In the last eLetter (July 7) we noted that gold’s daily chart pattern target was higher, at around 1400 and that silver had already achieved its daily pattern target of 20. From that eLetter…

“This momentum looks like a profit taking opportunity (profit taking is always a good thing and you do not owe any gold bug, miner or tout your allegiance) in progress for traders and those who want to lock in gains. But what happened last week rammed home some important technical confirmations as well.”

The sector then began to ease as it turned out to be a good opportunity for those who would take profits to do so. But the situation is complex, as only a minor pullback has taken place, risk is high but up trends are firmly intact (I personally believe there is a slightly better than even chance that new highs can be seen in the short-term).

This week’s NFTRH 404 has two main themes; the first to further detail the short, intermediate and long-term implications of last week’s bullish ‘Breadth Thrust’ in the US stock market (see the initial public post this subject: Breadth Thrust: Prelude to a Crash?) and the second to illustrate some building negatives to the first phase of gold’s new bull market. Following is a small portion of the gold analysis.

Please understand that the report contains much more information about the gold sector, the broad markets and the economy that I consider important in rational decision making. But since interest rates have been front and center lately, I thought this clip would work well for the eLetter.

<begin excerpt>

…perceptions are firming about “the new gold bull market” and this is with good reason as the bullish phase that appears to be engaging across financial markets all began as a twinkle in gold’s eye in January. Remember then? Not even silver had woken up. Gold and fellow ‘defensives’ like Treasury bonds and Utilities turned up as max angst enveloped the world’s markets.

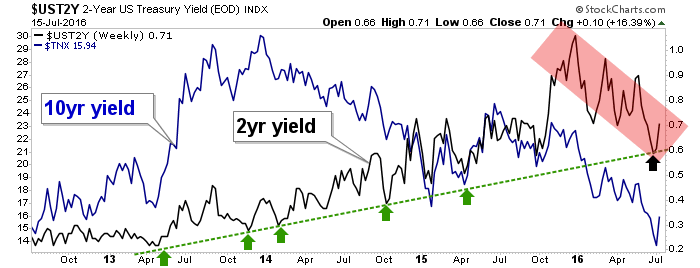

So therein lies part of the issue for gold. At some point, if the tide shifts from risk ‘off’ (Brexit is only a couple weeks behind us, after all) to risk ‘on’, all of these havens would likely get hit with the ugly stick. What’s more, if interest rates improbably (though not to us) start to rise and the yield curve fails to do the right thing, gold would be vulnerable. Again, the state of short-term and long-term US Treasury yields…

The rise in short-term yields was a bad thing for gold until 2016, which has seen an intermediate downtrend in yields. It was no coincidence that gold turned up with this.

But the trend line was hit and now the 2’s are bouncing. This would all be fine if the 10’s bounce harder, because the signal would be inflationary, which as we have reviewed, certainly fits one of gold’s utilities as inflation protection. That condition would be indicated by a rising yield curve and rising inflation expectations. The curve is not rising.

We have been working on a theme that sees a new inflation cycle in the making. The most exciting development there has been silver’s recent explosive up move in relation to gold. That has proven to be a precursor to the big upward bounce in US and global markets, which makes sense because one of Silver-Gold’s functions is to indicate risk ‘on’ vs. risk ‘off’. Job well done Silver-Gold ratio.

But as was the case through much of the post-2009 stock market bull, inflation expectations are depressed. From the rolling anxieties of Great Britain’s departure from the EU, to various terror and violent political events unfolding in what seems like routine fashion, you understand why market participants have not felt in a speculative mood, which is one prominent aspect of an inflation cycle and associated ‘inflation trade’.

But this does not mean risk is ‘off’ and gold favorable; not with the Silver-Gold signal and broad relief centering in equities. Indeed, we can continue to anticipate an inflationary phase as the 10 year b/e potentially makes a right side shoulder to an Inverted H&S, as we have speculated may come about.

But until inflation signals start to become a concern for a majority of participants there is a window for gold, silver and commodities to under perform in the near-term.

…related: