Daily Updates

Peter Grandich on Money Markets and Life 03/26/10

Topics:

- Dow comes within a whisker of 11,000, then retreats …. did we just see a classic reversal?

- Gold is looking as as strong as ever despite climbing $USD

- US Real Estate continues to crumble. How does this affect US Gov’t spending, bonds and interest rates?

- Questions from our great members

- Without further ado, here is this week’s show – Click HERE

Special offer from Mark Leibovit for Money Talks only: The intense analysis of Gold in the 10-12 page The VR Gold Letter is right now 75% off for the first month or $29.95 (regularly $125.00 a month). The weekly VR Gold Letter focuses on Gold and Gold shares.Go HERE and use the Money Talks promo code CBC12210

Market Monitor – The Nightly Business Report

TOM HUDSON Well, the stock market rally has room to run, even as it sits close to 18-month highs tonight, at least so says tonight’s “Market Monitor” guest. He’s Mark Leibovit, chief market strategist at vrtrader.com, and he joins us tonight from Phoenix. Mark, welcome back to NIGHTLY BUSINESS REPORT.

MARK LEIBOVIT, CHIEF MARKET STRATEGIST, VRTRADER.COM: Thanks for having me. Nice to meet you, Tom, on the air.

HUDSON: Nice to meet you as well. So more room to run. How much more room to run as we’re at these 18- month highs?

LEIBOVIT: Well, you know, the trend is your friend, as they say, and until we get a clear reversal pattern, and my technique using volume reversal in theory volume preceding price, until we get that volume reversal and we get an indication of important selling in the market, you let the market work for you. We have targets that still say this market could go higher, but you know, the bottom line is, you know, the trend is your friend and, you know, we’re just past that halfway retracement point that I mentioned in our previous interview, which was 10,005. So as you go through a half-way retracement, then you start saying, well, are we going to do a 6-1-8 retracement or a full retracement of decline, which would get you all the way back up to that 14,000 area. I don’t know if we can get there or not. I’m not thinking that. But we’re going to stay with it and we’re going to look at some other indicators here to guide us.

HUDSON: Yes. Well, Mark, let’s put some numbers to these ideas. And you brought along with you a model forecast for the Dow Industrials, for instance. And what you see here is this is basically your forecast for 2010 for the Dow, with the actual performance down below. And you see the dog days of summer being some tough months for long investors and the Dow ending the year near the lows of the year.

LEIBOVIT: Right. this is a cyclical forecast. So what we do with the annual forecast is we’re combining that with our volume work. So it’s like the proverbial weatherman looking out the window. You know, you wait for your short-term signals. You don’t stick with your big forecast until you get confirmation that, indeed, it’s happening. But yes, according to this model, we should run out of steam here some time this summer and have a pretty sharp correction. But how high are we going to be when we hit that top? Could it be 12,000, 14,000? You don’t know. So we will have to wait for that point. Could be quite high.

HUDSON: OK. So the velocity of the move higher, you’re unsure about, but the timing you think August looks like that could be the high for the Dow?

LEIBOVIT: That does appear to be the case at the moment, yes.

HUDSON: OK. Let’s take a look at the chart pattern on the S&P 500, the broad market here. And you’ve got what the technicians and yourself call a reverse head and shoulders pattern. You see the neck line, Mark, right there. Your projected target of 1,230, that brings us, what, about 5.5 percent by where we’re looking at to the close of the week this week?

LEIBOVIT: Right. Now remember, this measurement was made months and months ago, and I think in my September interview, we showed the Dow forecast, which was showing 11,500, which is the equivalent to S&P 1,230. So this is an existing forecast for months, and we haven’t got to that target yet of 1,230. We could go much higher. This just gives you an indication of where, I guess, a minimum expectation would be. So this would be about 1,105 in the Dow, 1,103 in the Dow, and if that occurs by August, that will be it. I suspect it will be higher, but we’ll see.

HUDSON: All right. Let’s take a look at some of the picks that you brought along with you in September and get a quick comment about the dollar, especially when it comes to the Central Fund of Canada (CEF) and the Silver (SLV) exchange-traded fund. Each of these certainly very commodities-based and precious metals-based. Do you still like these and is this a play on the U.S. dollar?

LEIBOVIT: Well, the dollar is still in an uptrend, which could be a problem for the precious metals, but according to the cyclical forecast, we’re due for a little correction here this summer, which could drive these metals higher. I’m hoping at a point we’re going to see the dollars and precious metals actually diverge and won’t track inversely as they have been.

But for now we’re going to stick with these players because I think there could be another run here in the precious metals in the next couple of months. And then after that, we may go into a correction as well. But how do you know gold won’t be 1,300, 1,400 this summer and then correct from a higher level? So let’s let the time work for us here a little bit and that’s what the dollar is saying, we’re going to pull back here in the dollar, and then a run later in the year.

HUDSON: Mark, just 15 seconds left, but I want to show the previous picks, the last two, PAL, North American Palladium (PAL), and Vanguard Total Stock Market (VTI) ETF. Each of these nice gains. Do you still like them? Put new money to work?

LEIBOVIT: Yes, I would hold PAL, I would hold V-T-I, I would hold C- E-F, these are all solid plays at least through the summer.

HUDSON: OK. Fair enough. They we go. Our Market Monitor guest this evening, Mark Leibovit, chief market strategist at vrtrader.com.

The weekly VR Gold Letter focuses on Gold and Gold shares. The letter is available to Platinum subscribers for only an additional $50 per month and to Silver subscribers for only $70 per month. Email me at mark.vrtrader@gmail.com.

Special offer from Mark Leibovit for Money Talks only: The intense analysis of Gold in the 10-12 page The VR Gold Letter is right now 75% off for the first month or $29.95 (regularly $125.00 a month). Go HERE and use the Money Talks promo code CBC12210

Marks VRTrader Silver Newletter covers Stock, TSE Stocks, Bonds, Gold, Base Metals, Uranium, Oil and the US Dollar.

More kudos – Mark Leibovit was named the #1 Intermediate Market Timer for the 10 year period ending in 2007; the #1 Intermediate Market Timer for the 3 year period ending in 2007; the #1 Intermediate Market Timer for the 8 year period ending in 2007; and the #8 Intermediate Market Timer for the 5 year period ending in 2007. NO OTHER ANALYST SURVEYED APPEARED IN ALL FOUR CATEGORIES FOR INTERMEDIATE MARKET TIMING AS PUBLISHED IN TIMER DIGEST JANUARY 28, 2008!

For a trial Subscription of The VR Silver Newsletter covering Stocks, Bonds, Gold, US Dollar, Oil CLICK HERE

The VR Gold Letter is available to Platinum subscribers for only an additional $20 per month, while for Silver subscribers the price is only an additional $70.00 per month. Prices are going up very shortl, so act now! Separately, the VR Gold Letter retails for $1500 a year! The VR Gold Letter is published WEEKLY. It is 10 to 16 pages jam-packed with commentary and charts. Please call or email us right away. Tel: 928-282-1275. Email: mark.vrtrader@gmail.com .

SP500 & Dow Intraday Charts & Futures Prices at Their Best

March 26, 2010

The market gapped higher this morning after yesterdays heavy selling. At this time the market (metals and indexes) are trading at resistance on light volume. This tells me people are a little spooked from yesterday and just do not want to buy at these lofty prices.

Stock Market Training Education

I am trying to provide you with more insight and trading tips/education because I know many of you enjoy it. So here is something some of you may find interesting…

Over the years I have found several things which happen repeatedly in the market. I always found it interesting that in an uptrend the market/commodity or stock tends to gap lower at the open the next day. And during a down trend the market tends to gap higher at the open.

Why is this? I don’t know for sure… but my thoughts are that the smart money (big guys & professional traders) manipulate the market using futures to artificially lower prices so they can buy more the at lower prices before everyone else jumps in. It’s similar but in the reverse during a bear market. Prices gap up so they can short more shares at a higher price before everyone starts selling again pushing prices lower.

I could be way off here as this is my personal opinion but I see it happen all the time… so whether I am right or wrong in my theory the fact is this price action happens.

Take a look at the SP500 & Dow Jones Futures Charts:

Market Gap Trading Conclusion:

In short, the market gapped up today (not good)…

I see the dollar is now trading at a short term support level and metals are trading at resistance. So maybe something will come out of this for a short play…

I hope this short reports was of use for getting a feel of how the market moves and what I am looking for in low risk setups.

Have a great weekend everyone. I don’t see anything tradable other than this intraday low risk setup which just broke down as I write this sentence, fun stuff…

Sign up for this FREE Newsletter HERE (scroll down and the location to subscribe is on the right hand side)

Be sure to get notified about my new day and swing trading service I am launching April 6th by entering your email address in the form “Subscribe” at the bottom of this Page HERE

Ed Note: The Letter (scroll down)to his Children is wonderful, and really nails the crisis’s impact on us all. The Title below is What Does Greece Mean to Me, Dad?

In this issue:

What Does Greece Mean to Me, Dad?

Dear Kids,

Ubiquity, Complexity Theory, and Sandpiles

Fingers of Instability

Washington DC, Albuquerque, and Guy Forsythe

“To trace something unknown back to something known is alleviating, soothing, gratifying and gives moreover a feeling of power. Danger, disquiet, anxiety attend the unknown – the first instinct is to eliminate these distressing states. First principle: any explanation is better than none… The cause-creating drive is thus conditioned and excited by the feeling of fear…” Friedrich Nietzsche

“Any explanation is better than none.” And the simpler, it seems in the investment game, the better. “The markets went up because oil went down,” we are told, except when it went up there was another reason for the movement of the markets. We all intuitively know that things are far more complicated than that. But as Nietzsche noted, dealing with the unknown can be disturbing, so we look for the simple explanation.

“Ah,” we tell ourselves, “I know why that happened.” With an explanation firmly in hand, we now feel we know something. And the behavioral psychologists note that this state actually releases chemicals in our brains that make us feel good. We become literally addicted to the simple explanation. The fact that what we “know” (the explanation for the unknowable) is irrelevant or even wrong is not important to the chemical release. And thus we look for reasons.

How does an event like a problem in Greece (or elsewhere) affect you, gentle reader? And I mean, affect you down where the rubber hits your road. Not some formula or theory about the velocity of money or the effect of taxes on GDP. That is the question I was posed this week. “I want to understand why you think this is so important,” said a friend of Tiffani. So that is what I will attempt to answer in this week’s missive, as I write a letter to my kids trying to explain the nearly inexplicable.

But first, let me note to Conversations subscribers that we have posted a Conversation I recently did with Professors Ken Rogoff and Carmen Reinhart, authors of This Time It’s Different, which has my vote for most important book of the last few years.

Last week we also posted a Conversation with two noted hedge-fund managers, Kyle Bass of Hayman Advisors (and his staff) here in Dallas and Hugh Hendry of the Eclectica Fund in London. Our discussion centered on what we all think has the potential to be the next Greece, but on a far more serious level.

That got a lot of positive response. Herb wrote, “Wow. What a great discussion. What smart guests, how little BS. Congratulations. It’s the best of your Conversations that I’ve listened to.”

And ACK wrote: “Wow!! Just the most important discussion I have been treated to as an investor and fund manager this year or last. Your product is dreadfully underpriced, as it delivers more value and education than almost any other subscription that I have… Thanks so much… This particular conversation was just mind-blowing!”

Actually, we get that last comment almost every issue, as we somehow seem to connect the dots for different listeners. When we started, I promised to do 6-8 a year, and we have already posted 5 timely Conversations in the first 3 months of this year, including my special Biotech Series as well as the Geopolitical Series with George Friedman.

For new readers, Conversations with John Mauldin is my one subscription service. While this letter will always be free, we have created a way for you to “listen in” on my conversations (or read the transcripts) with some of my friends, many of whom you will recognize and some whom you will want to know after you hear our conversations. Basically, I call one or two friends each month and, just as we do at dinner or at meetings, we talk about the issues of the day, back and forth, with give and take and friendly debate. I think you will find it enlightening and thought-provoking and a real contribution to your education as an investor.

And as you can see, I can get some rather interesting people to come to the table. Current subscribers can renew for a deeply discounted $129, and we will extend that price to new subscribers as well. To learn more, go to http://www.johnmauldin.com/newsletters2.html. Click on the Subscribe button, and join me and my friends for some very interesting Conversations. (I know the price says $199 on the site, but for now you will only be charged for $129 – I promise.)

And we are starting a renewal cycle with the subscriptions and have found a small bug in the software we purchased to handle them. Renewals are therefore not instantaneous. It may take a day, and for that we apologize. We are fixing it.

Oh, and by the way, since the Conversation on Japan was so well-received, the next one will be on China. Two brilliant managers (maybe three) with VERY divergent views. I may just toss in a few grenade-type questions and stand back and watch the show. And now on to this week’s letter.

What Does Greece Mean to Me, Dad?

Tiffani had been talking with her friends. A lot of them read this letter, and they were asking, “Ok, I get that Greece is a problem. But what does that mean for me here?”

The same day, a friend told me about a conversation she had with her 17-year-old Cal Tech daughter and her daughter’s boyfriend, who is also headed to Cal Tech. These are really smart kids, and they were asking her about some of my recent letters. “We understand what’s he saying, but we just don’t see what it means.” (For what it’s worth, the boyfriend wants to grow up to be Mohammed El-Erian of PIMCO. Go figure; I just wanted to be Mickey Mantle.)

Twice in one day is a sign, I am sure, so I will try and see if I can explain. And since all my kids must be wondering the same thing, this is kind of letter from Dad to see if I can help them understand why things are not going as well as they would like.

(A little background. I have seven kids, five of whom are adopted. A fairly colorful family, so to speak. Pictures at the end of the letter. Ages almost 16 through 33. Daughter Tiffani runs my business and, except for the youngest boy, they are all out on their own. Four are married or attached. It is not easy to watch them struggle to make ends meet, but Dad is proud. But listening to their stories, and the stories of their friends, help keep me in the real world.)

Dear Kids,

I know what a struggle it has been for most of you, and now three of you have a kid of your own. Expensive little hobbies, aren’t they? I know that you read my letter (well, except for Trey) and wonder what it means to you trying to pay your bills. Let me see if I can make a connection from the world of economics to the world of paying your bills. Sadly, what I am going to say is not going to make you feel any better, but reality is what it is. We’ll get through it together.

While life looks pretty good for Dad now, when I graduated from seminary in December of 1974 unemployment was at 8%, on its way to 9% a few months later. We lived in a small mobile home, which seemed wonderful at the time. I was proud of it. We scrimped and got by. My first job was a dead end, so I left after a few months. I guess I was lucky that no one would hire me, because I had to figure out how to make it on my own. All I really knew was the printing business I had grown up in, so I started brokering printing. Pretty soon I was doing just direct mail, and then designing direct mail. But there was never enough money. We were still in that mobile home six years later.

And prices were going up like crazy. We had inflation. I remember going to a bank in the late ’70s and borrowing money for my business at 18%, so I could buy paper for a job I had sold. Forget about borrowing for a new home or car. All I knew was that I was struggling to make ends meet (with a new kid!). There were a lot of nights where I would wake up at two in the morning with panic attacks about whether I could make payroll or pay bills until someone paid me. I didn’t understand that what the Fed and the government were doing was causing high inflation and unemployment.

I had a bank line I used to buy paper with. One day the bank abruptly cancelled that line and demanded their money, which I didn’t have – all I had was a warehouse full of paper and a contract that said I had a year to pay for it. The bank didn’t care. I told them they would just have to wait. I swear, they actually called my mother and told her they would ruin me if she didn’t pay that $10,000 line. She was scared for me (after all, you had to be able to trust your banker) and paid it without asking me. Turned out the bank finally went bankrupt later in the year. They were just desperate and trying anything they could do to get money, so they wouldn’t lose everything. They did anyway.

In short, times were not all that good, but we got through it. And now, 35 years later, it seems like déjà vu all over again. Every time we talk it seems like someone we know has lost a job.

And so how do the problems in a small country like Greece make a difference to you? There is a connection, but it’s different than the old “hip bone is connected to the thigh bone to the knee bone” thing. It is a lot more complicated. Let’s go back to a letter I wrote four years ago, talking about fingers of instability. One of the best analogies your Dad has ever written, according to many of his 1 million friends. So read with me a few pages, and then we’ll get back to Greece.

Ubiquity, Complexity Theory, and Sandpiles

We are going to start our explorations with excerpts from a very important book by Mark Buchanan called Ubiquity, Why Catastrophes Happen. I HIGHLY recommend it to those of you who, like me, are trying to understand the complexity of the markets. Not directly about investing, although he touches on it, it is about chaos theory, complexity theory, and critical states. It is written in a manner any layman can understand. There are no equations, just easy-to-grasp, well-written stories and analogies. www.Amazon.com

We all had the fun as kids of going to the beach and playing in the sand. Remember taking your plastic buckets and making sandpiles? Slowly pouring the sand into ever-bigger piles, until one side of the pile started an avalanche?

Imagine, Buchanan says, dropping just one grain of sand after another onto a table. A pile soon develops. Eventually, just one grain starts an avalanche. Most of the time it is a small one, but sometimes it gains momentum and it seems like one whole side of the pile slides down to the bottom.

Well, in 1987 three physicists, named Per Bak, Chao Tang, and Kurt Weisenfeld, began to play the sandpile game in their lab at Brookhaven National Laboratory in New York. Now, actually piling up one grain of sand at a time is a slow process, so they wrote a computer program to do it. Not as much fun, but a whole lot faster. Not that they really cared about sandpiles. They were more interested in what are called nonequilibrium systems.

They learned some interesting things. What is the typical size of an avalanche? After a huge number of tests with millions of grains of sand, they found out that there is no typical number. “Some involved a single grain; others, ten, a hundred or a thousand. Still others were pile-wide cataclysms involving millions that brought nearly the whole mountain down. At any time, literally anything, it seemed, might be just about to occur.”

It was indeed completely chaotic in its unpredictability. Now, let’s read these next paragraphs slowly. They are important, as they create a mental image that helps me understand the organization of the financial markets and the world economy.

“To find out why [such unpredictability] should show up in their sandpile game, Bak and colleagues next played a trick with their computer. Imagine peering down on the pile from above, and coloring it in according to its steepness. Where it is relatively flat and stable, color it green; where steep and, in avalanche terms, ‘ready to go,’ color it red.

“What do you see? They found that at the outset the pile looked mostly green, but that, as the pile grew, the green became infiltrated with ever more red. With more grains, the scattering of red danger spots grew until a dense skeleton of instability ran through the pile. Here then was a clue to its peculiar behavior: a grain falling on a red spot can, by domino-like action, cause sliding at other nearby red spots. If the red network was sparse, and all trouble spots were well isolated one from the other, then a single grain could have only limited repercussions.

“But when the red spots come to riddle the pile, the consequences of the next grain become fiendishly unpredictable. It might trigger only a few tumblings, or it might instead set off a cataclysmic chain reaction involving millions. The sandpile seemed to have configured itself into a hypersensitive and peculiarly unstable condition in which the next falling grain could trigger a response of any size whatsoever.”

Something only a math nerd could love? Scientists refer to this as a critical state. The term critical state can mean the point at which water would go to ice or steam, or the moment that critical mass induces a nuclear reaction, etc. It is the point at which something triggers a change in the basic nature or character of the object or group. Thus, (and very casually for all you physicists) we refer to something being in a critical state (or use the term critical mass) when there is the opportunity for significant change.

“But to physicists, [the critical state] has always been seen as a kind of theoretical freak and sideshow, a devilishly unstable and unusual condition that arises only under the most exceptional circumstances [in highly controlled experiments]… In the sandpile game, however, a critical state seemed to arise naturally through the mindless sprinkling of grains.”

Then they asked themselves, could this phenomenon show up elsewhere? In the earth’s crust, triggering earthquakes; in wholesale changes in an ecosystem or a stock market crash? “Could the special organization of the critical state explain why the world at large seems so susceptible to unpredictable upheavals?” Could it help us understand not just earthquakes, but why cartoons in a third-rate paper in Denmark could cause worldwide riots?

Buchanan concludes in his opening chapter, “There are many subtleties and twists in the story … but the basic message, roughly speaking, is simple: The peculiar and exceptionally unstable organization of the critical state does indeed seem to be ubiquitous in our world. Researchers in the past few years have found its mathematical fingerprints in the workings of all the upheavals I’ve mentioned so far [earthquakes, eco-disasters, market crashes], as well as in the spreading of epidemics, the flaring of traffic jams, the patterns by which instructions trickle down from managers to workers in the office, and in many other things.

“At the heart of our story, then, lies the discovery that networks of things of all kinds – atoms, molecules, species, people, and even ideas – have a marked tendency to organize themselves along similar lines. On the basis of this insight, scientists are finally beginning to fathom what lies behind tumultuous events of all sorts, and to see patterns at work where they have never seen them before.”

Now, let’s think about this for a moment. Going back to the sandpile game, you find that as you double the number of grains of sand involved in an avalanche, the likelihood of an avalanche is 2.14 times as unlikely. We find something similar in earthquakes. In terms of energy, the data indicate that earthquakes simply become four times less likely each time you double the energy they release. Mathematicians refer to this as a “power law,” or a special mathematical pattern that stands out in contrast to the overall complexity of the earthquake process.

Fingers of Instability

So what happens in our game? “… after the pile evolves into a critical state, many grains rest just on the verge of tumbling, and these grains link up into ‘fingers of instability’ of all possible lengths. While many are short, others slice through the pile from one end to the other. So the chain reaction triggered by a single grain might lead to an avalanche of any size whatsoever, depending on whether that grain fell on a short, intermediate or long finger of instability.”

Now, we come to a critical point in our discussion of the critical state. Again, read this with the markets in mind:

“In this simplified setting of the sandpile, the power law also points to something else: the surprising conclusion that even the greatest of events have no special or exceptional causes. After all, every avalanche large or small starts out the same way, when a single grain falls and makes the pile just slightly too steep at one point. What makes one avalanche much larger than another has nothing to do with its original cause, and nothing to do with some special situation in the pile just before it starts. Rather, it has to do with the perpetually unstable organization of the critical state, which makes it always possible for the next grain to trigger an avalanche of any size.”

Now let’s couple this idea with a few other concepts. First, one of the world’s greatest economists (who sadly was never honored with a Nobel), Hyman Minsky, points out that stability leads to instability. The longer a given condition or trend persists (and the more comfortable we get with it), the more dramatic the correction will be when the trend fails. The problem with long-term macroeconomic stability is that it tends to produce highly unstable financial arrangements. If we believe that tomorrow and next year will be the same as last week and last year, we are more willing to add debt or postpone savings for current consumption. Thus, says Minsky, the longer the period of stability, the higher the potential risk for even greater instability when market participants must change their behavior.

Relating this to our sandpile, the longer that a critical state builds up in an economy or, in other words, the more fingers of instability that are allowed to develop connections to other fingers of instability, the greater the potential for a serious “avalanche.”

And that’s exactly what happened in the recent credit crisis. Consumers all through the world’s largest economies borrowed money for all sorts of things, because times were good. Home prices would always go up and the stock market was back to its old trick of making 15% a year. And borrowing money was relatively cheap. You could get 2% short-term loans on homes, which seemingly rose in value 15% a year, so why not buy now and sell a few years down the road?

Greed took over. Those risky loans were sold to investors by the tens and hundreds of billions all over the world. And as with all debt sandpiles, the fault lines started to show up. Maybe it was that one loan in Las Vegas that was the critical piece of sand; we don’t know, but the avalanche was triggered.

You probably don’t remember this, but Dad was writing about the problems with subprime debt way back in 2005 and 2006. But as the problem actually emerged, respected people like Ben Bernanke (the chairman of the Fed) said that the problem was not all that big, and that the fallout would be “contained.” (I bet he wishes he could have that statement back!)

But it wasn’t contained. It caused banks to realize that what they thought was AAA credit was actually a total loss. And as banks looked at what was on their books, they wondered about their fellow banks. How bad were they? Who knew? Since no one did, they stopped lending to each other. Credit simply froze. They stopped taking each other’s letters of credit, and that hurt world trade. Because banks were losing money, they stopped lending to smaller businesses. Commercial paper dried up. All those “safe” off-balance-sheet funds that banks created were now folding. Everyone sold what they could, not what they wanted to, to cover their debts. It was a true panic. Businesses started laying off people, who in turn stopped spending as much.

As you saw from my earlier story about my bank experience, banks may do what unreasonable things when they get into trouble. (Speaking of which, my smallish Texas bank, where I have been for almost 20 years, just cancelled my very modest, unused credit line last month, and told me that letters of credit will not be rewritten without 100% cash against them. Not to worry, Dad is actually in the best shape of his life, business-wise, knock on wood. I hadn’t talked personally to a banker in years. When I asked the young clerk on the phone, “What’s going on?” he said it was just an order from his director. I switched banks last week, as I can smell a bank in trouble. And I again have a credit line – which I hope not to use.)

But the fact is, we need banks. They are like the arteries in our bodies; they keep the blood (money) flowing. And when our arteries get hard, we can be in danger of heart attacks. And it’s going to get worse, as banks are going to lose more money on their commercial real estate loans. Commercial real estate is down some 40% around the country.

There are a lot of books that try to pinpoint the cause of our current crisis. And some make for fun reading, like a good mystery novel. You can blame it on the Fed or the bankers or hedge funds or the government or ratings agencies or any number of culprits.

Let me be a little controversial here. The blame game that is now going on is in many ways way too simplistic. The world system survived all sorts of crises over the recent decades and bounced back. Why is now so different?

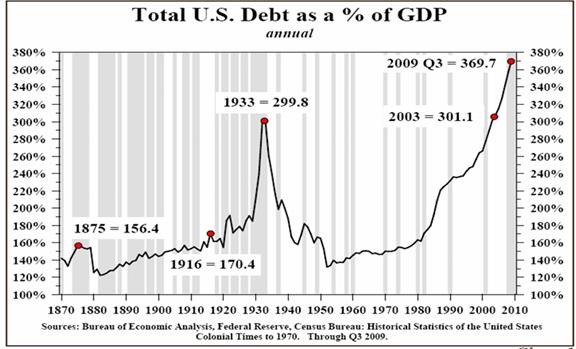

Because we are coming to the end of a 60-year debt supercycle. We borrowed (and not just in the US) like there was no tomorrow. And because we were so convinced that all this debt was safe, we leveraged up, borrowing at first 3 and then 5 and then 10 and then as much as 30 times the actual money we had. And we convinced the regulators that it was a good thing. The longer things remained stable, the more convinced we became they would remain that way. The following chart shows how our sandpile ended up. It’s not pretty.

I know Dad always say it is never “different,” but in a sense this time is really different from all the other crises we have gone through since the Great Depression that your Less-Than-Sainted Granddad used to talk about. What the very important book by professors Reinhart and Rogoff shows is that every debt crisis always ends this way, with the debt having to be paid down or written off or defaulted upon. That part is never different. One way or another, we reduce the debt. And that is a painful process. It means that the economy grows much slower, if at all, during the process.

And while the government is trying to make up the difference for consumers who are trying to (or being forced to) reduce their debt, even governments have limits, as the Greeks are finding out.

If it were not for the fact that we are coming to the closing innings of the debt supercycle, we would already be in a robust recovery. But we are not. And sadly, we have a long way to go with this deleveraging process. It will take years.

You can’t borrow your way out of a debt crisis, whether you are a family or a nation. And as too many families are finding out today, if you lose your job you can lose your home. What were once very creditworthy people are now filing for bankruptcy and walking away from homes, as all those subprime loans going bad put homes back onto the market, which caused prices to fall, which caused an entire home-construction industry to collapse, which hurt all sorts of ancillary businesses, which caused more people to lose their jobs and give up their homes, and on and on.

It’s all connected. We built a very unstable sandpile and it came crashing down and now we have to dig out from the problem. And the problem was too much debt. It will take years, as banks write off home loans and commercial real estate and more, and we get down to a more reasonable level of debt as a country and as a world.

And here’s where I have to deliver the bad news. It seems we did not learn the lessons of this crisis very well. First, we have not fixed the problems that made the crisis so severe. We have not regulated credit default swaps, for instance. And European banks are still highly leveraged.

Why is Greece important? Because so much of their debt is on the books of European banks. Hundreds of billions of dollars worth. And just a few years ago this seemed like a good thing. The rating agencies made Greek debt AAA, and banks could use massive leverage (almost 40 times in some European banks) and buy these bonds and make good money in the process. (Don’t ask Dad why people still trust rating agencies. Some things just can’t be explained.)

Except, now that Greek debt is risky. Today, it appears there will be some kind of bailout for Greece. But that is just a band-aid on a very serious wound. The crisis will not go away. It will come back, unless the Greeks willingly go into their own Great Depression by slashing their spending and raising taxes to a level that no one in the US could even contemplate. What is being demanded of them is really bad for them, but they did it to themselves.

But those European banks? When that debt goes bad, and it will, they will react to each other just like they did in 2008. Trust will evaporate. Will taxpayers shoulder the burden? Maybe, maybe not. It will be a huge crisis. There are other countries in Europe, like Spain and Portugal, that are almost as bad as Greece. Great Britain is not too far behind.

The European economy is as large as that of the US. We feel it when they go into recessions, for many of our largest companies make a lot of money in Europe. A crisis will also make the euro go down, which reduces corporate profits and makes it harder for us to sell our products into Europe, not to mention compete with European companies for global trade. And that means we all buy less from China, which means they will buy less of our bonds, and on and on go the connections. And it will all make it much harder to start new companies, which are the source of real growth in jobs.

And then in January of 2011 we are going to have the largest tax increase in US history. The research shows that tax increases have a negative 3-times effect on GDP, or the growth of the economy. As I will show in a letter in a few weeks, I think it is likely that the level of tax increases, when combined with the increase in state and local taxes (or the reductions in spending), will be enough to throw us back into recession, even without problems coming from Europe. (And no, Melissa, that is not some Republican research conspiracy. The research was done by Christina Romer, who is Obama’s chairperson of the Joint Council of Economic Advisors.)

And sadly, that means even higher unemployment. It means sales at the bar where you work, Melissa, will fall farther as more of your friends lose jobs. And commissions at the electronics store where you work, Chad, will be even lower than the miserable level they’re at now. And Henry, it means the hours you work at UPS will be even more difficult to come by. You are smart to be looking for more part-time work. Abbi and Amanda? People may eat out a little less, and your fellow workers will all want more hours. And Trey? Greece has little to do with the fact that you do not do your homework on time.

And this next time, we won’t be able to fight the recession with even greater debt and lower interest rates, as we did this last time. Rates are as low as they can go, and this week the bond market is showing that it does not like the massive borrowing the US is engaged in. It is worried about the possibility of “Greece R Us.”

Bond markets require confidence above all else. If Greece defaults, then how far away is Spain or Japan? What makes the US so different, if we do not control our debt? As Reinhart and Rogoff show, when confidence goes, the end is very near. And it always comes faster than anyone expects.

The good news? We will get through this. We pulled through some rough times as a nation in the ’70s. No one, in 2020, is going to want to go back to the good old days of 2010, as the amazing innovations in medicine and other technologies will have made life so much better. You guys are going to live a very long time (and I hope I get a few extra years to enjoy those grandkids as well!). In 1975 we did not know where the new jobs would come from. It was fairly bleak. But the jobs did come, as they will once again.

The even better news? You guys are young, still babies, really. Hell, I didn’t have a good year income-wise until I was in my mid-30s, and that was an accident (I literally won a cellular telephone lottery). And it has not always been smooth since then, as you know. But we get through bad stuff. That is what we do as a family and as the larger family of our nation and world.

So, what’s the final message? Do what you are doing. Work hard, save, watch your spending, and think about whether your job is the right one if we have another recession. Pay attention to how profitable the company you work for is, and make yourself their most important worker. And know that things will get better. The 2020s are going to be one very cool time, as we shrug off the ending of the debt supercycle and hit the reset button. And remember, Dad is proud of you and loves you very much.

Your trust me, we will get through this analyst,

John Mauldin

John@FrontLineThoughts.com

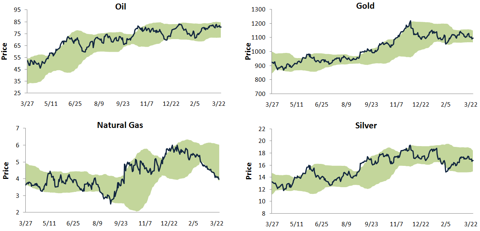

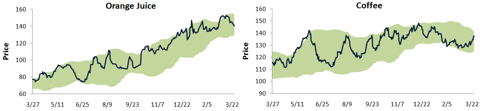

Below we highlight our trading range charts of ten major commodities. For each chart, the green shading represents between two standard deviations above and below the 50-day moving average. Moves above or below the green shading are considered extremely overbought or oversold.

Commodities have taken a back seat to stocks in recent weeks. As equities charge higher, commodities have mostly traded sideways. The only commodity shown that appears to be in a strong uptrend is platinum. While platinum has been strong, gold and silver have been trending lower. The auto industry has been strengthening lately, which could be a reason why platinum is outperforming the other precious metals (platinum is used in catalytic converters).

Of all the commodities, natural gas looks the worst. It is in a steep downtrend and is trading right at the bottom of its range. Is natural gas due for a bounce?

Finally, agriculture commodities like corn and wheat have really been performing horribly lately. Both are in nasty downtrends. (Click HERE to view larger charts)

Think B.I.G., by Bespoke Investment Group, provides some of the most original content and intuitive thinking on the Street. Founded by Paul Hickey and Justin Walters, formerly of Birinyi Associates and creators of the acclaimed TickerSense blog, Bespoke offers multiple products that allow anyone, from institutions to the most modest investor, to gain the data and knowledge necessary to make intelligent and profitable investment decisions. Along with running their Think B.I.G. finance blog, Bespoke provides timely investment ideas through its Bespoke Premium (http://bespokepremium.com/) subscription service and also manages money (http://bespokepremium.com/mm) for high net worth individuals.

Visit: Bespoke Investment Group (http://bespokeinvest.com/)

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair