The U.S. Bureau of Labor Statistics September Non-farm Payroll Report missed expectations as only 148,000 net new jobs were created in the U.S. compared to 180,000 which was anticipated by economists.

The fact that both U.S. job growth and economic growth is sluggish is old news by now. However, it is interesting to compare this against the narrative earlier in the year which suggested that the U.S. was beginning to accelerate out of its doldrums. The fact that we still hovering around “stall speed” speaks to how eager the investment industry is to embrace hope before increased growth in the recovery is actually confirmed.

However, with this miss, the Fed Chairman Nominee Janet Yellen has another reason to maintain the current rate of money-printing via Quantitative Easing (QE). We are almost back to where we started before the implementation of QE3 in September of last year when the market was cheering poor economic statistics in that they would increase chances for stimulus which would bolster investment prices.

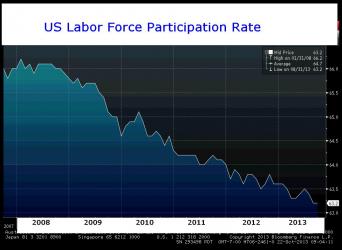

There is a growing and a nagging issue for Dr. Yellen though. The employment numbers of the last few years when contrasted against the mind-boggling magnitude of QE clearly question the efficacy of the policy. And, the September Non-farm Payroll report reaffirms that problem. Not only is job creation still below what we would normally expect in a garden-variety economic recovery, but the participation rate is still at Jimmy Carter Administration levels as it remained stuck at 63.2% from August to September.

So, is bad news good news? To the extent it prolongs QE and maintains a floor under equity prices it is. Beyond that, in the longer-term bad news is … bad news.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results.

Richardson GMP Limited, Member Canadian Investor Protection Fund.

Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.