Daily Updates

Shale Gas Going Global – An Interview with Dave Forest’

Dave Forest and I are philosophically aligned. Dave writes “Pierce Points” everyday (and I read it every day) and he is a former Casey Energy newsletter editor. We’ve started sharing ideas and a key one for both of us is that we see huge shareholder wealth being created for oil and gas investors as the new technologies now used in North America – horizontal drilling and fracking – get exported around the world.

Of course these technologies are 40 years old, but only in the last decade have they been perfected so they can get oil and gas out of shale rock.

Being able to make an economic hydrocarbon discovery in rock as opposed to the regular loose sands is about as simple as I can make the opportunity. It opens up the probability of billions of new barrels of oil to be discovered over the coming decade or two. Where is the next Saudi Arabia sized shale oil deposit? I think we could find out in the next decade.

These technologies were first perfected in the Barnett shale in Texas over a decade ago, and has now become the big growth engine of oil and gas production from Louisiana to northern British Columbia.

Literally tens of billions of dollars in stock values have been created for oil and gas investors by North American oil and gas plays like the Barnett, the Haynesville gas shale, and the Bakken and Cardium oil formations.

But the question for investors is now – what’s next for shale oil or shale gas? Where will the industry create billions in value next? Dave is much more technical than I am – he’s a geologist, I’m a journalist – so I asked him to share with readers where he sees the next big opportunities in shale oil and gas, for investors.

“These technologies are quickly going to move around the world,” he said. “Foreign companies are scrambling to learn the tricks and “take the show on the road”. We’ve seen a slew of farm-in deals from companies like Total on shale gas acreage in Texas, and other foreign companies in other basins. More than production, these companies are looking to learn from their North American partners, and use this to unlock new basins abroad.”

So which shale basins do you think will get developed next?

“Well, before I answer that, it’s important to know that economic shale gas is about more than just geology. There are a lot of gas-bearing shales around the world. But making money cracking shales is a tough game. You need high-quality services at a reasonable cost. China is cheap but probably not good, and the UK is good but well costs can run 2 to 3 times the cost for a comparable well in Texas. That blows your profitability.”

OK, sssoooo….how will investors know what the next big international shale play?

“Money will be made in overseas shale gas. But it will take places with

1) a strong gas market, and decent pricing,

2) lots of services competition, and

3) basins with good history of conventional production, where geologic data is readily available.

Poland and the Czech Republic have been held up as examples of countries where all these goals might be achieved.

Perhaps more interesting is the shale gas activity that’s starting to pick up in southeast Asia, e.g. northern Thailand. One angle here may be access to affordable, high-quality services from Japan. Combined with a strong southeast Asian gas market, shale gas projects might be economic here.”

In our next story, Dave will help us understand how market economics in the gas industry in Europe is changing, and how that could affect shale gas plays there.

Dave Forest’s analysis on the natural resources sector has been featured on BNN, Kitco.com, Financial Sense and the Daily Reckoning. He is a professional geologist and formerly advised a worldwide client base on oil/gas, mining and renewable energy at Casey Research LLC. Dave currently serves as managing director of Notela Resource Advisors Ltd. and writes the daily e-letter Pierce Points, on natural resources and the macro-economics that drive the sector.

You can sign up for Dave’s daily letter at www.piercepoints.com. (He is a great read – more concise than me).

Hello, this is Keith Schaefer, editor and publisher of The Oil & Gas Investments Bulletin. I started my subscription service in mid-2009 because I could see there was no place where retail investors could go to easily find which oil and gas companies were creating huge shareholder wealth by using exciting new technologies, such as horizontal drilling, fracing and 3D seismic.

These companies are increasing cash flows – and stock prices – by finding ways to get more oil and gas out of the ground. And junior and intermediate producers – $2-$20 stocks – are leading the way.

I find the leaders in the new plays that are using these technologies. My research is finding higher and higher flow rates from new wells in old formations as management teams fine tune their use of these new technologies.

It’s amazing how technology is lowering operating costs – and increasing profits – for many publicly traded energy companies.

I find the ones who have the capital and the knowledge to be the fastest growing in their area – this usually means they have a large undeveloped land position in an area where either production costs are very low or production rates can be very high. They are covered by several research analysts, so there is research support and institutional money flow behind them.

And my subscribers and myself are making money from my research. I eat my own cooking and buy all the stocks I research for subscribers.

I read MANY research reports, and I do a lot of original research – call management teams, talking to my contacts in the oil patch, scour company financials – to find the companies with the best chance to provide investor profits.

But these reports also give me many great story ideas for the blog, that haven’t hit the mainstream media yet. That’s why you should sign up at the blog to get notified of new stories.

I write the blog and the subscription service so everyone can understand the story. I keep it simple.

Subscribers get a minimum 10 issues a year, and there is often more than one stock presented.

The Oil and Gas Investments Bulletin is a completely independent service, written to build subscriber loyalty. No company ever pays in any way to be profiled.

I am so confident you will find value in my service I offer a 60 day, money back guarantee, no questions asked, for annual subscription purchases. Please read the sample report I have posted on the website to get an idea of how I profile these fast growing stocks.

Email me with any questions at editor@oilandgas-investments.com

Keith Schaefer

Publisher

CANADIAN HOME PRICES STILL BUBBLING

The Teranet-National Bank National Composite House Price Index (a mouthful!) was released yesterday. This relatively new house price index is similar to the U.S. Case- Shiller index. In short, January saw another increase in house prices, rising by 0.5% MoM, taking the year-over-year to 7.5% (the highest on record, which goes back to 2000.

Not surprisingly Toronto (+0.9% MoM) and Vancouver (+0.7% MoM) led the gains while Calgary posted a 0.5% drop. The index has gone up nine months in a row on a monthly basis but January’s 0.5% increase was the smallest — although relative to the U.S. Case-Shiller 0.3% result, it is still quite bubbly.

…..read the Whole Market Musings & Data Deciphering HERE

In This Issue:

• While you were sleeping — global equity markets are responding positively to a slate of very robust manufacturing diffusion indices for March

• Some first quarter earnings thoughts — the consensus is currently expecting 37% YoY earnings growth for Q1, with revenues up 10%

• Income is king — while equity markets have been a strong performer in the past year, risk-adjusted returns still belong to the fixed-income market

• Size matters — once the arithmetic boost from lesser inventory withdrawal is adjusted from the real GDP data, it shows that the economy only managed to rebound at a tepid 1.6% annual rate since the recession technically ended

• Lies, damned lies and statistics — the media was just fawning over the Case-Shiller home price numbers … give me a giant break

• Confidence or lack thereof

• Show me the money!

• Chicago! Chicago PMI at a three-month low of 58.8 in March

• Canadian spring — more signs of a spring thaw in Canada with January’s GDP coming in above expected, rising 0.6%

• Canadian home prices still bubbling

…..read the Whole Market Musings & Data Deciphering HERE

When it comes to equity analysts Teun Draaisma is a must-read. The European equity analyst famously called for investors to sell stocks in June 2007 when the markets were flashing a “full house sell” signal. He then flipped bullish in November of 2008 as the markets were pricing in a much more severe situation than Draaisma saw unfolding. He’s one of the few investors who actually got the downturn and the upturn correct and was able to connect the dots between cause and effect. In his latest strategy note Draaisma is saying the rally has gotten ahead of itself and that we’re due to for a correction as good news becomes bad news. In addition to being bearish about 2010 (see here), Draaisma says the better than expected growth in the near-term is putting more pressure on the Fed to raise rates and will lead to tightening measures sooner than most investors suspect:

“The rally since 5-February is nearing its end, we believe. Our thesis is that good growth will lead to tightening measures and struggling equity markets this year, just like in 1994 and 2004. The recent rally was larger than we expected, and in our eyes was due to:

1) there have been no positive payrolls or Fed language change yet (we even saw some loosening rather than tightening

measures last week, with the Greek bailout, the ECB keeping its wide collateral pool for longer and the Obama plan for troubled

mortgage borrowers).

2) sentiment had turned quite cautious in early February. Nevertheless, we do think the market peak associated with the start of tightening is near, and expect 2010 to show a volatile whipsaw pattern in equities. We expect good payrolls (April 2) and a Fed language change (April 30), some leading indicators are rolling over from multi-decade peaks (ECRI leading indicator for the US, OECD leading indicator for the world), and some sentiment surveys have turned more bullish.”

Draaisma believes the market will decline 11% in the next 3-6 months:

“The 3-6 month outlook: tactical caution. The last 12 months have been characterised by record stimulus and rising economic leading indicators. We think the next 6 months will be characterised by some stimulus withdrawal (as a reaction to good growth in Asia and US), and softening leading indicators. We reduced our equity exposure two months ago. We recommend selling into strength, and we think MSCI Europe will reach 1030 at some point later in 2010, down 11% from here.”

On a longer time horizon Draaisma says the markets remain entangled in a bear market and that investors should not be fooled by the cyclical bull within a secular bear:

“The multi-year outlook: the secular bear market that started in 2000 is not yet complete (pages 11-13). We believe the secular bear market is incomplete for a variety of reasons, including that banking crises and bailouts tend to precede debt crises; that the amount of debt has not been reduced yet (it only changed hands to the government); that equity valuations never reached end of bear market levels; and our historical analysis that equities tend to struggle for longer in the aftermath of secular bear markets. When the next earnings recession hits, perhaps in 2012, we expect equities to complete the bear market that started in 2000.”

Draaisma’s outlook isn’t exactly consensus, but then again, it never really has been. And that makes his research a breath of fresh air on Wall Street.

The proprietor of The Pragmatic Capitalist is the founder and CEO of an investment partnership. Prior to establishing his own business, TPC worked at Merrill Lynch Global Wealth Management. TPC is a Georgetown University alumnus, growing up in the DC area and now living in Southern California.

Rather than focus on one facet of markets, the goal at TPC is to assess and address global capital markets as a whole – with the understanding that all markets are intertwined and being an “expert” in one segment of the market without a vast knowledge of the others is futile.

The saying “common sense is very uncommon” has never been more applicable than it is to modern markets. TPC attempts to approach markets with sound reasoning and as little emotion as possible. A capitalist through and through, but always pragmatic…

High Conviction: Emerging Market Debt Now Offers Strong Potential

Which single asset class do you think will perform best in 2010?

“

We like emerging markets fixed income. We’re not convinced that global economies are as strong as equity investors appear to believe. Viewing total return as capital gains plus income, we’re expecting income to be a primary driver of total return in 2010.

Emerging markets have strong balance sheets, responsible fiscal and monetary policy and better long-term growth prospects. Of course, they’re not without risk. Many are dependent on foreign consumption, particularly on U.S. consumption, and the lack of foreign demand will weigh on their economies. However, we believe these markets still offer strong potential in 2010 with less risk than developed markets.”

…..read more HERE

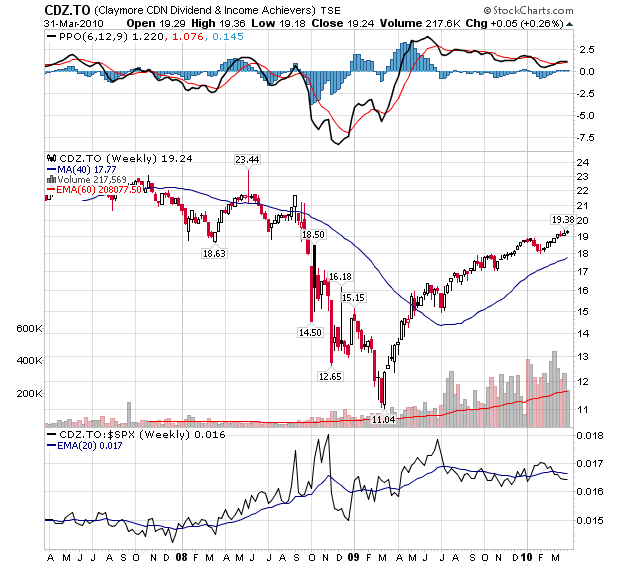

Yields, yields, is there any decent income out there? I’ve been looking at DVY, the ETF that follows the Select Dividend Index fund. I include a description of this ETF below. The current yield on DVY, according to Big Charts is 3.64%, which is not bad, these days. The chart below is from Stock Charts and shows the action of DVY from mid-1986 to the present. According to RSI, DVY is overbought. Richard Russell Dow Theory Letters

For those who want to buy DVY, I’d suggest buying it in quarters, 25% of your total intended commitment in four sections, say a quarter every three months. (Ed Note: Canadian Dividend ETF below)

Canadian Dividend ETF below CDZ.TO (from April 08)

Brief Excerpt from Richard Russell’s Dow Theory Letters. One of the best values anywhere in the financial world at only a $300 subscription to get his DAILY report for a year. HERE to subscribe. Amongst his achievements Richard was in cash before the 2008/2009 Crash and he has been Bullish Gold since below $300 Ed Note: Richard Russell is bullish Silver and holds one of the largest single positions he has held since the 1950’s in the precious metals.

John Middleton, CFA, CAIA joined Clinton, NJ based Brighton Financial Planning in August 2008 and assumed ownership in February 2010. Prior to Brighton, John spent 7 years with the Invesco Quantitative Strategies Group as a Senior Director and Client Portfolio Manager. While with IQS, John was responsible for over 50 clients worldwide with more than $2.5 billion in assets under management.

Seeking Alpha recently had the opportunity to ask John about his current asset allocation and perspective on opportunities in this market.

….buying greenfields for farming in Brazil and farmland in Canada to get into the farming business, on the basis that farming is going to be one of the great businesses over the next 20 years

– Jim Rogers – The legendary co-founder of Quantum Fund

The best investments – gold and farmland say’s Marc Faber

The Shape of Tomorrow’s Farming

By Dennis Avery – director of the Center for Global Food Issues at the Hudson Institute

Tomorrow’s farming will look like today’s, only more so. Crop and livestock yields per acre must triple again to protect wildlife habitat. Biotechnology will be increasingly vital. Confinement feeding will be even more important, to leave room for wildlife. Organic will prove to be a fad, as will locovores and vegetarians. Activists will be less credible than over the past 50 years.

The world’s farmers are facing the biggest challenge in their history. Expect more than 8 billion humans by 2050, with 7 billion of them affluent—compared with only 1.5 billion affluent today; trade and technology are powerful forces for increased wealth. Expect also a continuing surge in the number of companion cats and dogs, none of them vegetarian.

World food production must double by 2050, and production of meat and milk will more than double. Children need the key micronutrients of livestock products to prevent such diseases as pellagra and blindness due to severe Vitamin A deficiency. Their cognitive development also seems to benefit from high-quality protein.

Farming intensity must triple on the best land, in order to protect the poorer land which houses three-fourths of the wild species. Good farmland will become even more important, as one of the scarcest resources.

…..read the 7 page report HERE

Tom Fernandes: Going Long On Agriculture

Crigger: Is farmland an overlooked opportunity for investors?

Fernandes: Yes. We think it will be a great long-term investment, a great place to be. Most people on an institutional level don’t get too excited about it, because it’s a low yielder. It yields maybe 2-4 percent on investment, net of taxes, from a landlord perspective. That’s pretty low in an environment where muni bonds are yielding over 10 percent in some situations. A lot of institutional investors, you show them farmland investments, and they really don’t get too excited. So from a contrarian standpoint, that’s not too shabby.

But you have to be careful. People piled into farmland investing in the 1980s, and interest rates went higher and clobbered a lot of levered investments, most of which were farmers. It really depressed farmland prices, and it took more than a decade to improve the appetite for farmland.

So you’ve had a pretty big move in the prices. If I go back to Iowa in the early 2000s, farmland in the average acre made about $1,500 to $2,000 per acre. Now you’re pretty solidly at $3,500 per acre on average, and that includes less desirable land. Premier land may be $5,000, $6,000 per acre. So there’s been a big move there, and it’s not for the faint of heart. But you don’t have contango, and so on. Farmland’s something that we’re interested in, and we’re working on some investments there. It’s a good place.

….read the whole article HERE

Using Grains To Diversify Your Portfolio

“One such popular fund is the PowerShares DB Agricultural Fund (NYSE Arca: DBA), which holds a basket of 11 futures contracts dominated by grains. Although live cattle is the index’s largest individual holding, together corn, soybeans, wheat and Kansas City Wheat make up 35.84 percent of the portfolio. The rest of the index is divided among other top-performing ag futures, including sugar (11.33 percent), coffee (11.14 percent) and cocoa (10.45 percent).”

….read the whole article HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair