Homepage

Click HERE to find out more about the specifics of Currency Currents Professional and how you can subscribe today and get 2 free months of insights, research, global macro analysis, and actionable trades.

The next really big long term trade

Michael Campbell: Joining me on the line right now I’ve got the head analyst for Black Swan Capital. There’s so much that Jack Crooks does and I love his work because he writes some terrific things. Last year at this time you were telling us to keep an eye on the Euro. You said you think it’s going down at the outlook conference, that its a no-brainer trade. You said Greece is going to really cause trouble before it had hit the headlines. Obviously a very successful move as the Euro did have a major downward leg vis-à-vis the US dollar and the Canadian dollar so its a fortuitous time to get you on the line right now. You’ve been writing about the concept that when people feel like they don’t want any risk, they go to the US dollar and when they feel a little more risk friendly then they leave the US dollar. Where do you think we’re at generally with that now?

Jack Crooks: The risk, the so called risk on, risk off is still the co-relation that’s in play here to a degree. What we’re going to see is more political unrest throughout the Euro zone just because Germany is just sucking the wind out of everybody and nobody else is really able to participate in the growth there. Near term it looks like the dollar may correct in here from a trader’s stand point but longer term we still think that Euro theme is in play once we get past this sort of bit of growth optimism that we’ve seen recently based on just some of the global growth not only in the US. I think the US numbers have been okay but the Asian numbers have been very strong and that’s what really drives this risk appetite trade.

Michael: So it’s all about either aversion to risk or taking on a little bit more risk. That’s such an important concept for people to get.

Jack: Yes, it’s huge. It is a relevant game and the US dollar is the World reserve currency because the US’s capital markets are deeper than any other capital markets in the world. So the US can be very ugly but the US dollar can still go up because people have to move money for reasons of safety. Big money international investors that don’t have any other place to hide have to come to US. They might not like the US economy but they’re forced into the depths of the US capital markets.

Michael: For these huge pools of money there’s only three games in town, either going to be in the Euro, the US, or the Yen. The Canadian dollar just couldn’t absorb that kind of money movement and wouldn’t be considered because of it. New Zealand or Australia are in the same boat. My goodness though, if you list the problems in Japan it’s been in a 20 years of low growth, a recessionary environment and the demographics just suck. Yet the Yen’s done very well recently.

Jack: Japan is a perfect analogy. When people point to the US and note that the GDP is rising therefore the dollar has to fall, all we have to do is look at the Japanese Yen. These things are never that simple. That said, we think the game is about over for the yen.

.

Michael: Luckily as an investor I can now play a currency move with an exchange traded fund now, which trade just like stocks do. While it does look right now like the yen can’t go any further I know that markets can stay irrational longer than I can stay solvent. So how do you determine when its time to make a move?

Jack: I think you summed it up very well; things can always go lower than we think and always go higher than we think. In a piece that we wrote a few weeks ago, we talked about Barton Biggs back in 1995 who said that trade of the decade, may be the trade of the life time was to sell Japanese government bonds. Well he still probably hasn’t broken even on that trade if he did it. For 10 or 15 years now those interest rates have stayed low in Japan. Ultimately you have to look for some reason for a major trend change and it has to from some consolidation or some major fundamental change. We are actually starting to see a little bit around the edges in Japan. One of the things that we track very closely is the 20 year bond yield versus the Japanese Yen and they are usually just dead on the money. If your listeners can get to a 20 year bond yield chart and pull it up, bond yields have actually backed up in a very big way over the last week or so in Japan but the Yen is still near it’s low. So there’s a giant divergence to it. It hasn’t developed in that chart for a very long time but it’s something that we’re watching and we’re actually starting to pack on the Yen for that reason. That’s a fundamental capital flow change that’s not really showing up in the headlines.

Michael: What else do you think is happening out there?

Jack: Other than the Yen move which we think is very close here, the Euro we think ultimately it goes to par because we just don’t see the system surviving politically. We could see Ireland, Spain and Greece some going back to their own local currencies because they’re in a straight jacket. So the Euro coming apart eventually economically and politically still makes sense. We do think ultimately the Yen is really the next big trade because what we’re seeing in this isn’t new. One of the reasons the Yen has always been so strong is they have been historically able to fund themselves domestically because Japanese are savers. Now they are are not making 20% saving rates instead they’re about zero right now. There comes a point when they’re going to have start raising those long bond interest rates to attract international capital now in Japan. I think the game is about over in domestic funding and that we think it is going to be the next really big long term trade.

Michael: There’s just so much money swashing around the world, about 3.5 trillion dollars a day that trades a day in the currency markets. Which to put into perspective is two and a half to three times the size of the entire Canadian economy output in a year trading each day. So we’re talking massive amounts of money which is why governments and central banks can only talk the game because they learned a long time ago they couldn’t influence it directly.

Jack: Exactly, you’re exactly right. The markets are so big now there has to be some type of fundamental change in capital flow to change these trends it cannot come from a government or central bank. They don’t have the power to move these markets any longer.

Michael: I want to stay in Asia for a second and just get your comments on China because so much of our growth scenario, our rescue scenario takes place coming out of China.

Jack: Yes it sure does. Last week China’s purchasing index was above fifty for the month of August and they were below 50, so more vibrancy again. India is still growing well, Singapore looks pretty good, Australia looks very strong. We have to consider Australia an Asian economy at the moment. So there is growth there. A move to the risk appetite trade would mean the dollars starts to get hit again and we saw that this week. But while the numbers keep coming through in China the real concern continues to be for us a consumer in China just hasn’t been there. Also the fact that China continues to basically subsidize its interest rates. The interest rates in China are very, very suppressed artificially below the market. It’s creating huge implications for capital across a lot of different sectors. China knows this, but they continue to keep their interest rates suppressed and their currency suppressed because they play have to still export.

They are off the charts in terms of anything we’ve ever seen in history as an economy that’s weighted export versus consumer. Just nothing has even been close to where China is here. And the scenario that we draw from a major global metric change is exactly like of Japan. Japan was going to take over the world in the mid 1980’s and China has done the exact same from a financial and economic standpoint. Very much a parallel. We are not alone in this concern but that’s something that we continue to watch and if it does play out that China just cannot support its own growth domestically, it’s going to be very, very nasty for the global economy. So it’s something we continue to watch on our radar screen. But the near term numbers are strong and you got to go with it.

Michael: What about the Canadian dollar?

Jack: We like that a lot here from a trade standpoint because of the growth in Asia. Also the Canadian and Australian dollars are both commodity currencies and If we pull up the Canadian dollar against the Australian dollar chart, the Canadian dollar is extremely cheap here relative to the other commodity currency out there. That’s another reason we like it

Michael: That’s an easy one for Canadians cause we don’t have to trade it we just own it, we are it.

Jack: That’s right

Michael: Jack I want to thank you for taking the time as I say I know you are busy with other things there. But it’s always a pleasure to talk to you. And as I say I think the understanding of how the currencies are moving and why they are moving is the key to understanding really what the heck’s going on in the world and we appreciate your insights.

Jack: Thanks for having me Mike always my pleasure.

Michael: Just go to www.blackswantrading.com I read Jack’s comments every day I recommend them to people as I say that’s how you keep a handle on what’s going on in the world.

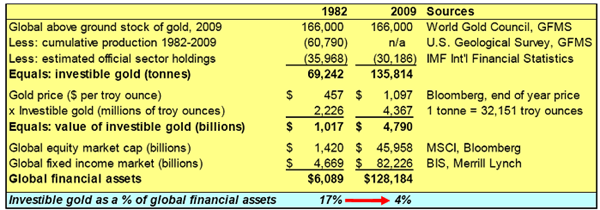

Thought-provoking table from Cembalest at JP Morgan comparing gold’s capitalization as a percentage of bond and equity market capitalization during other periods of market nihilism/strife/awfulness/madness.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair