Daily Updates

{mp3remote}http://www.howestreet.com/index.php?pl=/goldradio/index.php/mediaplayer/1439{/mp3remote}

Cycles…

From the October 2009 HRA Dispatch

David Coffin & Eric Coffin, HRA Advisories

Mayan Indian elder Apolinario Chile Pixtun has restated his belief that the world is not going to end in 2012. Or more precisely, that his beliefs don’t suggest the world should end despite it being the end of a major cycle in the Mayan calendar. According to China Daily, he is even more emphatic that he’s tired of being asked about it. 2012 is the end of a 5126 year cycle (end of the 13th of 13 Baktun). It also ends a 26800 year cycle that may relate to the Earth’s wobble, which is useful for gauging the drift of seasonal climate changes. China Daily also briefly mentions predictions by 16th century (Christian calendar) French herbalist Nostradamus that is being combined with the Mayan cycles to create buzz for a spate of movies and TV specials.

The Nostradamus’ predictions appear to be linear rather than cyclical. It’s hard to say since, like most good prophesy, they’re in code. The cycles described in Mayan calendars still have the more universal appeal. It’s comforting to think things will come around again. Mesoamericans outlined complex calendars that, we’re told, are quite accurate. That does make them useful to time planting, and also to justify the timing of power shifts. We assume feeding people generated much of the early buzz around star gazing, but as usual the technical breakthrough brought hangers-on.

Perhaps it will be 2012 when western economies at the centre of the debt/housing bubble hit that wall of resignation that creates a final bottom. That will partially depend on how the interest rate cycle plays out in each of them. Capital will continue to seek the safety of bonds for a while yet, assuming its not central banks doing all the buying. As long as yields stay low mortgage resets will keep some weaker players afloat. Bottoms are marked by capitulation, which for debt usually comes when rising interest rates submerge those still treading water. Yields would normally have to go a long way to generate this impact but this cycle features many overextended borrowers that need plenty of time to earn down debt loads.

Right now there is much confusion about whether a “typical” market cycle even applies. Asian growth economies that function somewhat differently than western markets (and differently than each other) are clouding crystal balls. These effects are skewed even more by price shifts against currencies. We seem to be between cycles, and probably are. In our little bit of the galaxy this means coming up with a new gauge for the price vs. stocks equation for copper and some other metals.

Most of the capital that flowed into copper earlier this year plans to use the stuff at some point, and sees potential for a supply squeeze. The question is whether taking a gain now will be rewarded with a lower buy-back price before the stocks are needed. Normally that would work but with metals being used as inflation hedges and pair trades against weak currencies prices (at least dollar prices) have gotten detached from the inventory cycle.

Notwithstanding last week’s new highs for gold, producer stocks move hesitantly, with plenty of traders waiting for “the other shoe to drop”, whatever that might be. Metals in general are continuing their anti-dollar rally. While we would still like to see falling inventories on the base metal side inventory levels have at least been flattening in the case of most metals and falling for zinc and aluminum. There is fear of bubbles and a multiplying list of grumpy bears now that the Dow has added a digit the way gold already had. Yes, a lot of this has to do with a flood of liquidity and speculation on what level profits (or the USD) might be at a year or two out. But, as we’ve noted several times recently its better to deal with the market that is than to try and tell it what to do.

Even though it’s considered the height of irrationality by some, renewed strength in many asset classes can continue as long as central banks flood the markets with liquidity and drive down the returns on competing assets like government debt.

The day may come when that won’t work any longer and bond yields take off so taking profits regularly continues to be a good idea. The day may come sooner when other central banks, the ECB in particular, start trying to jawbone their own currencies lower which could give the greenback a bounce and metals a correction. We expect that would be a correction however, not a panic, and those central banks will still have to prove they can back up words with actions. Jawboning is only a stop gap measure and the Dollar Index has breached several important technical levels on the downside. There will be support for most markets as long as decent economic stats continue to be reported and there is belief that the recession is at least easing. While we agree this is mainly (but not wholly) a currency trade, the longs in commodities have reason to be skeptical that central banks will “get it right” or that some turn of events will create a new batch of Dollar bulls. Central banks do no have the best of track records when it comes to controlling liquidity flows.

It would be nice to have some magic ratio that says “metal X is a buy when inventories equal Y and the US Dollar Index is at level Z”. We would like to say we that we already know, but we can’t. Unfortunately, we left our codebook in the other computer and, unlike Mayan calendars; we don’t think anything in this market is carved in stone.

Gain access to potential gains of hundreds or even thousands of percent! From March to June, HRA introduced four new gold explorers to subscribers. Those four companies have generated an average gain of 205%, to date! SPECIAL HRA OFFER: For a limited time only, HRA is offering free reports and a subscription savings. Click here for more information: http://www.hraadvisory.com/sh2009.html

The HRA – Journal, HRA-Dispatch and HRA- Special Delivery are independent publications produced and distributed by Stockwork Consulting Ltd, which is committed to providing timely and factual analysis of junior mining, resource, and other venture capital companies. Companies are chosen on the basis of a speculative potential for significant upside gains resulting from asset-base expansion. These are generally high-risk securities, and opinions contained herein are time and market sensitive. No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer, solicitation or recommendation to buy or sell any securities mentioned. While we believe all sources of information to be factual and reliable we in no way represent or guarantee the accuracy thereof, nor of the statements made herein. We do not receive or request compensation in any form in order to feature companies in these publications. We may, or may not, own securities and/or options to acquire securities of the companies mentioned herein. This document is protected by the copyright laws of Canada and the U.S. and may not be reproduced in any form for other than for personal use without the prior written consent of the publisher. This document may be quoted, in context, provided proper credit is given.

©2009 Stockwork Consulting Ltd. All Rights Reserved.

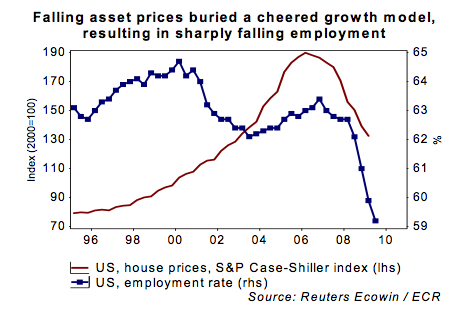

(Ed Note: This analysis courtesy of Victor Adair who notes that its been translated from Dutch so some of the syntax and grammar may not be familiar)

Great uncertainty regarding growth expectations

The bursting of the asset price and credit bubbles brought an end to the old growth model for Western consumption growth, based on credit growth with rising asset prices as collateral. Setting up a new growth model is complicated, however, and will be accompanied by painful measures. The way of less resistance for the authorities is therefore a return to the old growth model. This way is not without pitfalls, however.

There is a continual threat of a deflationary spiral as long as overcapacity remains great, consumers want to save more and repay debts and asset prices continue falling. To prevent this, the authorities have to stimulate the economy and financial markets sufficiently. It’s easy to make a mistake, however. If the economy is overstimulated, then the risk of higher inflation and long-term interest rates quickly increases. With too little stimulation, the economy can slide back into a deflationary spiral. Both ‘errors’ then have to be corrected by stimulating or tightening twice as hard. On balance, this generates a picture of volatile, but low growth for the coming years.

….read the whole document HERE.

Global Imbalances to Result in Complete Economic Chaos

Brazil announced this week that they will be implementing a 2% tax on fixed-income and equity purchases by foreign investors in an attempt to curb the appreciation of the Brazilian real, which is up 32% this year against the U.S. dollar. Brazil is trying to deter foreign investors from investing into their country, in an attempt to artificially prop up the U.S. dollar.

It is completely absurd for Brazil to care so much about having the ability to export their products to Americans who can’t afford them. They should be allowing the real to appreciate in value so that their citizens can enjoy an increased standard of living. The only people who will benefit from Brazil’s actions are those who own exporting companies in Brazil. The overwhelming majority of the people in Brazil will suffer, as the country will likely continue adding to their $231.5 billion in U.S. dollar reserves that will eventually be completely worthless.

Federal Reserve Chairman Ben Bernanke said this week that the U.S. should cut down on its budget deficit in order to reduce global imbalances. This is hypocritical, as it’s Bernanke who is allowing the U.S. to have such huge budget deficits by monetizing our government’s spending. Bernanke is the only person with the power to put a stop to the madness, but in his campaign to get reappointed, he most likely promised everybody in Washington that he would continue monetizing their spending in the future.

Bernanke continues to claim that the recession is over and the financial crisis is behind us, but the global imbalances he admits we still need to correct are getting more out of control than ever. Consumer spending now accounts for 71% of the U.S. GDP, well above the long-term average of 65%. If global imbalances were to correct, we would need the consumer spending portion of GDP to overcorrect down to below 60% for an extended period of time. This would certainly put the U.S. in a very deep recession, but only then would our economy have a real chance of truly becoming healthy.

After the U.S. financial markets collapsed in late-2008/early-2009, we saw the U.S. personal savings rate triple to a high in May of 6.2%. This was a step in the right direction but it didn’t last for long. The savings rate has since then fallen three months in a row back down to 3%. Any progress that was made has been lost. The imbalances are growing to new extremes that will eventually result in complete economic chaos and hyperinflation. Our only chance to rein in the imbalances before they do irreparable harm is to follow in the footsteps of the Reserve Bank of Australia and dramatically raise interest rates immediately.

Many so-called financial experts and stock analysts on CNBC have been proclaiming the rapidly declining U.S. dollar to be good for the U.S. economy, because it will boost our exports. We need to increase exports, but our country doesn’t produce enough products to export. In order to increase the manufacturing of products to export, we need to increase savings. Without savings, it is impossible to build new factories. A falling U.S. dollar discourages Americans from saving and destroys the value of savings.

A declining U.S. dollar is bad for all Americans. Oil prices are now back above $80 per barrel; gas prices will inevitably rise back above $4 per gallon. Last time gas rose above $4 per gallon, Congress held countless hearings trying to figure out why oil prices were rising, when in fact they were the ones causing it. Congress’s deficit spending and Bernanke’s willingness to monetize it creates the inflation that drives oil prices up. Let’s see if they figure it out this time, or if they once again place the blame on speculators and the free-market.

Please spread the word about NIA and have your friends subscribe for free at http://inflation.us

The National Inflation Association is an organization that is dedicated to preparing Americans for hyperinflation and helping Americans not only survive, but prosper in the upcoming hyperinflationary crisis.

With an $11.4 trillion national debt and $55 trillion in unfunded obligations for programs such as Social Security, Medicare and Medicaid, it is our belief that the United States for all intents and purposes is bankrupt and Americans need to take steps immediately to protect themselves from the potential loss of the purchasing power of their U.S. Dollars.

With total United States Federal Reserve and Treasury bailout commitments now at $14.1 trillion, of which $3.7 trillion has already been spent, we believe the largest financial crisis in history is ahead of us as a direct result of the U.S. government unwilling to accept a much needed recession.

It is our belief that foreigners will eventually stop lending the U.S. money and the Federal Reserve will most likely have to print the money to fund our deficit spending out of thin air.

The U.S. has abused its status of having the world’s reserve currency for far too long. With the potential for China to become a net seller of U.S. Treasuries to fund their own rightfully deserved stimulus plans, we believe there will soon be a run on the U.S. Dollar and a rush into hard assets like Gold and Silver.

Our goal is to help as many Americans as possible become aware of the disaster we are rapidly approaching. In our opinion, the wealth of most Americans could get wiped out during the next decade, but it will be an opportunity for a small percentage of Americans to become wealthy by investing into companies that historically have prospered in an inflationary environment, such as Gold and Silver miners and Agriculture producers.

Please sign-up to our free newsletter today to receive our latest stock suggestions and articles before they are posted on Inflation.us:

Fears of inflation and large U.S. budget deficits drove the dollar on Wednesday to its weakest level since August 2008 and helped push oil prices to their highest in more than a year.

The euro rose above $1.50, while crude oil prices climbed over $81 a barrel in trading on the New York Mercantile Exchange.

Analysts said that investors and traders are worried that the Federal Reserve, fearing another dip in the economy, will hold interest rates low for too long and fuel a bout of inflation. And investors also fear that the Obama administration will be unable to rein in trillions of dollars of deficit spending used to revive the economy.

….read more HERE.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair