Daily Updates

“Crude oil is the bloodline of the world. The world depends on oil to the point of political danger, which is why alternative energy will continue to grow in the future. As investors, we’ll continue to keep our eyes on good opportunities in gas, uranium, green energy, solar and wind energy. These have potential but it’ll still be many years before petro will be replaced or partially replaced.

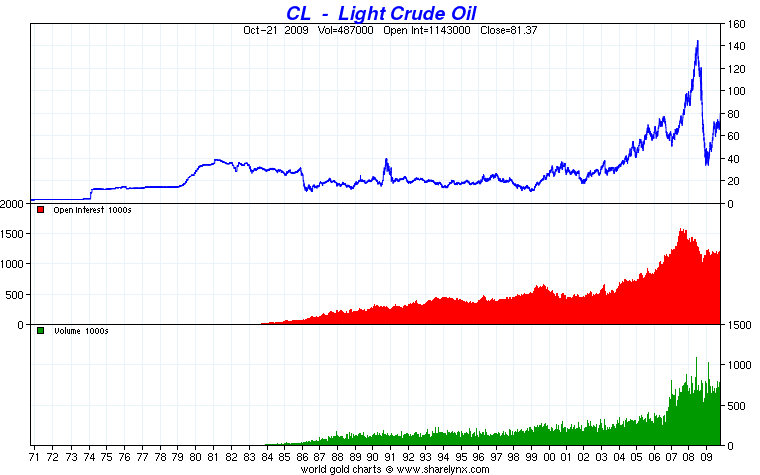

Meanwhile, oil’s upside also has great potential. Over the last 12 years, oil has been rising in a clear uptrend. While it temporarily dipped below this trend during the heat of the crisis last year, oil quickly bounced back this year, rising 75%.

Oil is now coming up from an extremely bombed out level. . .starting a multi-year rise, similar to 2001 when it was also near the lows.

Keep an eye on oil; it’ll remain very strong above $73 and while it’s been resisting in recent weeks once it closes above $81.50, a new high for the move could take oil to possibly $90. Oil’s major trend is up above $65.

Overall, we believe that a commodity boom will thrive as shortages for raw materials grow and demand continues to boom. We want you to stay invested and take advantage of the ongoing rises in these sectors as they evolve.” – Aden Forecast (11/17/2009)

A sizeable population of pundits is permanently bearish on crude oil prices. Earlier this year, when oil still hovered around USD40/barrel, plenty of bears predicted that oil prices would slump to USD20/barrel by the end of 2009.

And even as oil prices headed higher in the spring, several of these prominent bears continued to fight the tape, claiming that the ‘fundamentals’ didn’t support the rally in oil prices. As the rally continued some of the most prominent bearish arguments attributed the rise in oil prices to a weak dollar and/or the nefarious machinations of a group of speculators on the NYMEX futures market.

And this isn’t a recent phenomenon. The Energy Strategist turns 5 years old next March; in the first month of its publication, I was invited on a radio show to discuss energy prices. I spent most of the 20-minute segment debating the path of oil prices with the host, who maintained that U.S. oil supply and demand conditions didn’t support crude prices above USD50 a barrel—a level that was considered elevated at the time.

The relationship between U.S. inventories and oil prices has continued to deteriorate over the past year and a half. The big run-up in crude inventories from mid-2008 through early 2009 appeared to validate the oil bears’ thesis; inventories rose sharply, and crude prices fell precipitously during the financial crisis. But in 2009 oil has soared to over $80 a barrel, even as inventories continue to hover just off 20-year highs.

The relationship between U.S. oil inventories and global crude oil prices is broken for the simple reason that most of the marginal growth in oil demand is coming from the developing world. Viewing U.S. oil supply and demand numbers in a vacuum no longer suffices as an accurate proxy for movements in global oil markets. Nevertheless, a number of bearish analysts continue to trumpet the inconsistencies between U.S. inventories and global prices as unsustainable and the precursor to a major collapse—the same mistake they made in 2005 and 2006.” – Energy Strategist (11/18/2009)

The Energy Report HERE

Quotable

“Japan doesn’t need a stronger yen. Japan needs deregulation of its labor and capital market, privatization of state-owned industries, and a more pragmatic, progrowth domestic industrial policy focused on excising vested interests and the rigidities of domestic service industries. The promotion of growth and entrepreneurship is the only way to generate the kind ofemployment that the DPJ promised on the campaign trail. Unfortunately, this kind of policy path is particularly difficult for Mr. Hatoyama’s government, which is heavily reliant on labor unions for political support.”

FX Trading – Friday Ramble

I noticed a Reuter’s poll today. All the top banks were asked to provide their guess on just how undervalued the Chinese currency—yuan- was against the US dollar. The averageguesstimate was about 20%. That’s about 20% lower than my guess would have been, but no matter. What was interesting was their guess about when the Chinese currency would actually become convertible.

……read more HERE

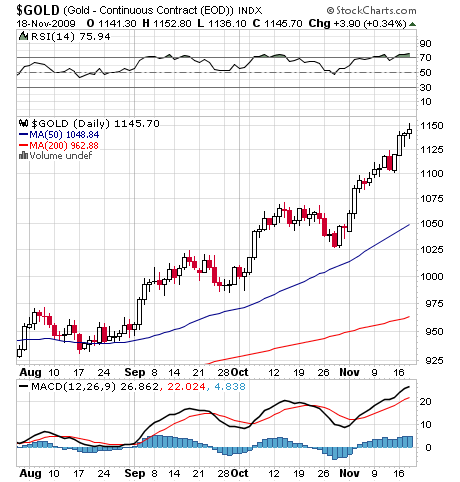

The rise in the gold price above $1,100 per ounce last week is a pretty good indicator that something has changed. For 18 months, the gold price had been in a trading range topping out around $1,000. It has now broken out decisively from that range. The opportunity for the world’s central banks to change policy and affect the economic outcome has been lost. The world economy is now locked on to an undeviating track towards another train wreck.

At most times, the gold price is not an economically significant indicator. In 1980-2000, it declined irregularly from $850 to around $280, and movements in it seemed to have had little or no effect on the global economy. That’s what you’d expect; even at $1,000 per ounce, the global production of gold is only around $100 billion annually, which would put the entire world’s gold extraction industry only 17th on the Fortune 500. When Gordon Brown sold Britain’s entire gold reserves in 1999, at a price below $300 per ounce, it seemed a defensible decision. I went to a meeting in 2001 hosted by a diverse group which believed that the U.S. Treasury was conspiring to suppress the gold price, and my main thought was: why would Treasury bother?

However, in relatively few periods, gold becomes of immense importance. When investors lose trust in conventional currencies, because monetary policy appears set to debauch them, gold is the immediately available safe haven. During such periods, gold’s former importance as a store of value becomes uppermost in the public mind, and its price becomes a major economic indicator.

Gold became important from about July 1978 to early 1980, during which period its price rose from $185 to $850 per ounce. For that 18 month period, the price of gold was the most important factor in day-to-day market fluctuations. The gold price, more than the inflation rate directly, moved markets and by extension moved monetary and to some extent fiscal policy in the major economies. Only after Paul Volcker took over at the Fed in late 1979 did M3 money supply begin to supplant it in investors’ analyses.

We now appear to be at the beginning of another such period. The exceptional monetary stimulus entered into around the world during the financial crisis last year has prevented a downward liquidity spiral, but at the cost of destabilizing markets. Both monetary and fiscal policy dials are stuck at settings that would have been unimaginable two years ago. While this has produced only the beginnings of economic recovery, it has brought a 50% bounce in the U.S. stock market, a return in the oil price to around $80 – at the top end of the historic range, adjusted for inflation – and now a breakout by gold above its historic high. The repeated previous failure of gold to break above $1,000 per ounce made it all the more significant when it finally succeeded in doing so.

Ben Bernanke’s Fed is ignoring this. It insists that it will maintain interest rates at the current near-zero level for an extended period, regardless of what the gold price does. By this, it is ensuring that the present bubble in gold and commodities will play out to its full extent. Had the Fed begun to tighten gently during the late spring or early summer, when it had become obvious that the U.S. economy was bottoming out, but while stock markets remained subdued and gold remained within its 2008-09 trading range, it’s possible that it could have deflated the incipient bubble, steering the U.S. and global economies back on to a sustainable growth path. The U.S. Treasury would have had to cooperate by beginning to reduce the federal deficit, but at this stage with unemployment in the 10% range, there would have been no need for draconian action on that front.

With current Fed policy, gold is headed rapidly toward $2,000 per ounce, probably within six months. The forecasters who see such a price, but suggest it would take four to five years to get there, are ignoring history. Since gold was able to get from $185 to $850 in 18 months in 1978-80, there is no reason why it cannot get from $1,100 to $2,000 in six months now. What’s more, although 1980’s peak seemed madness at the time, and was equivalent to nearly $2,400 today, there is no reason why gold cannot go much higher if it is given another year or so to get there. The supply of gold from new mining is around 1 million ounces per year LESS than in 1980 and the supply of speculative capital that could flow into gold is many times greater. Hence, a $5,000 gold price is possible though not certain, if present monetary policy is continued or only modestly modified – and that price could be reached by the end of 2010.

As was demonstrated by the housing bubble of 2004-06, modest rises in interest rates are not sufficient to stop a bubble once it is well under way. Given the Fed’s recent track record, it is most unlikely that we will get any more than modest and very reluctant interest-rate rises. Even if inflation is moving at a brisk pace by the latter part of next year, the price rises will be explained away, or possibly massaged out of the figures as happened in the early part of 2008. Hence the bubble will inexorably move to its denouement, at which point gold will probably be north of $3,000 an ounce and oil well north of $150 per barrel. Even though there will be no supply/demand reason why oil should get to those levels, and gold has almost no genuine demand at all, the weight of money behind those commodities in a speculative situation will push their prices inexorably upwards, beyond all reason until something intervenes to stop it.

At some point, probably before the end of 2010, the bubble will burst. The deflationary effect on the U.S. economy of $150 plus oil will overwhelm the modest forces of genuine economic expansion. The Treasury bond market will collapse, overwhelmed by the weight of deficit financing. Once again, the banking system will be in deep trouble. The industrial sector, beyond the largest and most liquid companies and the extractive industries, will in any case have remained in recession – it is notable that, in spite of the Fed’s frenzy of activity, bank lending has fallen $600 billion in the last year. Unemployment, which will probably enter the second downturn at around current levels, will spike further upwards. The dollar will probably not collapse, but only because it will have been declining inexorably in the intervening year, to give a euro value of $2 and a yen value of 60 to 65 yen to the dollar.

In the next downturn, the Fed will not be able to cut interest rates, because inflation will be spiraling, as in 1980. Instead it will need to raise them while dealing with a profound crisis in the bond markets. Capital in the U.S. will become still more difficult to come by, and unemployment will approach 15%. The U.S.’s only saving graces will be that the inflation will have prevented much further decline in the nominal prices of houses, while the decline in the dollar will have finally swung the payments deficit towards balance. U.S. real wages will be forced downwards by high unemployment, while banks’ relief on the home mortgage front will be balanced by a tsunami of collapsed credit card debt and other consumer debt.

2011 and 2012 will be very unpleasant years, as the Obama administration struggles to get closer to budget balance without pushing up taxes so far as to cause yet a third recession. Stock prices will be at or below their March 2009 lows, and will stay there even as earnings of export-oriented companies will be robust. (Conversely, retailers dealing in cheap imported goods, such as Wal-Mart, will be devastated.) Wages will be generally declining relative to prices, although may show some growth in nominal terms as inflation will be considerable. Foreign goods and services will be inordinately expensive in dollar terms.

The danger in those years will be that Ben Bernanke will attempt yet again to refloat the U.S. economy through inflation, buying government debt to fund the deficit and forcing short term rates well below the inflation rate. This danger is exacerbated by the Obama administration’s insouciance about deficits. Ben Bernanke on his own (and his predecessor Alan Greenspan) bears a large share of responsibility for the 2008 crash, but the Bernanke/Obama combination is potentially even more dangerous. If expansionary monetary and fiscal policies are pursued regardless of market signals, the U.S. will head towards Weimar-style trillion-percent inflation. That would make the government’s position easier as its mountain of Treasury debt became worthless, but devastate everybody else’s savings and impoverish the American people as Weimar impoverished 1920s Germany.

As I said, a train wreck. Probability of arrival: close to 100%. Time of arrival: around the end of 2010, or possibly a bit earlier. And at this stage, there’s very little anyone can do about it; the definitive rise of gold above $1,000 marked the point of no return.

The Bears Lair is a weekly column that is intended to appear each Monday, an appropriately gloomy day of the week. Its rationale is that, in the long ’90s boom, the proportion of “sell” recommendations put out by Wall Street houses declined from 9 percent of all research reports to 1 percent and has only modestly rebounded since. Accordingly, investors have an excess of positive information and very little negative information. The column thus takes the ursine view of life and the market, in the hope that it may be usefully different from what investors see elsewhere.

Martin Hutchinson is the author of “Great Conservatives” (Academica Press, 2005). Details can be found on the Web site www.greatconservatives.com

Near the Bottom New Bull?

The December Uranium Futures closed at $43.00 DOWN 1.00. The current bear market low is $42.00. June 13, 2007 hosted the bull market high of 154.95. Major support lies well under the market at $36.00.

The spot price of uranium quadrupled from 2004 to 2007. When it hit $138/lb, uranium became a certified bubble, which has now burst. For investors, this is the best possible news, of course. Nuclear power is the ultimate alternative fuel, as the French will tell you. You get all the power, 84% cheaper than coal, with none of the politics of rogue nations and none of the greenhouse emissions.

A friend of mine in the mining business told me (probably old news) that Denison Mines had closed a couple of its uranium mines due to current market conditions relative to uranium. To my way of thinking this is a sure sign we’re probably at or near the low for uranium.

Small Losses Equal Big Profits

Each week we receive dozens of E-mails from investors that have a history of great trades and yet their portfolios fail to grow. The most common trait in each of these cases is the failure to manage losses properly.

The facts are obvious! No one can successfully predict the market in every case so the key is to take small profits regularly and prevent losing plays from significantly eroding capital. Losses are bound to happen, they are inevitable; but that shouldn’t keep you from profiting on a regular basis. The fact is, it’s very difficult for most investors to close out losing plays early. Successful traders understand there is no reason to hang on to a losing position when there are so many other profitable plays that deserve their time and money.

Emotion is the capital killer! Hope, greed and fear all conspire to remove money from your account that you will never see again. What generally happens is that the trader says to himself, “If I just hold on…I’ll eventually break even”; “It can’t go lower!”; “It’s going to come back…it has to!”; The reality is, it rarely does.

One of the best ways to avoid this trap is to use a trading plan with pre-determined exits. Stop-loss orders can be used to remove on-the-spot decision making from the equation, and trailing stops can be used to follow a position into greater profits while protecting for reversals.

If you are going to have a plan, stick with it. Don’t jump into trades on emotion, wait for the proper entry points. Study and identify trends within individual issues before opening a position. Use technical support areas as buying opportunities and sell on rallies towards resistance. One of the oldest phrases is; “Buy on down days, sell on up days” and it is really not that difficult.

If you discover that your losses are consistently larger than your gains, stop trading! Step back, take a break, a few days off. When you are ready to try again, evaluate your trading strategies and review the losses to learn from previous mistakes, then move on!

Success will come when you create a favorable balance between hard work, sound judgment and patience. Too many traders give up after a few losing plays, long before they have time to learn and absorb the various methods required for profitable trading.

I have been told the feedback from “The MoneyTalks Allstar Trading Super Summit” in Vancouver on October 24 was excellent and my presentation very popular.

A the video of the conference is now available for purchase. A special promotion code has been created for VRtrader.com clients. Using this code you can get a 50% discount on the $117 price. The StockScores promotion code is – S2009ML

Folks just go to www.moneytalks.net , Click on the Banner box titled “The MoneyTalks Allstar Trading Super Summit Video“. This will take them to the shopping cart where the process is pretty straightforward.

Enjoy!

Marks VRTrader Silver Newletter covers Stock, TSE Stocks, Bonds, Gold, Base Metals, Uranium, Oil and the US Dollar.

More kudos – Mark Leibovit was named the #1 Intermediate Market Timer for the 10 year period ending in 2007; the #1 Intermediate Market Timer for the 3 year period ending in 2007; the #1 Intermediate Market Timer for the 8 year period ending in 2007; and the #8 Intermediate Market Timer for the 5 year period ending in 2007. NO OTHER ANALYST SURVEYED APPEARED IN ALL FOUR CATEGORIES FOR INTERMEDIATE MARKET TIMING AS PUBLISHED IN TIMER DIGEST JANUARY 28, 2008!

For a trial Subscription of The VR Silver Newsletter covering Stocks, Bonds, Gold, US Dollar, Oil CLICK HERE

The VR Gold Letter is available to Platinum subscribers for only an additional $20 per month, while for Silver subscribers the price is only an additional $70.00 per month. Prices are going up very shortl, so act now! Separately, the VR Gold Letter retails for $1500 a year! The VR Gold Letter is published WEEKLY. It is 10 to 16 pages jam-packed with commentary and charts. Please call or email us right away. Tel: 928-282-1275. Email: mark.vrtrader@gmail.com .

This brief initial comment from the Legendary Trader Dennis Gartman. For subscription information for the 5 page plus Daily Gartman Letter L.C. contact – Tel: 757 238 9346 Fax: 757 238 9546 or E-mail:dennis@thegartmanletter.com HERE to subscribe at his website.

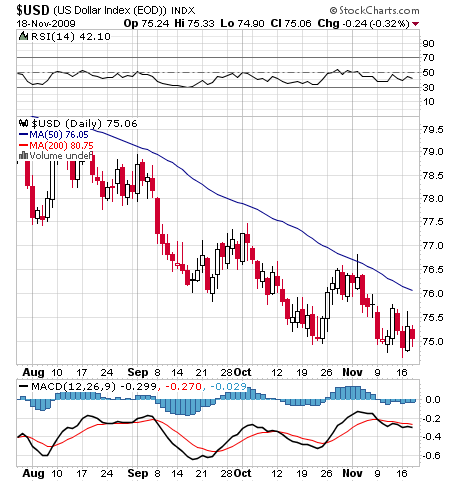

THE US DOLLAR IS FIRMER, AND IT IS ALMOST UNIVERSALLY SO, that is, the dollar is stronger relative to almost every other currency in our daily matrix of prices save for the Chinese Renminbi. Now, let us begin by understanding that the dollar is not materially stronger, for the movement over the course of the past twenty four hours are really rather modest by almost any standards. For example, over the course of the past thirty six hours of trading, the EUR/dollar rate has remained within the range of 1.4875 at the EUR’s worst levels and 1.4980 at its best. However, it is the “universality” of the dollar’s strength, modest though it might be, that has our interest as we write. We get the very real sense that the long-awaited material correction in the US dollar is about to begin.

Turning then to gold, firstly we note that as the dollar strengthens gold is of course weakening… but not all that much! Indeed, in foreign currency terms over the course of the past twenty four hours, gold is quite strong, vindicating our position of being long of gold predicated primarily in terms of other currencies other than the US dollar.

Dennis Gartman spoke about his timeless trading strategy at the Super Summitt go HERE for the Speaker Lineup and Sign Up HERE, Much more from some of the worlds best traders including:

Mr. Gartman has been in the markets since August of 1974, upon finishing his graduate work from the North Carolina State University. He was an economist for Cotton, Inc. in the early 1970’s analyzing cotton supply/demand in the US textile industry. From there he went to NCNB in Charlotte, N. Carolina where he traded foreign exchange and money market instruments. In 1977, Mr. Gartman became the Chief Financial Futures Analyst for A.G. Becker & Company in Chicago, Illinois. Mr. Gartman was an independent member of the Chicago Board of Trade until 1985, trading in treasury bond, treasury note and GNMA futures contracts. In 1985, Mr. Gartman moved to Virginia to run the futures brokerage operation for the Virginia National Bank, and in 1987 Mr. Gartman began producing The Gartman Letter on a full time basis and continues to do so to this day.

Mr. Gartman has lectured on capital market creation to central banks and finance ministries around the world, and has taught classes for the Federal Reserve Bank’s School for Bank Examiners on derivatives since the early 1990’s. Mr. Gartman makes speeches on global economic and political concerns around the world.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair