Daily Updates

· ![]() Commodities, Stocks Rally as Alcoa Earnings Top Estimates, Dollar Declines (Bloomberg)

Commodities, Stocks Rally as Alcoa Earnings Top Estimates, Dollar Declines (Bloomberg)

· Latvia `on the Edge’ After Government Mortgage Plan, Cicero’s Oates Says (Bloomberg)

· Final estimate for US budget deficit at $1,400bn (Financial Times) The government took in $2,100bn in fiscal 2009, a 16.6 per cent drop from the previous year as the recession led to sharp declines in individual and corporate income taxes, CBO said.

On the other half of the ledger, outlays increased 17.8 per cent to $3,500bn, CBO said.

Among the most expensive items were $154bn for bail-outs under the troubled asset relief programme, $91bn for the Fannie and Freddie bail-outs, and $100bn under the massive stimulus package approved in February.

Excluding items in the stimulus package, spending for unemployment benefits more than doubled to $120bn, CBO said.

Quotable

![]() “The world always makes the assumption that the exposure of an error is identical with the discovery of truth–that the error and truth are simply opposite. They are nothing of the sort. What the world turns to, when it is cured on one error, is usually simply another error, and maybe one worse than the first one.” – H.L. Mencken

“The world always makes the assumption that the exposure of an error is identical with the discovery of truth–that the error and truth are simply opposite. They are nothing of the sort. What the world turns to, when it is cured on one error, is usually simply another error, and maybe one worse than the first one.” – H.L. Mencken

![]() FX Trading – The Greatest Currency Ever … (Go Ahead and Google It!)

FX Trading – The Greatest Currency Ever … (Go Ahead and Google It!)

It almost seems as if we’re witnessing a veteran prize fighter on the decline, not only failing to win fights but taking brutal beatings along the way.

While the case can certainly be made that the US dollar has many years ahead as world reserve currency, the sentiment is that it does not.

Holding the “official” number one spot – world reserve currency – keeps the US dollar under the spotlight. And the US economy is right there with it. So even though the US wasn’t the only nation to fall into a major slump after a global crisis brought on global recession, it is the nation that gets judged most critically and often receives the most blame.

Don’t get me wrong: the US is no bastion of prudent finance; especially not lately. And the markets are biting down hard on that fact vis a vis the US dollar. But in doing so, it seems there’s very little bite left for any other currencies whose economies are in similar positions. It’s mob mentality at its finest.

So perhaps investors are just jumping on a sure thing – the dollar must go down. Perhaps other countries and other currencies are irrelevant to most. Though it might be hard to make that specific case as investors are finding plenty of money to funnel into emerging markets stocks and currencies. (See below.)

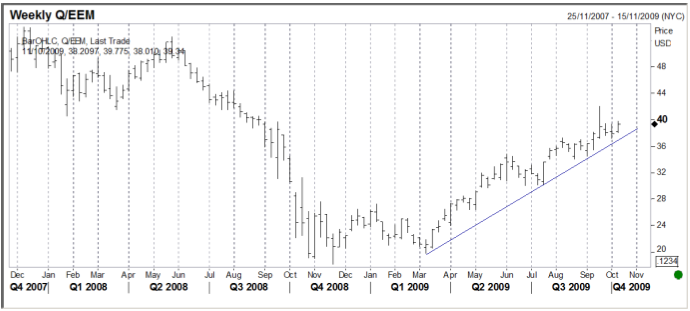

MSCI Emerging Market stock index, weekly:

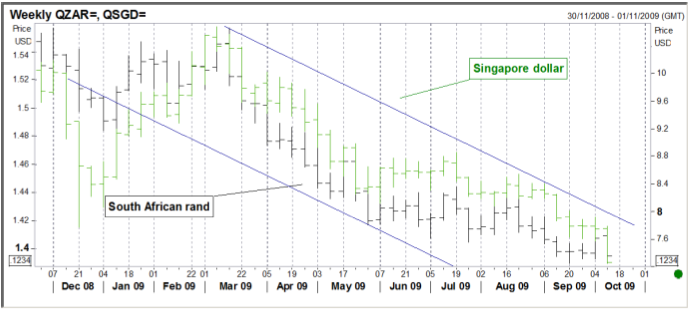

Singapore dollar and South African rand (USDSGD and USDZAR) weekly:

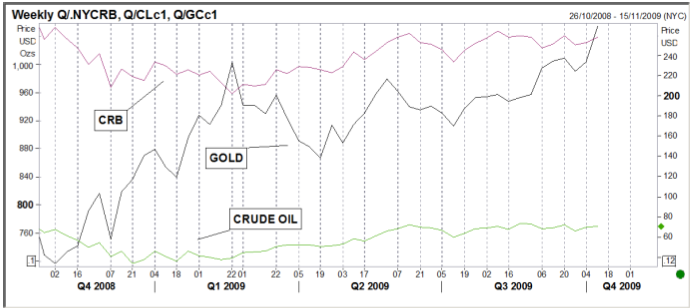

Must it go up just because the US dollar is going down? Maybe. Or perhaps vice versa. Perhaps gold is going up because investors really would prefer to steer clear of all currencies made of paper, especially the US dollar.

It’s been the mantra of gold bugs for as long as I can remember: paper currency is crap.

They are that convicted in their faith in the ultimate destruction of fiat and ultimate refuge of hard money – “Gold is the greatest currency ever created.” If you Googled ‘greatest currency ever’ I’d bet you’d find several articles trying to sell you on the unparalleled merits of gold as a currency.

Ok, we understand that (and will do our best to ignore the fact that the gold standard didn’t seem to work out as perceived. Don’t get me wrong, I love the idea of having a real money standard that will discipline politicians—for that reason alone we it would get my vote; but history shows countries cheated during the gold standard era and booms and bust didn’t go away).

We caught Jim Rogers for a brief moment on CNBC yesterday. Not surprisingly he was all over commodities – that’s the only place he’s putting his money, in case you were wondering. And whether or not he meant it, he categorized gold as a commodity when citing those commodities that were going through the roof, as they say.

Technically, gold is a commodity. But to investors, it’s only a commodity when it fits the commodity story; otherwise it’s a currency when it can fit the currency story.

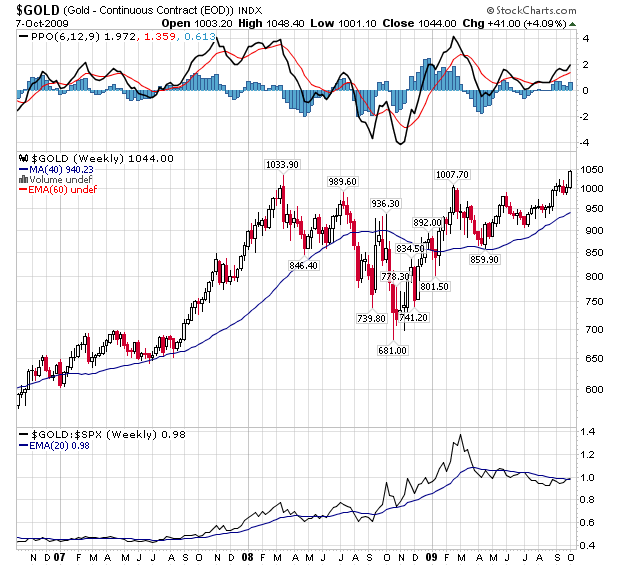

My point is: right now it seems to be a better fit for the currency story that gold bugs love. If it were a commodity story, then maybe we’d see things a little different from what the charts below tell us:

Gold, Crude Oil, CRB Weekly – last FOUR quarters …

New highs for gold; not so much for crude oil and the commodities index. Keep the global recovery and commodities story in your back pocket for another day.

John Ross Crooks III

Black Swan Capital LLC

Register HERE for the FREE Daily Currency Currents Newsletter.

Black Swan Capital is an independent minded currency advisory firm established to provide subscription-based services to help retail and institutional clients consistently attain above average profits trading and investing in both forex and currency futures markets. We tell our Members when to enter and exit and why. HERE for more information.

Our commitment is to deliver well researched trading recommendations that our clients understand and can efficiently execute through their brokers. We outline the reasons to enter a trade and define the risk. But our Members must understand there is a substantial risk of loss trading in forex (off-exchange retail foreign currency) and currency futures markets.

Register HERE for the FREE Daily Currency Currents Newsletter.As a subscriber to Currency Currents you stay tuned-in to our current global-macro view and our analysis of key investment themes driving currency prices. Nothing is off limits to us in this free-wheeling look at the markets. Some days you’ll receive ramblings on trading psychology, while other days we may take an academic approach in explaining esoteric economic issues. Ultimately we have one goal in mind: to help you get a handle on the key investment themes driving global capital flow. Because if you know where the money is going, it increases the probability that yourposition in the market will be a profitable one.

Ed Note: Dennis Gartman will be speaking at the:

The Money Talks All Star Trading Super Summit

Saturday, October 24, 2009 -The Sheraton Vancouver Wall Centre

Click HERE for the Speaker Lineup and to REGISTER if you want to take advantage of this Event.

“For me, pragmatism is not enough. Nor is that fashionable word,“consensus”….To me, consensus seems to be the process of abandoning all beliefs, principles, values and policies in search of something in which no one believes, but to which no one objects‐‐‐ the process of avoiding the very issues that have to be solved, merely because your cannot get agreement on the way ahead. What great cause would have been fought and won under the banner “I stand for consensus”? – Lady Margaret Thatcher, 1981

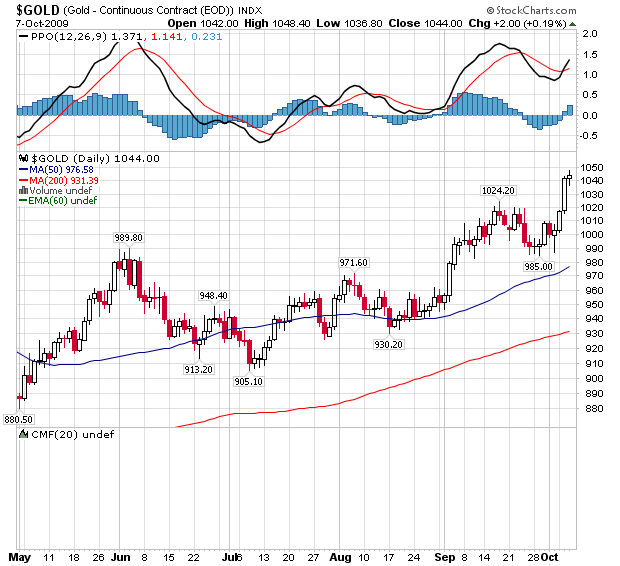

The debate in the gold market is whether the public is too heavily involved… or in some instances, involved at all. We have heard from friends in the business that the public is not nearly as involved in gold as it was back in the 80’s in the last great run up. Perhaps that is true, and we shall admit that we find it interesting that there are at least as many advertisements on television for gold selling opportunities as there are for those wishing to buy gold. We did not see that sort of thing back in the 80’s gold bull market. But gold is now the topic de jure almost everywhere, and while having dinner last evening at our club, the first question we were asked was “How much farther can gold go up?” We were asked this by an individual that had never, ever asked our opinion on anything financial before, and the question was clearly asked from a bullish… and hopeful… perspective.

We remain long of gold in Sterling, EUR and now US dollar terms, and having added to the position in dollar terms earlier this week, we’ll sit tight. We’d not argue, however, with those who might wish to write calls against their gold, for the premiums being offered are shockingly high. Indeed, we note that calls on gold $10 or $20 away from the current spot rate are demonstrably more expensive than are puts $10 or $20 below the current spot. This is evidence of the public’s willingness to bet bullishly of gold, and it is evidence, we thin, of an excessive speculative enthusiasm. Should gold make its way back down toward $1000-$1020, we’d be willing buyers once again; but at $1050, “Not so much:”

This brief comment from the Legendary Trader Dennis Gartman. For subscription information for the 5 page plus Daily Gartman Letter L.C. contact – Tel: 757 238 9346 Fax: 757 238 9546 or E-mail:dennis@thegartmanletter.com HERE to subscribe at his website.

Mr. Gartman has been in the markets since August of 1974, upon finishing his graduate work from the North Carolina State University. He was an economist for Cotton, Inc. in the early 1970’s analyzing cotton supply/demand in the US textile industry. From there he went to NCNB in Charlotte, N. Carolina where he traded foreign exchange and money market instruments. In 1977, Mr. Gartman became the Chief Financial Futures Analyst for A.G. Becker & Company in Chicago, Illinois. Mr. Gartman was an independent member of the Chicago Board of Trade until 1985, trading in treasury bond, treasury note and GNMA futures contracts. In 1985, Mr. Gartman moved to Virginia to run the futures brokerage operation for the Virginia National Bank, and in 1987 Mr. Gartman began producing The Gartman Letter on a full time basis and continues to do so to this day.

Mr. Gartman has lectured on capital market creation to central banks and finance ministries around the world, and has taught classes for the Federal Reserve Bank’s School for Bank Examiners on derivatives since the early 1990’s. Mr. Gartman makes speeches on global economic and political concerns around the world.

Twenty-five years ago, without a high school diploma or even a day’s worth of training, I found myself working as a stockbroker. I know that sounds hard to believe, but it’s the God’s honest truth. My last job before entering The Street was as a warehouse manager where I stacked boxes, oversaw inventory, and managed a few employees. But on my own time — lunch break, at night, and any minute I could eek out in between – I studied the markets. The whole Wall Street phenomena fascinated me, which lead me to start an investing club that grew to over 100 members. That’s where I was “discovered” by an honorable man who owned a NYSE-member brokerage firm. At the ripe-old-age of 28 I took my self-taught financial acumen and entered the stock biz.

Unfortunately, this newbie salesman/broker stunk at the very lifeline to building a book of business: cold-calling. One hang-up and I was done for the day. Thankfully, my boss published an investment newsletter and suggested I try one, too. I had demonstrated some decent analytical skills and he thought that by putting my views in writing I might overcome my horrific phone talents. That’s how The Grandich Letter began.

The early letters were little more than my thoughts typed (as in, from a typewriter) on pieces of paper, mimeographed and given to mostly prospective clients…..

….read pages 2-11 HERE including the Bottom Line.

The debate over deflation/inflation continues as some of our most astute economic observers take sides. It is interesting for me to see some great commentators take opposing positions on one of the most important topics of our time. Frankly, I think that both sides are missing part of the picture. The debate concentrates on the after shocks of inflation/deflation: prices.

“Prices” are the visible barometer that both sides of the debate gauge. The inflationists see (or warn about) “rising prices”. The deflationists see (or warn about) “falling prices”. There are very convincing cases by both sides.

In “real time” October 2009, the deflationists seem to have the upper hand. They point out that we have a “deflationary economic environment” due a variety of factors that are contributing to falling prices (such as deleveraging and unemployment). Inflationists see the current stage being set for future rising prices due to factors such as expanding money supply and a weakening dollar. What is the real deal?

First, let’s set the record straight on the terms…

Inflation: Is the condition where more money (such as a paper currency) is created by the issuing authority (the government’s central bank) and this growing supply of money is chasing a fixed basket of goods and services (and/or assets). Inflating the money supply (“monetary inflation”) is the problem and the symptom is usually rising prices (“price inflation”). Inflation is not the price of things going up…it is the price (or value) of money going down.

Deflation: Generally the opposite…The money supply is stable or shrinking relative to the supply of stuff we buy and subsequently there is less money chasing goods and services. In this case, the “value” of money usually increases.

Therefore, for prices to rise there needs to be more (and growing) money supplied to the market relative to what is being bought. Two things need to happen for prices to rise from an inflationary perspective:

- More money needs to be created.

- This money needs to “chase” what is being purchased (Think “circulation” or “velocity”).

This is a crucial point. Prices won’t go up just because the money supply expands; the money has to be actively “chasing” those goods or services (or assets) for the prices to see upward movement. For prices to go up (“price inflation”), you need monetary inflation (increasing the money supply) and velocity (the money is chasing goods, services and/or assets).

In recent years, the money supply has indeed expanded dramatically…but…relatively little “chasing” has been going on. If the Federal Reserve instantly created $10 trillion dollars and gave it to you, that is definitely monetary inflation but…if you merely put it in your sock drawer and hoard it, then it would not circulate (chase stuff) and therefore you wouldn’t see “price inflation”.

This is where part of the confusion and controversy is. Inflationists point out that money supply is growing dramatically and they are correct. Deflationists point to falling prices in many areas of the economy and they are also correct. Here is what we should be aware of…

THE PRICES OF GOODS, SERVICES AND ASSETS ARE MOST AFFECTED BY TWO FUNDAMENTAL FACTORS:

- THE MONEY SUPPLY (primarily enacted by government)

- DEMAND AND SUPPLY (primarily enacted by the marketplace)

Understanding the money supply (its growth or shrinkage) coupled with understanding “demand and supply” will give you a better picture of the economy. This, in turn, will make you a better analyst, money manager or investor. More on this in Part II.

This article appeared in Resource Investor. Sign up for their FREE Weekly Newsletter HERE.

Paul Mladjenovic, CFP is the author of Stock Investing for Dummies and Precious Metals Investing for Dummies. Paul’s latest educational program is How to Cash in on the Commodities Super Boom Seminar. His national financial seminars are at www.ProsperityNetwork.net and his blog is www.Mladjenovic.blogspot.com.

Quotable

“Hope always seems to spring eternal in liquidity-driven financial markets. That is very

much the case today in the aftermath of the biggest liquidity injection in modern

history. Unfortunately, along with that hope comes an acute sense of short-term

memory loss – notably, a failure on the part of the broad consensus of investors to grasp

the toughest lessons of the Great Crisis and Recession of 2008-09. This is a dangerous

combination for increasingly frothy financial markets. – Stephen Roach

….full comment HERE.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair