Daily Updates

Many stock analysts will tell you the basic strategy in the market is to buy low and sell high. While I’ve done that successfully for years, it’s not as easy as it sounds. What’s more, it’s a lot more difficult in bear markets and markets bound in trading ranges, which are two distinct possibilities going forward.

So an alternative might be to PARTNER with companies — and you do that by buying stock in companies that pay you regular cash dividends.

That’s the basic principle behind dividend paying stocks, one that is absolutely crucial — they pay YOU to own THEM.

Do dividend-paying stocks outperform non-dividend paying stocks over time?

The answer to this question is “it depends on your time frame.” If you compared the two during the go-go days of the tech bubble, dividend paying stocks were left in the dust. However …

In most markets, dividend paying stocks do at least as well as non-dividend paying stocks, once you add dividends back in, and in bearish or underperforming markets, dividend paying stocks can really outperform.

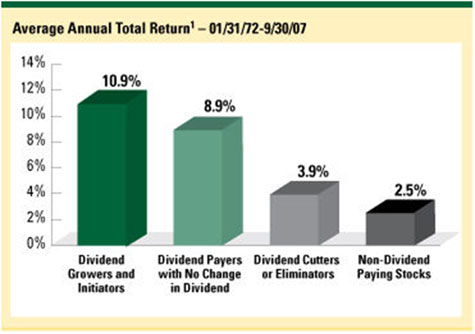

In 2008, Ned Davis Research published a chart showing just this going back to 1972. It clearly shows that stocks that are dividend payers outperform the non-payers over a longer time period.

The return differences result in dramatic differences in the absolute dollar growth of investment portfolios as well. The growth of a $100,000 portfolio invested in 1972 through September 2007 would equal:

- Non-dividend paying stocks: $240,000

- Dividend paying stocks: $3,223,000

- Dividend growers and initiators: $4,059,000

So, over a 35-year period, non-dividend paying stocks posted an average annual return of 2.5%. That’s less than T-bills. But dividend-paying stocks averaged an annual return of between 8.9% and 10.9%. That’s a huge difference.

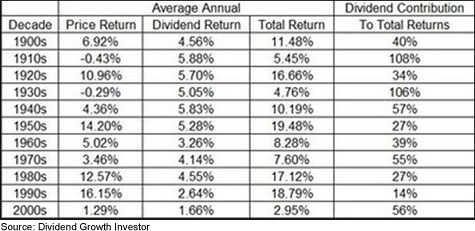

The combination of hefty dividends and share price appreciation is called “Total Return.” In the decade of the 2000’s, dividends contributed 56% of total return, according to research from Dividend Growth Investor.

I like high-yield stocks as much as the next man. But while you don’t want to put stocks with minimal yield in a dividend portfolio, you may not want to chase yields that are too high, either.

Why? Because at the very least, a stock with an elevated yield suggests that the market is discounting SOME kind of risk in the stock. A potential investor should be very sure he or she fully understands what those risks are before investing.

There are all sorts of dividend stocks of course. But you can find some really nice dividends in natural resources — royalty trusts and master limited partnerships (MLPs) can pay very nice dividends indeed.

Before you buy, here are 7 “Do’s” to consider when buying a dividend stock …

- Look for a good history of dividend growth, with the potential for dividend growth over time. After all, dividends are what this service is about. I like stocks with average annual dividend growth of 5% or more.

- When it comes to the actual dividend, we want at least 3% and preferably higher. Higher is better, as long as the dividend is safe. How do you know that? Read on …

- Find a company with strong financial performance in the past, and the potential for even better financial performance in the future.

- Look for good free cash flow. Strong free cash flow helps a company grow its dividend and its business.

- Target stocks with below-average debt. The financial leverage ratio, which is total assets divided by shareholders’ equity (book value), is a good all purpose debt measure. A leverage ratio of 1.0 means that the company has no debt, and the higher the ratio, the more debt, with leverage ratios below 5.0, and lower is better. Some industries carry more debt as part of their business models, so look for stocks with below-average debt compared to their peers.

- An advantage in the company’s business model, something that will protect them in the bad times and help them outperform in the good times.

- A good entry price. If a stock has already run up, consider entering it in stages. Because one truth of the market is that stocks go down as well as up, and we may get a better price later on. That said, you want to avoid stocks trading below $5 a share. They’re probably in trouble, and that means their dividend probably is, too.

- These are guidelines, not the clasps on a straightjacket. There will be exceptions. But it’s a good start.

Some Picks to Get You Started

Over the past couple months, I’ve been adding dividend paying stocks and funds to Red-Hot Global Small-Caps and Red-Hot Commodity ETFs. I like the added cushion that a nice dividend gives us.

One pick I’ve added to Red-Hot Global Small-Caps is MarkWest Energy Partners (MWE). It gathers and processes natural gas and other gases, as well as natural-gas liquids, from the Appalachian Basin, the Texas Panhandle, the Woodford Shale in Southern Oklahoma, The Haynesville Shale in East Texas, and the Marcellus Shale in Pennsylvania. It is one of the largest processors of natural gas in the Appalachian region and also has the largest intrastate crude oil pipeline in Michigan.

MarkWest has a current dividend yield of 8.6%, and pays $2.56. Over the past five years, its dividend has averaged 12.9% growth. MarkWest has racked up more than 10% gains since I recommended it in November, and I think it has the potential for more. Combined with an 8.6% dividend — a dividend that is also growing — this company’s potential for total return is outstanding.

Another excellent payer is pipeline and storage company Kinder Morgan Energy Partners (KMP). Its current dividend yield is 6.6%, and it pays a dividend of $1.05. Its dividend growth has averaged 7.8% over the past five years.

Dividends are an area where you may want to choose individual issues, rather than funds, because the dividends on some individual stocks, trusts and MLPs are so outstanding. There are good funds, but they don’t yield as much. For example, the PowerShares ETF High Yield (PEY), a perfectly nice fund, has a current dividend yield of just 2.4%. There are higher-yielding funds, and my Red-Hot Commodity ETFs subscribers are holding some of them.

In a market correction, the prices of the stocks and funds I’ve mentioned will probably go down, and their yields will likely go up. And that’s when you want to buy dividend stocks with both hands.

Be aware — a market correction could come at any time. And if you’re doing this on your own, you have to have a plan in place of not only when to get in, but when to get out.

Yours for trading profits,

Sean

This investment news is brought to you by Uncommon Wisdom. Uncommon Wisdom is a free daily investment newsletter from Weiss Research analysts offering the latest investing news and financial insights for the stock market, precious metals, natural resources, Asian and South American markets. From time to time, the authors of Uncommon Wisdom also cover other topics they feel can contribute to making you healthy, wealthy and wise. To view archives or subscribe, visit http://www.uncommonwisdomdaily.com.

Sean Brodrick graduated college with a journalism degree, and experienced the Internet boom and bust firsthand as the personal finance website he worked for suffered a spectacular flameout. The experience of being dumped on the curb with a handful of useless stock options gave him an appreciation for real assets, something he followed up when he joined Weiss Research as an analyst.

Sean left Weiss to become the investment director of the Sovereign Society, the world’s leading publisher of offshore asset protection strategies and global investment. There, his report, “70 Days to Empty” garnered acclaim for its analysis of the forces pushing America toward its next oil crisis, and was described by The Daily Reckoning as “the most important report you’re likely to read this year.”

Dr. Weiss lured Sean back by promising he could do anything he wanted. What Sean wanted to do was cover natural resources … especially the little-known, undervalued foreign stocks he picked as likely to ride the next wave of the commodity supercycle.

Now, Sean has a duo of services — Red-Hot Commodity ETFs and Red-Hot Global Small-Caps. He also contributes weekly to Uncommon Wisdom. His report, “The Golden Age of Uranium,” has gathered accolades from investors and industry insiders alike.

He is a weekly guest on Market Matters Radio, a frequent commentator on one of Canada’s premiere financial websites, HoweStreet.com, and from time to time he makes appearances on various U.S. radio and TV news programs. He contributes semi-regularly to Dow Jones Marketwatch.

Be sure to catch Tyler Bollhorn’s presentation at the World Outlook Conference this January 22, 23rd/2010

Do These Sound Familiar?

Stockscores.com Perspectives for the week ending January 17, 2010

![]()

Stockscores Founder Tyler Bollhorn will be a featured speaker at the 2010 World Outlook Conference in Vancouver Jan 22 and 23. This is a great conference and this year, Tyler will be demonstrating the new Money Talks/Disnat Trading Challenge game.

Those interested in attending this conference should Click Here to visit the World Outlook website for more information and to register.

As a trader, I have done a lot of stupid things to lose money. My only saving grace is that I have learned something from the mistakes and so now, when I see others doing the same things, I can say, “Hey, you are making a stupid mistake!” Here is a list of the stupid things that most of us do as we work our way through the learning process it takes to be a successful stock trader.

Fail to Limit Losses – I have not yet met someone who is always right in the stock market. That means you and I are going to be wrong some of the time. What is important is what we do when we are wrong. When the stock market shows that your analysis was incorrect, sell! Move on, get out, forget about it. Small losses won’t hurt you, using hope to justify holding a loser will.

Averaging Down – averaging down on a loser is buying more at a lower price, expecting the inevitable bounce that gets you out without a loss. This strategy will actually work a lot of the time, you just keep averaging down until the market reverses. However, when it fails to work, and you keep buying in to a stock’s bungee jump that fails to bounce, you can lose everything. Without capital preservation, you are just a spectator.

Get the $3,600 StockSchool Pro Free by just opening an account at:

- DisnatDirect named the number one Canadian brokerage for Traders by Surviscor! Open and Fund a brokerage account with DisnatDirect and receive the StockSchool Pro home study course free, including special Pro level access through the DisnatDirect client website. Offer only available to Canadian residents. For information, click here

Buying in to Emotion – it is tempting to buy more of a stock that is moving quickly higher. It is important to remember that when everyone is doing this, investors will inevitably pay too much. A simple rule is to not buy stocks that have run away from their trend line. You can buy stocks that have momentum, just wait for them to pull back to the trend line and buy them on short term weakness. Never chase.

Believing in Public Information – the stock market is efficient, it prices in all available information. That means the news release that you are reading has no value. The annual report has no value. So long as the general public has the same information as you, your decisions based on that information will provide random results.

Selling on Pull Backs – it is easy to be nervous with our winners because the feeling of having a winner turn in to a loser is not a nice one. So, we tend to sell our winners too early, getting out at the first sign of weakness to lock in the profit and give ourselves the congratulatory “you never go broke making a profit” speech. You have to maximize gains and learn to distinguish between the minor pull backs that are part of long term, money making trends and actual trend reversals. A trade is not successful until you have doubled your risk.

Taking Too Much Risk – emotion is the enemy of the trader. Cold hearted people, or at least those who do not care about the risk of the trade, are the best traders. To make sound decisions, you can not risk more on a trade than you are willing to lose. If you do, you will break your trading discipline and avoid selling losers when you are wrong or sell your winners too early.

Going Against the Mood of the Market – it is not easy to paddle a canoe up a river, against the current. It is also not easy making money on a stock when the mood of the market is against you. When considering a stock, I always first assess who is in control of the stock, buyers or sellers. To make money, you either have to trade with the group that is in control or pick the point where control changes from one group to another. Don’t go against the mood of the market.

Trade Possibility, not Probability – I remember an advertisement for a lottery, it said, “Think of the Possibilities!.” What if the lottery company suggested we think of the probabilities? We have all heard that we have a better chance of getting struck by lightening than picking the right numbers to win the lottery, but because we think of the possibilities, we continue to buy tickets. A lot of people approach the market the same way. They may look at a stock and describe all of the thing that could happen, how the company could find gold on a long shot mining exploration and how the stock could go rocketing higher. However, when you trade against probability, you are on the path to poverty.

![]()

The Canadian speculative stock markets have been the best performers in the past few months and continue to bring a lot of good trading opportunities. It is very important to not fall in love with the companies in this area because they often fizzle out quickly, but so long as you listen to the market for exit signals, you can do well trading them.

This week, I scanned the Canadian market for low priced stocks trading abnormal volume and with abnormal price action. I then inspected their charts for good pattern set ups.

![]()

1. V.SSE

V.SSE is breaking out from an ascending triangle pattern that has been building for six months and broke to the upside with very abnormal volume on Friday. There will be some selling pressure at the $0.15 price range but the volume was so abnormal on the break that I think it will have the power to move through resistance. Support at $0.065.

2. T.WES

T.WES has been building optimism over the past few months and Friday broke through resistance. Support at $2.50.

Click HERE for the Speaker Lineup at the World Outlook Financial Conferance and click HERE if you want to learn from some of the timeless advice from some of worlds best traders including the very successful Tyler Bollhorn.

![]()

Tyler Bollhorn started trading the stock market with $3,000 in capital, some borrowed from his credit card, when he was just 19 years old. As he worked through the Business program at the University of Calgary, he constantly followed the market and traded stocks. Upon graduation, he could not shake his addiction to the market, and so he continued to trade and study the market by day, while working as a DJ at night. From his 600 square foot basement suite that he shared with his brother, Mr. Bollhorn pursued his dream of making his living buying and selling stocks.

Slowly, he began to learn how the market works, and more importantly, how to consistently make money from it. He realized that the stock market is not fair, and that a small group of people make most of the money while the general public suffers. Eventually, he found some of the key ingredients to success, and turned $30,000 in to half a million dollars in only 3 months. His career as a stock trader had finally flourished.

Much of Mr Bollhorn’s work was pioneering, so he had to create his own tools to identify opportunities. With a vision of making the research process simpler and more effective, he created the Stockscores Approach to trading, and partnered with Stockgroup in the creation of the Stockscores.com web site. He found that he enjoyed teaching others how the market works almost as much as trading it, and he has since taught hundreds of traders how to apply the Stockscores Approach to the market.

References

Get the Stockscore on any of over 20,000 North American stocks.

Background on the theories used by Stockscores.

Strategies that can help you find new opportunities.

Scan the market using extensive filter criteria.

Build a portfolio of stocks and view a slide show of their charts.

See which sectors are leading the market, and their components.

Disclaimer

This is not an investment advisory, and should not be used to make investment decisions. Information in Stockscores Perspectives is often opinionated and should be considered for information purposes only. No stock exchange anywhere has approved or disapproved of the information contained herein. There is no express or implied solicitation to buy or sell securities. The writers and editors of Perspectives may have positions in the stocks discussed above and may trade in the stocks mentioned. Don’t consider buying or selling any stock without conducting your own due diligence.

John Mauldin Speaks: This week I am really delighted to be able to give you a condensed version of Gary Shilling’s latest INSIGHT newsletter for your Outside the Box. Each month I really look forward to getting Gary’s latest thoughts on the economy and investing. Last year in his forecast issue he suggested 13 investment ideas, all of which were profitable by the end of the year.

It is not unusual for Gary to give us over 75 charts and tables in his monthly letters along with his commentary, which makes his thinking unusually clear and accessible. Gary was among the first to point out the problems with the subprime market and predict the housing and credit crises. His track record in this decade has been quite good. I want to thank Gary and his associate Fred Rossi for allowing us to view this smaller version of his latest letter.

If you are interested in his letter, his web site is down being re-designed, but you can write for more information at insight@agaryshilling.com. If you want to subscribe (for $275), you can call 888-346-7444. Tell them that you read about it in Outside the Box and you will get the full 2010 forecast with price targets, but an extra issue with his 2011 forecast (of course, that one will not come out until the end of the year. Gary is good but not that good!) I trust you are enjoying your week. And enjoy this week’s Outside the Box….

John Mauldin, Editor

Outside the Box

2010 Investment Strategies: Six Areas To Buy, 11 Areas To Sell

(excerpted from the January 2010 edition of A. Gary Shilling’s INSIGHT)

Our investment strategies for 2010 follow from our forecast of continued economic weakness and deflation, as discussed earlier in this report and in previous Insights, especially our Dec. 2009 edition. We see the 2010 investment climate dominated by weak economic growth here and abroad, led by U.S. consumer retrenchment. More government fiscal stimulus and continuing Fed policy ease are likely in this setting. So is low inflation or deflation.

INVESTMENTS TO BUY

1. Buy Treasury Bonds. Long-term Insight readers know we started recommending long Treasury bonds back in 1981 when we forecast secular and huge declines in inflation and interest rates. So we declared back then that “we’re entering the bond rally of a lifetime.” The yield on 30-year Treasurys was 14.7% and our eventual target was 3%. Last year, yields blew through 3% to reach 2.6% at year’s end, so in our Jan. 2009 Insight we declared “mission accomplished” and removed Treasury bonds from our recommended list.

But then Treasurys sold off, pushing the yield on the 30-year bond to 4.7% at the end of 2009. So we’ve reactivated the strategy with our forecast of a return in yields to 3.0% or lower. Treasurys will continue to be a safe haven in a troubled world and benefit from deflation as well as their three sterling features. They are the best credits in the world. They are highly liquid. And they generally can’t be called by the Treasury, and calls limit price appreciation when interest rates fall.

A decline in yields from 4.7% at present to 3.0% may not sound like much, but the bond price would appreciate over 34%. If it occurs over two years, then two years’ worth of interest is collected, and the total return on the 30-year Treasury would be 44%. On a 30-year zero-coupon Treasury, which pays no interest but is issued at a discount, the total return would be about 64% — most attractive! Recall that in 2008 when 30-year Treasurys rallied from 4.5% to 2.7%, their total return for the year was 42%..

Treasury bonds way outperformed equities in the 1980s and 1990s in what was the longest and strongest stock bull market on record. The superiority of Treasurys has been even more so since then. Chart 1, our all-time favorite graph, shows the results from investing $100 in a 25-year zero-coupon Treasury bond at its yield high (and price low) in October 1981, and rolling it into another 25-year Treasury annually to maintain that 25year maturity. In November 2009, that $100 was worth $16,972 with a compound annual return of 20.1%. In contrast, $100 invested in the S&P 500 at its low in July 1982 was worth $2,099 in November for an 11.8% annual return including dividend reinvestment. So Treasurys outperformed stocks by 8.1 times!

….read more HERE (scroll down to the first chart and continue)

Update Sunday morning 01/17/10

My bags are packed and my bear suit is pressed but I have yet to leave the key on the counter at the “Don’t Worry” Be Happy” Hotel. Some may ask with almost two feet out the door, why not just hit the check out button on the TV and return back to where I belong?

In a business where many times you’re only as good as your last call, it’s going to be extremely difficult to surpass or match my last two market calls. My biggest sell recommendation ever came just two days after the all-time high in DJIA and my go long buy came just one day before the bottom last March. So unless I timed the ultimate top within hours, someone will surely say I’m slipping-Lol!

I promise this blog will be the first to note when I tell the desk “sayonara”.

The correction/consolidation in gold is nearing an end and while we can’t rule out one more dip below $1,100, I continue to believe the surprises in the gold market remain almost exclusively to the upside.

Given the fact that people are literally knocking themselves over in declaring their new-found love for the U.S. Dollar, the U.S. Dollar Index has seen barely a blip up. Bullish sentiment has gone from the low single digits to the majority yet the dollar has barely budge, net-net. While there’s still a window of opportunity for a decent bear market rally, time is not on the dollar bull’s side.

I continue to like going short 10-30yr. Treasuries here and on any further rallies.

I remain dead neutral on oil and gas.

- Northern Dynasty Minerals presentation in NYC last week

- Taseko Mines – What can I say? I sung for the fences on this one last year and the news this past week has led this to being a homerun. A teleconference is available this Tuesday. I remain a strong holder and believe a double digit share price in the next 12-24 months is not a “pipe dream.”

- Continental Minerals – I was forwarded this commentary on KMK and thought some would find it worthy.

- Nevsun Resources – Barring further sanctions and/or a significant decline in gold and copper prices, I don’t see much more downside risk in NSU. I do think however, a cheap takeover bid now around $4 could steal the company that otherwise couldn’t have happened before the U.N. sanctions. This is very high risk and only speculators/gamblers fully prepared to lose a significant part of their investment should be in this situation now.

- Evolving Gold – While my comments on BNN Friday are sufficient, I hope to make a further comment on EVG early in the week. Here’s a commentary from EVG after the news release.

Finally, a commentary on Donner Metals

On Major Moves, Grandich has been very right and not only saved many investors fortunes, but expanded them dramatically. On November 3, 2007 at the MoneyTalks Survival Conference, Peter Grandich of the Grandich Letter warned that “an unprecedented economic tsunami will hit American beginning in 2008”. Peter advised publicly to short the US market two days from the top in October, 2007 and stayed short until the last week of October, 2008. He began to buy stocks in March 7th, 2009. He also bought oil and oil related investments near the lows after the dive from $147.

….go to visit Peter’s Website.

Peter Grandich, chief market commentator, Agoracom.com, shares his top picks.

BNN takes your calls and emails on North American resource stocks with Peter Grandich, chief market commentator, Agoracom.com.

On Major Moves, Grandich has been very right and not only saved many investors fortunes, but expanded them dramatically. On November 3, 2007 at the MoneyTalks Survival Conference, Peter Grandich of the Grandich Letter warned that “an unprecedented economic tsunami will hit American beginning in 2008”. Peter advised publicly to short the US market two days from the top in October, 2007 and stayed short until the last week of October, 2008. He began to buy stocks in March 7th, 2009. He also bought oil and oil related investments near the lows after the dive from $147.

….go to visit Peter’s Website.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair