Market Opinion

As Americans observe the chaos in Greece, most assume that the strength of our currency, the credit worthiness of our government, and the vast expanse of two oceans, will prevent a similar scene from playing out in our streets. I believe these protections to be illusory.

Once again the vast majority fails to see a crisis in the making, even as it stares at them from close range. Just as market observers in 2007 told us that the credit crisis would be confined to the subprime mortgage market, current analysts tell us that sovereign debt problems are confined to Greece, Spain, Portugal, and perhaps Italy. They were wrong then, and I believe that they’re wrong now.

During the housing boom, subprime and prime borrowers made many of the same mistakes. Both groups overpaid for their homes, bought with low or no down payments, financed using ARMs instead of fixed rate mortgages, and repeatedly cashed out appreciated home equity through re-financings. The market largely overlooked the glaring similarities, and instead merely focused on FICO scores. Yes, prime borrowers had better credit, but their losses on underwater properties were no less devastating. As the magnitude of home price declines intensified, prime borrowers defaulted in levels that were almost as high as the subprime crowd.

So when mortgage backed securities started to go bad, it wasn’t as if the problems emanated in subprime and subsequently “contaminated” the rest of the market. All borrowers were infected with the same disease, but the symptoms merely expressed themselves sooner in subprime. The same is true on a national level, whereby Greece plays the part of the subprime borrower. Though the U.S. is considered to be the highest order of “prime” borrower, based on historic precedent, our debt to GDP levels are at crisis levels, and are not that much lower than Portugal or Spain. When off-budget and contingency liabilities are properly accounted for, one could argue that we are already in worse financial shape than Greece.

Most importantly, like Greece (and homeowners who relied on adjustable rate mortgages), we have a high percentage of short-term debt that is vulnerable to rising rates. The one key difference is that while Greece borrows in euros, a currency it cannot print, America borrows in dollars, which we can print endlessly. In reality however, this is a distinction with very little substantive difference.

What if Greece had not been a member of the euro zone and had instead borrowed in their former currency, the drachma? First, given its past history of fiscal shortfalls, Greece would not have been able to borrow nearly as much as it had (They may well have been forced to borrow in euros anyway). Under those circumstances, creditors would have been more reluctant to lend without the possibility of a German led bailout. Had Greece never adopted the euro as its currency, but nevertheless borrowed in euros, it would now face the same difficult choices, but would not be offered the carrots or sticks provided by other euro zone nations that are worried about the integrity of their currency. The IMF would have been Greece’s only possible savior.

Many of our top economists now argue that all would be well in Greece if the country was in charge of its own currency. In such a scenario, Greece would indeed have had no problems printing as many drachmas needed to pay its debts. However, would this really be a “get out of debt free” card for Greece?

The main reason the Greeks are protesting in the streets is that they do not want their benefits reduced or taxes raised to repay foreign creditors. But despite the likely domestic popularity of a drachma-printing policy, would it really get the Greeks off the hook? They would stiff their creditors by repaying them in currency of diminished value. But the same result could be achieved through an honest debt restructuring, which would involve “haircuts” for all creditors. In a restructuring, the pain falls most squarely on those who foolishly lent money to a “subprime” borrower.

But with inflation it’s not just foreign creditors who would suffer. Every Greek citizen who has savings in drachma would suffer. Every Greek citizen who works for wages would suffer. Sure nominal benefits are preserved and taxes are not raised, but real purchasing power is destroyed. If the cost of living goes up, the reduction in the value of government benefits is just as real.

Of course, the negative effects on the economy of run-a-way inflation and skyrocketing interest rates are worse than what otherwise might result from an honest restructuring or even out right default. It is just amazing how few economists understand this simple fact.

Just because we can inflate does not mean we can escape the consequences of our actions. One way or another the piper must be paid. Either benefits will be cut or the real value of those benefits will be reduced. In fact, it is precisely because we can inflate our problems away that they now loom so large. With no one forcing us to make the hard choices, we constantly take the easy way out.

When creditors ultimately decide to curtail loans to America, U.S. interest rates will finally spike, and we will be confronted with even more difficult choices than those now facing Greece. Given the short maturity of our national debt, a jump in short-term rates would either result in default or massive austerity. If we choose neither, and opt to print money instead, the run-a-way inflation that will ensue will produce an even greater austerity than the one our leaders lacked the courage to impose. Those who believe rates will never rise as long as the Fed remains accommodative, or that inflation will not flare up as long as unemployment remains high, are just as foolish as those who assured us that the mortgage market was sound because national real estate prices could never fall.

Click here for a description of my best selling just-released book How an Economy Grows and Why it Crashes. For in-depth analysis of this and other investment topics, subscribe to The Global Investor, Peter Schiff’s free newsletter. Click here for more information.

Peter Schiff C.E.O. and Chief Global Strategist

Euro Pacific Capital, Inc.

10 Corbin Drive, Suite B

Darien, Ct. 06840

800-727-7922

www.europac.net

schiff@europac.net

Mr. Schiff is one of the few non-biased investment advisors (not committed solely to the short side of the market) to have correctly called the current bear market before it began and to have positioned his clients accordingly. As a result of his accurate forecasts on the U.S. stock market, commodities, gold and the dollar, he is becoming increasingly more renowned. He has been quoted in many of the nation’s leading newspapers, including The Wall Street Journal, Barron’s, Investor’s Business Daily, The Financial Times, The New York Times, The Los Angeles Times, The Washington Post, The Chicago Tribune, The Dallas Morning News, The Miami Herald, The San Francisco Chronicle, The Atlanta Journal-Constitution, The Arizona Republic, The Philadelphia Inquirer, and the Christian Science Monitor, and has appeared on CNBC, CNNfn., and Bloomberg. In addition, his views are frequently quoted locally in the Orange County Register.

Mr. Schiff began his investment career as a financial consultant with Shearson Lehman Brothers, after having earned a degree in finance and accounting from U.C. Berkley in 1987. A financial professional for seventeen years he joined Euro Pacific in 1996 and has served as its President since January 2000. An expert on money, economic theory, and international investing, he is a highly recommended broker by many of the nation’s financial newsletters and advisory services.

The Final Reckoning?

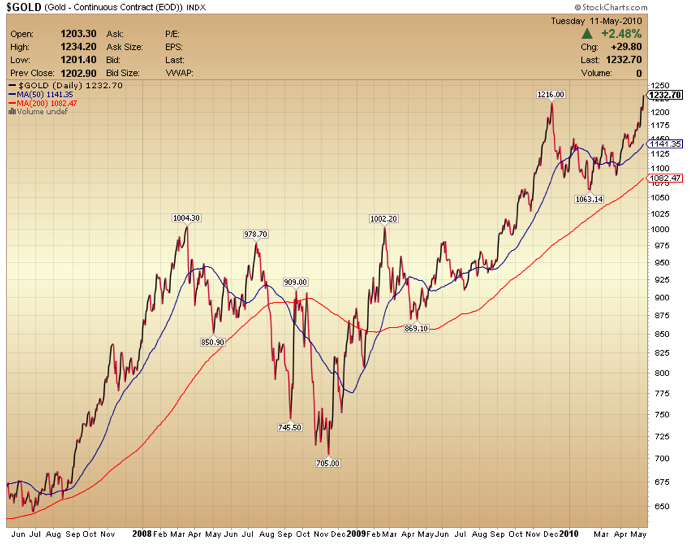

One look at Gold and you know something is very different this AM. This is definitely a lower left to upper right dynamic over the past three years. The appreciation from $650 to $1242 this AM is 91.1% or about 30% per year for each of the past three years. Even more surprising yesterday was the move in gold and silver (to $19.50 per ounce this AM) while the US dollar strengthened.

This is quite an unusual move and can only signal that gold and precious metals are being viewed as money substitutes. Even the resolute non-gold bug and friend Dennis Gartman said yesterday,

“The decision by the ECB to buy government debt, even though “sterilized” as the

Bank’s leadership says that those purchases shall be, will prove inflationary… or at least detrimental to the integrity of the currency itself. That process shall tend upon gold as gold becomes every day to be seen as the 2nd reservable “currency,” supplanting the EUR which had assumed that rule until quite recently on balance to put upward, perhaps relentless, pressure”.

It is true, of course, that gold and silver could correct. In fact it is inevitable that they will end in a parabolic crescendo. All assets correct at some point. Neither appears particularly extended here.

The reasons for the currency volatility, US dollar strength, Euro weakness and gold strength are obvious. All that debt in the OECD economies that has been used to save those “Too Big To Fail” is now finding its way to the sovereign debt level. Greece is, of course, the case study de facto. Greece’s plight is relatively small compared with debt and deficit ratios of Spain, Britain or the US. There really is no supra national authority that Greek defaulting sovereign debt can be pushed to. Furthermore, in the EU, it’s one for all and all for one if the union is to survive. It seems possible this AM, that the European Union and its currency the Euro may actually be disassembled.

The IMF/ EU rescue package is $970 billion. But where will this debt come from? Who will be the lenders of last resort? We see little Asian inclination to participate with the rescue of the Euro. The IMF seems loaned out. The Federal Reserve has extended US dollar swap lines, all this for the relatively small economy of Greece. One ramification is, of course, that a subset of the world is moving to gold and silver. Even more worrisome, this trillion dollar bailout is not nearly large enough to do the job except perhaps postpone the inevitable. As austerity measures begin to squeeze lifestyle in Greece, as they must, a nasty deflationary spiral will occur. Germans do not seem predisposed to a total Greek rescue. It does not seem possible that Greek public debt can be saved from ultimate default and that country can then grow out of its entitlement- induced torpor. Gold dynamics are simply recognizing this inevitability. However there is another dross lining to this event. It is the contagion that may ensue. Spain is a much bigger problem. Perhaps the UK and the US can inflate out of their self-induced debt by devaluing their currencies. Perhaps not.

To date the unwinding of the dollar carry has had somewhat the opposite affect, that of pushing the dollar higher and the Euro lower. Who wants Euros today? Hence the need for the Fed’s recent swap lines to supply the world with US dollars. As long as the Bernanke Fed keeps overnight rates low bubbles will be spawned through the dollar carry trade. Unwinding this carry will also be painful. Would raising US rates be more or less painful than the course now charted by our central bank and the Obama Administration? I do wonder if anyone in Washington really sees the likely outcome of this mess.

I am predisposed this AM to make a call. For the past two years I have been neutral on the inflation / deflation call. I’ve called it a tug of war. The US Fed (where I lectured last week) cheering for an inflation.

I think deflationary forces will now have the upper hand in the world. That would carry with it all sorts of implications. The barbell strategy is one to consider along with the discovery approach. As growth slows and sovereign defaults approach numerous austerity programs will be necessary. Owning cash and gold/silver (the barbell) will be an excellent way to counter the coming deflation. Of course I could be wrong. But there does seem to be an overwhelming potential for dissolution of the EU and a painful deflationary scenario that could last, as Rogoff and Reinhardt contend, for several years..

Gold is not reacting to inflationary expectations. Yesterday Goldcorp, my large cap pick, was up significantly.

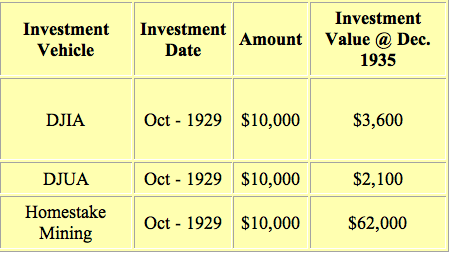

Could Goldcorp be the Homestake of the new millennium?

Sign Up for Michael Berry’s free daily letter HERE

The material herein is for informational purposes only and is not intended to and does not constitute the rendering of investment advice or the solicitation of an offer to buy securities. The foregoing discussion contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 (The Act). In particular when used in the preceding discussion the words “plan,” confident that, believe, scheduled, expect, or intend to, and similar conditional expressions are intended to identify forward-looking statements subject to the safe harbor created by the ACT. Such statements are subject to certain risks and uncertainties and actual results could differ materially from those expressed in any of the forward looking statements. Such risks and uncertainties include, but are not limited to future events and financial performance of the company which are inherently uncertain and actual events and / or results may differ materially. In addition Dr. Berry may review investments that are not registered in the U.S. He owns shares and in Goldcorp, Senesco Technologies, Natural Blue Resources, Horseshoe Gold, Derek Oil and Gas, Terraco Gold, Neuralstem, Piedmont Mining, MegaWest Energy, CGX Energy, Solares Lithium and Quaterra Resources. Dr. Berry is a paid advisor to Revett Minerals. We cannot attest to nor certify the correctness of any information in this note. Please consult your financial advisor and perform your own due diligence before considering any companies mentioned in this informational bulletin.

After last week’s action, “sell in May and go away” doesn’t look all that bad at the moment. But if one did, where would one go: cash, U.S. Treasuries, U.S. Dollar, gold? And if one did, when do you come back…if at all?

Remembering that I put my pant legs on one leg at a time like everybody else, I will try to paint the big picture and also comment on selected model portfolio stocks and Grandich client companies.

…..read more HERE

What was that all about? Chaos prevailed on world equity markets yesterday and it continued into overnight trading in Asia and Europe. The Dow Jones Industrial Average plunged 700 points in the 15 minute period after 2:40 PM EDT . Was it panic selling or a technology glitch? Probably both! Stop loss selling triggered an avalanche. The recovery was equally eerie. U.S. exchanges cancelled selected transactions between 2:40 PM and 3:00 PM where transactions either rose or fell by more than 60%. One thing is certain: Investor confidence in equity markets was significantly damaged. One of the best measures of the fall in confidence was technical action by the VIX Index. The spike in VIX suggests that confidence is unlikely to return to equity markets in the short term.

U.S. equity index futures continued to recover from a deep sell off. S&P 500 futures added 5 points in pre-opening trade despite overnight losses by equity markets in Asia and Europe. Citigroup gave European market a bearish start with a prediction that fears of sovereign debt contagion over Greece could trigger a near-term correction of up to 20%.

Interesting reactions to the U.S. April employment report released this morning at 8:30 AM EDT! Consensus was an increase in non-farm payrolls to 180,000 from 162,000 in March. Actual was an increase to 290,000. In addition, the March report was revised upward to 230,000. However, the rest of the report was less positive. Consensus for April Hourly Earnings was an increase of 0.1%. Actual was no change. Consensus for the April unemployment rate was unchanged at 9.7%. Actual was an increase to 9.9%. Initial reaction to the report by S&P 500 futures was a slight upward move to a gain of 10 points. However, profit taking quickly re-entered and futures moved lower.

Great news on employment in Canada! Canada added 108,700 jobs in April, the largest monthly gain since August 2002. Consensus was 24,000. Canada’s unemployment rate also slipped 0.1% to 8.1%. The Canadian Dollar immediately gained 1.00 U.S. cents on the news to 96.04 cents U.S. . The news raised speculation that the Bank of Canada will raise its overnight lending rate to major banks in June.

The London FT Index is mixed this morning following the election in the United Kingdom. The Tory party won the most seats, but do not have a majority. Negotiations between the three major parties will occur over the next week to determine who will govern.

Canadian investment dealers are not giving up on the Canadian energy sector. This morning TD Newcrest upgraded Canadian Natural Resources from Hold to Buy.

Alcoa added 2% after BMO Capital upgraded the stock from Market Perform to Outperform. Target price is $15.

EquityClock.com’s stock of the day

Technical analysis: A great gold stock – Great Basins Gold (GLG)

http://www.equityclock.com/2010/05/06/a-great-gold-stock-technical-analysis/

Weakness entered U.S. equity markets well before the computer generated meltdown at 2:40 PM EDT. The initial trigger was a break by major North American equity indices below their 50 day moving averages on Wednesday. The break prompted additional technical selling at the opening yesterday.

Charts published on equity chart services (e.g. www.stockcharts.com ) on individual equities are inaccurate due to the cancellation of trades. A full update on technical indicators will be offered in Monday’s Tech Talk after transaction adjustments have been completed.

……read more HERE (scroll down) for Brooke Thackray on BNN, EquityClock.com Reports Released Yesterday Market panics – Gold sought as safe haven: and Adrienne Toghraie’s “Traders Coach” column

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair