All attention is once again on Janet Yellen and the Federal Reserve this week, as the FOMC meets to determine whether an interest rate hike is warranted.

At this point, with Fed Funds futures prices pointing toward a 95% chance of a rate hike, an increase to the federal funds rate is a near certainty. But the implications and consequences of a rate hike are less so. Let’s dig into that further.

One thing I’ve noticed in speaking to investors is that there is often an inclination to group all interest rates together. When they hear about the Fed “raising rates,” many assume that interest rates across the board, for nearly everything, will rise. This couldn’t be further from the truth and warrants more explanation.

Interest rates come in all shapes, sizes and most importantly, maturities. That is, the length of the term over which money is borrowed, and therefore accrues interest.

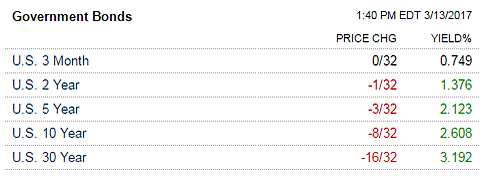

Take US Treasuries as an example. If you want to loan the US government money, they’ll pay you a different interest rate based on the term of the loan. You can see today’s pricing for a few select maturities in the table below:

If we take these maturities and their respective interest rates and plot them on a chart, we end up with what’s known as the yield curve. You can see this as the red line in the chart below.

The yield curve contains an immense amount of information about the health of an economy. Watching how it behaves over time is one of the best indicators of upcoming economic performance that we have.

Now let’s get back to our original question: what’s going to happen on Wednesday when the Fed hikes rates by a quarter point?

While most people have a tendency to see the Federal Reserve as masters of the universe, the truth is that they have less control than most people think. When the Fed raises and lowers interest rates, they are only changing the rate at which depository institutions (banks and credit unions) lend to each other on an overnight basis.

Since there’s a good chance that neither you or I represent depository institutions, what does this mean for us? Asked differently, how will depository institutions change their debt pricing as a result of the increase in their overnight rate?

When the federal funds rate increases, as it likely will on Wednesday, there is an immediate impact to certain types of adjustable-rate debt. Banks are quick to pass along this additional cost to consumers, and we typically see this in the form of a higher prime rate.

The prime rate is a key benchmark rate and represents the rate at which commercial banks lend to their least-risky customers. While each bank sets their own prime rate, the average consistently sits 3% above the federal funds rate. Therefore, any adjustable rate loans tied to the prime rate will see an increase by roughly the same amount that the Fed raises rates.

An increase in the Federal Funds rates also impacts LIBOR – the London Interbank Offered Rate – another key benchmark to which much adjustable-rate debt is tied. LIBOR is considered one of the most influential benchmark rates in the world and represents the rate banks charge each other for Eurodollars (US dollar-denominated deposits at foreign banks) on the London interbank market.

The relationship between LIBOR and the Federal Funds rate is not as direct as with Prime, but LIBOR also has a strong tendency to track the Federal Funds rate and usually rises when the Fed hikes rates.

This means that almost immediately after a Fed rate hike, many adjustable rate debts begin to accrue interest at a faster rate. As you can imagine, this forces more resources to be applied to debt servicing, leaving less for consumption, investment etc.

The net result of this is a minor slowing of the economy, which is exactly the Federal Reserve’s intention.

But interestingly, there is a feedback mechanism in place in which higher rates can actually beget lower rates, albeit for different types (and maturities) of debt.

Taking another look at our yield curve, many people adopt the simplistic view that if rates at the short end of the curve rise (the federal funds rate), it means that interest rates across all maturities will rise. This is simply not the case, and understanding why is critical to understanding the immense predictive power of the yield curve.

As mentioned earlier, when the Fed raises or lowers rates, it is only changing the rate at which banks lend to each other on an overnight basis. As we extend out in maturity, we find that the Fed’s control over rates is relinquished to that of the market.

Let’s use the 10-year Treasury note as an example. When borrowing or lending money for 10-year periods, do you really care what the overnight rate that banks lend money to one another is? Probably not. In this case, there’s a good chance you care more about things like oh, say, future economic performance and inflation, right?

Now consider this: When the Fed hikes rates, we just saw that it has an immediate impact on debt servicing costs for adjustable rate debt tied to prime and LIBOR. As we discussed earlier, this means fewer resources are available for consumption and investment, which implies a minor restraint to economic growth.

Since economic growth and inflation go hand in hand, a Fed rate hike actually works to quell rising inflation (one of its main purposes). And this, interestingly enough, can cause longer-term interest rates to fall.

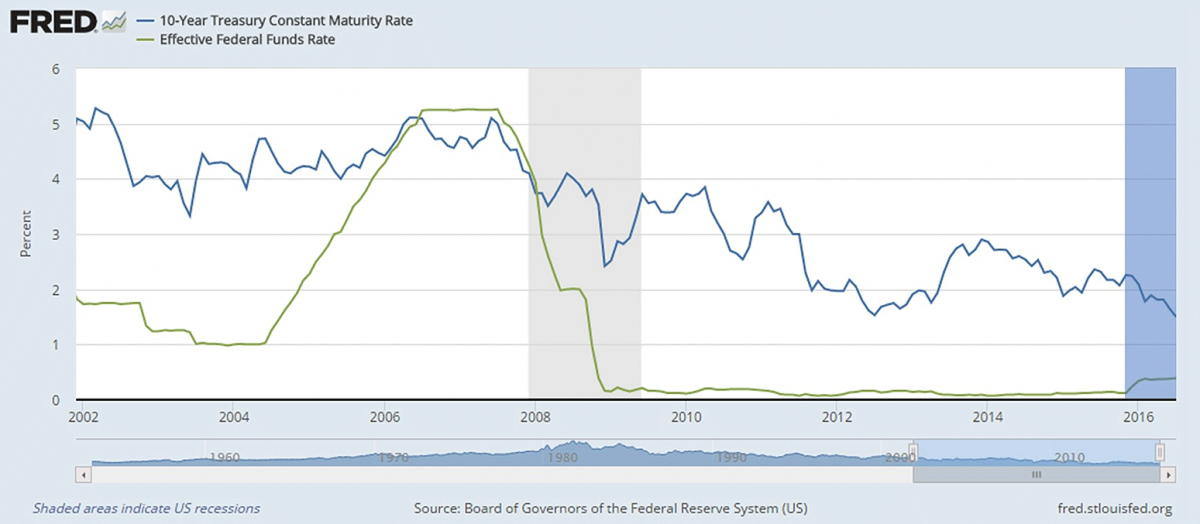

This is exactly what we saw after the Fed’s first rate hike back in December of 2015. Notice in the chart below that following the Fed’s rate hike (green line) the yield on the 10-year Treasury went down, rather than up.

Since mortgages and other types of long-term debt tend to be priced off of the 10-year note, this means that some borrowers actually saw a reduction in interest rates following the Fed’s first hike.

But a lot has changed since then. In the roughly five quarters since we saw the first rate hike, the 10-year note yield has gone from 1.5% to 2.6%. And during that time period, the Fed only raised rates by a quarter point…

We can see how this has played out in the chart of the yield curve below. This time, I’ve included black lines that show how the yield curve has shifted from its previous state.

Due to an improved economic outlook and the prospect of higher inflation, the long end of the yield curve (right side) has moved up substantially, while the left side (where the Fed exerts control) has remained relatively anchored. The result has been a steepening of the slope of the yield curve, which indicates a healthy economy that is capable of handling higher short-term interest rates.

This is one of the primary reasons that the market is both expecting a rate hike, and at the same time, we’re not seeing a sharp negative reaction in equity markets. This time around, the long-end of the yield curve has been leading the way higher, rather than the other way around.

In our current interest rate environment, the Fed has room to raise rates a few times without worrying about drastically flattening the slope of the yield curve. This is a good sign and suggests that investors will take Wednesday’s rate hike in stride, viewing it as another signal of an improving economy.

While higher interest rates and particularly an upward ratcheting federal funds rate have historically swung the pendulum too far, eventually throwing the economy into recession, that time is not now. For at least the short, foreseeable future, higher interest rates can go hand in hand with an improving economy.

The preceding content was an excerpt from Dow Theory Letters. To receive their daily updates and research, click here to subscribe.

….also: Hear Craig Johnson on Stocks, Bonds; Frank Holmes on Gold, Oil

Hear also Jim O’Sullivan on US Economy, Fed Rate Hikes, Market Outlook