TER: Wow!

CP: Yup, it’s pretty unusual. You have this tiny company, $60 million market cap, that has the opportunity to significantly improve the economics of one of the world’s major agricultural regions. It’ll take a couple of years to get into production and there will be many of the issues associated with building a new mine but they have a very talented, driven management team that is focused on making this project work. Equally important they have the support and backing of domestic industry, politicians and farmers. Management has kept the share structure small and they have kept a tight lid on costs which saved them during last year’s financial crisis. They also have bought a significant amount of stock for themselves in the open market which I like to see.

TER: Do you see any other companies that represent promising plays like Amazon’s?

CP: I have an investment in BioExx Specialty Proteins Ltd. (TSX-V:BXI), which has developed a unique technology for extracting protein from canola seeds. Canola has twice the protein profile as soy and is almost on par with beef and egg whites. BioExx is the first company to figure out how to efficiently unlock the protein from the seed without damaging the protein in the process. Their first plant is up and running and they have a pretty aggressive growth plan, with five plants running within a few years, each successive plant doubling capacity from the previous one.

TER: Would this protein be for human consumption? Animal consumption? What?

CP: The whole focus of the company is upon extracting protein from canola for human foods and their ability to do that is what distinguishes what they are doing from everyone else in the field. They still need to scale their processes and get their final regulatory clearances but the analysts are suggesting they will have human quality food production sometime this year. This is another company with a tiny market cap relative to its opportunity. It is a $300 million company that will be diving into a $16 billion market with highly proprietary technology that is way ahead of its competitors.

TER: Fascinating. Any nuggets to share in terms of alternative energy or natural gas?

CP: Alter NRG Corp. (TSX:NRG; OTCQX:ANRGF) is another company I own. They have a proven plasma gasification technology, developed by Westinghouse, that can turn all kinds of readily available and environmentally unfriendly substances like garbage, biomass and old tires into clean burning fuel. All of their competitors are either in the R&D stage or are working on giant projects that cannot handle the variety of feedstocks that Alter NRG can. I don’t fully understand the technology but I understand that a business that can turn household garbage into clean-burning fuel is a pretty good bet today, especially given the fact that they have a couple of plants already in commercial production and the whole company trades for about $130 million with over $30 million in cash. This is another example of a Canadian-listed company with a game- changing technology that has yet to attract investor attention.

Christopher K. Potter is the principal of Northern Border Capital Management, Inc., a Canadian-focused firm that he founded in 2002. A 1987 graduate of Hamilton College in Clinton, NY—which earned a place on U.S. News & World Report’s “Best Colleges 2010” list of Tier 1 liberal arts institutions— in 1988 he went to work for Preferred Utilities Manufacturing Corp., a leading combustion equipment design firm. By the time he left to study for his MBA at Columbia University, Chris was managing Preferred Utilities’ New York office. After being awarded his master’s degree, he joined Ten Squared L.P., a hedge fund focused on North American publicly traded securities. He was an investment analyst with the fund from 1996 until 1999 and the co-portfolio manager from 1999 until 2001. It was his last three years at Ten Squared, when he developed and managed the fund’s Canadian investment business, that led Chris to found Northern Border Capital Management, Inc.

Want to read more exclusive Energy Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Expert Insights page.

.…go directly to the Market Letter HERE

Market Comment

For the month of January, the S&P 500 ended up with a loss of 3.7% and S&P/TSX with a loss of 5.5%. January is typically positive and often used to gauge the mood of investors. The mood was anything but positive as the market suffered a one-two-three-four punch combination.

The first punch occurred on January 12th when the People’s Bank of China (PBoC) instituted a tightening monetary policy by raising banks’ required reserve ratio by a half-point. This was PBoC’s first meaningful move to tighten monetary policy in eighteen months. This was an attempt to cool the country’s 10.7% growth rate and to try to put a damper on rising commodity prices of which China is a large consumer.

The second punch was Obama introducing regulation to control bank operations and to separate banking and financial divisions with banks. Although most agree that there needs to be some reform in the banking sector, the regulations introduced were reminiscent of the controlling Glass-Stegall laws of the 1930s.

The third punch was India tightening its monetary policy on January 29th, raising its cash reserve requirement for banks by 75 basis points to 5.75%. This increase was put in place to try and calm rising inflation in the country. India also warned that its next move will be an increase in interest rates.

The fourth punch has the rising risk of a possible default by the Greek government on its debt obligations. Although an imminent default is not likely, expect the Euro to come under pressure as more Euro countries face their high debt problems, such as Spain and Portugal.

There is currently a divergence between the North American economy and the sovereign debt issues of Europe. Earnings have been improving, employment has been increasing, the economy has been growing and at the same time the world has been focusing on the quagmire of the sovereign debt issues. If and when Europe is able to satisfactorily address the debt issues the market will swing

back to looking at the positives and will respond by moving upwards.

…..read more HERE

SIGN UP for the FREE monthly THACKRAY MARKET LETTER HERE

Brooke Thackray is President of alphaMountain Investments, a firm that publishes investment reports and books. The main goal of the publications is to use seasonal analysis to give investors and money managers an edge in the markets.

– The Thackray Market Letter — Know Your Buy & Sells a Month in Advance —Individual stocks and Indexs analysed.

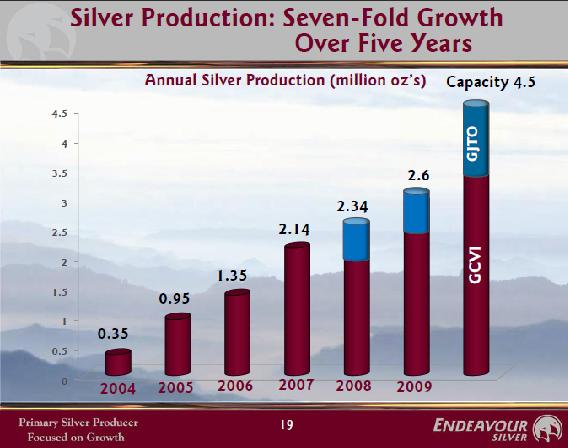

Endeavour Silver Corporation (EXK) announces that it has acquired an option to purchase the San Sebastián silver-gold properties in Jalisco State, Mexico from IMMSA (Grupo Mexico), one of the largest mining companies in Mexico.

San Sebastián del Oeste is an historic silver and gold mining district located in south-western Jalisco State, approximately 155 kilometres (km) southwest of Guadalajara and 40 km northeast of Puerto Vallarta, accessible by paved and gravel roads. One small, high grade, underground silver-gold mine, Santa Quiteria (75 tonnes per day), continues to operate in the district. The San Sebastián properties being acquired by Endeavour surround the Santa Quiteria mine and represent a new, district-scale, silver-gold exploration opportunity for the Company.

The San Sebastián properties (3,320 hectares) cover a classic, low sulfidation, epithermal vein system in four mineralized vein sub-districts named Los Reyes, Santiago de los Pinos, San Sebastián del Oeste and Real de Oxtotipan. Each sub-district consists of a cluster of quartz (calcite, barite) veins mineralized with sulfide minerals (pyrite, argentite, galena, and sphalerite). Each vein cluster spans about a 3 km by 3 km in area. In total, more than 50 small mines were developed historically within at least 20 separate veins.

As we can see from the news flow Endeavour are not allowing the grass to grow under their feet as the securing of this option to purchase clearly demonstrates. Find the time to walk through their recent presentation by Brad Cooke its very informative and its time well spent in our humble opinion, please click this link.

If you don’t already own their stock then start accumulating and buy on dips, such as this one. Endeavour is appearing on a silver screen near you as it trades in Canada, United States and Germany on the following Stock Exchanges:

EXK: NYSE-Amex,

EDR: TSX,

EJD: DB-Frankfurt,

EDR.WT: TSX)

Endeavour closed today in NYC at $3.30, up 4.76% on the a day.

All the best.

Got a comment then please add it to this article, all opinions are welcome and appreciated.

For those interested in Options Trading please click here.

To stay updated on our market commentary, which gold stocks we are buying and why, please subscribe to The Gold Prices Newsletter, completely FREE of charge. Simply click here and enter your email address.

For those readers who are also interested in the silver bull market that is currently unfolding, you may want to subscribe to our Free Silver Prices Newsletter.

For those readers who are also interested in the nuclear power sector that is currently coming back to life, you may want to subscribe to our Free Uranium Stocks Newsletter, just click here.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair