Daily Updates

AMARGOSA VALLEY, Nev. — In a rural corner of Nevada reeling from the recession, a bit of salvation seemed to arrive last year. A German developer, Solar Millennium, announced plans to build two large solar farms here that would harness the sun to generate electricity, creating hundreds of jobs.

But then things got messy. The company revealed that its preferred method of cooling the power plants would consume 1.3 billion gallons of water a year, about 20 percent of this desert valley’s available water.

Now Solar Millennium finds itself in the midst of a new-age version of a Western water war. The public is divided, pitting some people who hope to make money selling water rights to the company against others concerned about the project’s impact on the community and the environment.

“I’m worried about my well and the wells of my neighbors,” George Tucker, a retired chemical engineer, said on a blazing afternoon.

Here is an inconvenient truth about renewable energy: It can sometimes demand a huge amount of water. Many of the proposed solutions to the nation’s energy problems, from certain types of solar farms to biofuel refineries to cleaner coal plants, could consume billions of gallons of water every year.

“When push comes to shove, water could become the real throttle on renewable energy,” said Michael E. Webber, an assistant professor at the University of Texas in Austin who studies the relationship between energy and water.

Conflicts over water could shape the future of many energy technologies. The most water-efficient renewable technologies are not necessarily the most economical, but water shortages could give them a competitive edge.

In California, solar developers have already been forced to switch to less water-intensive technologies when local officials have refused to turn on the tap. Other big solar projects are mired in disputes with state regulators over water consumption.

To date, the flashpoint for such conflicts has been the Southwest, where dozens of multibillion-dollar solar power plants are planned for thousands of acres of desert. While most forms of energy production consume water, its availability is especially limited in the sunny areas that are otherwise well suited for solar farms.

At public hearings from Albuquerque to San Luis Obispo, Calif., local residents have sounded alarms over the impact that this industrialization will have on wildlife, their desert solitude and, most of all, their water.

Joni Eastley, chairwoman of the county commission in Nye County, Nev., which includes Amargosa Valley, said at one hearing that her area had been “inundated” with requests from renewable energy developers that “far exceed the amount of available water.”

Many projects involve building solar thermal plants, which use cheaper technology than the solar panels often seen on roofs. In such plants, mirrors heat a liquid to create steam that drives an electricity-generating turbine. As in a fossil fuel power plant, that steam must be condensed back to water and cooled for reuse.

The conventional method is called wet cooling. Hot water flows through a cooling tower where the excess heat evaporates along with some of the water, which must be replenished constantly. An alternative, dry cooling, uses fans and heat exchangers, much like a car’s radiator. Far less water is consumed, but dry cooling adds costs and reduces efficiency — and profits.

The efficiency problem is especially acute with the most tried-and-proven technique, using mirrors arrayed in long troughs. “Trough technology has been more financeable, but now trough presents a separate risk — water,” said Nathaniel Bullard, a solar analyst with New Energy Finance, a London research firm.

That could provide opportunities for developers of photovoltaic power plants, which take the type of solar panels found on residential rooftops and mount them on the ground in huge arrays. They are typically more expensive and less efficient than solar thermal farms but require a relatively small amount of water, mainly to wash the panels.

In California alone, plans are under way for 35 large-scale solar projects that, in bright sunshine, would generate 12,000 megawatts of electricity, equal to the output of about 10 nuclear power plants.

….read page 2 HERE.

Every few weeks the world’s most powerful and influential central bankers — those in charge of the world’s number one reserve currency, the U.S. dollar — come together in what’s called the Federal Open Market Committee (FOMC).

They discuss the economy, interest rates, financial markets and whatever else they deem important. Then they decide to set the Federal Funds Rate at a level they think is appropriate.

And last week was their week. So today I want to analyze what their decisions mean for the stock market and for you as an investor.

The Fed Statement Reassures

A Very Lax Monetary Policy …

After each FOMC meeting, the Fed releases a statement. And the one for September 23, 2009, is very telling in my opinion. Here’s its most important part:

“The Committee will maintain the target range for the federal funds rate at 0 to 1/4 percent and continues to anticipate that economic conditions are likely to warrant exceptionally low levels of the federal funds rate for an extended period.”

As you can see, the Fed is promising a continuation of its extremely lax monetary policy “for an extended period.” So all the recent media talk about a soon-to-begin exit strategy or a normalization of monetary policy was obviously premature. The Fed is reassuring us that there will be easy money for as far as the eye can see.

Why?

Two reasons come to mind:

First, the Fed is still very concerned about the economy … the employment situation is dire … and a double-dip recession is a real possibility.

Second, and more important, is that they know how precarious the banking situation still is. They know that the bad debt problems have not been solved … that most banks would go bankrupt if they had to implement mark-to-market rules … and that the banking system is still on life support.

This Is Important News

For the Stock Market

Since the Fed is confronted with two major problems — a shaky economy and an unstable banking system — it’s not worrying about a possible stock market bubble in the making.

Why is this so important?

Just look at the charts below. The stock market has rallied some 60 percent since the March low. But earnings are still very depressed. Hence the classic version of the P/E ratio — using twelve months trailing GAAP earnings — shot to the stratosphere!

Twelve-month trailing earnings as of the first quarter 2009 were a mere $6.86 for the S&P 500 making for a P/E ratio of 154. According to Standard and Poor’s, these earnings are estimated to rise to $7.51 in the second quarter, and $7.61 in the third quarter. Then they’re expected to jump to $39.35 in the fourth quarter and $43.58 in the first quarter 2010. Based on this last figure the P/E ratio will decline to 24.

Historically the normal range for this very P/E ratio — based on 12-month trailing GAAP earnings — has been between 10 (undervalued) and 20 (overvalued). Hence even if the corporate sector will see the estimated jump in earnings, the stock market is still very expensive.

Classic stock market valuation metrics show that this is a highly overvalued market. And overvalued markets can stay overvalued for a long time and even become more overvalued — as long as the Fed does not take away the proverbial punch bowl.

This means one of two things …

We’re Witnessing the Next Bubble, Or

Earnings Have to Increase Dramatically!

Right now I can’t rule out either one. I do, however, lean towards the first. And in reading the Fed’s FOMC statement one thing becomes obvious: If we’re on our way to a new stock market bubble the Fed will not prick it any time soon.

The September 23 statement that I cited earlier is as clear as you can expect from the Fed. Much clearer than anything Greenspan said during his long reign. His famous “irrational exuberance” speech, which was never followed by any action, is a perfect example.

Bernanke is much different …

From the very beginning of his career at the Fed he made it known that he’s a first class inflationist, and he strongly believes prosperity can be achieved by printing money. Now the Bernanke Fed is clearly reiterating this inflationary stance. By doing so the Fed is rubberstamping the current stock market rally and apparently not worrying about a possible bubble!

There is an old Wall Street saying: “Don’t fight the Fed.” I think it’s wise to heed it in today’s environment.

Best wishes,

Claus

This investment news is brought to you by Money and Markets. Money and Markets is a free daily investment newsletter from Martin D. Weiss and Weiss Research analysts offering the latest investing news and financial insights for the stock market, including tips and advice on investing in gold, energy and oil. Dr. Weiss is a leader in the fields of investing, interest rates, financial safety and economic forecasting. To view archives or subscribe, visit http://www.moneyandmarkets.com. Money and Markets

Claus Vogt is the editor of Sicheres Geld, the first and largest-circulation contrarian investment letter in Europe. Although the publication is based on Martin Weiss’ Safe Money, Mr. Vogt has provided new, independent insights and amazingly accurate forecasts that, in turn, have contributed great value to Safe Money itself.

Mr. Vogt is the co-author of the German bestseller, Das Greenspan Dossier, where he predicted, well ahead of time, the sequence of events that have unfolded since, including the U.S. housing bust, the U.S. recession, the demise of Fannie Mae and Freddie Mac, as well as the financial system crisis.

He is also the editor of the German edition of Weiss Research’s International ETF Trader, which has delivered overall gains (including losers) in the high double digits even while the U.S. stock market suffered its worst year since 1932.

His analysis and insights will be appearing regularly in Money and Markets.

Black Swan Live Webinar Event Today – Courtesy of Tom Busby’s DTI

Topic: Emerging Market Currencies

Time: 12:00 noon EST

Register: http://www.dtitrader.com/trading_education_Blackswan_WoW.htm

Quotable

“Anything in any way beautiful derives its beauty from itself and asks nothing beyond itself. Praise is no part of it, for nothing is made worse or better by praise” Marcus Aurelius

FX Trading – Warm up for Friday…

There have been much cryptic and not so cryptic comments of late from Federal Reserve Bank speakers. Some are implicitly calling for rate hikes sooner rather than later to mop up all the mess of money excess, others explicitly saying the Fed will likely surprise on the aggressiveness of future hikes…but the market doesn’t seem too concerned about that today, as the dollar is back under pressure this morning and trading lower against all the majors. I guess it was time for the dollar to take a breather, as it strung together a two-day rally. Two-day rallies are rare for Mr. Greenie these days.

Aussie has surged to fresh post-crisis high against the buck on more good economic news from down under. China continues to keep the music playing with another month of officially reported increase in manufacturing activity and rising employment—just in time for their big Beijing bash on Thursday for the party faithful. But keeping the music playing has caused concerns, as overcapacity in China is rampant, especially in the steel industry.

“The State Council, China’s cabinet, said in a strongly worded statement that highly polluting sectors including steel, coke, cement and plate glass must cut capacity, while silicon and wind power producers should pursue more orderly development,” the Financial Times reported.

Though this story doesn’t play into the traders view when it comes to currencies, it might be very important for “investors” in the currency market, assuming there is such a beast left. Why important? It’s important because Beijing is betting a lot of chips on the proverbial V-shaped recovery.

What if China has it exactly right and the US consumer rebounds in a big way? Well, it might mean the market starts taking Fed speakers seriously. That might throw quite a monkey wrench into the idea of the US dollar as the key carry-trade currency, something traders now seem to be feasting upon.

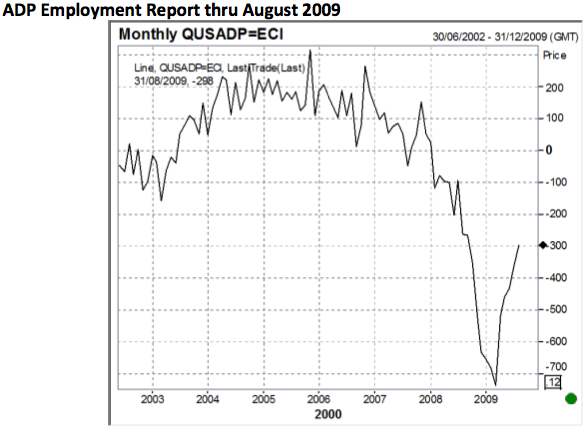

It has been those better than expect non-farm payroll days that have juiced both stocks and the dollar on the same day. We will likely find that out on Friday on the release of US non-farm payrolls report for September. But today we get a look at Friday’s warm-up act in the form of the ADP Employment Report [the ADP Employment Report defined].

So, given the run against the dollar today, just maybe the ADP report will mean something. A good report and bad price action in the buck could tell us something. Stay tuned.

Jack Crooks

Black Swan Capital LLC

www.blackswantrading.com

Register HERE for the FREE Daily Currency Currents Newsletter.

Black Swan Capital is an independent minded currency advisory firm established to provide subscription-based services to help retail and institutional clients consistently attain above average profits trading and investing in both forex and currency futures markets. We tell our Members when to enter and exit and why. HERE for more information.

Our commitment is to deliver well researched trading recommendations that our clients understand and can efficiently execute through their brokers. We outline the reasons to enter a trade and define the risk. But our Members must understand there is a substantial risk of loss trading in forex (off-exchange retail foreign currency) and currency futures markets.

Register HERE for the FREE Daily Currency Currents Newsletter.As a subscriber to Currency Currents you stay tuned-in to our current global-macro view and our analysis of key investment themes driving currency prices. Nothing is off limits to us in this free-wheeling look at the markets. Some days you’ll receive ramblings on trading psychology, while other days we may take an academic approach in explaining esoteric economic issues. Ultimately we have one goal in mind: to help you get a handle on the key investment themes driving global capital flow. Because if you know where the money is going, it increases the probability that yourposition in the market will be a profitable one.

“President Obama promises to cut spending in the US. But can he? Read this column out of Forbes by Bruce Bartlett, former Treasury Dept. economist — “Whenever I write about the federal deficit, some nitwit always demands to know why we don’t just cut spending,” says Bruce Bartlett. “Here is the simple, if unsatisfying, answer. We can’t. Nearly two-thirds of spending — 62% is mandatory, entitlements and interest on the debt. The defense budget — which will never be cut substantially, — consumes more than half of what remains, leaving a total of $485 billion for everything else. Given a deficit of $459 billion last year, a balanced budget would require the elimination of virtually every single domestic program, including all social programs, education, highways, border patrols, air traffic control, and the FBI. The only alternative is to reduce mandatory spending on Medicare and Social Security — and good luck with that. The elderly will fight anyone who tries to cut their benefits, even as they hypocritically demand fiscal responsibility. And seniors’ political power will only get stronger, as baby boomers get old. Face it, if the US ever stops running a deficit, it won’t be because Congress made massive cuts in federal spending. The votes aren’t there, and never will be.”

Ed Note: Full article “We can’t cut spending HERE or below this appropriate Alexis de Tocqueville quote:

A Democracy cannot exist as a permanent form of government. It can only last until the citizens discover they can vote themselves largesse out of the public treasury. After that, the majority always votes for the candidate promising the most benefits from the public treasury with the result that the Democracy always collapses over a loose fiscal policy, to be followed by a dictatorship, and then a monarchy. The average age of the world’s greatest civilizations has been 200 years. Great nations rise and fall. The people go from bondage to spiritual truth, to great courage, from courage to liberty, from liberty to abundance, from abundance to selfishness, from selfishness to complacency, from complacency to apathy, from apathy to dependence, from dependence back again to bondage.

We Can’t Cut Spending – by Bruce Bartlett

Every time I write about the need to raise revenues to pay for federal spending, some nitwit always demands to know why we don’t just cut spending. That is not a viable option to deal with our fiscal problem.

The first point that people need to understand is that we live in a democracy. We don’t have a dictator who can just wave his hand and abolish government programs. We have a president who may propose spending cuts, but before they take effect he must get agreement from both the House of Representatives and Senate, both of which may be controlled by a different party. Congress’ efforts to cut spending on its own are futile without prior agreement from the president to support them, as Republicans found out the hard way in 1995.

Direct presidential control over spending is extremely limited. By law, he must spend every dollar appropriated by Congress. And presidents have no control at all over three-fifths of the budget devoted to interest on the debt and entitlement programs–those like Medicare for which spending is automatic. Even Congress can’t reduce spending for entitlements unless it changes the law governing eligibility and programmatic operations. In other words, Congress can’t just appropriate less money to Medicare. It doesn’t work that way.

Even if the president’s party controls Congress by a wide margin–as is the case today–getting agreement even on popular measures, such as expanding health coverage, is very, very difficult, as we are seeing. One reason for this is that the Constitution gives the minority party influence disproportionate to its numbers in the Senate. Thus even though Republicans only have 40 seats, they have been very successful in blocking Obama’s health care reform initiative.

How much more strongly do you suppose 40 Senate Democrats would fight a Republican effort to massively cut spending if party control were reversed? What is the likelihood that every Republican would stand in unity for highly unpopular spending cuts that threaten the health and well being of millions of Americans? Just look at the so-called Blue Dog Democrats who are making life difficult for House Speaker Nancy Pelosi despite having a 78-seat majority. There undoubtedly would be an equally large group of Red Dog Republicans fighting every specific budget cut no matter how small.

If Democrats controlled Congress, as they do now and usually have when there was a Republican president, they could easily ignore a presidential effort to slash spending just as they ignored George W. Bush’s plans to privatize Social Security. At the end of the day, presidents may only propose, Congress must dispose.

Therefore, it is simply stupid and a waste of time to say that massive budget cuts are the answer to our problem without taking account of inevitable congressional resistance. Of course, presidents can try to influence Congress to be more supportive of their requests. They can give speeches to joint sessions of Congress, as Barack Obama recently did, or go over the heads of Congress to the people and try to create grass roots pressure, as Ronald Reagan often did, or they can try to pressure, cajole or threaten individual members of Congress the way Lyndon Johnson did. But at the end of the day, a president has to find at least a majority of congressmen and senators to vote for something or it doesn’t become law.

Devising a package of budget cuts large enough to prevent national bankruptcy must also deal with other realities that make them almost impossible to achieve. These include the changing nature of the federal budget and the changing composition of the population.

Many of those favoring budget cuts have ridiculous notions about how much of the budget can be cut without reducing services. A recent Gallup poll found that Americans generally believe that 50% of the budget is wasted. This suggests that they believe the federal budget could be cut in half without cutting anything important like Social Security benefits or national defense.

Just so people know the round numbers, total spending this year is about $3.6 trillion. At most, $200 billion of that represents stimulus spending, so even if there had been no stimulus bill and the economy had done as well as it has done, we would be looking at a $3.4 trillion budget.

Revenues are only about $2.1 trillion, so we would be looking at a substantial deficit even if the stimulus package was never enacted. Revenues would be even lower if Republicans had gotten their wish and the stimulus consisted entirely of tax cuts. How tax cuts would help people with no wages because they have no jobs or businesses with no profits to tax was never explained. But many right-wingers are convinced that tax cuts are the only appropriate governmental response no matter what the problem is.

Looking at last year’s budget, only 38% was classified as discretionary; that is, under Congress’s control through the appropriations process. All the rest was mandatory: entitlements and interest on the debt. Within the discretionary category, 54% went to national defense. Just $37.5 billion, 3.3% of the discretionary budget, went for international affairs including foreign aid. Over the years I have encountered many conservatives who thought that abolishing foreign aid was just about the only thing needed to balance the budget. Obviously, that’s nonsense.

Domestic discretionary spending amounted to $485 billion last year. With a deficit last year of $459 billion, we would have had to abolish virtually every single domestic program to have achieved budget balance. That means every penny spent on housing, education, agriculture, highway construction and maintenance, border patrols, air traffic control, the FBI, and every other thing one can think of outside of national defense, Social Security and Medicare.

This means that it is impossible to get control of spending without cutting entitlement programs. Many Republicans agree, but they never make any serious effort to do so. On the contrary, they defend entitlements when Democrats suggest cutting them. The Republican National Committee has run television ads opposing cuts in Medicare because Obama proposed using such cuts to fund health reform. Many demonstrators at right-wing tea parties were seen carrying signs demanding that the government keep its hands off Medicare.

Last year, we spent $456 billion on Medicare, and it is the fastest growing major government program. How likely is it that the people protesting Obama’s Medicare cuts will stand with Republicans if they propose cutting that program even more to balance the budget? They will switch sides in an instant. The elderly will fight anyone who tries to cut their benefits even as they hypocritically demand fiscal responsibility and rant about the national debt. The elderly are the reason why we have a national debt.

Unfortunately, the ranks of the elderly are rising. In 1980, those over age 65 constituted 11.3% of the population. Today they represent 13%, a figure that will rise to 16% in 2020 with the aging of the baby boomers and increasing longevity, 19.3% in 2030 and 20% in 2040, according to Census Bureau projections.

Furthermore, the elderly are a rising portion of the electorate. Back when Medicare was established, those over 65 constituted 15.8% of voters. Last year, they made up 19.5%. This is due to the rising percentage of elderly in the population and their increasing propensity to vote. In 2008, 72% of those between the ages of 65 and 74 reported voting while only 48.5% of those between the ages of 18 and 24 did.

When I raised these facts with a prominent Republican recently, he countered that Reagan had cut spending. But he didn’t. Spending rose from 21.7% of the gross domestic product in 1980 to 23.5% in 1983 before declining to 21.2% in 1988. And that improvement came about largely because favorable demographics caused entitlement spending to temporarily decline from 11.9% of GDP in 1983 to 10.1% in 1988. (Last year it was 12.5% of GDP.)

When I noted these facts, my friend pointed to British Prime Minister Margaret Thatcher as someone who showed that spending could be slashed. But she raised spending from 42.4% of GDP when she took office in 1979 to 46% of GDP in 1985. Only in her last years in office was spending cut to 38% of GDP. But keep in mind that Thatcher was in office for 10 years, longer than a U.S. president may serve, and had compete control of Parliament the whole time–something Reagan could only dream about.

In short, there is no evidence that it is politically possible to cut spending enough to make more than a trivial difference in our nation’s fiscal problems. The votes aren’t there and never will be. Those who continue to insist otherwise are living in a dream world and deserve no attention from serious people.

Bruce Bartlett is a former Treasury Department economist and the author of Reaganomics: Supply-Side Economics in Action and Impostor: How George W. Bush Bankrupted America and Betrayed the Reagan Legacy. Bruce Bartlett’s new book is available for pre-order:The New American Economy: The Failure of Reaganomics and a New Way Forward. He writes a weekly column for Forbes.com.

We could be “finally” seeing the makings of a U.S. Dollar rally. Some sentiment indicators are so oversold and with bullish sentiment among dollar traders in the single digits, one can’t but help think there’s a rally in here somewhere.

This by no means changes any of my long-term outlooks but can come into play on the metals and energy side of things for the very near-term.

The combination of this and what’s looking more and more like a self full-filling prophecy of the usual Commercials smashing the speculative longs on the Comex, could cause a very short-term shake out in gold. But with Physical buying so strong, any shakeout should only last as long as real hopes of the Vancouver Canucks winning the Stanley Cup.

The mini melt-up in the U.S. stock market continues to take hold.

The summer doldrums are gone and the month of October appears like it’s once again going to deliver large-scale volatility.

Ed Note: From Peters Link to – sentiment indicators

US Dollar May Have Set Important Bottom versus Euro

Forex Options and Futures markets show US Dollar sentiment at major bearish extremes versus the Euro, Swiss Franc, and Canadian Dollar. Such one-sided sentiment strongly suggests that the US Dollar could soon recover from its recently sizeable losses, and indeed we believe that the downtrodden Greenback could finally recover on a broad basis.

Volatility expectations themselves have remained fairly limited despite pronounced US Dollar weakness. This in itself suggests that the recent pace of dollar losses may not be sustained. More importantly, we are beginning to see signs that pairs such as the EURUSD reverse from their previously impressive trends. It clearly remains critical to watch price action in the weeks ahead. Sentiment can and does remain extreme for extended periods of time, but the confluence of bearish USD positioning suggests that the Greenback could soon turn against key counterparts.

DailyFX Forex Options Weekly Forecast

Futures positioning shows that Non-Commercial traders (typically large speculators) have become extremely net-long the Euro against the US Dollar. In fact, said speculative positioning is the most long EURUSD since it traded near 1.6000 in early 2008. We consistently warn that extreme positioning and sentiment can and does remain extreme for extended periods of time. Yet it is interesting to point out that options sentiment actually shows many traders are beginning to hedge against EURUSD weakness. It’s possible that the EURUSD has set a noteworthy medium-term top.

British Pound/US Dollar Options Analysis

Futures and options sentiment points to further losses for the British Pound, as markets have aggressively sold the currency through recent trade. Net Non-Commercial positioning dropped precipitously as the GBPUSD broke below the psychologically significant 1.6000. Yet current positioning is a good distance from major sentiment extremes. In other words, there is still a good deal of margin for further selling, and we cannot confidently call for any worthwhile GBPUSD corrections through upcoming trade. FX Options show that traders are indeed hedging against further GBP weakness.

US Dollar/Japanese Yen Options Analysis

Impressive Japanese Yen rallies (USDJPY declines) have led to similarly impressive positioning in futures markets, with Non-Commercial traders the most heavily net-short USDJPY since it last traded below 90. The key difference this time around is that forex options market sentiment is far less extreme. This gives the sense that the Yen has further room to run, and a challenge of generational lows near 87 seems plausible.

US Dollar/Canadian Dollar Options Analysis

Traders have grown extremely net-long the Canadian dollar (short the USDCAD) through recent trade, with FX Futures data showing sentiment at its most bullish since the pair traded near parity. Forex options markets likewise show that traders are increasingly betting on USDCAD weakness—emphasizing that sentiment remains extremely bearish. Given such headwinds, we believe that the USDCAD downtrend is near its end. The recent rebound in options sentiment shows that some are beginning to hedge against CAD weakness (USDCAD strength).

….for the US Dollar/Swiss Franc Options Analysis, Australian Dollar/US Dollar Options Analysis and the New Zealand Dollar/US Dollar Options Analysis go HERE and scroll down the page.

Charts and commentary provided by David Rodriguez, Quantitative Strategist at http://www.dailyfx.com

On Major Moves, Grandich has been very right and not only saved many investors fortunes, but expanded them dramatically. On November 3, 2007 at the MoneyTalks Survival Conference, Peter Grandich of the Grandich Letter warned that “an unprecedented economic tsunami will hit American beginning in 2008”. Peter advised publicly to short the US market two days from the top in October, 2007 and stayed short until the last week of October, 2008. He began to buy stocks in March 7th, 2009. He also bought oil and oil related investments near the lows after the dive from $147.

….go to visit Peter’s Website.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair