Jim Rogers has been bullish on agriculture for years now. He stated during an interview with the Economic Times in 2009:

Ten years from now, it may be farmers who will drive the Lamborghinis and the stock brokers will drive tractors or taxis at best.

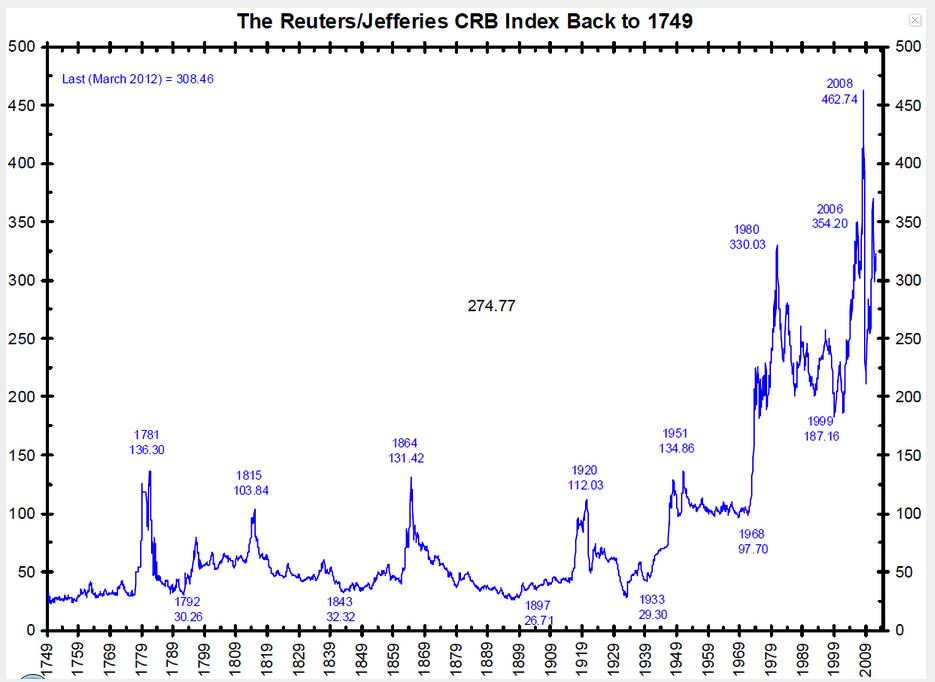

In order to get into his mind, one first needs to understand the mechanisms driving the commodities market, which is really the “real assets” market that includes agriculture, a very long term chart is in order. Here s one of the CRB interpolated from 1749 to the present.

….click HERE to enlarge this chart and read the rest of this detailed Historical article.

What’s happening here needs a bit of explanation. It would seem, from 1749 until 1968, the general nature of real asset prices is that they skirt along their floor with periodic spikes. We have long periods of stable prices from 1749-1779, 1789-1812, 1816-1861, and 1870-1914. After 1914 until 1952 things start going a little haywire, and the final stable period is between 1955 or so until 1968. After that, there is no longer such a thing is commodity price stability. Forget it.

If we look at the spikes and remember what was going on during those times, things start to make some sense. 1781 was the peak of the Revolutionary War Continental Dollar printing. 1815 marked the end of the War of 1812, marred by periodic national suspensions of specie payments for paper dollars, allowing banks to inflate the paper money supply during that time to finance the war. 1864 was, obviously, the Civil War, again financed by paper money called Greenbacks, America’s first relatively long experiment in fiat money. 1914-1920 is the World War I money printing, but more importantly, the founding of the Federal Reserve System which centralizes the money printing business and perhaps causes the Great Depression, among other things. In 1933, with commodities bottoming out, FDR confiscates all gold in the country and devalues it, enabling the Fed to print even more and inflate asset prices. World War II and the Korean War push up prices further, but the international link of the dollar to gold is still alive.

In 1968, it breaks down. With the Nixon administration printing dollars to finance the Vietnam War, foreigners begin cashing them in for gold. To stop a gold run, Nixon tries to create a fake gold market between central banks and ignore the free gold market everywhere else. This was called the “two tier gold market” that lasted from 1968 until 1971. After that, it was over. The dollar lost all definition, and real asset prices haven’t even had a short period of stability since then.

So we see, during periods of massive money printing, real asset prices always go up. The reason they go back down afterwards is that periods of money printing have historically been followed by periods of deflation, but this was only because, throughout the centuries, the dollar-gold anchor was always eventually restored. This time it doesn’t exist. This time, real asset prices will just keep going up in dollar terms.

Be that as it may, the reason Jim Rogers likes to focus on agriculture is that the statistics with agriculture are surprisingly shocking. According to the National Crime Records Bureau [NCRB], there were 17,368 Indian farmer suicides in 2009 alone. While farming may not have been the sole cause that attributes to such a sad statistic, the fact is that agriculture has been a horrible business for decades. It is not my intention to sound gloomy about this, but when one considers the cost of seeds and the labor involved, many farmers are literally working themselves to financial death because they simply can’t make a living. Additionally, with the average age of a farmer at 55, the supply of farmers is going down. They are getting older with few young replacements. And if this trend continues, we may not have enough food to go around and prices are going to have to rise higher than they are already.

Rogers, to my knowledge, is not long agricultural or commodity stocks, but rather commodities themselves. He’s said this before about gold miners, which he does not invest in. It stands to reason he would not be long agricultural stocks either. It’s Wall Street Trends 101 that says that stocks and commodities bull markets run inversely. However, this is true mainly for consumer goods industries rather than capital goods industries. For example, when wheat is expensive, so goes the theory, General Mills’ (GIS) profit margins on its cereals will tend to contract, and the company will lose revenue. For capital goods stocks however, it stands to reason that companies supplying the agriculture industry, rather than retailing off of it, will boom along with agricultural prices. So, for example, Deere and Company (DE) will sell more farm equipment to farmers who will make more money when agricultural commodities start getting more expensive.

Despite the logic of this theory, one needs to have quite a strong stomach to be long capital goods industries at this time. If you thought being long the general market was tough in 2008, take a look at a comparison graph between DE and SPY.

…click HERE to enlarge this chart and read the rest of this detailed Historical article.

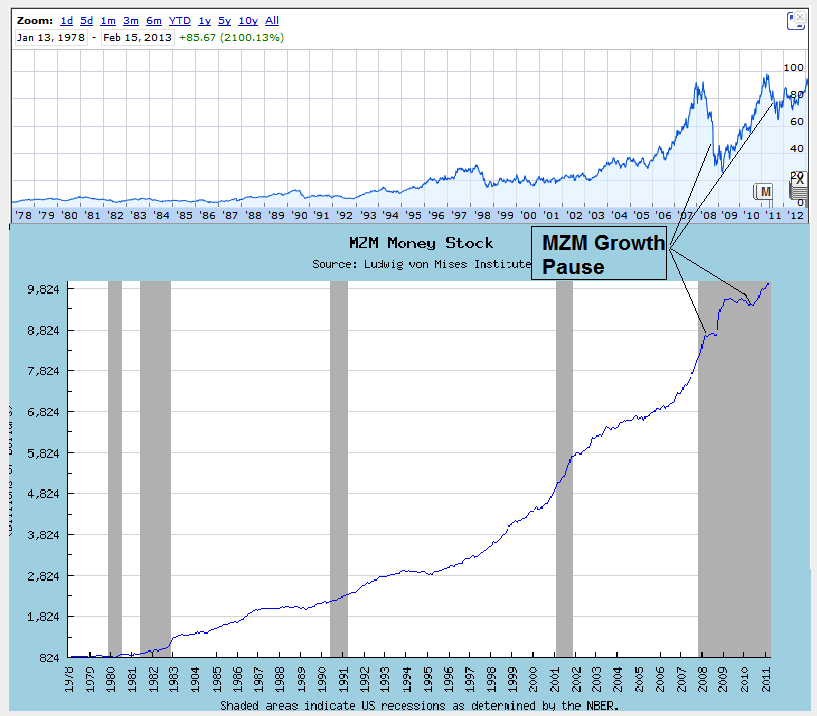

This extreme volatility can be correlated to the liquid money supply [MZM] fluctuations. Take a look at the long term chart of DE compared to the MZM, or liquid money supply in the economy along the same time period.

…click HERE to enlarge this chart and read the rest of this detailed Historical article.

Since Deere is at the very top of the structure of production, meaning capital goods as opposed to consumer goods which are at the bottom, liquid money supply moves to the top first, as interest rates are pushed down and long term investment projects are taken up, which require capital goods first and foremost. The problem is, once the Fed stops printing even for a few months after a long stretch of MZM increases, the boom cannot be sustained, and capital goods stocks fall rapidly. At the beginning of 2008, MZM growth clearly flat-lined for close to a year after a huge burst of growth starting in 1995 from $2.8T to nearly $8.8T, an increase of 214% in 13 years. With all the money from capital goods industries being supplied by the Fed suddenly drying up in 2008, the bubble deflated fast. Then the printing presses were fired up once again, and it resumed. As long as the Fed continues, holders of Deere and companies at the forefront of the structure of production will keep being first in line to receive the new Fed money. The minute he stops, DE shareholders will suffer.

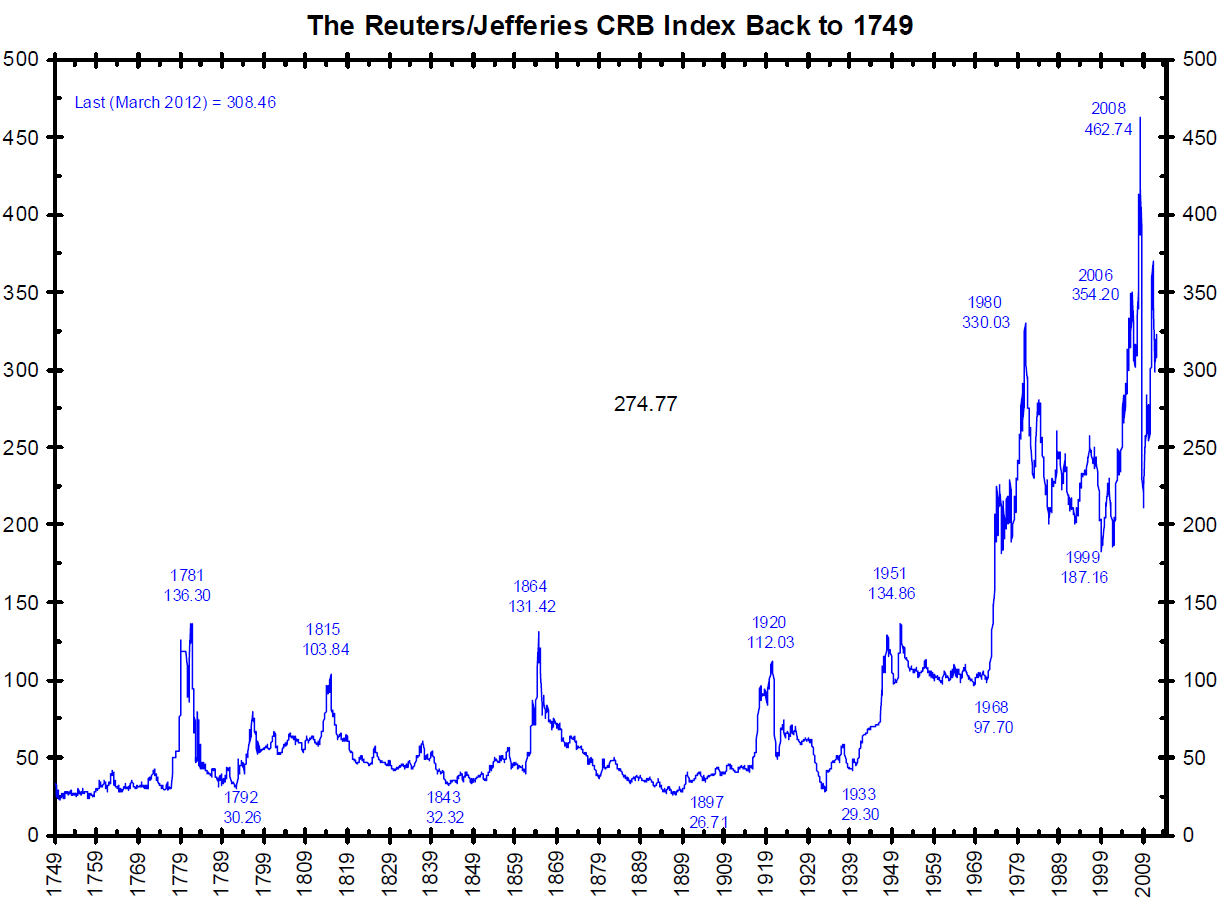

But this is not investing. This is just playing a game of chicken with the Fed. If you want to do it, go ahead. I’m not touching it with a ten foot pole. Instead of stocks like Deere, the safest way to play the agriculture game besides investing in farmland straight-up is agriculture futures ETF’s like DBA or, in honor of Rogers, RJA, an ETN that replicates the performance of the Rogers International Commodities Index. These are not for trading. Just look at the tail end of the 1749-present graph of the CRB. Don’t even try. They are for buying and waiting while shielding oneself from price inflation. We have seen that from 1749 until today, every time the government prints money, commodities skyrocket. It used to only be during war time. Now it’s just constant. It is heads you win, tails you win. Either the global economy will pick up, in which case there will be shortages and commodities will rise, or they will print money, in which case commodities will rise. This is already reaching epidemic proportions, as reports are multiplying now about the G20 “denying currency wars” meaning, money printing competitions. When all governments deny it, that’s when we know it’s definitely happening.

There may be one more way to play this, but only with leftover cash, nothing big. During my search, I came across a microcap that may have the business idea to benefit from real asset gains in agriculture while avoiding the gyrations of printing press manipulation at the capital goods level. Terra Tech Corp.,(TRTC.OB) is attacking a new niche, urban farmers, basically connecting capital goods directly with end consumers and “sowing together” the beginning and end phases of the structure of production. These are horticulturists who live in the city or suburbs and want to grow their own food and gain independence from Big Ag. Terra Tech has been expanding recently, thinning its already thin balance sheet and hammering its stock price, which already comes with fairly large speculative dangers. But when agriculture prices do start to climb, this market will inevitably expand as people may try to save money by growing food at home, which will save massively on transportation costs and increase supply.

In New York City for example, a new trend is slowly spreading where tenants grow food on their roofs and balconies, and Terra Tech sells the hardware for this. When farmers get richer and demand for MBA’s dwindles, people in urban areas are going to start flocking to farms. Urban areas are pretty crowded, but they are seriously lacking in food, which is almost all imported.

Only time will tell if Terra has the right idea. The next few quarters will be crucial, and will show if it can grow its revenues, which only started flowing in at the beginning of last year.

About Tal Ben-Ami

Holds an MBA in economics from TAU – Doctoral student.

{kind=link}