Daily Updates

Purpose of Holding Gold

Most central banks hold their nation’s gold in the vaults of the world’s leading financial centers’ central bank vaults. These include New York, London, and Canada among others. In a peaceful, cooperative world, this is sensible as one of the prime purposes of central banks holding gold is to cover the nation’s international trade payments when their own currency becomes unacceptable and their reserves of foreign exchange are depleted. By positioning the gold outside the country, it’s instantly accessible for payments or guarantees of payments.

Dangers of a Nation Holding Gold in Another Nation’s Central Bank

In the last week we have heard the announcement that Iran has (according to them) 907 tonnes of gold. The developed world has just outlawed Iran dealing in gold and silver (there are other places, where if they wished to do so they will be able to trade). With their gold inside Iran, it is outside the reach of the developed world though. If they had held their gold in the world’s main, developed world vaults that would have been frozen along with Iran’s other overseas assets. We may not agree to Iran’s politics and attitudes, but there is a lesson to be learned here.

Ownership implies the freedom to do what you want with an asset. In this case we are talking about a nation’s assets. The handling of Iran’s assets by freezing of their assets shows that other nations can interfere with that freedom. Governments feel free to impose restraints on other people’s assets within their jurisdiction. It is this concept of a right to restrain the rights of ownership that will prove a growing issue.

With the world changing from an under-developed world with a developed world to an emerging world drawing down power and wealth from the developed world, there are many changes taking place which will lower the levels of international cooperation in the days ahead as political, religious, monetary and economic pressures rise.

One nation that has foreseen these pressures coming is Venezuela. Their 160 tonnes of gold was held in Canada, the U.S. and European vaults and out of their full control. Their policies –including the nationalization of gold mining and export—have proved unpopular in the developed world too. With Venezuela being an oil exporter primarily, the unpopular President (outside the nation) felt it prudent to ship his nation’s gold back home. The process began a few months ago.

Venezuela’s Gold Comes Home

Venezuela has now succeeded in bringing its 160 tonnes of gold from the developed world’s central bank vaults (i.e. Canada, U.S. and Europe). There’s no doubt that such a move does secure the nation’s monetary sovereignty. Now, Venezuela’s gold cannot be subject to the political wishes of the U.S., Canadian or European governments.

Furthermore, there’s a potential 3,000 tonnes of gold under the ground in Venezuela and the likelihood that the government will take that into their vaults over the time it takes to mine it. They will then be in a position to take the U.S. dollars they receive for their oil and pay their miners for the gold, so diversifying their reserves away from currencies and into gold. If they do that, then this is one more source of supply that will be removed from the gold market.

Whatever the nation’s politics, it is a central banker’s duty to do all in its power to protect its nation’s gold and foreign exchange reserves in terms of control and value. With dollar hegemony, a great deal of that power remains in the hands of the issuer of that currency. As sovereignty issues grow, it is becoming incumbent on central bankers to do more to protect nation’s reserves. The most vulnerable nations are those whose politics differ drastically from the developed world or those whose international trading is not dependent on the major developed world. After all, if you are a kind of economic colony of a major nation it will exercise its influence far more effectively through other routes.

The conclusion that best suits vulnerable nations logically is to hold as much of its gold at home. Its dollars have to be held in New York and its euros in Europe –something they can do little about. But a nation like Venezuela with its reserves of gold at home and a ‘natural’ diversifier in the gold under the ground, is acting in that nation’s interests in building up its gold reserves at home.

China Following the Same Path

China has outlawed the export of gold and vigorously broadened the number of banking import licenses for gold. The resulting flows of gold in with nothing coming out, is leading to the total national stock of gold in China rising fast.

- Last year saw around 360.96 tonnes of gold produced there with the government encouraging this growth of local production. But this figure may be a heavy underestimation as scrap and non-China Gold Association member’s production is not included in that number

- 490 tonnes of gold came into China through Hong Kong with more imports possible through other routes, not included in this total.

- At the start of 2012, demand for gold during the lunar New Year jumped over 50% pointing to much higher imports in 2012. These could lead to a jump of reported imports of 750 tonnes in 2012

China is preparing Shanghai as the center for Yuan trading and as their leading financial center. Hong Kong is the current, financial center and has huge modern gold vaults already. We have issued an article in our newsletter [www.GoldForecaster.com] giving our views on China growing to a second or first gold market hub in time. But we repeat that NO gold is allowed to leave the country! With privately held gold open to confiscation at some point in time, we consider the total gold held inside China as part of that nation’s available stock of gold in their reserves.

Part II will cover:

· U.S. and U.K. citizens holding their gold in foreign vaults?

· Switzerland

· Gold held in a Swiss bank

· Gold held in a Private Vault in Switzerland

· What are the remaining dangers?

The Solution & Pending Announcement!

We’ve prepared a series of articles on this subject for publication over the next few weeks. To ensure you get these subscribe through www.GoldForecaster.com.

Market Buzz – The Reign of the Balance Sheet Will Continue in 2012

Canadian stocks closed at their highest level in nearly four months on Friday, powered by financial and energy issues. Surprisingly, healthy U.S. employment figures offset sluggish Canadian jobs data and uncertainty over a Greek debt deal and helped the market to solid gains.

U.S. job creation in January far outstripped analyst expectations, with the unemployment rate dropping to a near three-year low of 8.3 percent. In addition, the pace of growth in the U.S. services sector unexpectedly accelerated to its highest level in nearly a year.

All told, the Toronto Stock Exchange’s S&P/TSX composite index ended up 23.80 points, or 0.2%, at 12,577.28. It was the TSX’s highest close since October 8th and capped the index’s seventh straight weekly rise.

Of course, this raises the question as to whether a pull-back is in order. To that, we answer in the affirmative. However, we do have a number of companies we are focusing on and would find weakness in select names and excellent opportunity to buy.

But what to buy? Well, for the “type” of companies we are currently looking for we look no further than to one of our most successful 2011 investment themes of 2012. One we expect to continue on into 2012 – and perhaps even accelerate. The trend is “the reign of the balance sheet.” In the first month of 2012, companies with strong balance sheets including zero or manageable debt, solid cash positions, good working capital, and good cash generation continue to power the market and garner the most attention. This attention can come from good to premium multiples or, in the case of four companies from our coverage universe in 2011, premium takeover bids. Both can lead to superior returns for investors.

From crisis and volatility comes opportunity. That became very apparent this past year as we saw four of our Focus Buy recommendations, Bridgewater Systems Corporation, Breakwater Resources Ltd., MOSAID Technologies Incorporated, and Distinction Group Inc., receive premium takeover bids. The common theme with each of the companies was strong balance sheets and strong cash flow. In fact, the first three each had over 40% of their market capitalizations in cash at one point, with strong earnings, zero debt and growth.

This type of pristine balance sheet can withstand and even profit from a downturn (via strategic expansion through purchase of distressed assets). We believe companies that hold this profile will continue to attract more attention from individual investors and as potential acquisition targets in 2012.

In fact, this was one of the main reasons we released our 2012 Cash Rich/Debt Free, Profitable Canadian Micro to Mid-Cap Report this past week.

Looniversity – Reverse Stock Split

Through the soaring bubble market of the late ‘90s, many investors became very familiar with the concept of a stock split as the run-away tech stocks hit triple digits and management endeavored to keep the per share price tag at “affordable” levels. However, if the first quarter of 2008 is any indication of what we might expect over the near term, enter the bear market’s answer, a reverse stock split.

When a company engages in a reverse stock split, it substitutes one share of stock for a predetermined amount of shares of stock. Like its cousin the stock split, it does not increase the market capitalization of the company.

To illustrate, assume ABC Corporation has 10,000,000 shares of common stock outstanding. Assume the market price is $10 per share and that ABC Corporation declares a 1 for 4 reverse split.

After the reverse split, ABC Corporation will have 1/4 as many shares outstanding, or 2,500,000 shares outstanding. The stock will have a market price of $40. If an individual investor owned 100 shares of ABC before the split at $10 per share, he will own 25 shares at $40 after the split. In either case, his stock will be worth $1,000. He is no better off before or after. Except that the company hopes that the higher stock price will make the company “appear more attractive” and thus, more investors will purchase the stock and the stock price will be bid up.

There is no assurance that a company’s stock will rise in price following a reverse split. In fact, some academic research indicates that NYSE and AMEX listed companies that reverse split their stock that did not perform well subsequent to the split. This may be due in large part to the fact that most companies that reverse split are in rather poor financial shape to begin with.

Put It To Us?

Q. Can you elaborate on the term “dead money” in reference to the stock market?

– Erick Broden; Calgary, Alberta

A. Dead money is a common term used on Wall Street to describe money that does not earn a return for an investor. From money stashed in a mattress to a non-interest yielding checking account or a security that does not yield returns, all are considered dead money. Essentially, any money or investment that does not grow or yield gains for the investor is usually referred to as “dead money.”

When an investor invests in securities, the expectation is that the security or investment will yield some profitable returns. When an investment is not expected to yield any returns, the investment is referred to as a “dead money investment.” Examples of dead money investments are shares or stocks of companies that are not expected to improve or appreciate past their current price (over a particular period in many cases).

You can’t feel the heat until you hold your hand over the flame.

You have to cross the line just to remember where it lays.”

~ Rise Against. “Satellite” Lyrics ~

Friday morning traders and market participants awaited the key January employment report from the U.S. Bureau of Labor Statistics. The reaction to the supposedly wonderful report was a surge in the S&P 500 E-Mini futures contracts as well as several other key equity index futures.

The overall tenor among the financial punditry was predictable as wildly bullish predictions permeated the morning session on CNBC and in the financial blogosphere. However, after the report had been out for several hours notable independent voices such as Lee Adler of the Wall Street Examiner came out with information that suggested the numbers were an apparition of manipulated statistics.

I am not going to spend a great deal of time discussing the report, but the reaction to the news was decisively bullish on Friday. The question I want to know is whether Friday was a blow off top? In the recent past the S&P 500 has seen several key inflection points and intermediate-term tops form on non-farm payroll monthly announcements.

I follow a variety of indicators to help me decipher more accurately when the market is getting overbought or oversold. For nearly two weeks the market has been extremely overbought, but now we are reaching truly astonishing levels. The following charts represent just a few signals that the market is due for a pullback and a top is likely approaching.

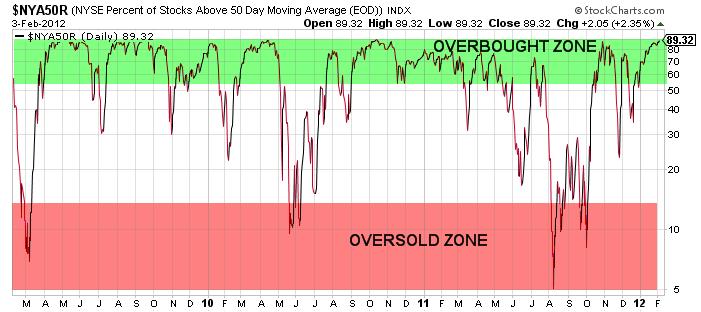

Percentage of NYSE Stocks Trading Above Their 50 Period Moving Average

The chart above clearly illustrates that as of Friday’s closing bell (02/03) over 89% of stocks were trading above their 50 period moving averages. Consequently that reading is one of the highest levels that we have seen in the past 3 years. In addition, over 73% of stocks that trade on the NYSE are currently priced above their longer-term 200 period moving averages. Another extremely overbought signal.

S&P 500 Bullish Percent Index Weekly Chart

The S&P 500 Bullish Percent Index is another great tool for measuring the overall position of the S&P 500. It is without question that the longer term time frame is reaching the highest level of overbought conditions in the past 3 years.

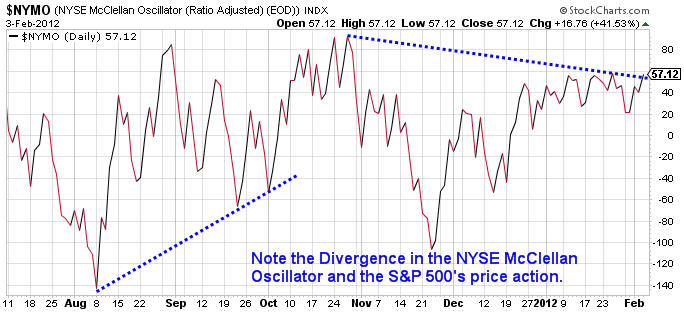

McClellan Oscillator Divergence with S&P 500 Price Action

The two charts shown above present an interesting situation regarding the divergence in the McClellan Oscillator and the price action in the S&P 500. The most recent example of this type of divergence occurred in October of 2011 and prices immediately reversed to the upside after several months of selling pressure. In fact, this correlation between reversals in the S&P 500 and divergences in the McClellan Oscillator works relatively well historically.

Clearly there are bullish voices arguing for the 2011 S&P 500 Index high of 1,370.58 to be taken out to the upside in the near future. Additionally, several market technicians in the blogospere have been pointing to the key resistance range between 1,350 and 1,370 on the S&P 500 as a likely price target. Obviously if those price levels are met strong resistance is likely to present itself. However, as a contrarian trader I have found that the more obvious price levels are the more likely it is that they either will not be tested or they will not offer significant resistance.

It is obvious that Chairman Bernanke and the Federal Reserve have embarked on a massive fiat currency printing campaign which has helped buoy risk assets to the upside. Through a combination of reducing interest rates on safety haven investments like Treasury’s and CD’s, the Federal Reserve has forced conservative investors and those living on a fixed income into riskier assets in search of yield.

This process helps elevate stock prices and creates the desired outcome for the Federal Reserve which involves the perception by average individuals that they are wealthier. The Fed calls this the “wealth effect” and they seem poised to insure that U.S. financial markets continue to ride upon a see of cheap money and liquidity.

Ultimately the Federal Reserve’s most recent announcements have served to help flatten the short end of the yield curve further while providing a launching pad for equities and precious metals. However, issues persisting in Europe could have an adverse impact on the short to intermediate term price action of the U.S. Dollar.

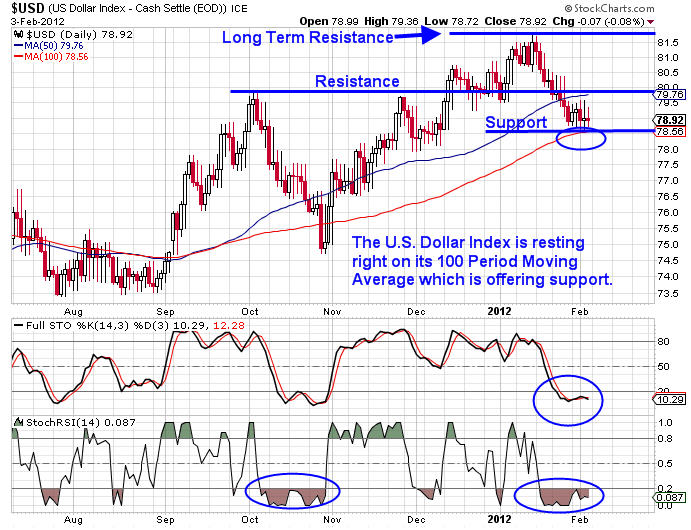

Right now everywhere I look I hear market prognosticators commenting on how hated the U.S. Dollar is and how Chairman Bernanke will not allow the Dollar to appreciate markedly in order to protect U.S. exports and financial markets. I think that the Dollar has the potential to rally in the short to intermediate term. Right now the U.S. Dollar Index appears to be trying to form a bottom.

U.S. Dollar Index Daily Chart

Obviously there is good reason to believe that the U.S. Dollar Index could reverse to the upside here. Whether it would have the strength to take out recent highs is unclear, but a correction to the upside not only seems unexpected by most market participants, but it seems plausible based on the weekend news coming out of Greece.

Monday morning the Greek government is set to determine if they will agree to the demands of the Troika in exchange for the next tranche of bailout funds. If the Greek government and the Troika do not come to an agreement, the Euro could sell-off violently.

Additionally there are already concerns about the next LTRO offering from the European Central Bank. The measure is to help provide European banks with additional liquidity, but there are growing concerns that the size and scope of the LTRO could have a dramatic impact on the Euro’s valuation against other currencies. Time will tell, but there are certainly catalysts which could help drive the U.S. Dollar higher.

Another potential indicator that the Dollar could see higher prices in coming days was the largely unnoticed bearish price action on Friday of precious metals. Both gold and silver have been on a tear higher over the past several weeks. Both precious metals have surged since the Federal Reserve announced that interest rates would remain near zero on the short end of the curve through 2014.

However, on Friday gold and silver were both under extreme selling pressure. The move did not get much attention by the financial media. The price action in gold and silver on Friday could be another indication that the U.S. Dollar is set to rally. The daily chart of gold is shown below.

Gold Futures Daily Chart

Obviously the reversal on Friday in gold futures was sharp. The move represented nearly a 2% decline for the session on the price of gold. However, as long term readers know I am a gold bull. I just do not see how gold and silver do not rally in the intermediate to longer term based on the insane levels of fiat currency printing going on at all of the major central banks around the world. The macro case for gold is very strong, but the short term time frame could reveal a brief pullback.

At this point, I suspect a pullback will present a good buying opportunity for those that are patient. However, I think it is critical to point out that this move in gold on Friday could be a signal that the U.S. Dollar is going to find some short to intermediate term strength. If the Dollar does start to push higher, it will likely put downward pressure on risk assets like equities and oil

While Friday’s price action may not mark a top, nearly every indicator that I follow is screaming that stocks are overbought across all time frames. Pair that with the Greece uncertainty and LTRO considerations and suddenly the Dollar starts to look a bit more attractive. Ultimately I am not going to try to pick a top, but the evidence suggests that it might not be too many days/weeks away.

By: Chris Vermeulen – Free Weekly ETF Reports & Analysis: www.GoldAndOilGuy.com

Co-Author: JW Jones – Free Weekly Options Reports & Analysis: www.Optionnacci.com

Nobody really expects Greece to default on its debt and leave the eurozone. But Greek leaders do seem to be squeezing as much drama as possible from the bailout process:

Euro zone loses patience with Greece

(Reuters) – Euro zone finance ministers told Greece on Saturday it could not go ahead with an agreed deal to restructure privately-held debt until it guaranteed it would implement reforms needed to secure a second financing package from the euro zone and the IMF.

Euro zone ministers had hoped to meet on Monday to finalize the second Greek bailout, which has to be in place by mid-March if Athens is to avoid a chaotic default. But the meeting was postponed because of Greek reluctance to commit to reforms.

Instead, the ministers held a conference call on Saturday to take stock of progress on the second financing package, which euro zone leaders set at 130 billion euros back in October.

“There was a very clear message that was conveyed from all participants of the teleconference … to the Greeks that enough is enough,” one euro zone official said. “There is a great sense of frustration that they are dragging their feet.

“They should get their act together and start talking honestly, decisively and speedily with the Troika on the aspects of the programme that remain to be finalized – on fiscal and labor market reforms,” the official said.

The Troika are the representatives of the European Commission, the European Central Bank and the International Monetary Fund, who have prepared a Greek debt sustainability analysis on which the second financing programme will be based. “The main issue is the lack of reform, or prior action, in Greece,” a second euro zone official said.

Euro zone ministers were also dissatisfied with Greek Finance Minister Evangelos Venizelos because they believed the minister was paying more attention to his position within his party ahead of the April elections, than to talks about reforms.

“There is a great sense of frustration with Minister Venizelos, who is very hard to get hold of because he is very busy campaigning for the leadership of (the Greek party) PASOK, so he is not available to meet with Troika members,” the first official said.

“He is preparing his own political future, rather than the future of his country. People are seriously disgruntled about that and have conveyed this very clearly to him this afternoon,” the official said.

Recordings of these conference calls would be instant YouTube hits.

And with all the threats flying around you’d think that Greece would have long since been cowed into submission and forced to accept German control over its budget in return for credit it needs to cover its short-term debts. That they’re holding out implies that they’re really not that worried and believe they can get better terms, which in this case means smaller cuts in domestic spending, less of a decline in local wages, and more cash from the ECB. They’re probably right.

Over the past few months major brokerage houses have been churning out reports on what would happen if Greece or another eurozone country leaves the currency union and reverts to its old money. And without exception the predictions are apocalyptic. Here’s a general scenario:

Greece can’t come to terms with the IMF, ECB, Germany, et al, and announces that it’s leaving the euro and returning to the drachma. Instantly, everyone with a Greek bank account empties it and moves the proceeds out of the country. Greek banks close, oil imports stop, the national health ministry runs out of pharmaceuticals, etc., etc. Chaos leads to depression and, probably, to some sort of authoritarian government.

So far, this sounds like Greece’s problem, and a damn good reason to accept a bailout on pretty much any terms. But what happens next changes everything. The minute Greece announces that it’s leaving, investors instantly start looking around for the next domino, decide that pretty much all the PIIGS countries qualify, and pull money out of their banks, causing them to collapse and sending those economies into free-fall.

Then, since French and German banks have lent hundreds of billions of euros to those now-bankrupt countries, and are on the hook for untold trillions of credit default and currency swaps, they fail as well. The entire continent is plunged into chaos, with no obvious exit. The eurozone dissolves, all because one tiny country decides to leave.

Greece, of course, has read these reports and understands its own power — and knows that Europe’s leaders understand it too. So the Greek finance minister spending his time campaigning rather than waiting by the phone for yet another conference call should be seen as a classic bargaining tactic. Like George Bush Sr. going on vacation as the first Gulf War ramped up, he’s saying that he’s not worried, that this is the other guy’s problem and that by the time he gets back to the office the other guy should have some nice answers waiting.

Given the stakes, expect a deal more to Greece’s liking next week.

Enter Portugal

But of course a Greek deal is the beginning, not the end. Before the signatures dry, Portugal will demand the same bailout, using the same end-of-the-world scenario as its bargaining chip. It will get what it wants, and then Ireland will step up to the table.

In the end, so runs the analyst consensus, the only alternative will be a “fiscal union” where Germany and a handful of other core countries assume the debts of the periphery, in the same way that Washington absorbed Fannie Mae and Freddie Mac’s $5 trillion of mortgage paper. The ECB meanwhile, will have no choice but to finance the whole mess by buying ten or so trillion euros of low-grade paper with newly-created currency.

The euro will fall versus the dollar, yen and yuan, which will be great for German exports and Greek tourism, but bad for the eurozone’s trading partners. They’ll respond with inflation of their own, and so on, as the currency war really gets going. In this scenario it’s hard to see an upside limit for gold and silver.

DollarCollapse.com is managed by John Rubino, co-author, with GoldMoney’s James Turk, of The Collapse of the Dollar and How to Profit From It (Doubleday, 2007), and author of Clean Money: Picking Winners in the Green-Tech Boom (Wiley, 2008), How to Profit from the Coming Real Estate Bust (Rodale, 2003) and Main Street, Not Wall Street (Morrow, 1998). After earning a Finance MBA from New York University, he spent the 1980s on Wall Street, as a Eurodollar trader, equity analyst and junk bond analyst. During the 1990s he was a featured columnist with TheStreet.com and a frequent contributor to Individual Investor, Online Investor, and Consumers Digest, among many other publications. He currently writes for CFA Magazine.

Today we find out just how seasonal those 200,000 new jobs were in December 2011. Consensus is for employment to grow by 140,000 — about par with population growth. Unemployment is expected to be unchanged at 8.5%.

As I am so fond of writing, no single month’s NFP matters all that much — focus on the overall trend to see what is significant. By way of the two charts below, the major overall trends have been improving. New Jobless claims have been ticking downwards since May of 2011. (Benchmark updates could be significant also).

We have seen a variety of retail sales disappointments — notably, Amazon.com (AMZN) and Ambercrombie & Fitch (ANF). Without more hiring and wage gains, higher consumer spending is going to be a difficult challenge to meet.

From a trading perspective, weakness would be problematic. With earnings slowing, the aforementioned soft retail, and the markets as overbought as they have been in a few months, the bulls don’t really need a weak number today.

From an investing standpoint, the outliers are where the risks lay: Too strong number (rather unexpected) might increase pressure on the Fed to end Operation twist and postpone QE3. A too weak number raises the possibility of a recession — currently thought of as not likely amongst most economists. A few observers — ECRI, Hussman, Rosenberg, Shilling, Faber, Rogers — think a recession is highly likely (For the record, I am still at 50-60% chance of recession, but willing to take that lower if the mixed data improves).

Hence, your reaction to today’s numbers should be a function of your positioning, holdings, timeline, and your risk management.

Employment situation report released at 8:30am

About Barry Ritholtz of the Big Picture

Barry L. Ritholtz is one of the few strategists who saw the the coming housing implosion and derivative mess far in advance. Ritholtz issued warnings about the market collapse and recession in time for his clients and readers to seek safe harbor.

Dow Jones Market Talk noted that “many market observers predict tops and bottoms, but few successfully get their timing right. Jeremy Grantham and Barry Ritholtz sit in the latter category…” For the prescience of his market calls in 2009, he was named Yahoo Tech Ticker’s Guest of the Year. (A summary of major market calls can be found here) His observations are unique in that they are the result of both quantitative data AND behavioral economics.

In 2010, Barry L. Ritholtz was named one of the “15 Most Important Economic Journalists” in the United States. Ritholtz writes a column on Investing for The Washington Post (His WaPo columns are here); he also contributes occasional column to Barron’s and Bloomberg (See The Myth of Uncertainty). Previously, he authored the popular “Apprenticed Investor” columns at TheStreet.com, a series geared towards educating novice and intermediate investors. Mr. Ritholtz has published more formal market analyses at Wall Street Journal, Barron’s, The Economist, and RealMoney.com.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair