Investment/Finances

Where Is All that Greek Gold?

The Greeks Write Back

The Euro and a Conspiracy of Hedge Funds

So Where’s the Inflation?

No Help for Homebuilders

The Singularity, San Antonio, Home, and Addictions

The economy grew in the fourth quarter by 5.9%, the most in years. The adjusted monetary base is exploding. Bank reserves are literally through the roof. The Fed is flooding money into the system in an effort to get banks to lend. An historically normal response by banks (to increase lending) would have been massively inflationary, causing the Fed to stomp on the brakes. Despite raising the almost meaningless discount rate (as who uses it?), this week Ben Bernanke assured Congress of an easy monetary policy, with rates remaining low for a long time. Many ask, how can this not be inflationary?

This week we look at some fundamentals of money supply and the economy. If you understand this, you won’t get misled by people selling investments, telling you to buy this or that based on some chart that shows whatever they are selling to be what you absolutely have to have to protect your portfolio and/or make massive profits. And we touch on a few odds and ends. And yes, I can’t resist, a few more thoughts on Greece. It will make for an interesting letter, as I’m writing on a plane to San Jose. And it will print a bit longer than usual, because there are a lot of charts.

Before we get into the meat of the letter, I want to give you a chance to register for my 7th (where do the years go?!) annual Strategic Investment Conference, cosponsored with my friends at Altegris Investments. The conference will be held April 22-24 and, as always, in La Jolla, California. The speaker lineup is powerful. Already committed are Dr. Gary Shilling, David Rosenberg, Dr. Lacy Hunt, Dr. Niall Ferguson, and George Friedman, as well as your humble analyst. We are talking with several other equally exciting speakers and expect those to firm up shortly.

Look at that lineup. These are the guys who got the calls right over the past few years. They called the housing crisis, the credit bubble, and the recession. And, in my opinion, these are some of the best in the world at giving us ideas about where we are headed.

Comments from those who attend the annual affair generally run along the lines of, “This is the best conference we have ever been to.” And each year it seems to get better. This year we are going to focus on “The End Game,” that is, on the paths the various nations are likely to take as they try to solve their various deficit problems, and how that will affect the world and local economies and our investments. We make sure you have access to our speakers and get your questions answered, and you’ll come away with excellent, practical investment ideas.

…..read more HERE

If the global economy could be described as a three ring circus, then the center ring attraction would definitely be the currency and debt exchanges between the United States and China. But for the past month the world’s attention has been distracted by an entertaining sideshow in which Greece and the European Union are jostling over a potential bailout for Greek debt and whether the European Union, and the euro itself, will exist for much longer. I believe the short-term problems in Europe are being overblown and the potential demise of the euro highly exaggerated. For those who can connect the dots however, the drama throws some much needed light on the far more daunting problems unfolding within our own fiscal house.

The scenario that is eliciting the greatest fears is that resentment from the more solvent EU members will prevent a bailout for Greece. If the Greek government then fails to adopt austerity measures that will bring it back in line with EU debt requirements, then an expulsion, or withdrawal, from the Union becomes a possibility. This could set off a domino effect that will bring down larger European political or monetary union. On the other hand, if Greece does receive a bailout, a moral hazard will be created that will encourage other indebted countries (Portugal, Spain, etc.) to press for equal benefits. Both scenarios would destroy confidence in the euro, remove the biggest rival of the U.S. dollar, and give a shot in the arm to the dollar’s global status.

However, there is a third more likely alternative that few are considering. My gut is that Greek politicians will find the prospect of being forced out of the union and re-creating their own currency, formerly called the drachma, even more unpalatable then swallowing the bitter pill of fiscal austerity. Even if defying the EU might seem like good politics now for Greek leaders, the risks associated with economic independence could be so daunting that politicians will refuse to roll the dice. Their better political choice would be to talk tough against draconian spending cuts but vote for them anyway. By playing the role of callous bullies, politicians in Berlin, Paris, and Brussels can provide Greek politicians with the political cover necessary for them to make the unpopular decisions. That way Greek politicians could have their cake and eat it too.

The best case for Europe would be a solution that is all stick and no carrot. This would mean that Greece would have to get its fiscal house in order with no help from the EU. However, even a solution that involved some help from Brussels, but still forced real reforms in Athens, would be seen as a positive for the euro.

Rather than being the beginning of the end for the euro, the Greek drama may well become the euro’s first major victory. If the EU forces Greek politicians to act more responsibly, the Union will show that it cares about the value of its currency and that it has the political will to keep its members in line.

On the other hand, the negative consequences for the EU, and the euro, of an outright Greek bailout would be devastating. Central to the euro’s viability is the limit it places on the ability of member nations to run deficits. The moral hazard associated with a Greek bailout would create a situation that would actually encourage all EU nations to run larger deficits because the costs of doing so would be borne by the more responsible members.

While I still have my doubts about the long-term viability of the euro, I feel that there will be many short-term successes before the experiment ultimately fails. In the meantime, if the euro can survive its current trial, its health could be bad news for the dollar. A battle tested euro, backed by a disciplined union, will have greater credibility as the currency capable of dethroning the dollar. This will eventually refocus attention back on the United States and will highlight the significant distinctions between the two economic powers.

First, while the European Union may have several member nations with fiscal problems, the same situation exists in the U.S. where many of our most populous States are currently navigating similarly dire financial straits. Like Greece, California cannot print money. So if leaders in Sacramento can’t find the will to raise taxes or cut spending, absent federal bailouts, default will be their only option.

However, my guess is that the political pressure in the U.S. to bailout State governments, or to avoid the huge cuts in State spending that would be required to avoid default, will be too great to resist. While Germans are vehemently opposed to bailing out Greeks, I do not foresee the same level of opposition on the part of New Yorkers to bailing out Californians, especially since New York will likely need its own bailout in the not too distant future.

This is especially true since most voters will not be asked to pay higher federal taxes to finance State bailouts. We will simply “pay” for State bailouts the same way we “pay” for all the others, we will borrow from abroad or print money.

As a result, none of the States will be forced to make the necessary spending cuts, and many will actually increase spending even faster, even as their tax bases continue to shrink. Those States that may have otherwise acted responsibility will likewise be incentivized to run large deficits themselves to get their fair slice of the bailout pie.

Of course, on a Federal level, there will be no one to force Uncle Sam’s hand, because unlike Greece, our government can print money. Since printing money is far more politically popular than cutting spending, raising taxes on the middle class, or honest default, it is the most likely option our leaders will choose.

If these two scenarios unfold, the EU holding the line on Greece and Washington caving to California, creditor nations will be presented with a clear message as to where to hold their currency reserves. The stampede out of the dollar will begin, and the greenback’s tenure as the world’s reserve currency will enter its final act. Such an outcome would also throw light on the solvency of the United States itself, which has its own debt issues which in many ways are far more daunting than those faced by the European Union. The real tragedy will play out not in Greece, but in America.

Founded in 1980 and headquartered in Westport, Connecticut, Euro Pacific is a full service, FINRA-registered broker/dealer that has historically been recognized for its expertise in foreign markets and securities. Through its direct relationships with countless foreign trading desks, the firm’s clients are able to avoid the large spreads often imposed by domestic market makers of foreign securities, thereby substantially reducing overall transaction costs. See The Euro Pacific Advantage

Though we offer access to all U.S. stocks and bonds, and are certainly knowledgeable in domestic investments, we specialize in international securities. By trading foreign stocks and bonds through Euro Pacific Capital, individual investors can benefit from our extensive experience in this highly specialized area. Euro Pacific Capital’s clients gain access to foreign markets which are out of reach for most individual investors trading through traditional brokerage firms. With Euro Pacific’s guidance, buying foreign stocks and bonds, and building a truly global portfolio, has never been easier. Let us put our experience to work for you.

…..read the written summary below…..

The Fed’s “Exit Plan” Is Just Another Secret Gift To Wall Street

The Fed is planning to detail its “exit plan” this week, the WSJ says. This exit plan is the means by which the Fed will gradually reverse the tremendous stimulus it is still pumping into the economy and financial system.

As we’ve noted often over the past year, the Fed is in a bind. During the financial crisis, it bought hundreds of billions of dollars of real-estate and other assets from banks to reduce mortgage rates and ease the pressure on bank balance sheets. This, in turn, pumped hundreds of billions of new dollars into the economy, which has enabled the banks–and bankers–to make a killing over the past year. The question is how the Fed can reverse this stimulus without killing the economy.

The idea behind giving the banks cheap money was that the banks would lend it to consumers and businesses. Unfortunately, that hasn’t happened: Since the start of the crisis, bank lending has fallen off a cliff. The banks are, however, lending to the Federal government, which needs to fund record deficits by borrowing more than $1 trillion a year. The combination of the Fed’s desire to stimulate lending via cheap money and the government’s desire to stimulate the economy by running a huge deficit has made it a great time to be a bank: Banks can borrow from the government at artificially cheap rates and then lend the money back to the Federal government at higher rates, pocketing the difference.

And now it’s going to get even better to be a bank.

Why?

Because the first part of the Fed’s exit plan will reportedly be to increase the amount of interest the Fed pays on “excess reserves.”

Banks are required to keep a certain percentage of their assets in cash at the Federal Reserve. Any cash above this required amount is “excess reserves,” and the Fed is currently paying 0.25% interest on these reserves. The Fed’s exit plan will call for increasing this interest rate, to encourage the banks to keep more money in excess reserves instead of lending it into to the economy and thus expanding the money supply.

The idea here is that, by increasing the amount of money on account at the Fed, the Fed will reduce the amount of money that gets loaned out to businesses and consumers, thus forestalling inflation. Increasing interest paid on excess reserves will also put off the day that the Fed has to start selling its real-estate assets back to banks, a process that might create taxpayer losses and raise mortgage rates, which the Fed is loathe to do.

Of course, in the process of increasing interest paid on reserves, the Fed will be paying banks even more not to lend. In the process, it will be giving banks yet another way to take nearly free money from the taxpayer and give it back to the government at a higher rate–and then pocket the difference.

It’s a great time to be a banker.

…..also read: How To Make The World’s Easiest $1 Billion HERE

London based Simon Hunt travels to China many times a year, is an authority on copper and the Long Wave theory of cycles. I generally don’t follow Long Wave analysis, but Simon does make me think and check my own views carefully. The point of Outside the Box is not to send you material that I agree with, but ideas from smart people which make us think. So, enjoy my friend Simon’s latest forecast and ideas. – John Mauldin, Editor Outside the Box

Before we get to this week’s Outside the Box, a quick note about my writing on Greece in last Saturday’s letter. I made the point that if Greece defaults it does not necessarily mean they have to leave the EU, any more than if Illinois defaulted they would have to leave the United States. Greece could still use the euro and life could go on. EXCEPT. The markets would no longer lend the Greek government money at anything close to a livable rate. Greece would be forced to balance its budget. Since they are part of the euro, devaluing the currency is not an option. The results of controlling their fiscal deficit would not initially be pretty and would almost insure a serious prolonged recession or depression in the Greek area, with fall out in the region. It would be a sad decade for Greece. But in the long run, it is a better option than default.

Further, and more important to the rest of Europe and the world, the results of a Greek default would be financial turmoil. 250 billion euros (and maybe 300!) of Greek debt is in international bond funds, pension and insurance companies, and above all at banks. Think German banks. Already undercapitalized banks. Also, think of all the investment banks who have been selling relatively cheap (given the apparent risk) credit default swaps on Greece, in an unregulated market, exposing their balance sheets. What should be a simple, if sad, matter for the Greeks, becomes a problem for the world, just as subprime debt in the US caused a world credit crisis. And the risk of contagion from Portugal, Spain, et al is serious. 2 trillion euros of debt could get downgraded by the bond market in very short order. It could be a replay of the last credit crisis, just with new actors as the prime problem.

Bailing out Greece without serious and credible deficit reductions by their government over the next few years would simply delay the problem, and it is not altogether clear the bond markets would go along for very long. At the end of the day, it may be the bond market which forces the Greek government and its people to take some very bitter medicine. Stay tuned. This is just the beginning of what will be a series of sovereign debt crises over the coming decade. It is important for the world that we get this one solved right, or the consequences will be quite severe.

Now, this week’s Outside the Box is from my friend Simon Hunt, based in London. Simon travels to China many times a year, is an authority on copper and the Long Wave theory of cycles. When we are together, and often over emails, we have some fairly interesting debates. I generally don’t follow Long Wave analysis, but Simon does make me think and check my own views carefully. And as I often write, the point of Outside the Box is not to send you material that I agree with, but ideas from smart people which make us think. So, enjoy my friend Simon’s latest forecast and ideas.

John Mauldin, Editor

Outside the Box

February Economic Report

by Simon Hunt

This year is likely to be a year of surprises.

……read it all right HERE

via John F. Mauldin

johnmauldin@investorsinsight.com

Sign up for the Free Outide the Box Newsletter HERE.

John Mauldin is a Fort Worth, Texas businessman, now living in Uptown Dallas, and the father of seven children, ranging from ages 13 through 30, five of whom are adopted.

He was Chief Executive Officer of the American Bureau of Economic Research, Inc., a publisher of newsletters and books on various investment topics, from 1982 to 1987. He was one of the founders of Adopting Children Together Inc., the largest adoption support group in Texas. He currently serves on the board of directors of The International Reconciliation Coalition and the International Children’s Relief Fund. He is also a member of the Knights of Malta, and has served on the Executive Committee of the Republican Party of Texas.

He is a frequent contributor to numerous publications, and guest on TV and radio shows as well as quoted widely in the press.

John is the President of Millennium Wave Advisors, LLC (MWA) which is an investment advisory firm registered in multiple states. John Mauldin is President of Millennium Wave Securities, LLC a FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB).

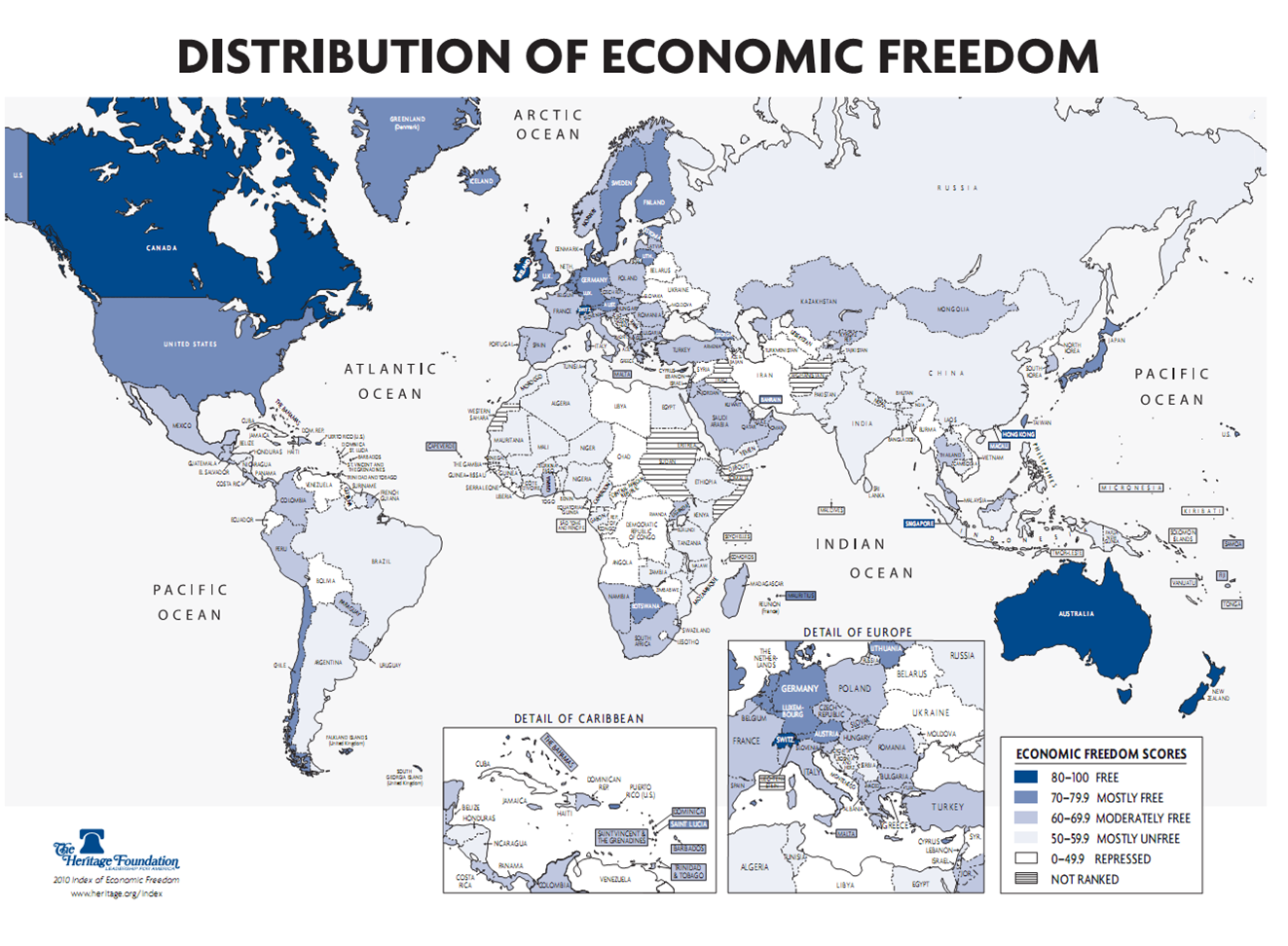

Hoven’s Index for January 24, 2010

Economic freedom is the fundamental right of every human to control his or her own labor and property. In an economically free society, individuals are free to work, produce, consume, and invest in any way they please, with that freedom both protected by the state and unconstrained by the state. In economically free societies, governments allow labor, capital and goods to move freely, and refrain from coercion or constraint of liberty beyond the extent necessary to protect and maintain liberty itself.

The Freedom score for the US in the last five years:

2006: 81.2

2007: 81.2

2008: 81.0

2009: 80.7

2010: 78.0

The Freedom score for Canada in the last five years:

2006: 77.4

2007: 78.0

2008: 80.2

2009: 80.5

2010: 80.4

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair