Daily Updates

Income tax returns are due in eight days. And as you’re scrambling to get yours finished, how you’ve spent your money in 2009 should be fresh on your mind. That’s why this is a great time to start (or revisit) your personal savings plan for the rest of this year.

Now, we all know about the “conventional” ways to save — including opening a traditional savings account, starting a Christmas club account, accumulating debit card rewards or bank points with our everyday purchases, and setting up monthly automatic deposits to savings accounts.

So, today I’d like to explore five unconventional methods for socking away a little extra cash each month …

Savings Strategy #1:

Separate your long distance phone carrier

Instead of bundling all your phone services, consider separating them. There are several long distance phone carriers that charge you cheap rates for only the long distance calls you make.

How it works: They charge about 3 cents or 4 cents per minute with six-second billing increments and no minimums or monthly fees.

For instance, if you call someone out of state and talk for an hour or so, your bill can be as low as $5 or $6, including taxes and fees, for the month. And if you don’t talk to anyone in a month, your bill is zero!

Pioneer Telephone is one example of a company that offers this type of service. But there are plenty of others with similar services. Just do a quick Internet search and you’ll find lots of choices.

Savings Strategy #2:

Enroll in your local utility company’s budget plan

By enrolling in a budget plan, participating customers pay about the same amount each month, no matter what the temperature does.

How it works: The utility company looks at your energy usage for the previous 12 months. Then, your monthly budget billing amount will be based on the average of your actual bills during the last 12 months.

While it may not actually save you money, the predictable nature of this payment system makes it much easier for you to budget. And that means it will be far easier for you to find ways to regularly plan and save.

Savings Strategy #3:

Switch to a cash-back gas credit card

If you haven’t done so already, consider applying for a gas-company credit card that offers cash-back rebates with your purchases.

For example, BP Plc has the following program for their customers: If they buy Amoco Ultimate gas they will earn a 2 percent rebate on every $1 of net purchases made at BP locations with no limit on the number of rebates they can accumulate in the program.

Then, for every $25 earned in rebates they can receive a $25 BP gift card … receive a check for the amount … or donate the rebate to an environmental charity.

And there are plenty of other gas companies offering similar rebate programs. A simple Internet search will yield plenty of choices

Savings Strategy #4:

Download coupons online

If you’re looking for discounts on your purchases, they’re probably just a mouse click away.

Taking the time to search for online coupons could mean big savings on products you regularly buy.

One popular website is coupons.com, and all you need to get started is your zip code. The site will tell you which coupons apply to your area. Another website I like is SmartSource.com, the self-described “#1 Website for Printable Grocery Coupons.”

Plus, if you buy items online, it almost always pays to do a quick search for coupons that apply to the particular online store or product you’re looking at.

And if you have an iPhone, an application like Yowza can also help you save money while on the go. The app finds deals and coupons in your geographic area … then, at the cash register, you show the clerk the Yowza deal on your mobile device and they’ll simply scan the barcode on the screen!

One word of warning: When visiting these websites or downloading mobile phone apps, some stores you patronize may not honor online coupons or deals. So before you run out the door with your online coupons in hand, please check with your local store to see if they accept them.

Best wishes,

Amber

This investment news is brought to you by Money and Markets. Money and Markets is a free daily investment newsletter from Martin D. Weiss and Weiss Research analysts offering the latest investing news and financial insights for the stock market, including tips and advice on investing in gold, energy and oil. Dr. Weiss is a leader in the fields of investing, interest rates, financial safety and economic forecasting. To view archives or subscribe, visit http://www.moneyandmarkets.com.

On December 11th, 2009 NIA declared silver the best investment for the next decade. In our December 11th article, we said that it wasn’t a coincidence that the very day Bear Stearns failed was the same day silver reached its multi-decade high of over $21 per ounce. We went on to say, “The reason why we believe the Federal Reserve was so eager to orchestrate a bailout of Bear Stearns, is because Bear Stearns was on the verge of being forced to cover their silver short position.”

Tid-Bit: What famous law enforcement man used silver in more ways than one? Answer at end of article

JP Morgan took over the concentrated short position in silver from Bear Stearns and gained complete control over the paper price of silver. Within weeks, JP Morgan was able to manipulate the price of silver down to below $9 per ounce. NIA believes they were able to drive the price of silver down through “naked short selling”, selling paper silver that is unbacked by physical silver.

On February 5th, we witnessed another sharp decline in silver prices, which NIA described on February 7th as being “just a temporary wash out, before a huge surge in silver prices later in 2010”. Since then, silver prices have rebounded by 18%. The temporary wash out that occurred on February 5th was predicted by independent metals trader Andrew Maguire, who came out this week exposing the fraud that is taking place in the paper silver market.

On February 3rd, Andrew Maguire wrote Eliud Ramirez, a senior investigator for the CFTC’s Enforcement Division, giving him the “heads up” for a “manipulative event” signaled for February 5th. He warned the CFTC that JP Morgan was about to manipulate down the price of silver after the release of non-farm payroll data on February 5th. Andrew said that the takedown would happen regardless of if employment was better or worse than expected and the price of silver would be flushed to below $15 per ounce. During the next couple of days, silver was crushed from $16.17 per ounce down to a low of $14.62 per ounce.

Despite all of the evidence given by Andrew Maguire to the CFTC of gold and silver manipulation, Andrew wasn’t allowed to speak at last week’s CFTC hearing on limiting gold and silver positions held by banks like JP Morgan. Bill Murphy of the Gold Anti-Trust Action Committee (GATA) was allowed to speak (within a five-minute time constraint) and present some of Andrew Maguire’s evidence, but right when his presentation began there was a technical failure of the live television broadcast, which was mysteriously fixed as soon as he was done speaking. Bill Murphy was scheduled for several mainstream media television interviews after the CFTC hearings, but they were all abruptly cancelled at once.

A couple of days after the CFTC meeting, Andrew Maguire and his wife were involved in a bizarre hit-and-run car accident in London where a second car coming out of a side street struck their vehicle, which resulted in a police chase using helicopters and patrol cars before the suspect was nabbed. Andrew and his wife were released from the hospital with minor injuries. (NIA does not believe in conspiracy theories but when you consider that this is a potential multi-trillion dollar fraud that could bring down the world’s financial system, it really makes you think.)

The silver market provides a window into what is happening in the gold market. Because the silver market is very small and its short position is so concentrated, its price is easier to manipulate than gold, but the same manipulation is taking place in gold on a much larger but less noticeable scale. In our opinion, the CFTC is under pressure not to do anything about the manipulation because the lower gold and silver prices are, the stronger the U.S. dollar appears to be. If we saw an explosion to the upside in gold and silver prices, it would result in a complete loss of confidence in the U.S. dollar.

NIA believes the precious metals markets are currently being artificially suppressed by paper gold and silver that doesn’t physically exist. At last week’s CFTC hearings, Jeffrey Christian of the CPM Group admitted that banks have leveraged their physical bullion by 100 to 1. This means for every 100 ounces of paper gold/silver that trade, there could be as little as 1 ounce of physical gold/silver in the vaults backing it. However, Mr. Christian sees no problem with this because he says “it has been persistently that way for decades” and there are “any number of mechanisms allowing for cash settlements”.

What Mr. Christian fails to realize is, most investors around the world holding paper gold/silver believe they own physical gold/silver. There will come a time when these investors don’t want cash settlements in U.S. dollars, but they will want the physical precious metals themselves. When investors around the globe eventually call for physical delivery of their precious metals, NIA believes it will result in the biggest short squeeze in the history of all commodities.

The physical silver market is now more tight than ever before. In the first quarter of 2010, the U.S. mint sold 9,023,500 American Silver Eagles, the most since the coin debuted in 1986 and up from 8,299,000 sold in the fourth quarter of 2009. All U.S. silver mines combined are currently producing only 40 million ounces of silver annually. This means the U.S. needs to use almost all of its silver production just to keep up with the demand for American Silver Eagle coins.

Silver closed this week at a 10-week high of $17.89 per ounce and a major short squeeze to the upside could be imminent. With the spotlight now on JP Morgan, NIA believes they will be less likely to naked short silver at these levels and manipulate the price down like in February. With the mainstream media blackout, it is important for NIA members to work harder than ever to spread the word and help expose what could be the largest fraud in the history of the world.

Please spread the word about NIA and have your friends and family subscribe for free at: http://inflation.us

What famous law enforcement man used “silver”?

Answer: He used silver bullets and rode his horse, Silver

This week we look at two brief essays for your Outside the Box. The first is my friend Barry Habib talking to us about where mortgage rates are headed. Barry gives us a very simple, but logical analysis on why rates are headed up. Then we jump to Spencer Jakab writing in the Financial Times about the problems in the municipal markets. Seems we may be under funded on our public pensions by about $3.5 trillion. As a tease to his column:

“Taking a page out of Greece’s playbook, the peeved treasurer of America’s largest state fired off letters this week to the chiefs of Goldman Sachs and other banks questioning their marketing of credit default swaps on California’s debt . The instruments, he complained, “wrongly brand our bonds as a greater risk than those issued by such nations as Kazakhstan.”

“Insulting indeed, but who exactly should be insulted?”

It helps if you have seen Borat, or at least a trailer, but the message is the same.

I am off to Phoenix and San Diego, the NYC next week, so I will be writing on the road. Have a great week.

John Mauldin, Editor

Outside the Box

Where Are Rates Headed And Why?

By: Barry Habib, Chairman, Mortgage Success Source

So the Fed stopped buying Mortgage Backed Securities, and people are wondering if this will affect mortgage rates. There’s been plenty of whistling past the graveyard, guesswork and denial, where so-called experts have been trying to tell us that there will be minimal – if any – change to rates.

That pipe dream is just nonsense.

Let’s look at what we can expect for mortgage rates and the overall Bond market in the months ahead. During the past fifteen months, the Fed purchased $1.25 Trillion in MBS, which represented 80% of the mortgage market. Prior to this program, mortgage rates were above 6%. Now that the Fed program has ended, it’s reasonable to assume that mortgage rates will rise back towards those levels.

Just How Much Money is $1.25 Trillion?

In today’s financial headlines – the word Trillion is often casually thrown around. So much so, that it’s easy to lose perspective on how much money this really represents. Picture a stack of $100 bills. It might surprise you to know that it only takes a stack four inches high to be worth $100,000. So $1,000,000 would be a stack of $100 bills 40 inches tall. How about a Billion? Well, you would have to stack $100 bills up to the top of the Empire State Building…twice…in order to reach a Billion. So to picture $1.25 Trillion represented by a stack of $100 bills – that stack would be 850 miles high. If you could turn that stack on its side and were able to drive alongside it, it would take you longer than 14 hours to reach the end. If you laid those $100 bills down side by side, they would travel around the world 50 times. We’re talking about a lot of money here.

The Fed’s purchasing influence has been significant. And now in the absence of this safety net, Bond prices and mortgage rates will experience greater volatility and a gradual worsening. Adding to this is the fact that the Fed will, albeit gradually, begin to sell some of their mortgage holdings, as they reverse their quantitative easing measures. It doesn’t take a rocket scientist to see that this will pressure Bond prices…but read on, because there are additional factors at play, which will influence Bond prices lower and mortgage rates higher.

What Moves Mortgage Rates?

Mortgage Rates are not pegged to the 10-year Treasury Note, as some have reported in the media. Those in the know do understand that mortgage rates are based on the pricing of Mortgage Backed Securities (MBS)…and these Mortgage Bonds are influenced by many different factors.

They respond quite well to technical signals as well as Stock market volatility, as money can be drawn from or parked into Mortgage Bonds. Certainly, the news and inflation implications also play a heavy role in influencing Mortgage Backed Securities.

And just like the aforementioned influential factors, Treasuries can also play a role in the price direction of Mortgage Bonds. Last year, the 10-year Treasury Note was at approximately 2.2% and has since moved towards 4%. During this time, mortgage rates have been virtually unchanged. But now, Treasuries are offering yields that are close to the current Mortgage Backed Security rates, which are offered to investors.

Let’s take a moment to understand the difference between the mortgage rate a borrower pays and the coupon yield on a Mortgage Backed Security that an investor receives. If a borrower pays 5.25% on their loan, only 4.5% of that is passed on as a coupon yield to the investor. This is because the mortgage loan servicer (that’s who you make your payment to) takes a piece of the action. Additionally – the aggregators of these loans, like Fannie Mae and Freddie Mac take a piece as well. And let’s not forget the folks on Wall Street, who need to get paid for underwriting, securitizing and selling this paper.

We know that Treasuries are backed by the full faith and credit of the US Government and are free from state income tax. And the 10-Year Treasury Note, while clearly not pegged to Mortgage Backed Securities, does offer investors a competitive alternative with a similar maturity period to Mortgage Backed Securities. But because of greater safety and tax advantages, the 10-Year Note will always trade at a lower yield than Mortgage Backed Securities, and therefore put a floor beneath how low Mortgage Backed Security coupon yields and corresponding home loan rates for borrowers can go.

The US is spending at an unprecedented rate – and its spending money it doesn’t have. This means that more and more Treasuries will continuously need to be auctioned off. And in order to entice buyers to keep absorbing this supply, yields will very likely need to continue higher, just as they have for over the past year.

Additionally – sovereign debt has come into question. Downgrades in the sovereign debt of both Greece and Portugal are a warning to the US that the same can happen here, which would drive the cost of borrowing much higher. Our government currently spends $1.49 for each $1.00 it brings in. Our debt is now 57% of GDP…and rising. Does anyone really believe that Treasury yields are headed lower? As Treasury yields move higher from their current levels, mortgage backed security coupon yields will also need to move higher in order for investors to want to purchase them.

The Ever-Important Carry Trade

While the Fed’s end of the MBS purchase program and eventual selling of MBS – along with an almost certain move higher in Treasury yields – all tell us that mortgage rates are headed higher, there is another important element that could have an even greater influence in moving yields higher and prices lower throughout the Bond market. It’s called an unwinding of the “carry trade.” The low interest rate environment in the US has provided fertile ground for the carry trade, where large investors can borrow at very low rates, and leverage into higher yields, resulting in huge returns.

Let’s take an example: An investor wishes to purchase $1M in Mortgage Bonds yielding 4.5%. This would provide $45,000 as an annual return. In order to make the purchase, the investor puts up only 10% of $1M, or $100,000 in cash – and borrows the other $900,000 at the Fed Funds Rate + 2%, for example – which would be a borrowing cost of 2.25% or $20,250. This investor receives a $45,000 return, but subtracts a $20,250 cost to borrow $900,000 – leaving them with a net return of $24,750. Remember, the investor needed only to invest 10% of the $1M purchase – or $100,000 in cash. This gives the investor a whopping 24.75% return on their investment in a boring little old Mortgage Bond. And of course, this “carry trade” can be used in other securities as well.

While the investor understands that there are always market risks at play – the juicy 24.75% yield cushion gives them much added comfort to stay in the trade. But the biggest risk for the investor is if their borrowing costs – which are based on the Fed Funds Rate – were to rise.

When the Fed starts to hike rates, it will signal the beginning of a tightening cycle. A few Fed hikes can cause the yield cushion to quickly evaporate…and the decline in Bond values from overall higher yields could turn the trade from highly profitable to highly costly in a very short period of time. So why do these carry trade investors have such a care free attitude and confident air? It’s because Ben Bernanke and the Fed have assured them that there is nothing to fear. How did the Fed do that?

Via “Fed Speak,” these carry trade investors hear that “conditions warrant exceptionally low rates for an extended period of time.” Translation: your biggest fear – that a hike in the Fed Funds Rate, which increases your borrowing costs and wipes out your gains – won’t happen anytime soon. It’s this “extended period” verbiage that is keeping the carry trade in place. When the Fed removes the “extended period” language, this will signal that hikes will begin in the near future, and that risk will prompt investors to begin to “unwind” their carry trade holdings. This will include the selling of Mortgage Backed Securities, which will assuredly push yields higher still.

When will the Fed remove the “extended period” language? It may happen sooner than you think. Kansas City Fed President Thomas Hoenig has officially dissented to the “extended period” language at the last two Fed meetings. And recently, St. Louis Fed President James Bullard, while yet to officially dissent, has stated that he feels “extended period” is inappropriate language and should be replaced by “data dependent.” And there have been grumblings from other Fed members, who are growing more concerned that leaving rates too low for too long can spawn asset bubbles or inflation down the road.

What It All Comes Down To

When all the factors are considered – the chances of higher interest rates are a virtual lock. And anyone in the market to borrow should consider acting sooner rather than later. With such low rates still in our hands…and all these various factors pointing at the inevitable fact of rates moving higher…you have to wonder what people sitting on the sidelines are waiting for?

It brings to mind the closing scene of the movie “Dumb and Dumber,” where two good-hearted but incredibly stupid heroes Lloyd and Harry are hitch-hiking, when along pulls up a bus full of beautiful Hawaiian Tropic models in bikinis. The models tell Lloyd and Harry that they are looking for two “oil boys” to lube them up before each of their photo shoots on the tour. Lloyd and Harry explain that there is a town down the road, where they should be able to find two lucky guys to help them out. As the bus pulls away, Lloyd and Harry look at each other and declare that one day their opportunity will come – they just have to keep their eyes open.

Here’s hoping you have your eyes wide open to take advantage of this fleeting opportunity…before it’s gone.

California ire over Borat bonds

By Spencer Jakab for the Financial Times (www.ft.com)

Maybe Bill Lockyer not make benefit glorious state California?

Taking a page out of Greece’s playbook, the peeved treasurer of America’s largest state fired off letters this week to the chiefs of Goldman Sachs and other banks questioning their marketing of credit default swaps on California’s debt . The instruments, he complained, “wrongly brand our bonds as a greater risk than those issued by such nations as Kazakhstan.”

Insulting indeed, but who exactly should be insulted? Home to Hollywood, Californians may derive their hazy image of Kazakhstan from Sacha Baron Cohen’s satirical take on a country where he claims the main forms of entertainment include the “running of the Jew”, the sport shurik “where we take dogs, shoot them in a field and then have a party”, and where the favourite plonk is made of fermented horse urine. The real Kazakhstan, though not problem-free, looks fairly solid compared to California and many other states – a fact that should worry investors in America’s $2,800bn municipal bond market.

On paper, California’s debt of $85bn supported by 37m citizens and the world’s eighth largest economy looks more manageable than Kazakhstan’s nearly $100bn heaped on its poorer population of 16m. Go beyond headline figures though and Kazakhstan, with the world’s 11th largest oil reserves, an economy that grew more than 8 per cent annually from 2002 through 2007 and unemployment of just 6.7 per cent looks positively vibrant next to the Golden State’s joblessness of 12.4 per cent.

Meanwhile, Kazakhstan’s modest budget deficit and $25bn rainy day fund make it a paragon of fiscal virtue compared to a state forced to pay bills with IOUs last year and possibly again this summer. Unlike US states, Kazakhstan has its own currency and central bank. If it were to raise taxes or cut public services, wealthy Kazakhs could hardly defect to Kyrgyzstan the way Californians, already facing some of the highest levies and worst schools in the nation, might decamp to, say, Utah.

But such head-to-head comparisons do not even begin to spell out the relative woes of American states compared to many developing nations. In addition to their headline borrowings, equal to almost a quarter of national output, states and cities have made trillions more dollars in promises to current and future retirees. Pensions are nominally underfunded by an already scary $1,000bn according to the Pew Center for the States, but that uses their own rosy actuarial assumptions. Former Social Security administrator Andrew Biggs reckons the shortfall would be up to $3,500bn if calculated using a more conservative private sector methodology. Tack on another trillion or so for unfunded health benefits and America’s states appear to have dug a hole so deep no amount of austerity can fill.

Demographics, too, favour developing countries. Even with a relatively restrained birth rate, the median Kazakh is four years younger than the median American and will live ten years less, cutting down the country’s dependency ratio. And while California’s innovators may or may not crank out future iPods, Kazakhstan will soon export even more oil as its giant Kashagan field and pipelines to booming China come on stream.

States’ borrowing costs are supported by a minuscule historical default rate on traditional municipal debt but also by the distortion of being tax-exempt. Lacking this feature, taxable California “Build America Bonds” given a direct federal subsidy yield 6.3 per cent for a 2022 maturity, some 2.4 percentage points above comparable US Treasuries. A more modest spread than Greek bonds over Germany’s, to be sure, but then Greek credit protection is also pricier.

After resorting to Hellenic-style fiscal sleight-of-hand to plug this year’s budget hole, it is alarming to hear California’s officials blame the messenger in similar style. They must grasp that markets don’t lie and creditworthiness is unrelated to superficial wealth. For example, Californians who illegally employ Mexican migrants as maids or gardeners might be surprised to learn that swaps traders consider its poor southern neighbour about half as risky a borrower as their state. Jagzhemash!

This article from:

John F. Mauldin

johnmauldin@investorsinsight.com

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor’s services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. (“InvestorsInsight”) may or may not have investments in any funds cited above.

PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

Communications from InvestorsInsight are intended solely for informational purposes. Statements made by various authors, advertisers, sponsors and other contributors do not necessarily reflect the opinions of InvestorsInsight, and should not be construed as an endorsement by InvestorsInsight, either expressed or implied. InvestorsInsight and Business Marketing Group may share in certain fees or income resulting from this publication. InvestorsInsight is not responsible for typographic errors or other inaccuracies in the content. We believe the information contained herein to be accurate and reliable. However, errors may occasionally occur. Therefore, all information and materials are provided “AS IS” without any warranty of any kind. Past results are not indicative of future results.

We encourage readers to review our complete legal and privacy statements on our home page.

InvestorsInsight Publishing, Inc. — 14900 Landmark Blvd #350, Dallas, Texas 75254

© InvestorsInsight Publishing, Inc. 2010 ALL RIGHTS RESERVED

Special offer from Mark Leibovit for Money Talks only: The intense analysis of Gold in the 10-12 page The VR Gold Letter is right now 75% off for the first month or $29.95 (regularly $125.00 a month). The weekly VR Gold Letter focuses on Gold and Gold shares.Go HERE and use the Money Talks promo code CBC12210

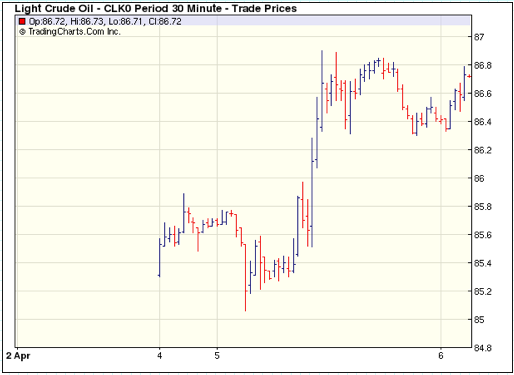

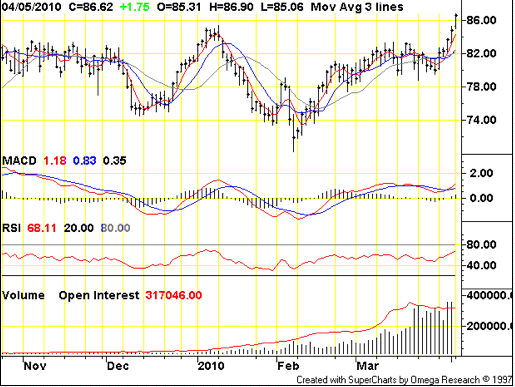

CRUDE OIL – ACTION ALERT –

Crude Oil closed at $86.68 +1.81 or 2.13%.

A strong open to the new week for capital markets after an extended holiday weekend would encourage a strong performance from crude oil. The third consecutive advance for this benchmark commodity has established remarkable momentum at fresh 17-month highs. Having surpassed the $84-level swing high last Thursday, there has been a notable interest among the speculative crowd to participate in this next leg of a larger bull trend. Looking at the delayed open interest on the benchmark NYMEX active futures contract, net positions rose 1.35 million contracts through Thursday – the highest level since March 18th (back when the gauge rose to a recent historical high). Today’s strength is no doubt sourced from the overall rebound in risk appetite. With most US market’s closed this past Friday for the US non-farm payrolls report, investors in the different asset classes had to play catch up. With only currency and bond traders online to trade the actual release, the initial response was one that encouraged interest rate forecasts, which subsequently boosted the dollar. However, the detrimental effect a higher currency would have on oil was overshadowed by the tentative gains in growth-related assets that would naturally develop alongside improved confidence in economic health. That being said, there was a notable limit to optimism in the Dow Jones Industrial Average. This is perhaps partly a side effect of a significant portion of the market still out for the holiday. If European shares help cycle the market even higher tomorrow, crude traders may soon see the $89.50 level that represents the mid-point of the 2008 to 2009 tumble that brought the commodity from record high to five-year low with the fallout from the worst financial crisis in generations.

Intraday chart @ 12:15am 04/06/10 Pacific time

Daily Close 04/05/10

Chart via Don Vialoux

Maverick Investing in the Age of Obamanomics

The most important thing you need to know about investing in the Age of Obamanomics is: invest in inflation. Consider two key investments that are perfect for the Age of Obamanomics: precious metals and carefully selected stocks. When we’re done with this chapter, you’ll know exactly what to look for and how to avoid the pitfalls.

Your investment program should be based in coins and bullion. Invest at least one-third of your assets in gold and silver coins or bars.

Precious Metals Are Basic to a Ruffonomics Portfolio

Gold and silver are perfect pure inflation hedges. Strictly seen as an investment, as the dollar shrinks in value, gold will be worth thousands of dollars an ounce and silver will be worth hundreds of dollars an ounce. Glenn Beck, one of my favorite talk show hosts, said he is “not buying gold as an investment, although it will be a good investment, but as insurance.” He doesn’t tell us what he is insuring against, but I’ll tell you. He’s insuring against the plummeting loss of purchasing power of all dollar-denominated investments, even the possible collapse of the dollar.

Precious metals feel so solid. When I was in South Africa, I went ten thousand feet down in a gold mine, and then came up to visit where they were producing gold bars. I held a new gold bar in my hands. It felt like wealth. It was real.

Then I went to the mint that manufactured krugerrands, South African gold coins, and we were permitted to handle these coins. Same feelings. I understand why people killed for them.

In these current circumstances, not buying gold or silver is one of the dumbest money decisions you can make in 2009-2010. Here are just a few reasons why this is so:

1. Obamanomics: Socialist states always inflate the paper currency. Obama, Congress, and the Federal Reserve are diluting the dollar like never before by creating more of it. Accommodating Obama and Congress, the Fed has manufactured trillions of dollars out of nothing at by far the fastest pace in history, and it’s accelerating. The government has given trillions to the big banks, which will loan the dollars into circulation or give them to politicians to spend into circulation. This money expansion currently dwarfs several times over the monetary explosion that led to the Carter-driven metals bull market in the ‘70s. I can’t overstate what is happening. Economists may call this monetary-expansion process “inflation” but it really should be called “dilution”—dilution of the money supply and consequently its value. Inevitably, sooner or later, consumer prices rise and laymen then mistakenly call that “inflation.” Calling rising prices inflation is like calling falling trees hurricanes. When will the public catch on? Price inflation and gold prices are the chief measurements of public awareness. Sooner or later, awareness becomes a critical mass, the public catches on, and the metals go through the stratosphere.

2. Real money: Gold and silver (especially silver) have been real money over and over again, in all ages of time and on all continents. Ever since Gutenberg invented the printing press 400 years ago, the world has been littered with worthless dead paper currencies every seventy-five to eighty years, due to runaway money printing. Every time the dominant currency has been inflated, gold and silver coins have become hugely profitable investments, and sometimes the only surviving currency.

Throughout history, each time a paper currency finally caved in to inflation, gold and silver (especially silver) became the only universally acceptable coin of the realm. Gold and silver as a means of exchange and a store of value have always survived. They have always been symbols of wealth, far more precious in our consciousness than any mere paper.

During periods of hyperinflation, there always comes a time when people refuse to accept more and more counterfeit, inflated money or base-metal coins in return for their hard-produced goods and services. At that point, society instinctively turns to gold and silver. It has happened over and over again, and as George Santayana said, “Those who cannot remember the past are condemned to repeat it.”

3. It’s early in the game: Gold and silver are early in an historic bull market (in fact, as this is written, it’s only a Golden Calf), making this a low-risk investment with an awesome upside for the long-term investor. Especially silver. This gold and silver bull market will dwarf the last great one in 1973-80, when fortunes were made by relatively small amounts of money invested by amateur investors (many of them my readers). All of the factors that created the last bull market are here again, only amplified several times.

4. Supply and demand: Both metals are far rarer than most people know. All the gold ever mined since the dawn of history, including that in Central banks, gold fillings, and sunken shipwrecks in the Caribbean, etc. would cover a football field about four-feet deep. It would make a cube about the size of a typical 8-room house. Demand is now leaping past new supplies.

Likewise, most of the easy silver has been mined over the centuries, even with primitive methods. For example, during the Roman millennium, they used silver coins for currency and exhausted the Spanish silver mines.

Now that prices are high enough to make gold and silver mining profitable again, it will take as much as seven to ten years to develop new mines, and stagnant supply and rising demand have made higher prices inevitable for the imminent future.

Click HERE to subscribe to Rufftimes

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair