Market Opinion

Junior braces for life without Kennecott at Whistler project

Investors can expect to see a flurry of reports on Kiska Metals Corp. (TSX: T.KSK, Stock Forum) as the junior gears up for some key developments that will influence the pace of exploration at its flagship Whistler copper-gold project in Alaska.

Last week, Stockhouse joined a group of investment newsletter writers on a helicopter tour of a 527 square kilometer exploration site that is located in the heart of bear-hunting country about 150 kilometres northwest of the city of Anchorage.

In the coming weeks, it will be the turn of analysts from Canaccord/Genuity and Union Securities Ltd. to take the 40-minute float plane ride from Anchorage to a 60-person camp site, which is not accessible by road.

Kiska President and Chief Executive Officer Jason Weber is playing host in a bid to prepare the market for two key milestones.

One is the possibility that Kennecott Exploration Inc. – a subsidiary of Rio Tinto Plc NYSE: RTP will elect not to exercise back-in rights that would allow the U.S. company to earn a 60% stake in the project, leaving Kiska with the other 40%.

The second is planned financings that Weber hopes will raise up to $15 million for exploration at Whistler.

In an interview, Weber said he believes the lack of clarity concerning the ownership structure has been an overhang on Kiska’s stock price – which traded at 85 cents on Tuesday. It is why the company is waiting anxiously for Kennecott to make its intentions known.

“The direction of the decision is less important than the actual decision itself,’’ said Weber, adding that he can see the merits of continuing to have a strong partner with deep pockets.

“But if they walked away, I see a tremendous opportunity for us to build value at the project,’’ he said.

When Stockhouse visited the Kiska camp last week, the company was focusing on a cluster of targets, all of which lie within 25 kilometres of Whistler, the project’s only defined deposit so far.

Essentially, Kiska is exploring the same geological belt as the giant Pebble copper-gold discovery, which is being developed in southwestern Alaska by Northern Dynasty Minerals Ltd. TSX: T.NDM and Anglo American Plc OTO: AAUKY

Pebble has an estimated resource of 5.94 billion tonnes in the measured and indicated category, containing 55 billion pounds of copper, 66.9 million ounces of gold, and 3.3 billion pounds of molybdenum. A further 4.84 billion tonnes is listed in the inferred category, containing 25.6 billion pounds of copper, 40.4 million ounces of gold. and 2.3 billion pounds of molybdenum.

By comparison, Whistler has an indicated resource of 30 million tonnes, grading 0.87 grams per tonne gold, 2.46 grams per ton silver, and 0.24% copper as well as an inferred resource of 134 million tonnes, grading 0.64 grams per tonne gold, 2.18 grams per tonne silver, and 0.20% copper).

That amounts to an estimated 5.75 million gold equivalent ounces.

However, with a new Whistler resource estimate due in November the company is working on a theory that the property is host to a number of gold-copper porphyry systems, of which Whistler is just one example.

For instance, it has a drill rig set up on the steep slopes of its Island Mountain discovery, which is located 23 kilometres to the south of Whistler and hosted within a 4.5 by 3.0-kilometre area of anomalous gold-copper soil and rock geochemistry.

In early July, the company said a drill hole located about 50 metres from the discovery hole intersected two zones of gold mineralization. The upper zone averages 0.70 grams per tonne gold; 2.5 grams per tonne silver and 0.16% copper over 129.8 metres, starting at a depth of 31.2 metres.

A lower gold-only intersection averaged 0.78 grams per tonne gold over 151.6 metres, beginning at a depth of 23.5 metres.

“We still have a lot to learn about this area,’’ said Weber, who is hoping to build inferred tonnes and ounces through continued drilling.

In order to fulfill its obligations to Kennecott, Kiska has spent about $8.5 million to complete 23 holes along what is known as the Whistler corridor area.

Aside from drilling on Island Mountain, the company has been probing targets in an area known as Round Mountain about 10 kilometres north of the Whistler deposit and in the Raintree East area about three kilometers northeast of Whistler.

Inside the camp, speculation is rife that the mineralization in the main Whistler deposit and other nearby discoveries is not sufficiently rich in copper to attract the interest of Kennecott, which retains a 2% net smelter return royalty stake in the project, even if it walks away.

However, the project will remain in limbo until Kiska senior geologist Mike Roberts delivers a final report to Kennecott, likely in early August.

If Kennecott opts to back in, it will need to reimburse Kiska for 200% of its exploration expenses, an amount that is expected to reach a minimum total of $25 million. Should it decide to stick around, the U.S. company would also be required to advance the project to the production stage in order to earn a 60% stake in the property.

But with Kennecott out of the picture, Kiska would look to bolster its treasury by doing another round of financings, possibly in the fall. “I’m thinking $10 to $15 million, and likely bigger,’’ said Weber.

Meanwhile, it is clear that project geologists will have to come up with a lot of metal to justify the cost of developing a road and power infrastructure in what is essentially a pristine wilderness area, comprised of mountains, lakes and wetlands.

Kiska officials say the chances of Whistler being developed may improve if partners NovaGold Inc. TSX: T.NG and Barrick Gold Corp. TSX: T.ABX proceed with a plan to build a 525-kilometre natural gas pipeline in a bid to deliver power to the proposed Donlin Creek gold mine in northwestern Alaska.

It is expected that the pipeline would run from upper Cook Inlet on Alaska’s southwest coast to the project site, possibly crossing an area near the Whistler claim block along the way.

By using natural gas instead of a combination of wind power and diesel, NovaGold says it expects to reduce the cost of power, which accounts for about 25% of the project’s total operating costs.

“If that goes through, that changes the whole picture,’’ said Weber.

If it doesn’t, the company would look to other options including potential connections to a proposed power generation at Chakachamna Lake, which is located the southwest of the exploration site.

If Whistler proves to be economic, Kiska would need to build a 55-mile road, allowing concentrates to be shipped to the natural gas port at Tyonek. However, it would appear that Kiska still has a lot of work to do before it can start to think about developing infrastructure.

For the time being, the company will focus on expanding the main Whistler deposit and other nearby discoveries. “We want to see how big that these things really are,’’ said Weber.

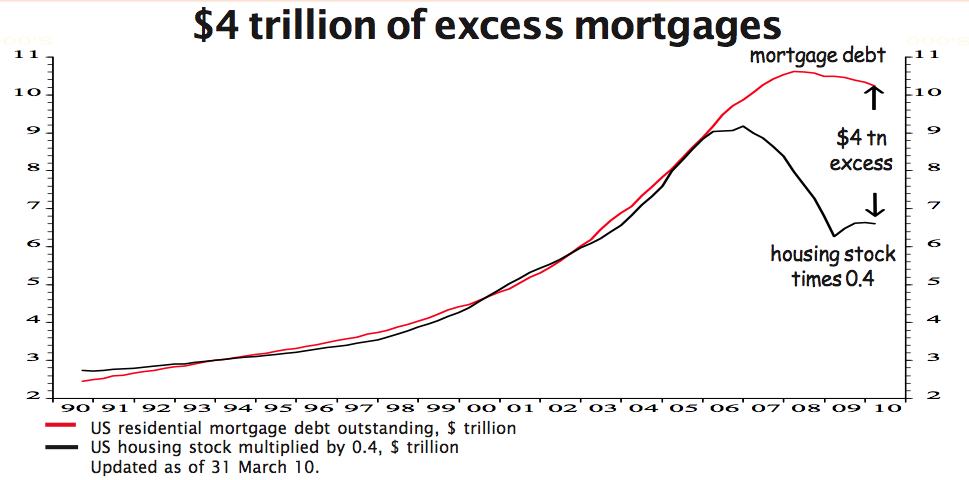

“Can the US economy really return to “business as usual” when it has 4 million houses surplus to requirement, when 1 out of 4 mortgages are in negative equity, and when by our calculation, it is burdened with $4 trillion of excess mortgage debt, equivalent to 30% of GDP?”

I have been covering the US Real Estate market for decades. I grew up with RE (mom was a RE broker and an investor). I have been a housing bear for about 5 years. I recognized the credit bubble and inevitable bust long before most other analysts/strategists/economists did.

I mention this just to inform readers that it is very rare that I come across any housing analysis that surprises me or adds to my understanding of the real estate landscape in a major way.

Which is why I am so pleased to introduce you to Dhaval Joshi, Chief Strategist at London based hedge fund RAB Capital (and former Societe Generale and J P Morgan Strategist).

Dhaval’s analysis looks a variety of housing data relative to household formation, housing stock, vacancy rates, and inventory is not the typical housing review. It is quite illuminating.

Enjoy:

The $4 Trillion Dollar Question

Can the US economy really return to “business as usual” when it has 4 million houses surplus to requirement, when 1 out of 4 mortgages are in negative equity, and when by our calculation, it is burdened with $4 trillion of excess mortgage debt, equivalent to 30% of GDP?

For many years, total mortgage debt consistently and reliably equalled 0.4 times the value of the US housing stock. Intuitively, this average of 0.4 makes perfect sense as every property usually has a mortgage ranging from 0 to 0.9 times its value. So in 1990, $6 trillion of housing collateral could support $2.5 trillion of mortgages, and by 2006, $23 trillion of housing collateral could support $10 trillion of mortgages. But since then, the US housing stock’s value has slumped to $16 trillion which means the amount of mortgage lending supportable by the collateral has plunged to $6 trillion. However, actual mortgage debt has remained at $10 trillion – $4 trillion too high.

The fact that mortgage debt has barely declined suggests that relatively few homeowners have defaulted on their mortgages or paid off debt yet. Instead, a quarter of all borrowers are sitting on negative equity. That’s just as well – because were mortgage debt to shrink by even half of $4 trillion, the US economy would slump.

Perhaps homeowners are patiently expecting house prices to rise again. But if so, they may be in for a long wait. Prices are likely to be weighed down by a massive oversupply of homes relative to underlying demographic demand. Whether you look at the houses to population ratio, the houses to household ratio or vacant houses ratio, the conclusion is the same – there is a 3% surplus of properties, equivalent to 4 million homes. And with household formation running at just 0.9 million while the US is still building 0.6 million new homes annually, only 0.3 million of the oversupply will be absorbed per year (see page 5).

Ultra low rates to stay

A recent study by the Federal Reserve (The Depth of Negative Equity and Mortgage Default Decisions by Bhutta, Dokko and Shan) investigated the question: at what point do underwater homeowners “strategically default” on their mortgages? Surprisingly, it found that the average borrower doesn’t walk away from his home until negative equity reaches a very high level, -62%. But the fascinating thing was that there was something that could trigger underwater borrowers to default much, much earlier – and that something was an interest rate rise.

With a quarter of US mortgages underwater, and likely to stay that way for some time, the Fed must follow its own research if it wants to prevent a cascade of defaults. Hence, expect US interest rates to stay ultra low for an ultra long time.

…..many more interesting charts @ Question: Can the US overcome the Housing $4 Trillion Hangover?

The other great silver play in Mexico is Endeavour Silver, which Chris has written on as well.

Chris Berry: Endeavour is an interesting story. Their goal is to become a mid-tier silver producer, and when I say mid-tier, I mean 5 million to 10 million ounces per year. They have two main areas in Mexico where they mine and produce silver. One is Guanajuato and the other is Guanacevi. In May, I visited Guanajuato, and between the two areas, they have about 56 million ounces of silver between the proven and probable and inferred categories, 85% of which is mineable. The name of the game for them is to continue to make discoveries on their current high-grade properties, and basically, just acquiring more land to justify a higher valuation. I think they’re going to continue to do that, which is one of the reasons I like them.

“Michael Berry: We’ve spent a lot of time analyzing silver. I was involved in a big gold-silver find a few years ago, which was Penasquito, and that is now over a billion ounces of silver. I think silver is undervalued. Silver was the original money, if you will, that was used in the ancient days. The Greeks used silver from Laurion to defeat the Persians and restore democracy in Athens in the fourth century BC. When FDR sponsored the special silver purchase in 1934 some academics believe he broke the back of deflation. I think silver is very much undervalued, and it will be pulled along with gold. It’s very wise to have silver exposure, and with silver you can actually afford to own it in-kind. You can own silver coins. We’ve seen silver go from $4 maybe eight or nine years ago to about $18 today. Silver hasn’t performed quite as well as gold, but it’s moved up well.

Chris Berry: Silver’s one main difference from gold is that silver is an industrial metal as well as an investment metal. It sort of depends on your view of where you think the markets are going, but the “poor man’s gold” is certainly one way to accumulate hard assets and protect against some of these geopolitical hiccups.”

Silver Fever! Many people today are talking about silver’s undervaluation relative to gold. Numerous analysts see gold prices moving higher and with them silver prices. Several large organizations have forecast $20 to $25 per ounce silver by year end 2010. This is silver fever! A look back in history tells us that silver has been around much longer than any fiat currency and had a much larger geopolitical impact.

1. Silver Fever

2. Silver in Antiquity

More important, it imposed severe deflation on China, the only major country still on a silver standard, which brought forward in time and in increased severity subsequent war time inflation and postwar hyperinflation. The silver purchase program thereby contributed, though perhaps only modestly, to the ultimate triumph of the Communists.

Milton Freidman, Franklin D. Roosevelt, Silver and China, Journal of Political Economy 1992 Vol. 200

Silver Fever! Many people today are talking about silver’s undervaluation relative to gold. Numerous analysts see gold prices moving higher and with them silver prices. Several large organizations have forecast $20 to $25 per ounce silver by year end 2010. This is silver fever! A look back in history tells us that silver has been around much longer than any fiat currency and had a much larger geopolitical impact. As I was researching the other day, I came across an article from Time Magazine from May 1933. The title of the article … “Silver Fever!”

It seems President Roosevelt decided to increase the price of silver by allowing the Treasury to purchase 400,000,000 ounces of the white metal in 1933, above the market price. The idea here, in part was to raise silver’s price through a sequence of open market purchases and hence help drive the U.S. economy out of its deflationary funk by remonetizing silver. The Roosevelt Administration was interested in creating a silver monetary economy given the depth of the Depression. In April 1933 the President authorized the Treasury to pay $.71 per ounce when silver was selling for $.64. The world took note. Speculators bid the price of silver higher.

The U. S. had purchased about 400,000,000 oz. or about 1 ounce in every 30 thought to exist. This was however twice the world’s annual output. So the US government had effectively cornered the global silver market. Time’s editorial writes,

“Eager to profit from the corner, speculators helped the U. S. boost the world price to the U. S. price, 71¢. Last week when it reached that level, Franklin Roosevelt raised the ante for a second time, put the U. S. price at 77¢.”

Speculators then took the metal to $.81 per ounce very quickly. There were no sellers. Silver went bid globally. As Milton Freidman pointed out in his 1992 article (above) silver’s prospective monetary role in the US was destroyed. Perhaps the saying “Be careful what you wish for …” has much verity here. It is interesting to note however that the Roosevelt Administration saw the silver re-pegging of the US monetary system as a way out of the Depression.

Since the printing press has seemed ineffective in our present situation, we wonder how Dr. Bernanke might feel about remonetizing today?

But every action has an equal and opposite reaction. China had been the one country that had remained on a silver monetary standard. With Washington’s silver purchase program their currency values (Yuan) soared. Physical silver left China en masse. China actually put export controls on silver and appealed to “all patriotic….

…..read more SILVER FEVER!

Sales of gold coins and gold bars to the public rocketed in May to a record for a single month at 485,000 ounces. At the same time last year, the comparable figure was just 83,000 ounces – Australian Mint

“”The Golden Rule”: “Who has the gold, makes the rules”. And China is on a headlong path to accumulate as much gold as it can. China is now the world’s largest producer (miner) of gold, and all the gold mined in China must be sold to the government. What in the world could the Chinese be planning? Here’s what I’m thinking. The yuan will become the world’s most wanted currency, heavily backed by gold and a stable government plus the planet’s biggest military. In due time, China will be the new owner of the world’s reserve currency.” – Richard Russell Dow Theory Letters

“In the absence of the gold standard, there is no way to protect savings from confiscation through inflation. There is no safe store of value. If there were, the government would have to make its holding illegal, as was done in the case of gold. If everyone decided, for example, to convert all his bank deposits to silver or copper or any other good, and thereafter declined to accept checks as payment for goods, bank deposits would lose their purchasing power and government-created bank credit would be worthless as a claim on goods. The financial policy of the welfare state requires that there be no way for the owners of wealth to protect themselves.

“This is the shabby secret of the welfare statists’ tirades against gold. Deficit spending is simply a scheme for the confiscation of wealth. Gold stands in the way of this insidious process. It stands as a protector of property rights. If one grasps this, one has no difficulty in understanding the statists’ antagonism toward the gold standard.”by Alan Greenspan in 1967

Nightmare vision sparks rush for gold

Goldfinger, the villain of the eponymous James Bond film, hatched a plot to increase the value of his bullion by detonating a nuclear device inside Fort Knox, making America’s gold supply radioactive for 60 years.

No less exciting, though rather more unsettling, is the real-life drama taking place on the world’s financial markets, where investors have piled into gold on fears that capitalism is about to crumble.

As a result, the gold price has soared to record levels, rising 9 per cent this year to reach a peak of US$1264.90 ($1778.54) an ounce, with influential names in the world of finance predicting it could top US$2000. Among them is Jim Rogers, the investment guru who called the start of the commodities rally in 1999.

Having narrowly averted a financial Armageddon in 2008, investors are worried the authorities have transferred western indebtedness from banks and consumers to national governments.

In their worst moments, panicky investors and savers visualise a world that has been turned upside down by a sovereign debt crisis that breaks the euro and flattens the once mighty dollar. As the West sinks into a quagmire of its own making, demand plummets and the world is dragged into another Great Depression.

Even the emerging markets of China, India and Brazil are affected as export markets shrivel. Political instability follows, with riots on the streets and unemployment at levels not seen since the 1930s.

This nightmare vision has rattled investors around the word, driving the gold price ever higher. Of all the precious metals, it is the most popular as an investment.

Since the earliest times, it has been seen as both a symbol of prosperity and a store of wealth. In the modern era, it has been bought as a hedge against economic, political or social crises, and as protection against the plummeting value of currencies.

“Debt on government balance sheets and worries that the world could be heading towards a double-dip recession are behind the gold surge,” says Charles Cooper at Oriel Securities.

Cooper says there is concern we could be heading towards a second leg of the financial crisis and governments “could be tempted to print more money to dig us out of a hole”.

“That could precipitate inflation, making gold even more popular as a safe haven.”

Hundreds of kilometres away from Cooper’s offices in London, Kerry Tattersall, marketing director of Austrian Mint, is in ebullient mood.

Sales of gold coins and gold bars to the public rocketed in May to a record for a single month at 485,000 ounces. At the same time last year, the comparable figure was just 83,000 ounces.

Tattersall says: “This is an incredible time. We have had people coming into the mint and asking for advice on how to convert all their savings to gold. Not that we think that’s a good idea. We recommend customers have a diversified portfolio.”

The mint’s most popular product is its 1 ounce gold coin, which retails for about €1000 ($1770). Also on offer are 1 kilo gold bars that sell for €31,300. Silver is also growing in popularity, with Tattersall saying that sales have soared from 1 million ounces in May 2009 to 1.85 million now.

In Britain, Adrian Ash, head of research at BullionVault.com, says the company is looking after US$800 million worth of gold for its international clientele, up about 20 per cent on a year ago. “We are the beneficiaries of uncertainty which has grown since the Greek crisis,” he says.

The World Gold Council says shareholders are deepening their exposure to gold-mining companies and central banks are buying bullion on the open market. Marcus Grubb, WGC managing director, says: “The backdrop is the continuing financial crisis and people’s desire to protect their wealth in uncertain times.”

The Bank of England recently published figures that showed the value of gold in its vaults had risen from £72 billion ($152 billion) in early 2008 to £125 billion in February 2010. Much of the rise in value can be accounted for by the increase in the price, but analysts say there is evidence of central banks either stocking up on gold or deferring sales.

Britain would have far more in gold if former finance minister Gordon Brown had not taken the decision in 1999 to sell 415 tonnes of UK bullion, the equivalent of 60 per cent of the country’s gold reserves.

Philip Newman, research director of precious metals consultancy GFMS, says central banks sold 365 tonnes of gold in 2006, but just 41 tonnes in 2009.

In Bristol, in the west of England, Mark Dampier of stockbroker Hargreaves Lansdown says retail investors are seeking greater exposure to gold by investing in commodities funds.

“Another option is to invest in gold-backed exchange-traded funds that have become increasingly popular since they were introduced in 2003.”

Diversified mining companies such as Anglo American and Rio Tinto have seen a two-way pull on their stock prices. That’s because the value of many commodities they produce has been pulled down by worries about the fragility of economic recovery. But specialist gold miners such as Randgold Resources have seen their shares rise strongly.

Dampier believes gold will continue its upward trajectory because “governments have printed money like there is no tomorrow, debasing their currencies. I wouldn’t be surprised if they print even more before the crisis is over,” he says.

Not everyone is bullish about gold, however. Julian Jessop of Capital Economics says some of the fears about a double-dip recession are overdone and inflationary pressures will remain subdued for several years. But one support for gold could be continuing uncertainty about the euro.

Suki Cooper, commodities analyst at Barclays Capital, says in the short term gold will be supported by demand for jewellery from the Far East; at the same time there is “a re-evaluation of how gold is perceived in the market”.

Cooper reckons the floor for gold in the long term is US$850 an ounce against an average price of US$310 in 2002. But in real terms the price of gold is still a long way off the inflation-adjusted US$1600 that it reached in 1980 when inflation was rampant and the economic downturn was at its worst. Read into that what you will.

There’s real bullion in those hills

Deep beneath the Swiss Alps, nervous Germans are storing gold in military bunkers that have been sold off by the Swiss state.

Mindful of the hyperinflation that wreaked havoc in Germany during the 1920s, German investors have been at the forefront of gold purchases in Europe.

A growing number are keen to store the precious metal outside the banks, which have been distrusted since the onset of the credit crunch. And, with the future of the euro in doubt, investors are seeking a refuge against the threat of monetary depreciation.

Switzerland is cashing in on those concerns. Old military bunkers in the Bernese Oberland now serve as maximum security vaults for nervous Europeans.

Meanwhile, egged on by commercials trumpeting the virtues of special-issue gold coins, investors in the US have been moving into precious metals. But there, storage is becoming a headache.

One of the biggest banking vaults in New York lies beneath HSBC’s US headquarters in Manhattan. With demand on the up, HSBC last year decided to restrict access to the vault, telling small investors to go elsewhere.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair