Market Opinion

08/30/10 Paris, France – Let’s see, what happened this summer? Easy question. The recovery went missing.

Ben Bernanke said so last week…or almost. He noted that the economy wasn’t quite as spiffy as he had hoped and that the Fed stands ready, willing, and able to provide more help.

The stock market liked the news. After falling for many days, it rallied 164 points on Friday. Gold was flat.

The New York Times reports:

THE American economy is once again tilting toward danger. Despite an aggressive regimen of treatments from the conventional to the exotic – more than $800 billion in federal spending, and trillions of dollars worth of credit from the Federal Reserve – fears of a second recession are growing, along with worries that the country may face several more years of lean prospects.

On Friday, Ben Bernanke, chairman of the Fed, speaking in the measured tones of a man whose word choices can cause billions of dollars to move, acknowledged that the economy was weaker than hoped, while promising to consider new policies to invigorate it, should conditions worsen.

Yet even as vital signs weaken – plunging home sales, a bleak job market and, on Friday, confirmation that the quarterly rate of economic growth had slowed, to 1.6 percent – a sense has taken hold that government policy makers cannot deliver meaningful intervention. That is because nearly any proposed curative could risk adding to the national debt – a political nonstarter. The situation has left American fortunes pinned to an uncertain remedy: hoping that things somehow get better.

This is where the Great Recession has taken the world’s largest economy, to a Great Ambiguity over what lies ahead, and what can be done now. Economists debate the benefits of previous policy prescriptions, but in the political realm a rare consensus has emerged: The future is now so colored in red ink that running up the debt seems politically risky in the months before the Congressional elections, even in the name of creating jobs and generating economic growth. The result is that Democrats and Republicans have foresworn virtually any course that involves spending serious money.

“There are many ways in which you can see us almost surely being in a Japan-style malaise,” said the Nobel-laureate economist Joseph Stiglitz, who has accused the Obama administration of underestimating the dangers weighing on the economy. “It’s just really hard to see what will bring us out.”

Japan’s years of pain were made worse by deflation – falling prices – an affliction that assailed the United States during the Great Depression and may be gathering force again. While falling prices can be good news for people in need of cars, housing and other wares, a sustained, broad drop discourages businesses from investing and hiring. Less work and lower wages translates into less spending power, which reinforces a predilection against hiring and investing – a downward spiral.

What kind of help can the Fed give?

Well, the only kind it has left. Team Bernanke has already given the economy as much conventional, monetary medicine as he could. Rates are at zero. They’ve been at zero for two years. What more can you do?

The Fed has also used its unconventional tool – quantitative easing – to add $1.4 trillion to the Fed’s own balance sheet. It buys bonds with money it creates – out of thin air – especially for that purpose.

We wish we could do that. When the Fed wants to buy something it just snaps its fingers. Presto! New money. Money that didn’t exist before. How neat is that? You want a new car? You don’t draw on savings. You don’t wait until you’ve got enough money. You don’t sit down meekly in front of the credit desk to see if you qualify for financing. You just write a check and tell the bank to cover it.

The Fed has already done quite a bit of quantitative easing. Normally, when it buys a bond with money it invented, the new money goes away automatically when the bond matures. So, the Fed has already said it would turn over its bond holdings, rather than let them mature and expire. And now Bernanke says he is ready to go further – by buying more bonds.

But the Fed is hesitating. It knows it can increase the potential money supply by buying more bonds. But it doesn’t know how much good it will do. So far, the banking system is not lending…and not converting this monetary base into the kind of consumer and business loans that boost consumer prices.

The Fed knows, too, that investors may begin to worry about inflation. Bond buyers may begin to worry about a crash. At some point, these nagging worries could turn into a raging panic. But the Fed doesn’t know where that point is. Neither does anyone else.

And nobody knows whether or not it is possible to transmit just a little bit of inflation – enough to avoid deflation and persuade consumers to shop – by means of quantitative easing. It might be like a runaway train. Once you’ve lost control…it’s too late. Markets now seem to anticipate lower inflation rates. The threat of higher levels could incite investors, consumers and business to get rid of dollars. This would nudge inflation rates up…and build momentum towards even higher price hikes. Every little increase in inflation rates could intensify the desire to exit dollars and US bonds… Who knows where the train would stop?

Meanwhile, President Obama says he’s not happy with the level of growth in the US economy. Which just goes to show how preposterous and absurd the whole discussion has become. Economic growth is a function of what people choose to do with their money. Sometimes they pursue growth. Sometimes they want safety. At present, they seem to prefer to play it safe. Households save. Banks stockpile cash. Businesses put expansion plans on hold and refuse to hire.

What sense does it make for an elected president to take issue with the express, legitimate and sensible desires of the people he is supposed to represent?

It’s hard to believe that more than ten years have gone by since we began writing The Daily Reckoning out of a Paris office back in July of 1999…

Since then, a lot has changed. We have seen the dot com boom and bust…a massive expansion of credit…real estate mania and meltdown…and epic highs and lows in the markets.

Nothing about the past ten years has been boring. And we have been there throughout, trying to help readers make some sense out of our global economy. And hopefully providing a few laughs along the way.

In short, we pen The Daily Reckoning each day – for free — to show you how to live well in uncertain times. We aim to make each article the most entertaining 15-minute read of your day.

If you haven’t signed up yet, I urge you to do so right here. And don’t worry. It’s 100% free – no credit card is required.

Beating Big Oil

Energy is — and always will be — a profitable long-term play.

You should know that by now.

If you don’t believe it, you’re better off burning your cash for warmth.

Last week, I shed some light on the Mexican oil crisis. At first glance, I’ll admit my sour view of Mexico’s oil production is more doom and gloom, but I’m hard pressed to find a reason why they won’t self-destruct from Pemex’s production collapsing.

But does that grim outlook mean we’re should throw in the towel?

Absolutely not…

Several weeks ago, I asked a quick, simple question: Right now, which energy plays are you most comfortable holding for the long run?

The answers that flooded my e-mail inbox shocked me.

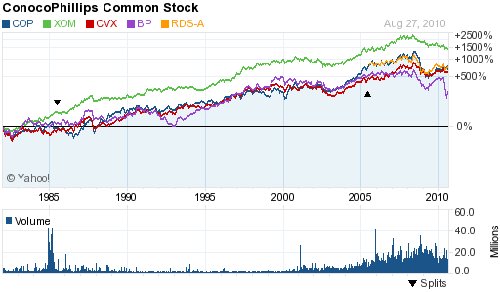

The vast majority of responses were one of the supermajor oil companies: ExxonMobil, ConocoPhillips, Royal Dutch Shell, Chevron, and BP.

I had to learn why.

Trouble for the supermajors

At first, I had to grudgingly admit the supermajors have given shareholders a nice return — assuming you were lucky enough to invest in them twenty-five years ago…

No matter how skeptical I am of the supermajors, they’ve certainly paid off over the long run — even if it took holding your position for two decades.

But their luck has run out.

There’s one reason why I’m not too thrilled about their future returns: national oil companies.

You’ve heard of them before… China’s CNOOC, Saudi Arabia’s Saudi Aramco, Russia’s Gazprom, and Venezuela’s PDVSA are just a few on that list.

And let’s not fool ourselves; these are the true oil giants. In total, national oil companies control approximately 90% of the world’s proven oil reserves and more than half of the world’s oil production. That share will continue growing over time.

Think about it…

Two years ago, oil prices reached an all-time high of $144 per barrel. If anything, countries are suddenly realizing how valuable their natural resources have become — and they’re not going to give them up without a fight.

When Iraq first opened bidding to develop several major oil and gas fields, companies were rejected because their bids were too low. Yet the complications which arose during Iraq’s bidding process were trivial compared how other countries handled the supermajors.

In Chavez’s May Day takeover in 2007, he officially took control of the last privately run oil fields. Compensation for the former owners was far lower than market value.

Now, it’s doubtful that Venezuela’s state-run company will have neither the money nor expertise to develop the massive Orinoco Belt oil projects.

Within the last few years, it’s almost become cliché for countries to give the finger to ExxonMobil and crowd. And the increased sensitivity over national resources is a signal that things will get much tighter for the supermajors.

The effect was clear…

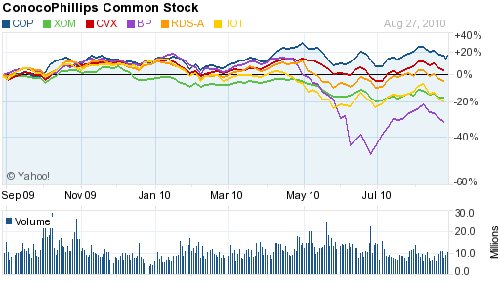

Over the last year, only two of the six supermajors have managed a small gain for shareholders.

Take a look for yourself:

As I said before, there are much better long-term opportunities than these dying supermajors.

Infrastructure investing

One of the problems with energy traders today is that they always fail to look ahead. Maybe they don’t have the same bullish outlook on energy that we do.

Not that those opportunities aren’t there, mind you.

Sometimes the stars align, and all the hard work you’ve put into your research pays off handsomely. My readers are always quick to point toward the 727% gain they banked on one such occasion.

However, there is another side to the equation — one that investors often forget even exists. It’s not just about production. Remember that. If the trillion barrels of untapped oil locked in the Green River formation has taught investors anything, it’s that oil is worthless unless you can bring it to market.

That is also becoming a harsh reality for many Bakken producers, who have been forced to ship their crude by rail and sell their oil at a discount. And yet it’s not just U.S. producers that are looking for relief.

Remember how the United States has been shifting the bulk of its oil imports to Canada?

Our Saudi oil imports have decline 35% within the last seven years. Meanwhile, Canadian crude imports have surged 61% during the last decade.

I’d suggest taking a closer look pipeline stocks. Many of them are expanding current projects to meet future demand.

And the fact that these pipeline plays have managed to outperform the supermajors over the past year is not a coincidence…

It’s only going to get better here on out for them, too.

Until next time,

Keith Kohl

Energy and Capital

P.S. At the heart of these pipeline profits is the latest oil boom to hit North America. The best part is that my readers and I have been closing gain after gain from the beginning. And right now, we’re on the verge of making our next round of profits. Feel free to check out our latest oil report, highlighting one company that has an ace up its sleeve. Click here to learn more about this opportunity.

Buying Bonds like everyone else?

Chart inserted by Money Talks

If a new survey proves accurate, home sellers and hungry real estate agents won’t have many “renters-wanting-to-be-owners” prospects anytime soon:

“More than a quarter of Americans currently renting houses and apartments have no intention to ever buy a home, according to a survey published on Wednesday [8/18}…The survey, by real estate search site Trulia.com, found 27 percent of renters do not plan to ever buy a home. Although 72 percent still expect to buy eventually, that proportion is down from 77 percent six months ago…Of those who do hope to become homeowners, two-thirds say they will wait two years or more.” — Reuters (8/19)

What’s more, the article goes on to say that this lack of interest in home ownership among renters is growing despite the fact that:

“U.S. home loan rates are the lowest since record-keeping began in 1971. The average 30-year rate fell to 4.44 percent in the week ended August 12, according to loan company Freddie Mac.”

Renters have long been a key source of potential home buyers. So this survey is grim news for anyone hoping for a quick recovery in the real estate market.

And, if the economy becomes more depressed, another source of home buyers would dry up — namely people who would move if they were offered a new job. And “mover uppers” who already own a home may also decide to stay put.

Indeed, if the economy keeps going downhill, surveys of renters in the next 6-12 months could show even less inclination to buy a home. Here’s what Robert Prechter wrote in the second edition of Conquer the Crash (pp. 151-152):

“In a depression, buyers just go away. Mom and Pop move in with the kids, or the kids move in with Mom and Pop. People start living in their offices or moving their offices into their living quarters.”

And what if the stock market is headed south? Prechter continues: “Real estate prices have always fallen hard when stock prices have fallen hard.”

If the stock market trend is a reliable indicator of real estate prices, those of us with real estate interests would do well to watch the stock market.

That’s what we do at Elliott Wave International — analyze and forecast the financial markets. Discover our market forecasts so you can reach informed conclusions about your financial future. You’re under no obligation for 30 days when you click HERE to read our Financial Forecast Service now.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair